- Electrical Equipment & Services

- Asia Pacific Gas Leak Detectors Market

Asia Pacific Gas Leak Detectors Market Size, Share, and Growth Forecast 2026 - 2033

Asia Pacific Gas Leak Detectors Market by Product Type (Fixed Detectors and Portable Detectors), Technology (Electrochemical, Infrared, Semiconductor, Catalytic, and Others), Application (Industrial, Commercial, Residential, and Others), and Regional Analysis 2026 - 2033

Asia Pacific Gas Leak Detectors Market Size and Share Analysis

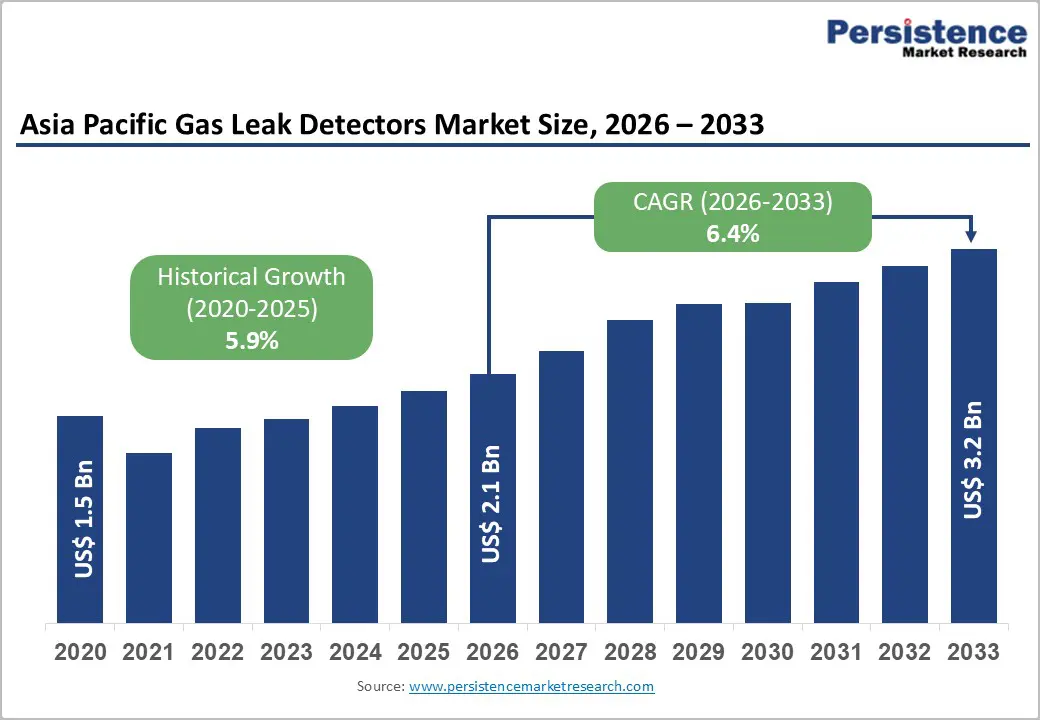

Asia Pacific gas leak detectors market size is likely to be valued at US$ 2.1 billion in 2026 and is projected to reach US$ 3.2 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

Market expansion is primarily driven by tightening industrial safety regulations, rapid industrialization in emerging Asian economies, and the increasing adoption of gas detection systems in the oil & gas, chemical, and urban residential infrastructure sectors. Governments across China, India, and ASEAN nations are enforcing stricter occupational safety mandates aligned with ILO and national disaster management frameworks, thereby compelling industries to invest in advanced leak-detection technologies.

Key Industry Highlights:

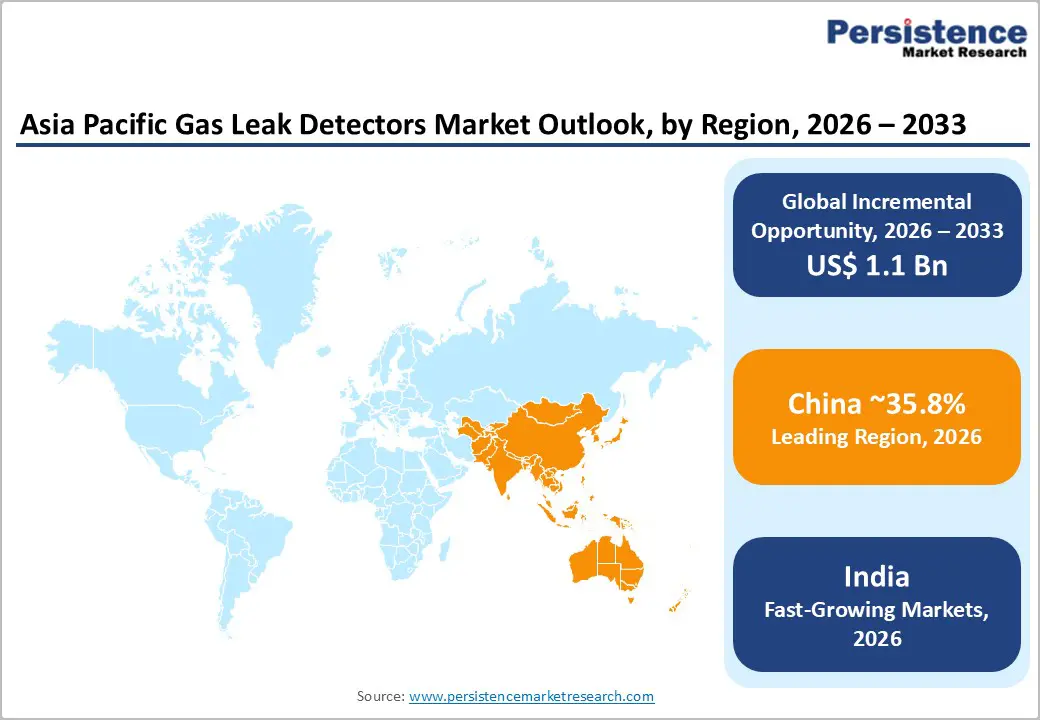

- Leading Country: China dominates the Asia-Pacific region with a 35.8% regional market share. Extensive industrial clusters, stringent GB 50325-2020 standards, municipal pipeline upgrades, and city-level ordinances requiring QR-coded LPG cylinder tracking position China as the primary regional market driver through 2033.

- Fastest-Growing Country: Southeast Asia's fastest-growing subregion, with an 8.5% CAGR; a USD 220 billion petrochemical and gas infrastructure investment pipeline; mandatory continuous monitoring requirements; and emerging regulatory frameworks, establishes

- Indonesia, Malaysia, Thailand, and Vietnam are the highest-growth opportunity zones.

- Dominant Product Type: Fixed Detectors account for 52% of the market. Mandatory continuous monitoring requirements in refineries, LNG terminals, and process industries drive fixed-detection penetration, with infrared and open-path laser systems commanding premium average selling prices.

- Fastest Growing Application: Industrial applications are the fastest growing at 7.2% CAGR, Oil and gas, chemical, and petrochemical sector expansion, coupled with rising safety mandates and hazard complexity, are accelerating detector adoption in upstream, midstream, and downstream operations.

- Key Market Opportunity: Hydrogen-specific detection represents a major market opportunity. Government support for a hydrogen economy across Japan, South Korea, and China, combined with specialized sensor development and regulatory requirements for hydrogen infrastructure, creates exceptional niche opportunities for technology innovators.

| Key Insights | Details |

|---|---|

| Asia Pacific Gas Leak Detectors Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 3.2 Bn |

| Projected Growth CAGR (2026 - 2032) | 6.4% |

| Historical Market Growth (2020 - 2025) | 5.9% |

Market Dynamics

Drivers - Stringent Industrial Safety and Environmental Regulations

Industrial safety enforcement across the Asia Pacific has intensified significantly over the past decade, directly accelerating the adoption of gas leak detection systems. Regulatory frameworks aligned with International Labour Organization (ILO) conventions and national safety laws mandate continuous gas monitoring in hazardous workplaces, including refineries, chemical plants, fertilizer units, and mining facilities. According to the ILO, more than 2.3 million work-related fatalities occur annually worldwide, with toxic gas exposure identified as a major industrial hazard.

Countries such as China, India, Japan, and South Korea have strengthened compliance inspections, imposing penalties, plant shutdowns, and insurance restrictions for non-compliance. In China, the Work Safety Law requires real-time detection systems in high-risk industries, while India’s Factory Act amendments emphasize gas monitoring in confined spaces. These regulatory pressures compel facility operators to deploy fixed and portable gas detectors not only for compliance but also to reduce operational downtime, litigation risk, and reputational damage, making safety instrumentation a non-discretionary investment.

Rapid Urbanization and Expansion of Gas Infrastructure

Rapid urbanization across the Asia-Pacific region is significantly increasing the risk of gas exposure in residential and commercial environments. According to the United Nations Department of Economic and Social Affairs, Asia accounts for over 50% of global urban population growth, driving massive expansion of city gas distribution networks. Governments are actively promoting the use of piped natural gas (PNG) and liquefied natural gas (LNG) to reduce reliance on coal and biomass.

According to the International Energy Agency, the Asia-Pacific region is the fastest-growing natural gas-consuming region through 2030, increasing the need for early leak detection in apartment complexes, hospitals, hotels, and commercial kitchens. Municipal authorities in India, China, and Japan increasingly mandate the installation of gas alarms in new residential buildings and public buildings. This structural shift toward gas-based urban energy systems is creating sustained demand for compact, affordable, and low-maintenance gas leak detectors across non-industrial end users.

Restraints - High Total Cost of Ownership and Budget Sensitivity Among SMEs

The high total cost of ownership (TCO) remains a significant constraint in the APAC gas leak detectors market, particularly for small and medium-sized enterprises (SMEs) operating under strict capital and operational budget constraints. While the upfront procurement cost of gas leak detectors is already a concern, the overall TCO extends far beyond initial installation. Expenses related to periodic calibration, sensor replacement, system upgrades, software licensing, and preventive maintenance substantially increase long-term financial commitments.

Compliance-driven investments often compete with production expansion, workforce costs, and energy expenses, forcing SMEs to opt for lower-cost, basic detection solutions or delay adoption altogether. The absence of flexible financing models, such as leasing or pay-per-use options, further limits affordability. Currency fluctuations and import dependence for advanced detection components in several APAC countries also introduce pricing volatility, thereby increasing procurement risk. As a result, SMEs often perceive gas leak detectors as a regulatory burden rather than a value-generating safety investment.

Limited Technical Expertise, Training Gaps, and System Misuse

Limited technical expertise and persistent training gaps pose another critical constraint for the APAC gas leak detectors market, particularly in emerging economies with fragmented industrial safety ecosystems. Advanced gas leak detection systems increasingly rely on digital interfaces, sensor networks, wireless connectivity, and data analytics, which require skilled personnel for correct installation, calibration, interpretation, and maintenance. Many industrial facilities, particularly SMEs, lack adequately trained safety engineers or instrumentation specialists. Inadequate training often leads to improper sensor placement, delayed calibration, and incorrect alarm threshold settings, resulting in false alarms or undetected leaks.

High workforce turnover in the manufacturing, construction, and utilities sectors across APAC exacerbates knowledge continuity challenges, making consistent system operation difficult. Language barriers, limited access to localized technical documentation, and insufficient after-sales support in remote or semi-urban areas further intensify the problem. In some cases, gas leak detectors are installed solely to meet compliance requirements and remain underutilized or switched off during routine operations.

Opportunities - Rapid Shift Toward Smart, Connected, and Data-Driven Safety Systems

The rapid digital transformation of industrial and commercial infrastructure across the Asia-Pacific region is creating significant growth opportunities for smart, connected, and data-driven gas leak detection systems. Traditional gas detectors function as isolated safety devices, whereas next-generation systems are increasingly integrated with IoT platforms, cloud analytics, and industrial automation networks. These systems enable continuous remote monitoring, real-time alerts, centralized dashboards, and predictive maintenance, capabilities that significantly enhance operational safety and efficiency.

Industries such as oil & gas, chemicals, semiconductors, and pharmaceuticals are adopting smart safety architectures to minimize unplanned downtime and reduce incident response times. Connected detectors can automatically transmit leak data to control rooms, trigger ventilation systems, and initiate emergency shutdown protocols without human intervention. This automation is particularly critical in large-scale industrial complexes and unmanned facilities, where manual inspection is impractical.

Insurers and regulators increasingly favor digital safety systems due to their ability to generate auditable safety logs and compliance reports. As enterprises across China, Japan, South Korea, and India accelerate adoption of smart factories and intelligent buildings, demand is shifting from standalone hardware toward integrated safety ecosystems.

Vendors offering software-enabled detectors, subscription-based monitoring, and analytics-driven insights are well-positioned to capture higher margins and long-term, recurring revenue, making this one of the most structurally attractive opportunities in the market.

Emergence of Hydrogen, LNG, and Alternative Gas Applications

The accelerating transition toward cleaner energy sources across the Asia Pacific is generating new and highly specialized demand for advanced gas leak detection technologies. Governments and energy operators are investing heavily in liquefied natural gas (LNG) terminals, hydrogen production facilities, gas-blending infrastructure, and alternative-fuel applications to meet decarbonization and energy-security goals. These developments significantly increase safety requirements, as hydrogen and LNG pose greater ignition and explosion risks than conventional fuels.

Hydrogen presents unique detection challenges due to its low molecular weight, high diffusion rate, and extremely low ignition energy. Even minor leaks can escalate rapidly, making early detection at very low concentration levels critical. Conventional catalytic or semiconductor sensors are often insufficient, driving demand for advanced infrared and electrochemical detection technologies capable of ultra-low ppm sensitivity and fast response times.

LNG infrastructure, including regasification plants, cryogenic storage tanks, and marine bunkering facilities, requires robust detection systems capable of operating under extreme temperature and pressure conditions. As the Asia Pacific emerges as the world’s largest LNG-importing region and a key hub for hydrogen pilot projects, safety regulations are evolving to mandate specialized detection systems for these environments. This shift creates premium growth opportunities for manufacturers with application-specific expertise, advanced sensor technologies, and compliance-ready solutions tailored to next-generation energy systems.

Category-wise Insights

Product Type Analysis

Fixed detectors maintains a dominant market position with approximately 52% market share, driven by mandatory continuous monitoring requirements in refineries, LNG terminals, power generation facilities, and process industries throughout the Asia Pacific region. Fixed detection systems provide permanent infrastructure monitoring for hazardous process areas, storage facilities, and equipment locations requiring uninterrupted surveillance and rapid alarm activation. Infrared point detectors configured for 0-100% LEL hydrocarbon measurement remain the default specification in process areas, while open-path laser systems guard perimeter fence lines and pipeline rights-of-way.

Fixed systems overcome installation challenges through standardized mounting architectures, integrated power management, and automated self-diagnostic capabilities ensuring reliability across extended operational periods.

Portable Detectors represent approximately 48% market share and are expanding at the accelerating rate of approximately 7.8% CAGR, driven by technological miniaturization enabling four-gas capabilities within palm-sized enclosures weighing under 100 grams, improving worker compliance and field mobility.

Calibration-free disposable single-gas units meet entry-level needs for SMEs, while sophisticated multi-gas models integrate man-down alarms, GPS positioning, and wireless connectivity. Transportable detectors bridge operational gaps during plant commissioning, pipeline hot-work operations, and emergency response scenarios, operating as stand-alone nodes with wireless backhaul to centralized command centers.

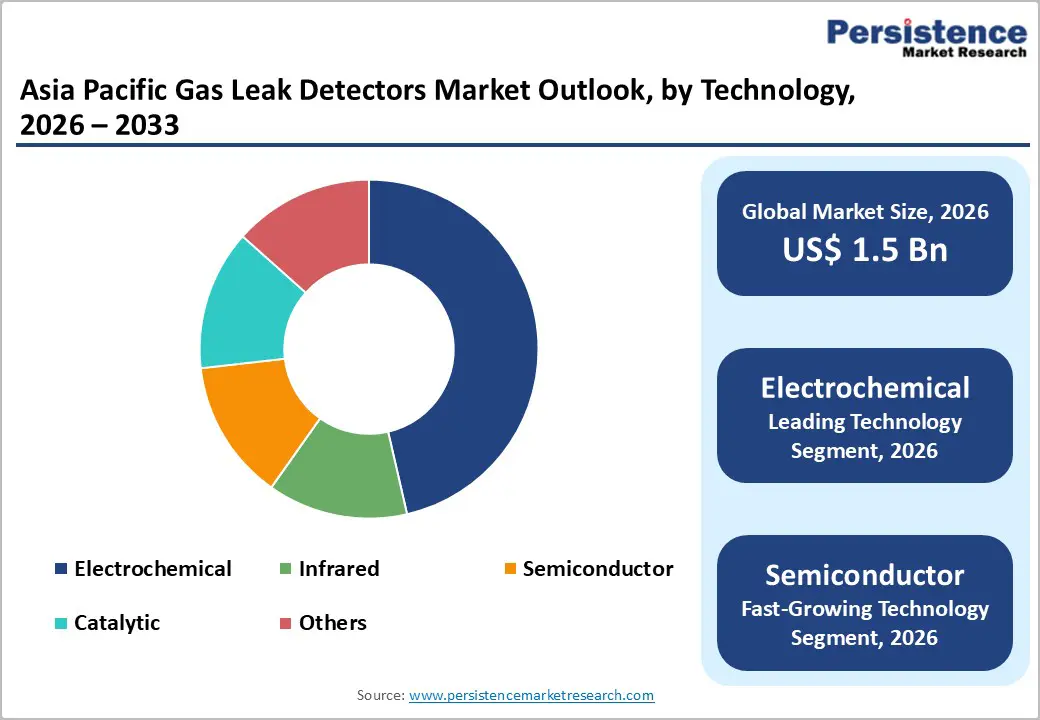

Technology Analysis

Electrochemical sensors maintain market dominance with approximately 36% market share, representing the most established technology for toxic gas detection across carbon monoxide, hydrogen sulfide, nitrogen dioxide, and chlorine applications. Electrochemical technology offers proven reliability, cost-effectiveness, and a proven track records across diverse industrial environments.

Infrared detection technology commands approximately 28% market share and is expanding at an accelerating rate through enhanced sensitivity for hydrocarbon measurement and compatibility with complex multi-component gas streams. Infrared systems provide non-contact measurement capabilities, rapid response times, and superior accuracy without requiring chemical reagents, establishing value in process industries and research applications.

Semiconductor-based sensors account for approximately 18% of the market and are expanding at a CAGR of approximately 8.2%, driven by miniaturization, which enables integration into portable and wearable detection devices. Catalytic bead technology maintains approximately 14% market share, particularly in combustible gas detection applications where proven reliability and straightforward implementation remain competitive advantages. Others, including ultrasonic, optical, and laser-based detection systems, account for approximately 4% of the market but are experiencing accelerated adoption in specialized applications, such as leak localization and long-range monitoring.

Application Insights

Industrial applications, including oil and gas, chemical, and petrochemical sectors, command approximately 54% market share, reflecting stringent process-safety mandates and comprehensive hazard spectrums spanning benzene, hydrogen sulfide, and combustible gases. Upstream and midstream projects in Malaysia, Thailand, and Australia specify triple-redundant fixed detector arrays, plus additions of flame and ultrasonic systems, thereby locking in elevated average selling prices and sustained capital equipment investments.

Commercial applications encompassing hospitals, hotels, restaurants, and commercial facilities represent approximately 28% market share, driven by indoor air quality requirements, natural gas distribution infrastructure monitoring, and regulatory mandates for occupancy safety. Residential applications account for approximately 18% market share, with increasing consumer awareness of carbon monoxide poisoning risks, natural gas safety, and formaldehyde off-gassing from building materials driving detector adoption in residential buildings and multifamily housing complexes throughout urban centers.

Regional Insights

China Gas Leak Detectors Market Trends

China represents the largest market within the Asia Pacific gas leak detectors market, accounting 35.8% share driven by rapid industrialization, strict safety regulations, and continuous expansion of energy infrastructure. The country’s strong presence in oil & gas, chemicals, mining, power generation, and urban gas distribution has made gas leak detection systems a mandatory safety component across most industrial facilities.

Regulatory enforcement by national and provincial authorities is pushing industries to upgrade from conventional detectors to smart, IoT-enabled, and wireless gas leak detection systems that offer real-time monitoring, predictive maintenance, and centralized data management. Another key trend in China is the growing adoption of fixed gas detectors in large-scale manufacturing plants and pipeline networks, supported by extensive investments in smart factories and industrial automation.

Domestic manufacturers are focusing on cost-competitive sensor technologies and localized certifications, enabling wider penetration among small and mid-sized enterprises. Urbanization and the expansion of residential and commercial gas networks are also increasing demand for household and building-level gas leak alarms. Overall, China’s market trend is characterized by regulation-led adoption, technological advancement, and large-volume deployments, positioning the country as the primary growth engine for gas leak detectors in the APAC.

India Gas Leak Detectors Market Trends

India is emerging as one of the fastest-growing markets for gas leak detectors in the APAC region, supported by industrial growth, expanding city gas distribution networks, and rising awareness of workplace and public safety. The government’s focus on industrial safety compliance, infrastructure development, and the expansion of energy access has significantly increased demand for both fixed and portable gas leak detectors.

Key end-use sectors include manufacturing, oil & gas, chemicals, power generation, construction, and municipal utilities, where safety audits and compliance requirements are becoming more stringent. A notable trend in India is the rapid expansion of city gas distribution (CGD) projects, which is driving demand for gas detection systems across pipelines, compressor stations, and residential connections.

Smart city initiatives and modernization of industrial facilities are encouraging the adoption of digital and wireless gas detection technologies. While cost sensitivity remains a challenge, increasing domestic manufacturing under national industrial initiatives is improving affordability and accessibility.

As a result, India’s gas leak detectors market trend is defined by high growth momentum, infrastructure-driven demand, and gradual technological upgrading, making it a key contributor to the long-term expansion of the APAC gas leak detectors market.

Competitive Landscape

The APAC gas leak detectors market exhibits moderate consolidation among dominant global suppliers, including Honeywell International, Emerson Electric, Thermo Fisher Scientific, Drägerwerk, and General Electric, collectively commanding approximately 58% aggregated market share through comprehensive product portfolios, established distribution networks, and advanced research capabilities.

Market leaders pursue expansion through strategic acquisition of specialized detection manufacturers, establishment of enterprise partnerships with major industrial operators, and substantial research and development investment in emerging technologies, including artificial intelligence-driven false alarm reduction and wireless sensor network integration.

Honeywell's comprehensive safety solutions portfolio spanning detection, monitoring, and analytics platforms, exemplifies integrated business model trends combining hardware with digital services. Emerson Electric's focus on industrial process automation positions the company as a preferred supplier for integrated control systems incorporating gas detection. Dräger's emphasis on digital safety platforms represents emerging business model trends emphasizing cloud-connected ecosystem services. Mid-sized regional suppliers maintain competitive positions through specialization in specific industrial segments, geographic markets, or advanced technology niches, with local manufacturers increasingly leveraging cost advantages and regulatory knowledge to penetrate SME segments.

Key Market Developments

- In September 2025, Emerson Electric Announces Wireless Connectivity Integration for Asia Pacific Industrial Facilities - Emerson Electric deployed a wireless sensor network integration, enabling real-time data transmission from gas detector arrays to be centralized on monitoring platforms. Technology substantially reduces installation costs through the elimination of hardwired cable infrastructure, accelerating adoption in brownfield facility retrofitting projects throughout the region.

- In December 2024, Honeywell International Launches AI-Enabled False Alarm Reduction for Multi-Gas Detection Systems - Honeywell International introduced advanced artificial intelligence algorithms for gas detector networks, enabling sophisticated pattern recognition distinguishing authentic leak signatures from environmental noise and sensor artifacts. The innovation significantly reduces false alarm rates while maintaining superior detection sensitivity and regulatory compliance capabilities.

- In June 2024, Thermo Fisher Scientific Expands Hydrogen Detection Capabilities Supporting Emerging Hydrogen Economy - Thermo Fisher Scientific unveiled specialized hydrogen-specific detection systems featuring palladium-alloy catalytic sensors achieving sub-0.4% LEL sensitivity thresholds for hydrogen applications. The product expansion aligns with expanding hydrogen infrastructure initiatives throughout Japan, South Korea, and China

Companies Covered in Asia Pacific Gas Leak Detectors Market

- Honeywell International, Inc.

- Emerson Electric Co.

- Thermo Fisher Scientific Inc.

- Drägerwerk AG & Co. KGaA

- General Electric

- MSA

- United Technologies Corporation

- Tyco International plc.

- Industrial Scientific

- New Cosmos Electric Co. Ltd.

- Riken Keiki Co., Ltd.

- Hanwei Electronics

- Teledyne Technologies

- INFICON

- Siemens AG

Frequently Asked Questions

The Asia Pacific gas leak detectors market was valued at US$ 2.1 billion in 2026 and is projected to reach US$ 3.2 billion by 2033, expanding to a 6.4% CAGR. This consistent growth trajectory reflects intensifying regulatory mandates, rapid industrial expansion, and accelerating adoption of advanced detection technologies across oil and gas, chemical, petrochemical, and commercial sectors throughout the Asia Pacific region.

Primary growth drivers include stringent workplace safety regulations, including Malaysia's Occupational Safety and Health Amendment 2022, South Korea's mandatory five-gas measurement standards, and China's GB 50325-2020 building safety requirements. Massive petrochemical, oil, and gas infrastructure investments, LNG facilities, and processing complexes drive continuous monitoring requirements.

Fixed detectors dominate with approximately 52% market share, driven by mandatory continuous monitoring requirements in refineries, LNG terminals, and process industries. Portable Detectors represent 48% market share and expand at an accelerating 7.8% CAGR driven by miniaturization, wireless connectivity, and worker safety compliance improvements.

China maintains market leadership with approximately 35.8% regional market share through extensive industrial clusters, stringent regulatory standards, and municipal infrastructure upgrades. Southeast Asia, including Indonesia, Malaysia, Thailand, and Vietnam, emerges as the fastest-growing sub-region with 8.5% CAGR, driven by a USD 220 billion petrochemical investment pipeline and mandatory continuous monitoring requirements.

Hydrogen-economy infrastructure development across Japan, South Korea, and China represents exceptional opportunity, with government support programs mandating hydrogen-specific detection systems. Digital ecosystem integration enabling predictive maintenance optimization, artificial intelligence-driven false alarm reduction, and cloud-connected monitoring platforms creates sustainable service revenue opportunities extending beyond traditional detector sales into recurring software licensing models.

Market leaders include Honeywell International leveraging comprehensive safety solutions and AI-driven analytics platforms, Emerson Electric combining industrial automation expertise with integrated detection systems, Thermo Fisher Scientific specializing in advanced analytical detection technologies, Drägerwerk emphasizing digital safety platforms and intrinsically safe product design, General Electric, MSA, and regional specialists including New Cosmos Electric, Riken Keiki, and Hanwei Electronics capturing cost-sensitive SME segments through localized solutions and regulatory expertise.