- Automotive Components & Materials

- Automotive Clutch Disc Market

Automotive Clutch Disc Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Clutch Disc Market by Product Type (Organic Clutch Discs, Ceramic Clutch Discs, Metallic Clutch Discs, Sintered Clutch Discs), Transmission Type (Manual Transmission, Automatic Transmission, Semi-Automatic Transmission), Application (Passenger Cars, Commercial Vehicles, Motorcycles, Heavy-Duty Trucks), and Regional Analysis for 2025 - 2032

Automotive Clutch Disc Market Size and Trends Analysis

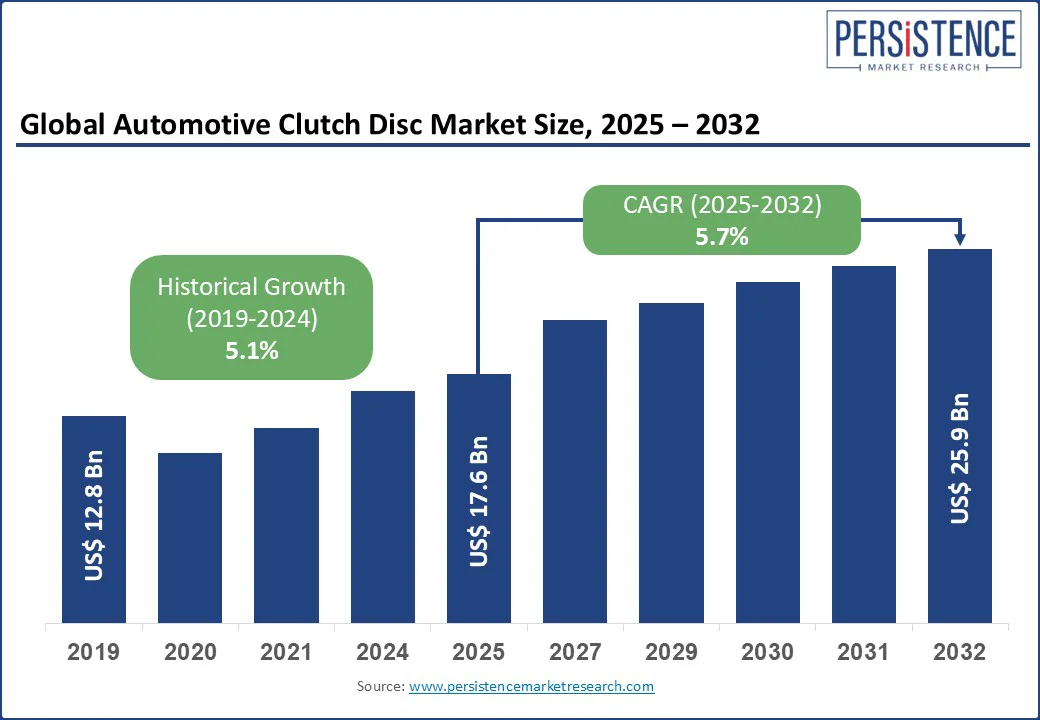

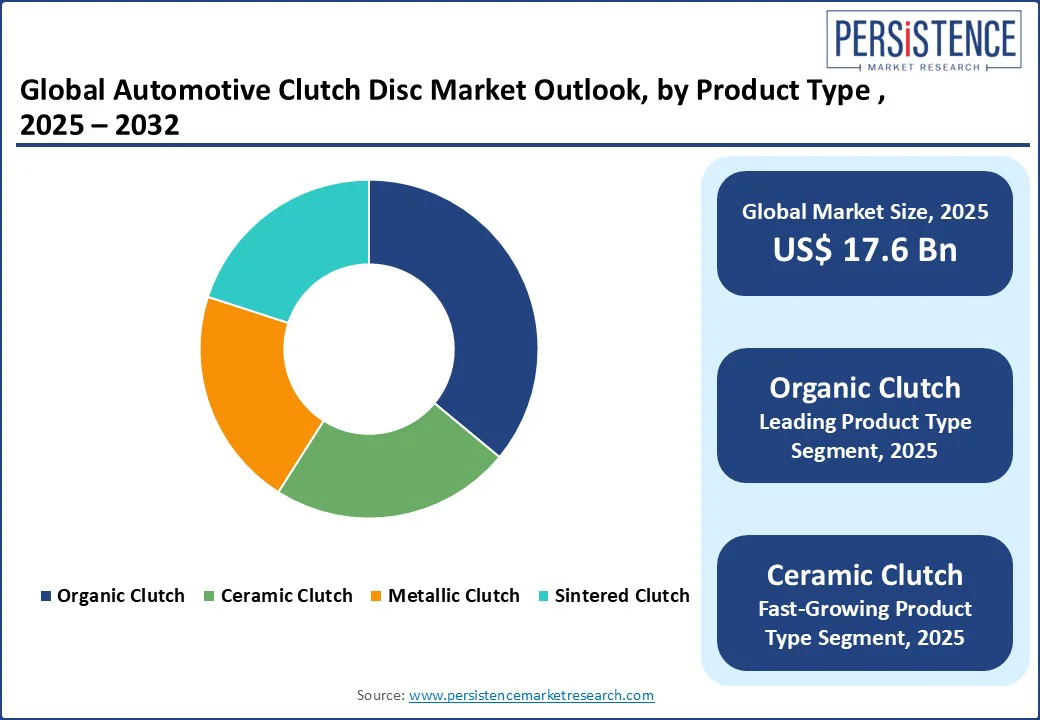

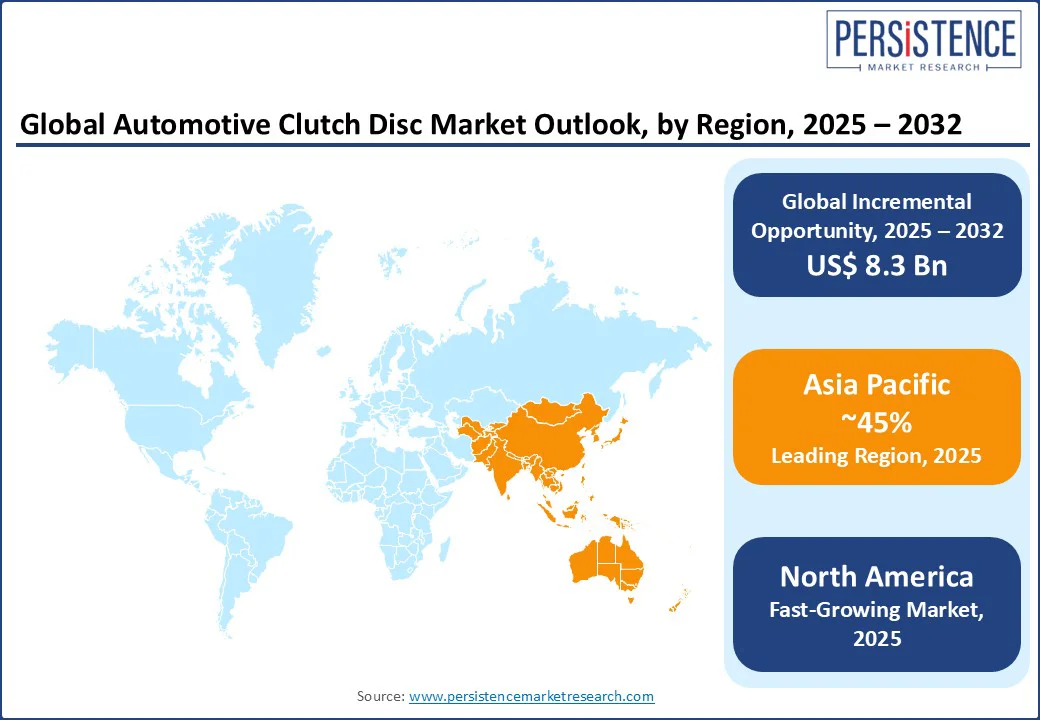

The global automotive clutch disc market is likely to value at US$ 17.6 Bn in 2025 and reach US$ 25.9 Bn by 2032, registering a CAGR of 5.7% during the forecast period from 2025 to 2032.

The rising demand for fuel-efficient vehicles, advancements in transmission technologies, and the increasing production of passenger and commercial vehicles globally have encouraged the need for clutch discs in vehicles. The automotive industry is propelled by the need for durable, high-performance clutch plates that meet the demand for modern automotive designs and adhere to the mechanical needs of the vehicle.

Key Industry Highlights:

- Leading Region: Asia Pacific, holding a 45% market share in 2025, driven by robust automotive manufacturing, rapid urbanization, and increasing vehicle ownership in countries such as China and India.

- Fastest-growing Region: North America is fueled by technological advancements in transmission systems, growing demand for electric and hybrid vehicles, and a strong automotive aftermarket.

- Dominant Product Type: Organic Clutch Discs, commanding nearly 36% market share, reflecting their widespread use in passenger cars and motorcycles due to affordability and smooth performance.

- Leading Application: Passenger Cars, accounting for over 74% of market revenue, driven by the global surge in personal vehicle ownership.

- Historical Growth: The automotive clutch disc industry registered a CAGR of 5.1% from 2019 to 2024, driven by rapid increase in fuel-based vehicle production and demand for advanced transmission systems.

|

Global Market Attribute |

Key Insights |

|

Automotive Clutch Disc Market Size (2025E) |

US$ 17.6 Bn |

|

Market Value Forecast (2032F) |

US$ 25.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.1% |

Market Dynamics

Driver - Rising Demand for Fuel-Efficient and High-Performance Vehicles

The automotive clutch disc market is being significantly driven by the rising demand for fuel-efficient and high-performance vehicles. Consumers today are increasingly prioritizing vehicles that deliver better mileage, lower emissions, and superior driving dynamics, largely due to fluctuating fuel prices, stringent environmental regulations, and growing environmental awareness. High-performance clutch discs play a crucial role in achieving these goals by ensuring efficient power transmission from the engine to the drivetrain, reducing energy losses, and improving overall vehicle responsiveness.

In passenger cars, particularly in emerging markets, the trend toward compact and fuel-efficient models boosts the adoption of lightweight, durable clutch discs. Meanwhile, in sports cars, motorcycles, and performance-oriented vehicles, there is heightened demand for clutch systems that can handle higher torque and provide smoother, faster gear shifts.

Automakers are responding by incorporating advanced materials like ceramics, carbon composites, and improved organic compounds, which enhance both efficiency and performance. For instance, in 2024, Schaeffler introduced a next-generation lightweight clutch disc designed to improve transmission efficiency by up to 10%, directly supporting automakers’ fuel economy targets.

Restraint - High Costs of Advanced Clutch Technologies

The automotive clutch disc market faces a key restraint in the form of high costs associated with advanced clutch technologies. Modern performance-oriented and fuel-efficient vehicles increasingly require clutch systems made from premium materials such as carbon composites, ceramics, or high-grade metallic compounds. While these materials offer superior heat resistance, durability, and torque-handling capabilities, they are significantly more expensive than conventional organic options.

Additionally, advanced manufacturing techniques, precision engineering, and stringent quality control further add to production expenses. These costs are particularly burdensome for price-sensitive markets, where affordability remains a major purchasing factor. The integration of new technologies-such as self-adjusting clutches or lightweight designs-also demands higher R&D investments, increasing the final product cost.

For instance, a high-performance carbon-ceramic clutch disc can cost several times more than a standard organic disc, making it less accessible for mass-market vehicles. For example, in 2023, Exedy Corporation introduced a motorsport-grade carbon clutch system priced significantly higher than conventional models, limiting its adoption outside professional racing and premium sports cars.

Opportunity - Advancements in Lightweight and Eco-Friendly Clutch Materials

The automotive clutch disc market presents a significant opportunity through advancements in lightweight and eco-friendly clutch materials. As the automotive industry moves toward stricter emission regulations and improved fuel efficiency, manufacturers are investing in innovative materials such as carbon composites, advanced ceramics, and reinforced organic fibers. These materials not only reduce the overall weight of the clutch system, enhancing vehicle fuel economy, but also improve durability and heat resistance, leading to longer service life.

Eco-friendly solutions, including recyclable composites and bio-based resins, are gaining traction as automakers aim to reduce their carbon footprint throughout the supply chain. Lightweight clutches also improve driving dynamics by reducing rotational inertia, making them appealing for both electric and high-performance vehicles.

For instance, in 2024, Schaeffler introduced a new generation of lightweight, recyclable clutch discs designed to meet EU sustainability targets, while in 2023, Exedy developed an organic-fiber-based clutch disc for hybrid vehicles, balancing performance with environmental responsibility. Such innovations fuel market growth by meeting sustainability and performance demands simultaneously.

Category-wise Analysis

Product Type Insights

Organic Clutch Discs dominate the automotive clutch disc market, expected to account for approximately 36% of the share in 2025. Their dominance stems from their affordability, smooth engagement, and versatility across a wide range of vehicles, including passenger cars and motorcycles.

Organic clutch discs, made from composite materials like resin and organic fibers, offer a cost-effective solution for standard driving conditions while providing reliable performance. Their compatibility with manual and semi-automatic transmissions enhances their applicability in price-sensitive markets like India and Southeast Asia.

The Ceramic Clutch Disc segment is the fastest-growing from 2025 to 2032, driven by increasing demand for high-performance vehicles and heavy-duty applications. Ceramic clutch discs offer superior heat resistance and durability, making them ideal for sports cars, commercial vehicles, and heavy-duty trucks that operate under high torque and extreme conditions.

The rise of motorsports and the growing popularity of performance vehicles in North America and Europe, coupled with advancements in manufacturing that reduce production costs, are accelerating the adoption of ceramic clutch discs, particularly in premium and commercial vehicle segments.

Transmission Type Insights

Manual Transmission holds the largest market share, accounting for approximately 65% of revenue in 2025. Its popularity is driven by its widespread use in passenger cars and motorcycles, particularly in emerging markets like India, Brazil, and Southeast Asia, where manual transmissions remain dominant due to their affordability and driver preference for control. Manual transmissions rely heavily on clutch discs for smooth gear shifts, making them a critical component in these markets.

Semi-Automatic Transmission is the fastest-growing segment, fueled by its increasing adoption in passenger cars and commercial vehicles. Semi-automatic transmissions combine the ease of automatic systems with the control of manual systems, appealing to consumers seeking a balance between performance and convenience. The growing popularity of semi-automatic transmissions in urban markets, where traffic congestion necessitates smoother gear transitions, is driving demand for specialized clutch discs.

Application Insights

Passenger Cars lead the automotive clutch disc market, holding a 74% share in 2025. The segment’s dominance is driven by the global surge in personal vehicle ownership, particularly in Asia Pacific and North America. Passenger cars require reliable and cost-effective clutch systems to ensure smooth driving experiences, with organic clutch discs being the preferred choice due to their affordability and performance. The rise of compact and mid-sized cars in urban markets further boosts demand for clutch discs tailored to smaller engines.

The Commercial Vehicles segment is the fastest-growing, driven by the increasing demand for logistics and transportation services. Commercial vehicles, particularly heavy-duty trucks, require durable clutch discs, such as ceramic and sintered types, to withstand high torque and prolonged use. Regulatory requirements for fuel efficiency and emissions in the commercial vehicle sector further accelerate the adoption of advanced clutch technologies.

Regional Insights

North America Automotive Clutch Disc Market Trends

North America is rapidly emerging as the fastest-growing region in the global automotive clutch disc market, with the United States and Canada at the forefront of this expansion. The region’s growth is propelled by the increasing adoption of advanced transmission systems, including semi-automatic and dual-clutch transmissions, which require high-performance clutch discs.

The U.S., in particular, holds a dominant position within the region, driven by its robust automotive industry and strong aftermarket demand. In 2024, the U.S. produced approximately 10 million vehicles, with a significant portion incorporating advanced clutch systems to meet fuel efficiency standards.

The growing popularity of electric and hybrid vehicles, which require specialized clutch discs for hybrid powertrains, further boosts market growth. Additionally, consumer awareness of sustainability and regulatory policies, such as the U.S. EPA’s emission standards, are driving demand for lightweight and eco-friendly clutch materials. The presence of advanced manufacturing and R&D facilities in the U.S. supports innovation in clutch disc technologies, positioning the region for sustained growth through 2032.

Europe Automotive Clutch Disc Market Trends

Europe holds a significant share in the automotive clutch disc market, driven by strong automotive manufacturing, sustainability initiatives, and growing demand for high-performance vehicles. Leading countries include Germany, the UK, and France. Germany benefits from its advanced automotive industry, with companies like ZF Friedrichshafen and Schaeffler investing heavily in lightweight and durable clutch technologies.

The UK’s market is bolstered by the growing adoption of semi-automatic transmissions and the shift toward eco-friendly materials, supported by initiatives like the UK’s Net Zero Strategy. France’s market is driven by investments in hybrid vehicle production and sustainable automotive components.

The EU’s stringent regulations, such as the Green Deal and CO2 emission targets, drive the adoption of advanced clutch systems, though compliance with complex environmental laws poses challenges. Europe’s automotive clutch disc market is projected to grow steadily from 2025 to 2032.

Asia Pacific Automotive Clutch Disc Market Trends

Asia Pacific is projected to hold a dominant 45% share of the global automotive clutch disc market in 2025, driven by a combination of robust automotive manufacturing, rapid urbanization, and rising vehicle ownership, particularly in high-growth economies such as China and India.

The region’s thriving automotive industry benefits from the presence of leading vehicle manufacturers, extensive production facilities, and cost-effective labor, enabling large-scale output for both domestic consumption and export. Rapid urbanization has led to increasing demand for passenger vehicles, while expanding industrial activity and logistics networks are boosting sales of commercial vehicles, all of which contribute to higher clutch disc demand.

In countries such as China, government incentives for modernizing vehicle fleets and transitioning to cleaner, more efficient technologies further encourage the adoption of advanced clutch systems. Meanwhile, India’s fast-growing middle class and improving road infrastructure are spurring sales of motorcycles and small cars, segments where cost-effective organic clutch discs are widely used.

Additionally, the rise of electric and hybrid vehicle manufacturing in Asia Pacific presents opportunities for lightweight, eco-friendly clutch solutions tailored to new drivetrain requirements. Collectively, these factors position the region as both the largest and one of the most dynamic markets for automotive clutch discs in the coming years.

Competitive Landscape

The global automotive clutch disc market is characterized by intense competition, regional strengths, and a mix of global and local manufacturers. In developed regions like North America and Europe, large firms such as BorgWarner, Schaeffler, and ZF Friedrichshafen dominate through advanced technology, scale, and partnerships with major automakers.

In Asia Pacific, rapid automotive production and growing demand for affordable clutch systems attract investments from both local and international players. Companies are focusing on sustainability, cost-efficiency, and performance to gain a competitive edge.

Innovations in lightweight materials and digital manufacturing have emerged as key differentiators, enabling customized solutions and faster production times. Strategic acquisitions and R&D initiatives further intensify the competitive landscape.

Key Industry Developments:

- In 2025, ZF unveiled the TraXon 2 Hybrid, an eco-friendlier version of its TraXon transmission for trucks and buses. At the ACT Expo in North America, they showcased how it supports hybrid operations and helps cut carbon emissions—up to 14% in short-haul, 9% in long-haul, and up to 40% in plug-in hybrid setups.

- In May 2025, BorgWarner secured two important dual-clutch (DCT) transmission projects in China: A 7-year extension with a German OEM for DCT clutch assemblies made in Tianjin. These assemblies improve smoothness, reduce friction losses, and boost transmission efficiency across conventional and mild-hybrid vehicles.

- A new DCT module program with a major transmission manufacturer for SUVs and sedans. This compact, thermally robust module will be produced in Taicang and is set for mass production by the end of 2025.

Companies Covered in Automotive Clutch Disc Market

- Haldex

- BorgWarner

- Torotrak

- Aisin Seiki

- Schaeffler

- Mahle

- Exedy

- Denso

- ZF Friedrichshafen

- Nagoya Rubber

- FTE Automotive

- Hengst

- Clutch Auto

- Valeo

Frequently Asked Questions

The Automotive Clutch Disc market is projected to reach US$ 17.6 Bn in 2025.

The surge in demand for fuel-efficient and high-performance vehicles is a key driver.

The Automotive Clutch Disc market is poised to witness a CAGR of 5.7% from 2025 to 2032.

Advancements in lightweight and eco-friendly clutch materials are a key opportunity.

BorgWarner, Schaeffler, ZF Friedrichshafen, Aisin Seiki, and Valeo are key players.