- Medical Devices

- Auto Keratometer Market

Auto Keratometer Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Auto Keratometer Market by Product Type (Handheld Auto Keratometer, Benchtop Auto Keratometer), Application (Myopia (Nearsightedness), Hyperopia (Farsightedness), Astigmatism, Other Ophthalmic Conditions), End-user (Hospitals, Ophthalmic Clinics, Diagnostic Centers, Educational & Research Institutes), and Regional Analysis for 2026 - 2033

Auto Keratometer Market Trends & Analysis

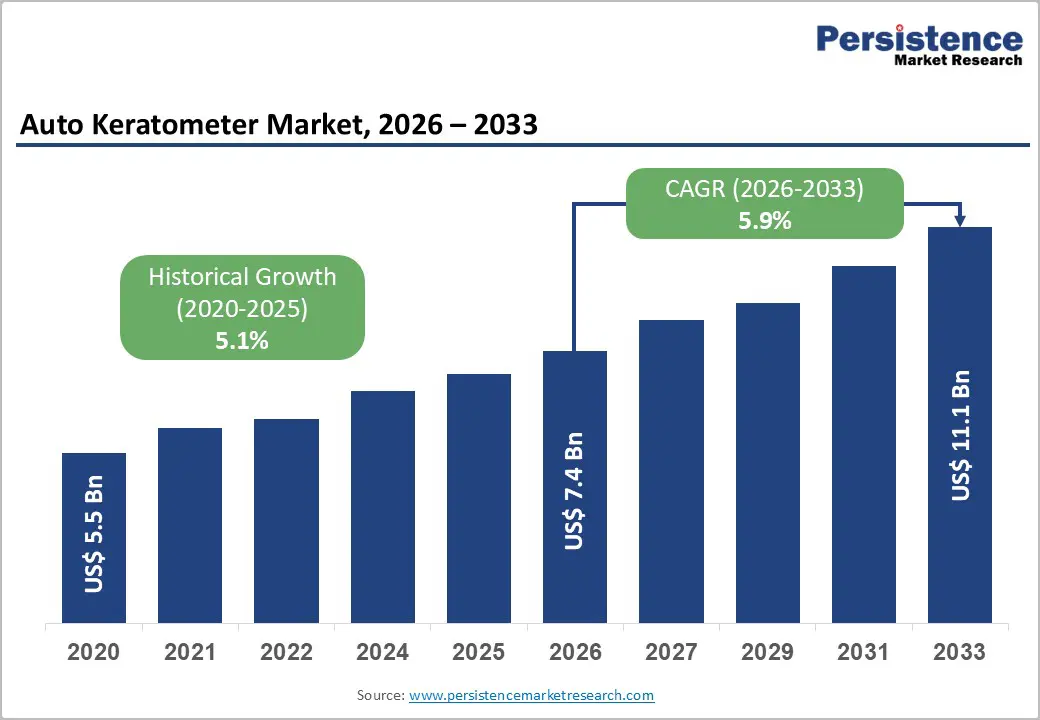

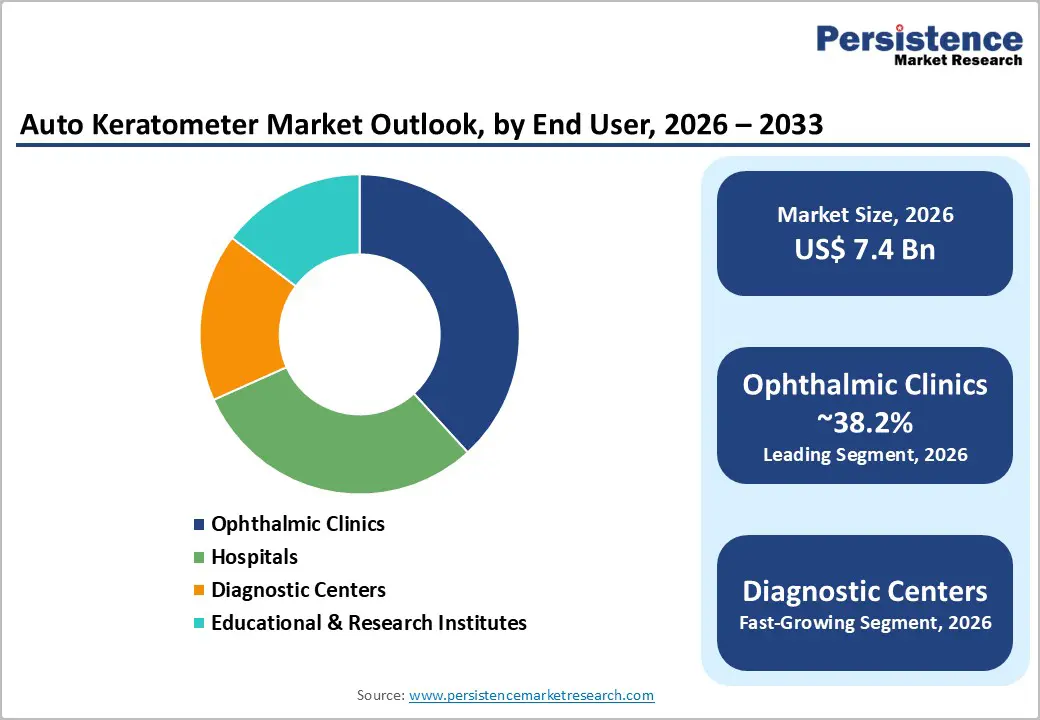

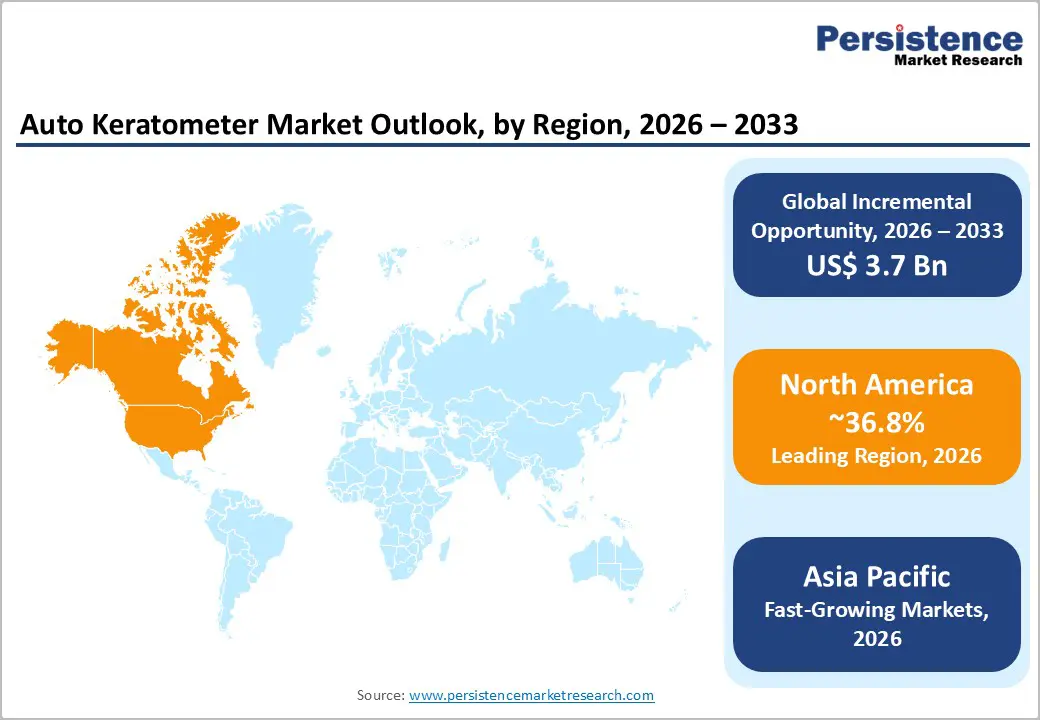

The global auto keratometer market size is anticipated at US$ 7.4 billion in 2026 and is projected to reach US$ 11.1 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

The rise in global myopia prevalence, with 2.6 billion people currently affected worldwide (WHO/Holden et al., Ophthalmology), expanding surgical volumes for cataract and refractive procedures requiring precise pre-operative keratometry, and aging population growth driving astigmatism diagnosis and management demand are the primary structural growth drivers.

Key Industry Highlights:

- Leading Product Type: Handheld auto keratometers lead at 55.3% share and grow fastest at 6.7% CAGR, driven by Asia Pacific pediatric myopia screening program expansion and teleophthalmology deployment.

- Leading Application: Astigmatism leads at 32.4% share; Myopia is likely to achieve a fast-growth driven by WHO-recognized global epidemic affecting 2.6 billion people and national childhood screening mandates.

- Leading End-user: Ophthalmic clinics lead at 38.2% share; diagnostic centers grow fastest at 6.1% CAGR, driven by multi-specialty diagnostic network expansion across Asia Pacific and Middle East.

- Regional Leadership: North America leads at 36.8% share with U.S. at US$ 2.4 Bn; Asia Pacific grows fastest at 7.3% CAGR with China at US$ 734.9 Mn and India at US$ 439.6 Mn in 2026.

- Strategic Milestone: Carl Zeiss Meditec's €30 Mn Shanghai expansion (January 2025) and Topcon's KR-1W Wavefront Analyzer launch position premium multifunction keratometry platforms at the center of China's myopia management program procurement expansion globally.

Market Dynamics Analysis

Drivers - Global Myopia Epidemic Driving Mass Population Screening and Diagnostic Instrument Demand

The WHO recognizes myopia as a critical public health concern, with current global prevalence among children and young people reaching 30.47% across 276 studies in 50 countries, projected to rise to 39.80% by 2050 when an estimated 740 million cases will exist globally (Brien Holden Vision Institute, Ophthalmology, 2016). Approximately 2.6 billion people worldwide are currently affected by myopia (Holden BA et al.), creating an unprecedented public health imperative for mass corneal curvature screening programs where auto keratometers serve as the front-line diagnostic instrument.

High-prevalence East Asian nations, with childhood myopia rates of 70-90% in China, South Korea, and Singapore (WHO Visual Impairment Atlas), are investing in school-based myopia screening programs where portable handheld auto keratometers enable scalable population-level corneal curvature assessment without pupil dilation or specialist physician involvement.

The WHO Global Action Plan for the Prevention of Avoidable Blindness has identified myopia management as a priority intervention target, catalyzing national ophthalmic screening infrastructure investments across China, India, and Southeast Asian nations that directly expand auto keratometer procurement volume across ophthalmic clinic, school vision screening, and primary healthcare facility end-user categories through 2033.

Expanding Cataract and Refractive Surgery Volumes Mandating Precise Pre-Operative Keratometry

The WHO estimates 65 million people globally are blind from cataracts, with annual global cataract surgery volume exceeding 20 million procedures (International Agency for the Prevention of Blindness), each requiring pre-operative auto keratometry to determine corneal curvature parameters essential for intraocular lens (IOL) power calculation and premium toric IOL axis alignment for astigmatism correction. Cataract surgery volumes are increasing at 3-4% annually across developed markets and 6-8% in Asia Pacific driven by aging demographics and expanding surgical access programs.

LASIK and refractive surgery volumes, with over 900,000 LASIK procedures performed annually in the U.S. alone (American Refractive Surgery Council), each require pre-operative keratometry data to map corneal curvature irregularities and calculate ablation parameters, creating a structurally captive, procedure-proportional auto keratometer utilization demand at every refractive surgery center globally. The global ophthalmic surgical equipment market, projected to exceed US$ 12 Bn by 2030 (IAPB), sustains auto keratometer procurement as a mandatory pre-surgical measurement instrument across cataract, refractive, and corneal transplant surgical workflows, reinforcing the medical necessity-driven demand base that insulates market growth from discretionary spending fluctuations through 2033.

Restraints - Regulatory Approval Complexity for Advanced Auto Keratometer Configurations Delaying Market Entry

Auto keratometers, classified as Class II medical devices under FDA 21 CFR Part 886.1500 and Class IIa under EU MDR 2017/745, require 510(k) premarket notification submissions, CE marking conformity assessment, and ISO 10342 ophthalmic instruments standards compliance documentation that extend new product market entry timelines by 12-24 months per jurisdiction. The EU MDR's mandatory clinical evaluation requirements and post-market surveillance obligations, effective for all legacy Class IIa ophthalmic devices from May 2024, imposed comprehensive reauthorization burdens on established auto keratometer product lines, potentially removing 15-20% of non-compliant devices from European market circulation and creating temporary supply disruptions at ophthalmic facilities dependent on specific device configurations.

Shortage of Trained Ophthalmic Technicians Constraining Device Utilization in Emerging Markets

While auto keratometers deliver automated corneal curvature measurement results, accurate data acquisition requires properly trained ophthalmic technicians to position patients correctly, select appropriate measurement modes, and interpret measurement quality indicators, a human capital dependency that constrains device utilization rates at under-resourced ophthalmic facilities across South Asia, Sub-Saharan Africa, and Latin America. The International Council of Ophthalmology estimates a global deficit of 200,000+ trained ophthalmic personnel, with technician shortages particularly acute in low-and-middle-income countries where ophthalmic device procurement is outpacing workforce development capacity, creating sub-optimal device utilization and delaying return-on-investment justification for new auto keratometer capital procurement at public health facility programs.

Opportunities - Integrated Autorefractor-Keratometer-Topographer Combination Device Adoption

The convergence of autorefraction, keratometry, corneal topography, and wavefront aberrometry into single multifunction ophthalmic diagnostic platforms is generating a structurally distinct upgrade procurement cycle at established ophthalmic clinics and hospitals investing in diagnostic workflow consolidation and data integration with electronic health record systems. Combined autorefractor-keratometer devices, such as Topcon's KR-800, Nidek's ARK-1s, and Zeiss i.Profiler Plus, deliver parallel diagnostic outputs from a single patient positioning session, reducing examination time by 30-40% while expanding the breadth of corneal parameters captured per consultation.

The global autorefractor market is projected to reach US$ 3.25 billion by 2030 at 11.0% CAGR (Market Research, 2026), with integrated autorefractor-keratometer combination devices capturing an expanding share of this addressable market as ophthalmic facilities prioritize workflow efficiency and diagnostic comprehensiveness.

For auto keratometer manufacturers, integrated combination device platforms generate 40-60% higher average selling prices per unit versus standalone keratometers while addressing the equipment capital investment consolidation requirements of hospital procurement committees, creating a structurally superior value proposition that is progressively displacing standalone keratometer upgrades across hospital, ophthalmic clinic, and diagnostic center end-user procurement programs globally through 2033.

Handheld Auto Keratometer Deployment in Pediatric Myopia Management and Teleophthalmology Programs

Handheld auto keratometers, capable of measuring cooperative and non-cooperative pediatric patients in supine and seated positions without requiring chin-rest stabilization, are gaining rapid adoption for school-based myopia screening programs, pediatric eye care mobile clinics, and teleophthalmology platforms in China, India, and Southeast Asian nations implementing national childhood vision health initiatives. China's National Health Commission launched a school-age vision health improvement program targeting 90% childhood myopia screening coverage by 2025, with handheld portable auto keratometer procurement serving as primary enabling instruments at school health examination stations across 300 million school-age children.

India's Rashtriya Bal Swasthya Karyakram (RBSK) child health screening initiative, covering 270 million children across 2,300 districts, is progressively integrating vision screening protocols that create handheld auto keratometer procurement requirements at district-level health facilities. The handheld auto keratometer segment leads the market at 55.3% share and grows fastest at 6.7% CAGR through 2033, with addressable market opportunity in pediatric myopia screening and teleophthalmology applications estimated at US$ 1.5-2.0 Bn by 2030 across Asia Pacific, Latin American, and African public health screening program procurement expansions.

Category-wise Analysis

Product Type Insights

Handheld Auto Keratometers lead the product type segment with a 55.3% market share in 2026. Handheld configurations command segment leadership through their versatile measurement capability for pediatric patients, bedridden hospital patients, and community screening program participants who cannot access stationary benchtop instruments, addressing the broadest clinical deployment range of any auto keratometer configuration. Their portability enables deployment in mobile ophthalmic screening clinics, rural outreach programs, school-based vision checks, and emergency ophthalmic care settings that collectively represent the highest-volume procurement end-use scenarios in Asia Pacific and emerging market healthcare systems.

Benchtop auto keratometers retain competitive dominance in premium hospital and surgical center pre-operative measurement applications, but handheld's combined clinical flexibility and emerging market procurement volume sustain its segment leadership firmly through 2033.

Handheld Auto Keratometers are also the fastest-growing product type at 6.7% CAGR through 2033. Asia Pacific national myopia screening program expansion, India's RBSK child health vision screening integration, and teleophthalmology platform deployment across underserved populations requiring portable diagnostic instrument specifications are collectively driving handheld auto keratometer adoption acceleration beyond benchtop growth rates through 2033 globally.

Application Insights

Astigmatism leads the application segment with a 32.4% market share in 2026. Astigmatism's dominance reflects both its high global prevalence, affecting approximately 1 in 3 adults globally (American Academy of Ophthalmology), and its direct dependency on auto keratometry as the essential corneal curvature measurement modality for astigmatism diagnosis, contact lens fitting, and pre-surgical toric IOL planning. Every cataract surgery patient with co-existing astigmatism requires keratometry data for toric IOL axis selection and power calculation, creating a high-frequency, procedurally mandatory auto keratometer utilization pattern that sustains astigmatism application segment revenue leadership. Myopia's rapidly growing screening volume will narrow the gap through 2033, but astigmatism's surgical workflow dependency sustains its leading position.

Myopia (Nearsightedness) is the fastest-growing application segment at 7.0% CAGR through 2033. The WHO-recognized global myopia epidemic, affecting 2.6 billion people with projections reaching 4.76 billion by 2050, combined with national childhood myopia management programs in China, India, Singapore, and South Korea mandating serial keratometry monitoring for myopia progression tracking, is driving myopia application segment acceleration through 2033.

End-user Insights

Ophthalmic Clinics lead the end-user segment with a 38.2% share in 2026. Ophthalmic clinics command segment leadership as the highest-volume point of care for routine refractive error diagnosis, contact lens fitting, myopia management follow-up, and pre-surgical assessment, where auto keratometry is performed as a standard examination component in virtually every patient consultation. Their concentration of ophthalmic specialist expertise, high examination throughput, and direct billing for ophthalmic diagnostic procedures create the strongest per-facility auto keratometer procurement and utilization intensity of any end-user category globally. Hospitals hold competitive procurement scale for premium benchtop configurations, while diagnostic centers are growing rapidly through multi-disciplinary vision health center development.

Diagnostic Centers are the fastest-growing end-user segment at 6.1% CAGR through 2033. Expansion of multi-specialty diagnostic center networks across Asia Pacific and Middle East healthcare systems, integrating ophthalmic diagnostic services with general health screening programs and corporate employee wellness examinations, is driving structured auto keratometer procurement investment across diagnostic center chains targeting ophthalmic service revenue expansion through 2033.

Regional Market Insights

North America Auto Keratometer Market Share

North America held a leading 36.8% share of the global auto keratometer market in 2025, driven by the U.S.'s high ophthalmic surgical volume, with over 4 million cataract procedures and 900,000 LASIK procedures annually generating mandatory pre-operative keratometry demand, FDA regulatory infrastructure ensuring premium auto keratometer adoption, and dense private ophthalmic clinic and ambulatory surgery center networks generating high per-facility device utilization and replacement procurement cycles.

U.S. Auto Keratometer Market: Myopia Surge & Surgical Growth

The U.S. market is estimated at US$ 2.4 Bn in 2026, anchored by Topcon, Nidek, and Zeiss premium benchtop auto keratometer placements at ambulatory surgery centers, Vision Source and MyEyeDr ophthalmic clinic chains, and academic medical centers. FDA 510(k) clearance frameworks sustain OEM market entry discipline. Canada contributes to the provincial health system ophthalmic clinic network procurement, and academic ophthalmology research institute device investment programs through 2033.

Europe Auto Keratometer Market Insights

Europe holds a 24.6% share of the global Auto Keratometer Market in 2025, driven by EU MDR 2017/745 compliance-driven device upgrade cycles, Germany's world-class ophthalmic technology manufacturing base hosting Zeiss and Haag-Streit headquarters, and comprehensive national health system ophthalmology coverage generating sustained public hospital auto keratometer procurement programs across Germany, France, the U.K., and the Nordics.

Germany Auto Keratometer Market: Premium Tech & NHS Procurement

Germany's market is estimated at US$ 414.6 Mn in 2026, anchored by Carl Zeiss Meditec AG's Jena headquarters R&D investment, Haag-Streit premium benchtop keratometer placements at university hospital ophthalmology departments, and Bundesgesundheitsministerium-funded cataract program keratometry investments. The U.K. contributes NHS ophthalmology department procurement. France sustains Essilor-linked ophthalmic clinic network device placements, while Spain contributes Zeiss and Topcon distributor network surgical center procurement programs through 2033.

Asia Pacific Keratometer Market Trends

Asia Pacific is the fastest-growing region at 7.3% CAGR by 2033, driven by China's national childhood myopia management program mandating keratometry-based screening at school health examination stations, India's expanding ophthalmic clinic infrastructure under Ayushman Bharat PM-JAY coverage, and Japan's aging population driving cataract surgery volumes requiring pre-operative keratometry at an estimated 1.5 million annual procedures.

China Auto Keratometer Market Trends

China's market is estimated at US$ 734.9 Mn in 2026, driven by National Health Commission myopia screening program handheld auto keratometer procurement and Aier Eye Hospital Group and He Eye Specialist Hospital surgical center investments. India's market at US$ 439.6 Mn is expanding through LV Prasad Eye Institute network growth and Sankara Nethralaya diagnostic center procurement. Japan contributes Topcon and Nidek domestic premium keratometer placements across Japan Ophthalmological Society-affiliated teaching hospital ophthalmology departments.

Competitive Landscape

The global Auto Keratometer Market is moderately consolidated, with Topcon, Nidek, and Carl Zeiss Meditec collectively commanding approximately 45-50% of global auto keratometer revenue in 2025. Key differentiators include measurement repeatability specifications within ±0.01D, integrated EHR connectivity, AI-assisted corneal irregularity flagging, and combined autorefractor-keratometer platform portfolios. Device-as-a-service procurement financing and cloud-based measurement data management platforms are emerging as competitive differentiators.

Integrated multifunction ophthalmic platform development combining keratometry, autorefraction, and corneal topography, geographic expansion into Asia Pacific pediatric myopia screening programs, and CE/FDA-compliant next-generation handheld device innovation define the dominant competitive strategic themes across global auto keratometer market participants.

Strategic Developments

- In January 2025, Carl Zeiss Meditec AG expanded its ophthalmic diagnostic instrument manufacturing and service center in Shanghai, China, investing €30 Mn to strengthen keratometry and refraction platform localization, regulatory approval, and service delivery for China's national myopia management program procurement expansion.

- In June 2024, EssilorLuxottica launched its Vision Care Connect platform, integrating auto keratometry data from its Visionix V500 multifunction device into a cloud-based patient vision health management platform for ophthalmic clinic chains, enabling longitudinal myopia progression keratometry tracking across pediatric patient populations.

Auto Keratometer Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.5 Bn |

| Current Market Value (2026) | US$ 7.4 Bn |

| Projected Market Value (2033) | US$ 11.1 Bn |

| CAGR (2026 - 2033) | 5.9% |

| Leading Region | North America |

| Dominant End User | Ophthalmic Clinics - 38.2% |

| Top-ranking Product Type | Handheld Auto Keratometer - 55.3% |

| Incremental Opportunity | US$ 3.7 Bn |

Companies Covered in Auto Keratometer Market

- Topcon Corporation

- Nidek Co., Ltd.

- Carl Zeiss Meditec AG

- Canon Inc.

- Canon Medical Systems

- EssilorLuxottica

- Haag-Streit Group

- TOMEY Corporation

- Reichert Technologies

- Luneau Technology Group

- Visionix

- Righton (Rexxam Co., Ltd.)

- GRAND SEIKO Co., Ltd.

- Potec Co., Ltd.

- BON Optic GmbH

Frequently Asked Questions

The auto keratometer market is valued at US$ 7.4 Bn in 2026, projected to reach US$ 11.1 Bn by 2033.

The WHO-recognized global myopia epidemic affecting 2.6 billion people mandating corneal screening and expanding cataract and refractive surgery volumes requiring mandatory pre-operative keratometry are the primary structural growth drivers.

The auto keratometer market is projected to grow at a CAGR of 5.94% from 2026 to 2033, building on a historical 5.14% CAGR from 2020 to 2026.

Integrated autorefractor-keratometer-topographer combination platform adoption and handheld auto keratometer deployment in Asia Pacific pediatric myopia national screening programs represent the highest-value actionable growth opportunities through 2033.

Topcon Corporation, Nidek Co., Carl Zeiss Meditec AG, Canon Medical Systems, EssilorLuxottica, Haag-Streit, TOMEY Corporation, Reichert Technologies, Luneau Technology Group, GRAND SEIKO, and Potec are the leading global market participants.