- Automotive Components & Materials

- Automotive Balance Shaft Market

Automotive Balance Shaft Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Balance Shaft Market by Engine Type (Inline 3 Cylinder, Inline 4 Cylinder, Inline 5 Cylinder and V 6 Cylinder), by Manufacturing Process (Forging and Casting), by Vehicle Type (Passenger Vehicles, LCV and HCV) and Regional Analysis for 2026 - 2033

Automotive Balance Shaft Market Size and Trends Analysis

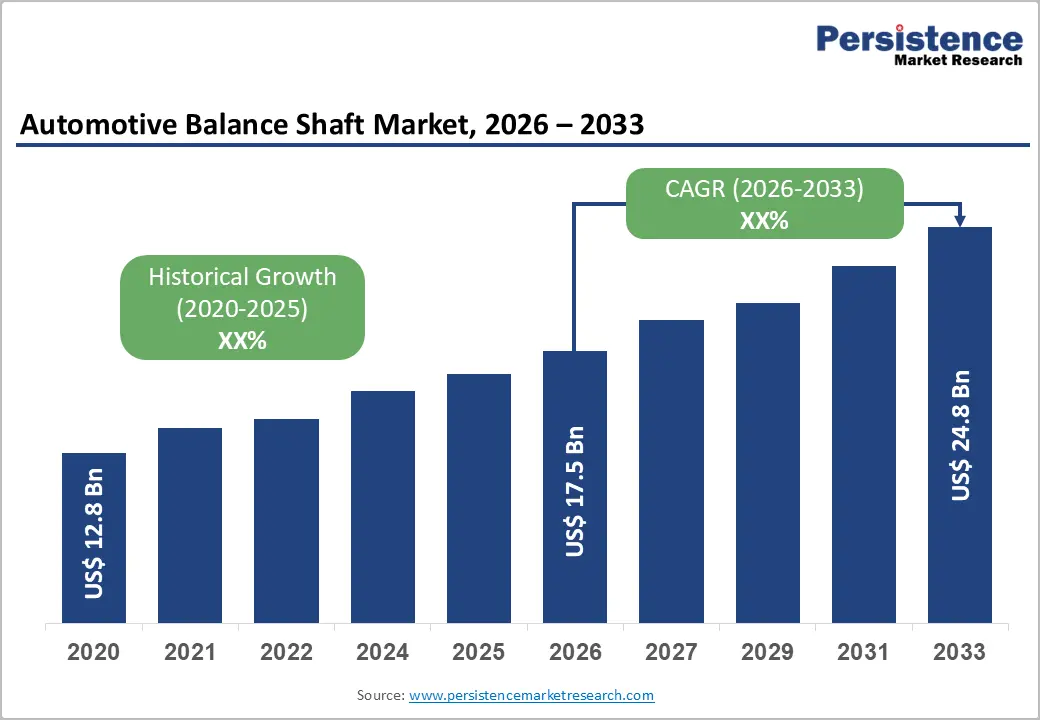

The global automotive balance shaft market is likely to be valued at US$ 16.24 billion in 2026 and is projected to reach US$ 24.82 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033. Growth is driven by increased production of inline-4 and V6 engines, which require noise, vibration, and harshness (NVH) reduction, heightened regulatory emphasis on emissions and fuel-efficiency standards, and rising demand for refined engine performance in hybrid and commercial vehicles.

Key Industry Highlights:

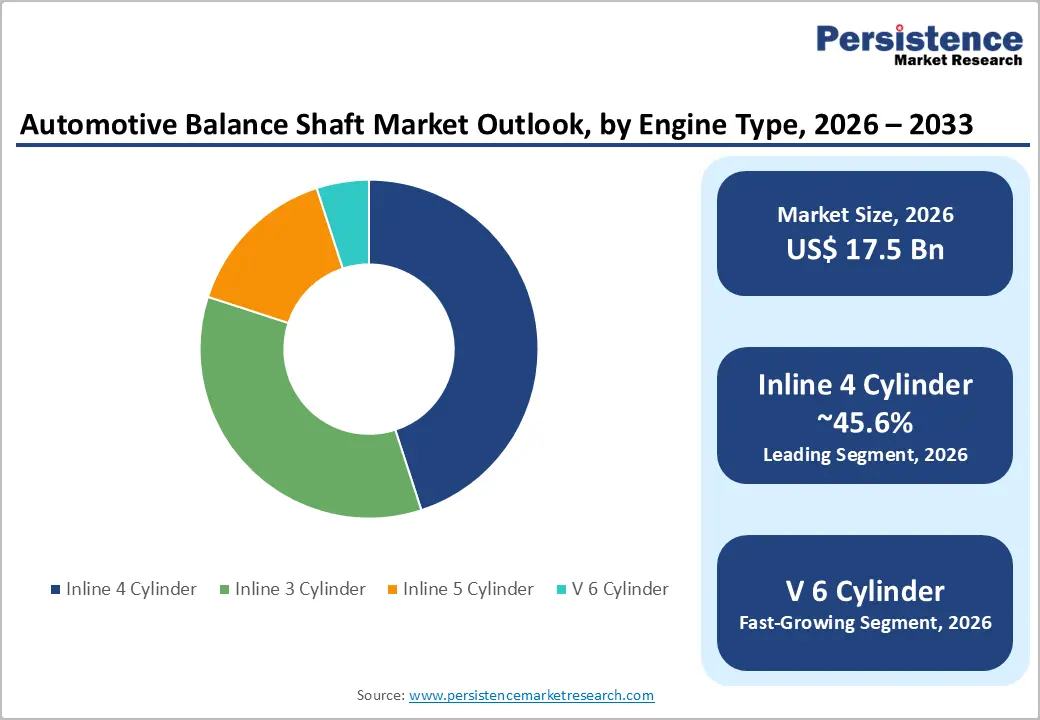

- Engine type segmentation: Inline-4-cylinder engines dominate at a 45.6% share (~US$7.41 billion in 2026), while V6-cylinder engines are the fastest-growing at a 6.8% CAGR, driven by premium SUV expansion and luxury vehicle demand.

- Manufacturing process shift: Forged balance shafts represent 52% of market value (~US$ 8.44 billion 2026), growing at 5.5–6.5% CAGR, outpacing cast alternatives at 3.5–4.5% CAGR due to lightweight and durability advantages.

- Vehicle type dynamics: Passenger vehicles dominate at 62.4% share (~US$ 10.12 billion 2026), while LCVs are the fastest growing at 6.5% CAGR, driven by e-commerce expansion and commercial fleet demand.

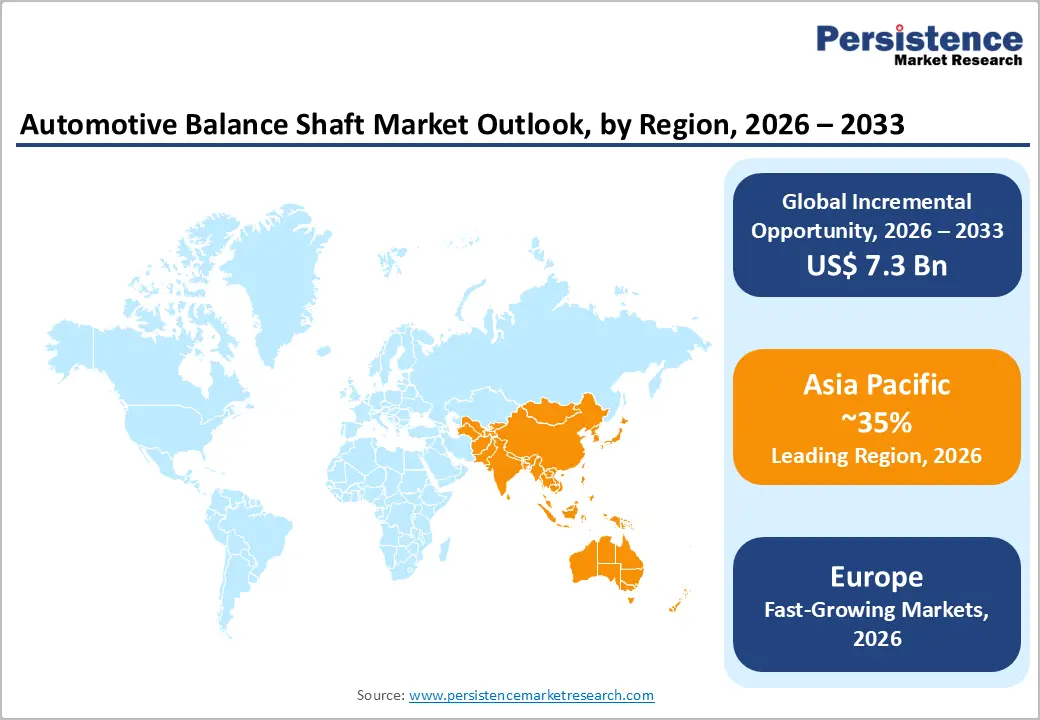

- Regional performance: Asia Pacific dominates at 35% global share (~US$ 7.5 billion 2026) with 5.5% CAGR; Europe exhibits moderate growth (4.0% CAGR) driven by Euro 7 compliance; North America reflects a mature market (3.5% CAGR).

- Strategic positioning: Hybrid powertrain specialization emerging as key differentiator; lightweight forged systems capturing market share from cast alternatives; regional manufacturing expansion in emerging markets supporting localized supply chains and cost optimization.

| Key Insights | Details |

|---|---|

|

Automotive Balance Shaft Market Size (2026E) |

US$ 17.5 Bn |

|

Market Value Forecast (2033F) |

US$ 24.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.1% |

|

Historical Market Growth (CAGR 2020 to 2024) |

4.5% |

Market Dynamics

Drivers - Regulatory Emission Standards and Fuel Efficiency Mandates Driving Engine Refinement

Global regulatory frameworks—including EU Euro 7 standards, EPA Tier 3/Tier 4 emissions regulations, and CAFE fuel-efficiency requirements — mandate substantial improvements in engine efficiency, emissions reduction, and noise/vibration control across automotive manufacturers. These regulations directly incentivize investment in advanced engine technologies, including balance shaft systems, to achieve secondary vibration suppression that is critical for meeting NVH (noise, vibration, harshness) requirements and overall engine refinement.

The transition toward smaller-displacement, turbocharged engines (downsizing strategy) paradoxically increases balance shaft demand, as three- and four-cylinder turbocharged engines produce greater secondary vibration, requiring more complex balance shaft configurations. Additionally, hybrid and plug-in hybrid vehicle architectures require refined NVH performance to mask interactions between the electric motor and internal combustion engine, thereby driving the adoption of balance shafts at increasing rates across hybrid platforms.

Rising Production of Inline-4 and V6 Engines in Emerging Markets and SUV Expansion

Global vehicle production continues shifting toward light trucks, SUVs, and commercial vehicles across both developed and emerging markets. Inline-4-cylinder engines remain the most widely adopted engine architecture, valued at approximately US$7.41 billion (2026) due to their cost-effectiveness, fuel efficiency, and widespread consumer acceptance in compact and mid-size vehicles.

V6 engines are experiencing resurgent demand in premium SUVs, luxury vehicles, and commercial applications, with growth projected at an estimated 6.8% CAGR, driven by market share gains in SUV segments, particularly in North America, Europe, and emerging markets in Asia-Pacific. China, India, and Southeast Asia are experiencing rapid growth in vehicle production, with an annual production CAGR of 4–6% through 2033, resulting in increased demand for balance shafts from new-vehicle assembly. Additionally, commercial vehicle markets (light commercial vehicles and medium-duty trucks) are adopting advanced balance shaft systems to improve engine durability and longevity, thereby supporting sustained demand growth across non-passenger-vehicle segments.

Restraint - EV Adoption and Long-Term Structural Decline in ICE Powertrain Demand

Electric vehicle adoption is accelerating globally, with EV sales projected to account for 50% or more of total vehicle sales by 2035 in developed markets and 15–25% in emerging markets. Since balance shafts are components exclusively for internal combustion engines (ICE) and hybrid powertrains, rising EV penetration creates a structural headwind to the growth of the balance shaft market. Although hybrid vehicles (conventional hybrid, plug-in hybrid, and mild hybrid 48V architectures) will continue to require balance shafts for ICE refinement, the long-term market outlook indicates a decline.

Average balance shafts per vehicle produced as EV share rises. This structural decline is partially offset by increased balance shaft complexity and value in hybrid powertrains requiring enhanced NVH control, but long-term growth will moderate substantially as EV penetration approaches 70% of developed market production by 2040.

Supply Chain Concentration and Rising Raw Material Costs

Balance shaft manufacturing relies on specialty steel alloys, forging capabilities, and precision machining capacity, all sourced from concentrated supplier bases, particularly in Asia and Europe. Raw material costs, driven by volatile steel pricing and volatility in nickel, chromium, and molybdenum, increased by 15% in 2024–2026, pressuring manufacturers' margins.

Additionally, geopolitical supply chain disruptions (China's trade restrictions, war-related logistics constraints in Ukraine) have led to 18–24-month lead times for specialized forging equipment and alloys, constraining manufacturers' ability to scale production to meet demand. Smaller, independent balance shaft manufacturers lack vertical integration, long-term supply contracts, or hedging strategies, and face margin compression and competitive threats relative to larger suppliers with integrated sourcing and production networks.

Opportunity - Hybrid and Plug-in Hybrid Vehicle NVH Refinement at Scale

The transition toward hybrid and plug-in hybrid vehicles (projected at 30% of global vehicle production by 2035) creates substantial demand for advanced balance shaft systems delivering superior NVH control to mask electric motor-ICE interactions and transition smoothness critical for consumer acceptance. Hybrid powertrain architectures require specialized balance shafts optimized for bi-directional vibration suppression and dynamic load management across engine-on and engine-off operational modes. This emerging segment is estimated at US$ 4–7 billion annually and growing at 8% CAGR, representing a high-margin opportunity for suppliers offering hybrid-specific balance shaft solutions with integrated diagnostics, variable damping, and precision control. Early-mover suppliers that establish hybrid balance shaft specialization can secure premium positioning and sustained competitive advantages through 2035 and beyond.

Commercial and Heavy-Duty Vehicle Engine Durability Solutions

Heavy commercial vehicles (trucks, buses) and light commercial vehicles require heavy-duty balance shafts optimized for extended service intervals (500,000–1,000,000-mile durability), extreme thermal cycling, and high-vibration environments. Global commercial vehicle production is expanding, particularly in the Asia Pacific and emerging markets, with an annual CAGR of 3–5% supporting steady demand growth in heavy-duty balance shaft segments. Suppliers offering commercial vehicle-specific balance shafts with enhanced durability certifications, extended warranty, and integrated condition-monitoring can command 20–30% price premiums and capture disproportionate market growth in this underserved premium segment estimated at US$ 2.5 billion annually, growing at 6% CAGR.

Category-wise Analysis

Engine Type Insights

Inline-4-cylinder engines represent the largest market segment at 45.6% share (~US$ 7.41 billion 2026), driven by widespread adoption in passenger vehicles, commercial vehicles, and cost-sensitive segments where balance shafts are essential for secondary vibration suppression. Inline-4 architectures account for approximately 65–70% of all vehicle production globally, supporting continued high-volume balance shaft demand. This segment is expected to grow at approximately 4% CAGR through 2033, reflecting steady demand offset by EV penetration headwinds. Market value is projected toward US$ 9.5–10.2 billion by 2033.

V6 cylinder engines are the fastest-growing segment at an estimated 6.8% CAGR, with market value of approximately US$ 3.2 billion (2026) projected to grow toward US$ 5.0 billion by 2033. V6 growth is driven by premium SUV expansion (particularly in North America and Europe) and luxury vehicle segments where advanced balance shaft systems supporting enhanced NVH and refined engine performance are standard features. V6 engines in hybrid and plug-in hybrid configurations require specialized balance shafts with dynamic damping and variable stiffness, optimizing both ICE and hybrid operation modes, supporting premium pricing and above-market growth rates.

Manufacturing Process Insights

Forged balance shafts represent approximately 52% of market value (~US$ 8.44 billion 2026) and are growing at an estimated 5.5–6.5% CAGR, driven by superior durability, lightweight design capability, and precision manufacturing advantages. Forging processes create denser material microstructures and superior fatigue resistance, enabling smaller dimensions, reduced mass (20–30% lighter), and extended service life relative to cast alternatives. Advanced forging techniques including warm forging, precision die design, and integrated surface treatments enable tighter dimensional tolerances and superior surface finish, reducing post-machining requirements and lifecycle costs. Forged balance shafts command 15% price premiums relative to cast alternatives, supporting margin expansion for suppliers with forging capabilities.

Cast balance shafts (representing 48% market share ~US$ 7.80 billion 2026, reflecting mature market saturation and progressive shift toward forged alternatives in premium vehicle segments and hybrid applications. Cast production remains cost-competitive for high-volume, non-performance-critical applications in emerging markets and commercial vehicles, but OEM preference is increasingly shifting toward forged products for NVH-sensitive applications.

Vehicle Type Insights

Passenger vehicles represent the largest segment at 62.4% share (~US$ 10.12 billion 2026), reflecting global vehicle parc dominated by sedans, coupes, and compact vehicles requiring two-shaft balance shaft systems for inline-4 engines. Passenger vehicle segment growth is estimated at approximately 4–5% CAGR, driven by vehicle production growth, increasing feature penetration in emerging markets, and technology upgrade cycles.

Light commercial vehicles are the fastest-growing segment, with a market value of approximately US$3.1–3.4 billion (2026), projected to reach US$4.8–5.5 billion by 2033. LCV growth is driven by global e-commerce and the expansion of last-mile delivery, creating demand for commercial vehicle fleets with optimized engine durability and longer service intervals. Additionally, the expansion of the light truck and SUV market in North America and emerging markets drives above-average growth in LCV balance shaft demand.

Regional Insights

North America Automotive Balance Shaft Market Trends

North America represents an estimated US$ 3.8–4.2 billion market (2026) with projected growth to US$ 5.5 billion by 2033, reflecting 4.1% CAGR-below global baseline, reflecting market maturity. The U.S. dominates regional demand, driven by significant vehicle production volume, a large SUV and light truck market, and a mature OEM presence with established balance shaft supplier relationships.

The regulatory environment emphasizes EPA emissions standards, NHTSA safety requirements, and CAFE fuel-efficiency mandates. These frameworks establish a stable baseline demand for balance shaft systems, supporting compliance-driven engine development.

North American automotive production is relatively stable (~10 million vehicles annually), with light trucks and SUVs accounting for 70% of sales, driving disproportionate demand for V6 engines and premium balancer shafts. The competitive landscape features global leaders (Mahle Powertrain, GKN Driveline, Schaeffler) alongside regional specialists supporting Tier-1 suppliers and OEM aftermarket operations.

Europe Automotive Balance Shaft Market Trends

Europe represents an estimated US$3.5 billion market (2026), with projected growth to US$5.0 billion by 2033, reflecting a positive CAGR over the forecast period. Germany, France, the U.K., and Spain lead European demand, driven by strong OEM presence (Volkswagen, BMW, Mercedes, PSA, Stellantis), adoption of advanced engine technology, and stringent emissions regulations (Euro 7). The regulatory environment is characterized by EU energy efficiency directives, emissions standards (Euro 7 targeting near-zero NOx), and NVH requirements. These regulations directly drive investment in advanced balance shaft technologies that support engine downsizing, fuel-efficiency improvements, and refined NVH performance.

European automakers are early adopters of advanced balance shaft systems optimized for turbocharged four-cylinder and hybrid powertrains. Diesel engine production (still 30–40% of the European market) requires heavy-duty balance shafts optimized for high-compression, high-vibration diesel engines, creating embedded demand for specialized solutions.

Asia Pacific Automotive Balance Shaft Market Insights

Asia Pacific represents an estimated US$ 7.5 billion market (2026) with projected growth to US$ 15 billion by 2033, reflecting 5.5 CAGR highest growth among global regions. The region is the largest market by absolute size (~51% of the global market in 2024), anchored by China's dominance, Japan's technological leadership, and emerging manufacturing in India and Southeast Asia.

China leads regional demand with approximately US$ 3.5 billion market (2026), and 7.9% projected CAGR, driven by the world's largest vehicle production (~28 million vehicles annually), domestic OEM expansion (BYD, NIO, Xpeng), and SUV market penetration. Japan maintains technological leadership in advanced balance shaft design and lightweight materials, commanding a disproportionate share of premium/export markets.

Competitive Landscape

The market for automotive balance shafts is highly competitive, with major companies seeking to strengthen their market presence through innovation, strategic alliances, and broader product lines. Firms are investing significantly in research and development to develop lightweight, durable, and efficient balance shafts. Innovations such as forged balance shafts are gaining popularity for their compact size and effective natural damping.

Additionally, as regulatory pressures to reduce greenhouse gas emissions intensify, manufacturers are focusing on developing balance shafts that improve fuel efficiency and reduce vehicle emissions. This trend is encouraging the use of balance shafts in both passenger cars and commercial vehicles.

Key Developments

- In January 2025, Cummins introduced the 6.7-liter turbo diesel engine for the 2026 Ram Heavy Duty vehicle. Cummins and Stellantis confirmed the continuation of their collaboration to provide engines for the Ram brand by 2030. This 6.7-liter turbo diesel engine, described as the most advanced diesel engine for pickups to date, will be available in the newly revealed 2026 Ram 2500 and 3500 Heavy Duty pickups, and the Ram 3500, 4500, and 5500 Chassis Cab trucks.

- In May 2024, Subaru Corporation, Toyota Motor Corporation, and Mazda Motor Corporation joined forces to develop new engines optimized for electrification, with a focus on carbon neutrality. With these new engines, all three companies intend to enhance compatibility with motors, batteries, and other electric-drive components.

Companies Covered in Automotive Balance Shaft Market

- Hitachi Astemo Americas, Inc.

- Marposs S.p.A.

- MAT Foundry Group Ltd.

- SAC Engine Components Pvt. Ltd.

- American Axle & Manufacturing, Inc.

- SHW AG

- OTICS Corp.

- Engine Power Components, Inc.

- Sansera Engineering Limited

- TFO Corporation

- Others Key Players

Frequently Asked Questions

The Automotive Balance Shaft market is estimated to be valued at US$ 17.5 Bn in 2026.

The key demand driver for the Automotive Balance Shaft market is the growing need for smoother engine operation and improved vehicle comfort through reduced vibration, noise, and harshness (NVH) particularly in internal combustion and hybrid powertrains.

In 2026, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Automotive Balance Shaft market.

Among the Product Type, Inline 4 Cylinder holds the highest preference, capturing beyond 45.6% of the market revenue share in 2026, surpassing other Engine Type.

The key players in Automotive Balance Shaft are Hitachi Astemo Americas, Inc., Marposs S.p.A., MAT Foundry Group Ltd. and SAC Engine Components Pvt. Ltd.