- Automotive Components & Materials

- Automotive Engine Management System (EMS) Market

Automotive Engine Management System (EMS) Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Engine Management System (EMS) Market By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Others), Component (Engine Control Units (ECUs), Sensors, Fuel Pumps, Others), and Regional Analysis for 2025 - 2032

Automotive Engine Management System (EMS) Market Share and Trends Analysis

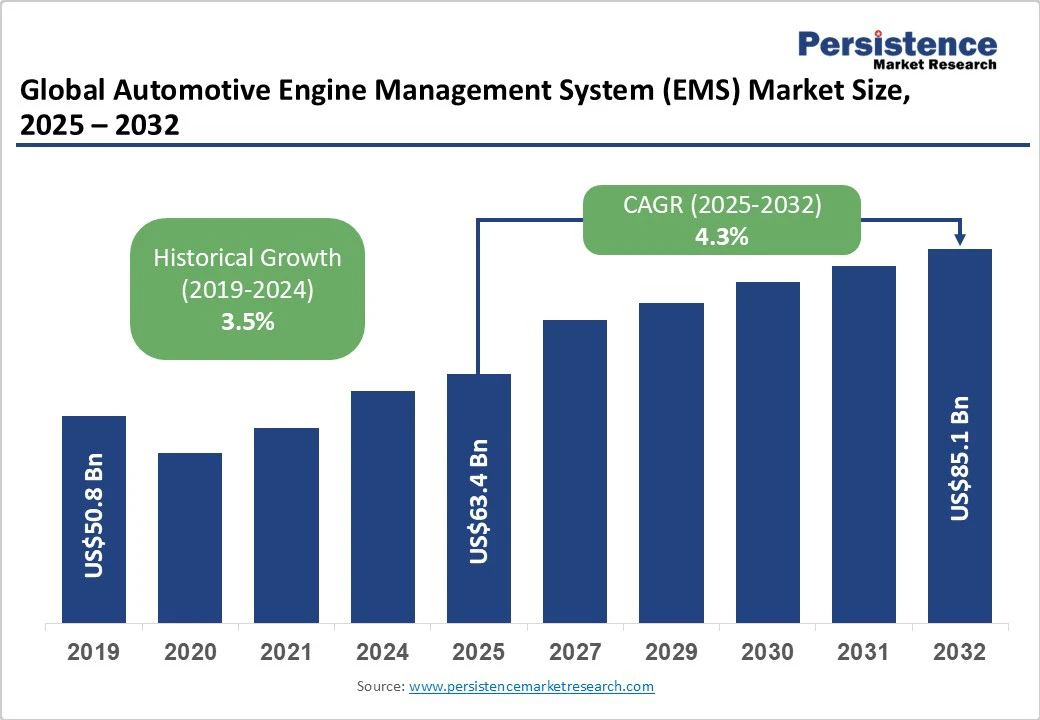

The global automotive engine management system (EMS) market is expected to be valued at US$63.4 billion by 2025. It is estimated to reach US$85.1 billion by 2032, growing at a CAGR of 4.3% during the forecast period 2025-2032, driven mainly by the integration of advanced electronic control systems and regulatory mandates targeting emission reductions. The market expansion is attributed to the strong demand for passenger vehicles and the growing adoption of gasoline engine management systems.

Technological advancements such as AI-enhanced engine control units and sensor innovations are improving fuel efficiency and reducing emissions. Additionally, increasing consumer demand for enhanced vehicle performance and tightening global environmental standards are significant catalysts influencing market growth.

Key Industry Highlights

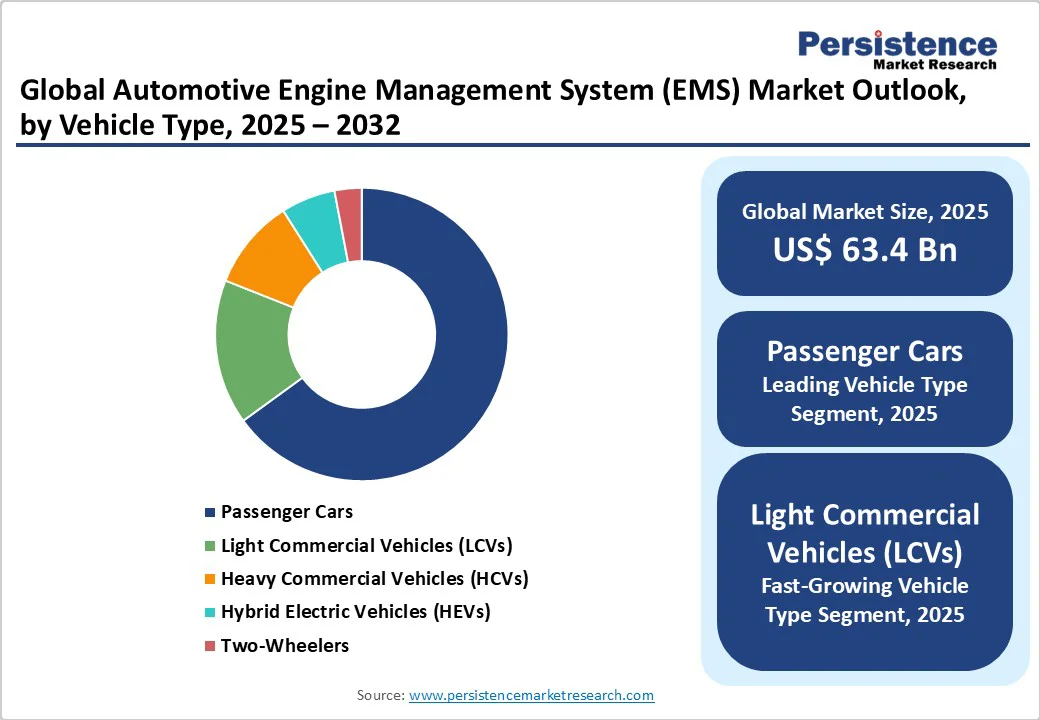

- Dominant & Fastest-growing Vehicle Types: Passenger cars hold the largest market share, estimated at 65.0% in 2025; light commercial vehicles are expanding the fastest, at a CAGR of 5.6% through 2032.

- Leading & Fastest-growing Engine Types: Gasoline engine management systems lead with a 58% share in 2025, while hybrid engine EMS solutions are the fastest-growing, with a forecasted CAGR of 7.8% from 2025 to 2032.

- Dominant & Fastest-growing Components: Engine control units dominate the components market with a 60.0% share in 2025, whereas sensor technologies are the fastest-growing subset, growing at a 6.3% CAGR during 2025-2032.

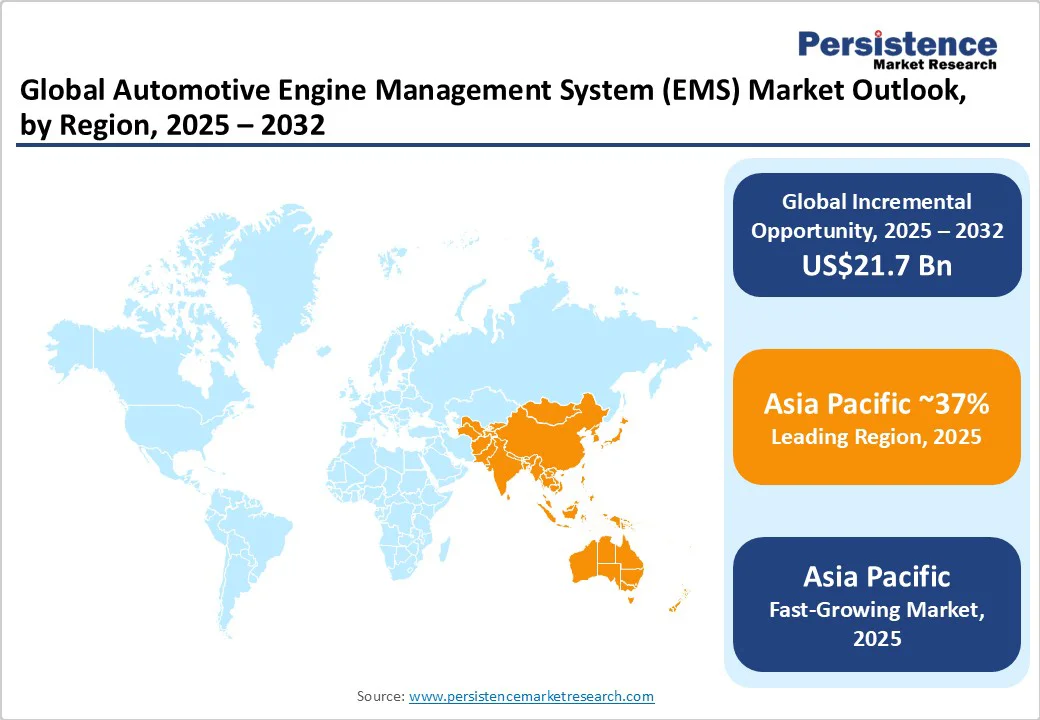

- Leading Region & Fastest-growing Regional Market: The Asia Pacific represents the largest regional market, with a 37.0% share and a forecast CAGR of 6.5%, driven by regulatory reforms in China and India for vehicles.

- August 2025: At the Austrian Grand Prix, MotoGP introduced a stability control system that reduces engine torque to help prevent slides and enhance rider safety, differing from traction control, which addresses tire spin.

|

Key Insights |

Details |

|

Automotive Engine Management System (EMS) Market Size (2025E) |

US$63.4 Bn |

|

Market Value Forecast (2032F) |

US$85.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Stringent Emission Regulations and Advancements in Engine Control Systems

Governments worldwide are imposing increasingly stringent emission standards that directly influence automotive EMS. Regulations such as the Euro 6/VI in Europe, the Corporate Average Fuel Economy (CAFE) standards in the U.S., and Bharat Stage VI in India mandate substantial reductions in NOx, CO2, and particulate matter emissions. According to the International Energy Agency (IEA), passenger cars equipped with advanced EMS technology can reduce fuel consumption by up to 15.0%, contributing significantly to emission compliance. Engine management systems precisely control fuel injection, ignition timing, and air-fuel ratios, which are critical to achieving these reductions. Regulatory frameworks are expected to tighten further by 2030, maintaining strong growth momentum for EMS components and associated technologies.

The integration of artificial intelligence (AI), machine learning (ML), and IoT technologies is revolutionizing the automotive engine management system market landscape. Advanced engine control units now utilize real-time data processing to dynamically optimize engine performance, enabling predictive maintenance and adaptive fuel management. Technological developments are enhancing engine efficiency, lowering emissions, and improving drivability. AI-driven ECUs analyze data from sensors such as oxygen, temperature, and knock sensors to instantly adjust engine parameters, improving fuel efficiency by 10–18%, according to SAE. The future rollout of powered sensors and embedded software solutions is expected to further expand EMS capabilities.

Exorbitant Pricing of Advanced EMS Technologies and Supply Chain Uncertainties

A key restraint is the high cost of advanced engine management systems. Cutting-edge ECUs and multi-sensor arrays require significant R&D and costly materials, resulting in vehicle production costs that increase by 7% to 12% for passenger cars, according to automotive trade data. This poses a challenge in price-sensitive markets, particularly in emerging economies, where affordability is a crucial factor. Further, compliance with evolving regulations extends certification timelines and adds financial strain on OEMs, slowing EMS adoption in cost-competitive segments.

EMS production relies on globally sourced semiconductors and specialized electronics, making it vulnerable to geopolitical tensions and supply chain disruptions. The COVID-19 pandemic and ensuing chip shortages reduced global automotive output by 8%-10% in 2023, according to the Semiconductor Industry Association. These disruptions elevate costs and delay EMS deployment. While OEMs are adopting localized manufacturing and diversified sourcing strategies, these challenges are expected to persist, impacting EMS market growth in the near to medium term.

Increasing Vehicle Ownership in Emerging Economies

Emerging markets such as China, India, and ASEAN countries offer significant growth potential for the automotive engine management system (EMS) market, driven by rising vehicle ownership, improving living standards, and stricter emission regulations. Government incentives promoting cleaner vehicle technologies are further accelerating the adoption of EMS, particularly in the Asia Pacific region. For example, India’s enforcement of BS-VI emission norms in 2025 mandates the use of advanced EMS to ensure compliance and competitiveness. With the regional automotive market projected to grow at over 7% annually, EMS providers have a prime opportunity to deliver cost-effective, regulation-compliant solutions tailored to these markets.

The growing adoption of hybrid electric vehicles (HEVs) is opening a lucrative avenue for EMS vendors. HEVs rely on sophisticated EMS to manage electric power systems, engine start-stop functions, regenerative braking, and fuel optimization. These systems are increasingly vital amid tightening emission norms and rising demand for fuel-efficient vehicles. Policy support for low-emission mobility is expected to drive HEV penetration further, positioning hybrid EMS as a key growth segment. Market forecasts estimate the EMS opportunity in the hybrid segment to reach US$7–9 billion by 2032, underlining the importance of innovation in hybrid-compatible EMS for capturing long-term value in evolving markets.

Category-wise Analysis

Vehicle Type Insights

Passenger cars are expected to continue to dominate the automotive engine management system market, holding an estimated 65.0% revenue share in 2025. This leadership is attributed to the high production volumes of cars worldwide, including growth in emerging economies and stringent emission and fuel efficiency regulations that prioritize passenger vehicles. The increasing implementation of advanced EMS technologies, such as AI-enabled ECUs and multi-sensor configurations, in passenger cars supports stricter regulatory compliance and an enhanced driver experience. Additionally, the consumer shift toward fuel-efficient, technologically advanced personal vehicles is fueling the ongoing demand growth in this segment.

The light commercial vehicle (LCV) segment is forecast to exhibit the fastest CAGR between 2025 and 2032. This rapid growth is underpinned by the expansion in the e-commerce sector and last-mile delivery logistics, which have increased the reliance on LCVs. The demand for fuel-efficient, low-emission engines equipped with advanced EMS to optimize operational costs is escalating in key markets such as India, China, and the U.S. Furthermore, urbanization trends combined with increasing retail convenience preferences encourage fleet modernization, accelerating EMS adoption in commercial transportation.

Engine Type Insights

Gasoline engine management systems lead this segment with an estimated 58.0% of the automotive EMS market share in 2025, favored by consumer preferences and regulatory restrictions that are reducing diesel car production globally. Regulatory policies such as Euro 6/7 in Europe and Bharat Stage VI in India tighten emission controls, impacting diesel engines more considerably and causing original equipment manufacturers (OEMs) to shift focus toward gasoline and hybrid powertrains. Gasoline vehicle EMS benefits from relatively advanced infrastructure and lower cost compared to diesel-focused systems, further supporting market share leadership.

The hybrid engine EMS segment, however, represents the fastest-growing category with a forecast CAGR of about 7.8% for 2025-2032. Hybrid vehicles integrate combustion engines and electric motors, requiring sophisticated EMS to enable seamless engine start-stop capabilities, energy recovery, and optimized fuel consumption. The growing emphasis on reducing vehicular emissions and improving fuel economy through hybridization in mature markets, combined with incentives in developing regions, drives this acceleration. Increasing consumer adoption, driven by environmentally friendly policies and advancements in EMS functionality, supports this dynamic growth trend.

Component Insights

Engine control units (ECUs) are expected to account for approximately 60.0% of the automotive engine management system market revenue share in 2025, due to their critical role in real-time engine monitoring and control, which enables meeting emission and efficiency standards. Technological innovations such as AI-enabled ECUs for predictive maintenance and adaptive fuel management enhance their strategic importance and adoption rates. ECUs serve as the system's brain, integrating data from multiple sensors and making instantaneous adjustments to optimize performance.

Sensor technologies, comprising oxygen, temperature, knock, and position sensors, are forecasted as the fastest-growing component sub-segment with a CAGR of 6.3% from 2025 to 2032. The segment growth is propelled by advancements in sensor precision, reliability, and integration with IoT platforms for richer data analytics. These sensors provide crucial input variables that empower ECUs to execute optimal engine control strategies, thus playing a significant role in emission reduction and fuel efficiency enhancement. Market players are investing in the development of next-generation smart sensors with predictive capabilities, further augmenting this growth trajectory.

Regional Insights

North America Automotive Engine Management System (EMS) Market Trends

In 2025, North America is projected to capture approximately 28.0% of the automotive engine management system market share. The regional market growth is led predominantly by the U.S., which possesses a highly developed automotive sector characterized by advanced technology adoption and well-established regulatory frameworks. Emission reduction policies, such as the California Air Resources Board’s (CARB) stringent standards, incentivize OEMs to implement advanced EMS technologies for compliance and competitive advantage.

The integration of EMS into autonomous and connected vehicle ecosystems is a key driver of growth in North America. The region benefits from strong R&D investments in AI-based engine control and smart sensor technologies. Leading global players are accelerating innovation through regional hubs, boosting technology adoption. Evolving regulations, including anticipated CAFE standard updates, are driving the need for greater fuel efficiency, which further supports EMS market growth. Investment is flowing into scalable EMS solutions for both passenger and commercial vehicles, signaling strong potential for tech-driven expansion.

Europe Automotive Engine Management System (EMS) Market Trends

Europe is expected to hold about 30.0% of the EMS market globally in 2025, supported by key automotive hubs such as Germany, the U.K., France, and Spain. Propelling the market expansion here are the EU’s regulatory harmonization efforts, including the introduction of Euro 7 emission standards, which mandate further reductions in NOx and particulate matter emissions. These increased standards necessitate widespread EMS upgrades and the adoption of cutting-edge fuel management and exhaust gas recirculation technologies. With a forecast CAGR close to 4.0% for 2025-2032, the Europe automotive EMS market is gaining momentum from a strong manufacturing base and a consumer trend favoring fuel-efficient and lower-emission vehicles.

Germany, in particular, leads the way due to its robust industrial capacity and supportive regulatory framework for green mobility. Moreover, the automotive industry in Europe is characterized by a rapid adoption of digital EMS technologies such as predictive diagnostics and sensor fusion. Investment opportunities arise around enhanced sensor development and ECU software update platforms that meet evolving environmental policies and consumer demands for vehicle efficiency.

Asia Pacific Automotive Engine Management System (EMS) Market Trends

The Asia Pacific is likely to dominate the automotive EMS market share, accounting for approximately 37.0% in 2025. Key contributors include China, Japan, India, and ASEAN nations. The regional market is expanding rapidly, with an estimated CAGR of 6.5% from 2025 to 2032, fueled by increasing vehicle production, rising urban population, and tightening regulatory emission norms such as China VI and Bharat Stage VI standards. The growing middle class and government incentives for cleaner technologies are further accelerating the adoption of EMS.

China’s aggressive clean vehicle policies and infrastructure investments enhance market growth prospects, while India’s transition to BS-VI norms drastically increases the need for advanced engine management systems. The competitive advantage in the Asia Pacific lies in cost-efficient manufacturing and the presence of major suppliers of engine management systems and their components, creating an integrated supply chain ecosystem. Investment trends focus on developing scalable EMS units configured for emerging market cost sensitivities, alongside advanced sensors and ECUs designed to meet global emission and fuel efficiency benchmarks.

Competitive Landscape

The global automotive engine management system (EMS) market is moderately consolidated, with top players, including Bosch, Denso, Continental AG, and Delphi Technologies, holding around 65% market share. These leaders leverage strong OEM ties and broad product portfolios. High entry barriers, driven by strict quality standards, technical complexity, and compliance demands, limit new entrants. Competition centers on ECU software innovation, sensor accuracy, and integration. Success depends on delivering tailored, cost-efficient EMS solutions, expanding into emerging markets, and staying ahead of evolving regulations.

Leading EMS market players are embracing innovation-led strategies, focusing on AI and IoT-enabled engine control systems to boost fuel efficiency and reduce emissions. Cost leadership is achieved through scalable manufacturing and strategic partnerships, supporting expansion into emerging markets. Business models are shifting toward EMS-as-a-service platforms, offering remote diagnostics and software updates to drive recurring revenue and enhance customer retention. Key differentiators include high sensor precision, adaptive control algorithms, and strong after-sales support, positioning these companies for long-term, sustainable growth.

Key Industry Developments

- In August 2025, Mahindra introduced new engines and its modular NU-IQ platform, compatible with E30+ ethanol fuel. Equipped with sensors to monitor ethanol content and heaters for better cold starts, the platform supports India’s goal of 30% ethanol blending by 2030. At Auto Expo 2025, Mahindra showcased flex-fuel vehicles alongside other automakers, signaling a strong industry shift toward greener mobility.

- In July 2025, STMicroelectronics agreed to acquire NXP’s MEMS sensor business for US$950 Million to boost its automotive and industrial offerings. The unit, which earned US$300 Million in 2024, includes sensors for safety, engine management, and monitoring. The deal, closing in H1 2026, is expected to be earnings-accretive and will expand ST’s technology portfolio to meet the growing demand of OEMs for safety and automation.

- In April 2025, at Auto Shanghai 2025, Marelli unveiled its ProZone zone control unit, marking a significant step toward its shift to software-defined vehicles. By consolidating systems such as thermal and chassis control into centralized units, the zonal architecture cuts weight, cost, and complexity. Aiming to lead the global zone control unit market by 2026, Marelli offers flexible, upgradeable solutions with integrated AI-driven technologies.

Companies Covered in Automotive Engine Management System (EMS) Market

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Delphi Technologies

- Magneti Marelli S.p.A.

- ZF Friedrichshafen AG

- Valeo SA

- Hitachi Automotive Systems

- Robertshaw Controls

- BorgWarner Inc.

- Aptiv PLC

- Faurecia SE

- Marelli Automotive Lighting

- Mahle GmbH

- Autoliv Inc.

Frequently Asked Questions

The automotive engine management system (EMS) market is projected to reach US$63.4 Billion in 2025.

Increasing consumer demand for enhanced vehicle performance and tightening global environmental standards are driving the automotive engine management system (EMS) market.

The automotive engine management system (EMS) market is poised to witness a CAGR of 4.3% from 2025 to 2032.

Key market opportunities lie in the integration of advanced electronic control systems alongside technological advancements such as AI-powered engine control units and innovative sensor technologies.

Robert Bosch GmbH, Denso Corporation, and Continental AG are some of the key players in the automotive engine management system (EMS) market.