- Biotechnology

- Autologous Matrix-Induced Chondrogenesis (AMIC) Market

Autologous Matrix-Induced Chondrogenesis (AMIC) Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Autologous Matrix-Induced Chondrogenesis (AMIC) Market by Material (Hyaluronic Acid, Collagen, Polyethylene glycol (PEG), polylactic-co-glycolic acid (PGLA), Others), Application (Knee cartilage repair, Hip cartilage repair, Ankle cartilage repair, Others), End-user (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers (ASCs), Others), and Regional Analysis from 2026 to 2033

Autologous Matrix-Induced Chondrogenesis (AMIC) Market Share and Trends Analysis

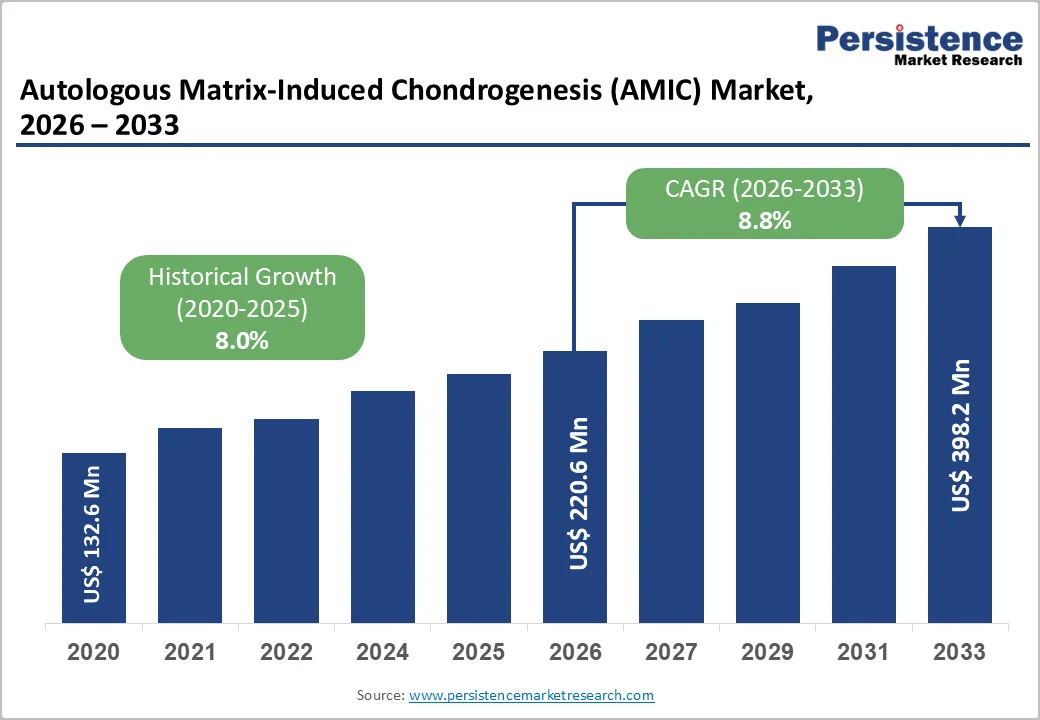

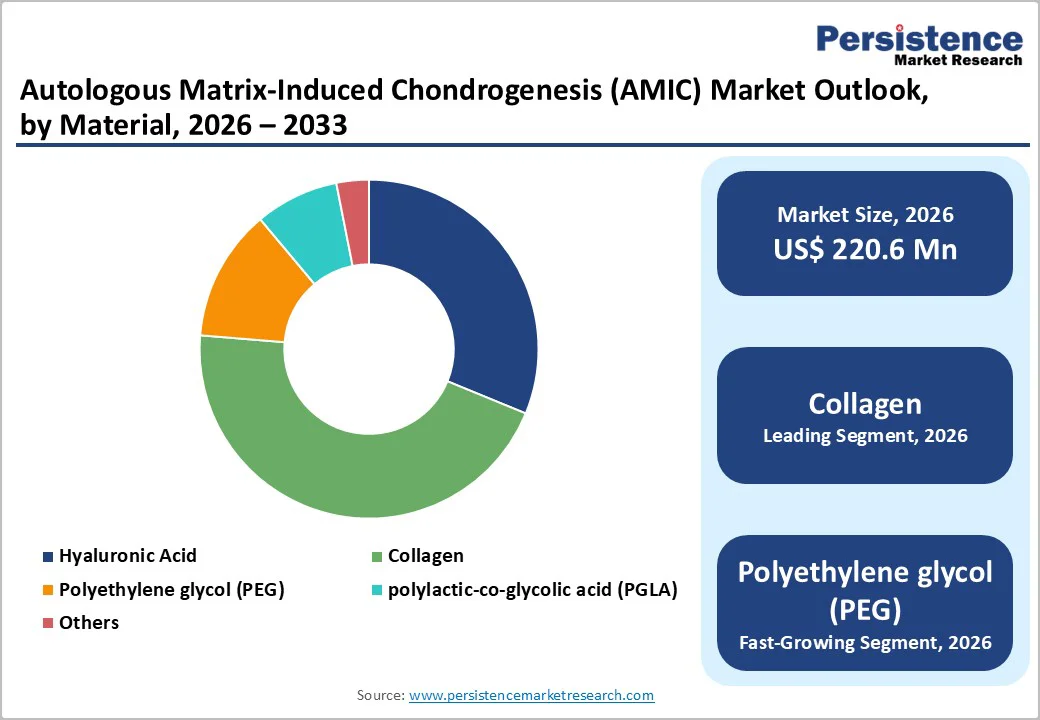

The global autologous matrix-induced chondrogenesis (AMIC) market size is estimated to grow from US$ 220.6 million in 2026 and projected to reach US$ 398.2 million by 2033.

The market is projected to record a CAGR of 8.8% from 2026 to 2033. The market is expected to grow steadily, driven by rising cartilage injuries, increasing prevalence of osteoarthritis, and growing demand for minimally invasive joint repair.

Key Industry Highlights

- Dominant Segment: Knee cartilage repair leads the 2025 AMIC market with 55.5% share, driven by rising osteoarthritis prevalence, sports- and injury-related cartilage damage, increasing preference for minimally invasive procedures, adoption of advanced biomaterial scaffolds, and expanding orthopedic surgeon expertise and hospital infrastructure.

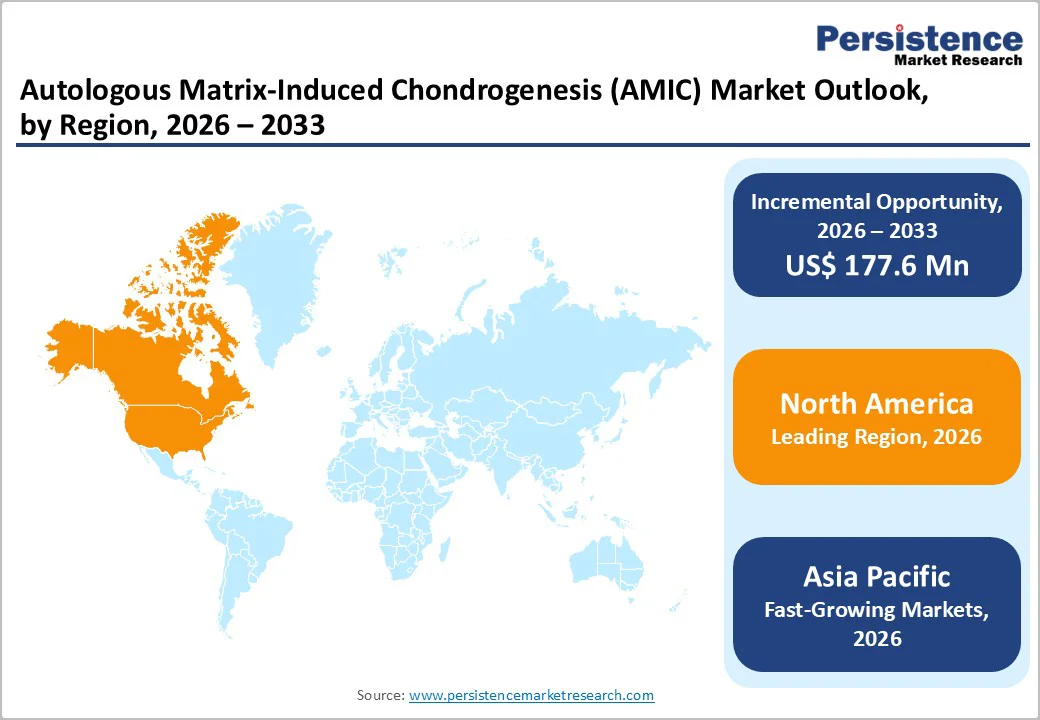

- Dominant Region: North America holds 41.6% share due to established healthcare infrastructure, surgeon experience, regulatory efficiency, and high adoption of advanced cartilage-repair procedures. Europe follows closely, while Asia-Pacific grows fastest, supported by expanding orthopedic centers, rising patient awareness, and increasing adoption of AMIC procedures using locally manufactured biomaterials.

- Market Drivers: Growth is driven by the increasing incidence of cartilage injuries and osteoarthritis, rising demand for minimally invasive joint repair, advances in biomaterials and scaffold technologies, expanding access to orthopedic care, and growing awareness among patients and surgeons of joint-preservation procedures.

- Market Opportunity: Key opportunities include the development of composite and hybrid scaffolds, the expansion of AMIC into hip, ankle, and other joints, the adoption of cost-effective and next-generation biomaterials, collaborations to improve scaffold designs, the integration of regenerative medicine techniques, and growth in emerging regions with increasing orthopedic care access and patient awareness.

| Key Insights | Details |

|---|---|

| Autologous Matrix-Induced Chondrogenesis Market Size (2026E) | US$ 220.6 Mn |

| Market Value Forecast (2033F) | US$ 398.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 8.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.0% |

Market Dynamics

Driver - Growing Adoption of Minimally Invasive Joint Repair Techniques

Growing adoption of minimally invasive joint-repair techniques is a key driver for the AMIC market, aligned with the rising global burden of cartilage damage. Symptomatic osteoarthritis affects approximately 528 million people worldwide, with the knee being the most frequently affected joint. The AMIC procedure, especially when performed arthroscopically, meets a huge demand by offering effective cartilage repair with reduced surgical trauma.

Studies indicate that arthroscopic AMIC achieves functional outcomes comparable to open surgery while lowering the risks of stiffness and revision. As outpatient and less-disruptive orthopedic care becomes standard, both patients and surgeons increasingly opt for AMIC procedures, fueling market growth and adoption of advanced cartilage-regeneration techniques.

Restraints - High Procedure and Biomaterial Costs

High costs of advanced cartilage-repair procedures are a major restraint for the AMIC market. In the United States, simpler cartilage repair procedures like microfracture average around $7,300 per patient, while cell- or scaffold-based techniques, including AMIC and autologous chondrocyte implantation, can range from $16,000 up to $23,000 depending on scaffold type and hospital stay.

Even though AMIC is less expensive than fully cell-based therapies, the procedure incurs costs for biomaterial scaffolds, operating room use, anesthesia, and postoperative care, which collectively add several thousand dollars compared to standard arthroscopic surgeries. In lower- and middle-income countries, such high out-of-pocket expenses restrict patient access, especially when insurance coverage is limited or absent.

These financial constraints reduce procedure adoption, limit market growth, and slow penetration in emerging regions. As a result, while AMIC offers effective cartilage repair and minimally invasive advantages, its high procedural and material costs remain a significant barrier to broader utilization.

Opportunity - Development of Advanced Biomaterials and Composite Scaffolds

Advances in biomaterials and composite scaffolds are unlocking new potential for AMIC by improving cartilage-regeneration outcomes and making the technique more reliable.

For example, a recent systematic review of hydrogel composite scaffolds demonstrated that such constructs more closely mimic the structural, mechanical, and biochemical properties of native cartilage than single-material scaffolds that support cell attachment, proliferation, and cartilage extracellular-matrix formation.

New nanocomposite hydrogels and fiber-reinforced hydrogel scaffolds have shown a ~80% increase in mechanical strength (compressive modulus) compared with traditional hydrogel scaffolds, while maintaining biocompatibility and allowing chondrocytes to produce cartilage-specific matrix.

Composite scaffolds incorporating natural and synthetic polymers (such as chitosan, hyaluronic acid, and gelatin) offer adjustable degradation rates, porosity, and biomechanical properties that closely match the healing timeline in cartilage repair. These innovations make AMIC more effective, durable, and suitable even for large or irregular defects, expanding its applicability beyond simple cartilage lesions.

Category-wise Analysis

By Material Insights

Collagen holds a 45.1% share of the global market in 2025, as it is the primary structural protein in the cartilage extracellular matrix, making it highly biocompatible, biodegradable, and biologically instructive for cartilage repair. Studies show that collagen type I and II hydrogels promote chondrogenic differentiation of mesenchymal stem cells and enhance glycosaminoglycan production, which is essential for a healthy cartilage matrix.

Collagen scaffolds closely mimic the native cartilage microenvironment, supporting cell adhesion, appropriate mechanical porosity, and nutrient diffusion, thereby promoting stable cartilage regeneration, high cell viability, and robust extracellular matrix deposition.

Their proven safety, effectiveness, and compatibility with arthroscopic AMIC procedures make collagen-based scaffolds the preferred choice among surgeons and biomaterial manufacturers, maintaining their dominant position in the market.

By Application Insights

Knee cartilage repair dominates the AMIC market with 55.5% share in 2025, because the knee is the most commonly affected joint in cartilage damage and osteoarthritis. Worldwide, knee osteoarthritis affects approximately 16% of adults aged 15 and older, rising to around 23% among those over 40, representing hundreds of millions of people with symptomatic knee cartilage issues.

The knee accounts for roughly 60-85% of all osteoarthritis cases, driven by age-related degeneration, sports injuries, and joint trauma. This large patient population creates strong demand for effective cartilage-repair procedures.

Consequently, surgeons and biomaterial developers focus primarily on knee applications, and most AMIC procedures target knee joints. This concentration of clinical need and procedure volume ensures that knee cartilage repair remains the dominant application segment in the AMIC market.

Regional Insights

North America Autologous Matrix-Induced Chondrogenesis (AMIC) Market Trends

North America dominates the autologous matrix-induced chondrogenesis (AMIC) market with a 41.6% share in 2025, driven by the high prevalence of osteoarthritis and other joint disorders, extensive orthopedic infrastructure, and widespread use of advanced cartilage-repair procedures.

In the United States, approximately 27.9% of adults report some form of arthritis, with nearly half affected by osteoarthritis. Around 1.77 million arthroscopic procedures are performed annually, reflecting significant procedural capacity, and knee arthroscopies increased almost 50% between 1996 and 2006.

The region also has a high number of experienced orthopedic surgeons, exceeding 20,000, and well-established reimbursement systems that improve patient access to scaffold-based treatments such as AMIC. This combination of disease burden, procedural infrastructure, and favorable healthcare and insurance frameworks positions North America as the dominant region in the global AMIC market.

Europe Autologous Matrix-Induced Chondrogenesis (AMIC) Market Trends

Europe is a significant region for the AMIC market due to a high burden of cartilage-related disorders and advanced orthopedic infrastructure. Approximately 101 million Europeans suffer from osteoarthritis, a 48% increase since 1990, while musculoskeletal disorders affect nearly 30% of the EU population. Knee osteoarthritis alone impacts over 40 million people, driving significant demand for cartilage-repair procedures.

Minimally invasive orthopedic surgeries, including arthroscopy and scaffold-based cartilage repair, are widely adopted as alternatives to joint replacement, particularly for working-age patients and early-stage disease. Strong healthcare systems, favorable reimbursement policies, and widespread access to specialized orthopedic centers support the uptake of procedures.

Combined, these factors position Europe as a stable and significant regional market for AMIC, with substantial potential for continued growth and innovation in cartilage-repair technologies.

Asia-Pacific Autologous Matrix-Induced Chondrogenesis (AMIC) Market Trends

Asia-Pacific is seeing rapid AMIC growth due to a rising burden of osteoarthritis and musculoskeletal disorders linked to ageing populations and shifting lifestyles. In 2021, the age-standardized prevalence of osteoarthritis in high-income Asia Pacific reached ~8,608 per 100,000, among the highest globally. The region now accounts for one of the fastest increases in knee osteoarthritis incidence and disability burden.

Countries such as China report knee OA prevalence around 28%, rising steeply with age and higher body-mass index. At the same time, expansion of orthopedic and regenerative-medicine infrastructure, broader access to surgical care, and growing awareness of joint-preservation techniques have boosted demand for cartilage-repair procedures like AMIC.

This convergence of high disease burden, unmet treatment need, and improving access to care drives Asia Pacific’s position as the fastest-growing AMIC region.

Competitive Landscape

Leading companies in the AMIC market focus on high-quality collagen and biomaterial scaffolds, innovative composite designs, and strict surgical compatibility. They invest in research, regenerative medicine, and scaffold development, partnering with orthopedic centers and hospitals to enhance procedure efficacy, patient outcomes, safety, and adoption, driving global market growth and expanding minimally invasive cartilage-repair solutions.

Key Industry Developments:

- In September 2025, A recent retrospective study reported positive outcomes for patients undergoing arthroscopic repair of talar osteochondral defects using a collagen-matrix scaffold (Chondro-Gide) under the Autologous Matrix-Induced Chondrogenesis (AMIC) technique. Sixteen patients with talus defects saw major improvement: the average ankle-function score (OMAS) rose from 30 pre-surgery to 72.7 at 12 weeks post-surgery, while mean pain (VAS) fell from 7.85 to 2.69. Most individuals reported restored ankle function and reduced discomfort.

Frequently Asked Questions

The global autologous matrix-induced chondrogenesis market is projected to be valued at US$ 220.6 million in 2026.

Rising cartilage injuries, osteoarthritis prevalence, demand for minimally invasive repair, advanced biomaterials, and growing orthopedic awareness drive the AMIC market.

The global autologous matrix-induced chondrogenesis market is poised to witness a CAGR of 8.8% between 2026 and 2033.

Opportunities include advanced scaffolds, composite biomaterials, stem cell integration, expansion to new joints, and growth in emerging orthopedic markets.

Anika Therapeutics, Inc., Arthro-Kinetics, B. Braun Melsungen AG, BioTissue AG, CartiHeal, Geistlich Pharma AG.