- Pharmaceuticals

- Global Anti-Vascular Endothelial Growth Factor Therapeutics Market

Global Anti-Vascular Endothelial Growth Factor Therapeutics Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Anti-Vascular Endothelial Growth Factor Therapeutics Market by Product (Eylea, Lucentis, Beovu, Vabysmo, and Others), by Application (Macular Edema, Diabetic Retinopathy, Retinal Vein Occlusion, Age-related Macular Degeneration, Myopic Choroidal Neovascularization, and Others), by End User (Hospitals, Ophthalmology Centers, Ambulatory Surgical Centers (ASCs), and Others), and Regional Analysis from 2026 to 2033.

Anti-Vascular Endothelial Growth Factor Therapeutics Market Share and Trend Analysis

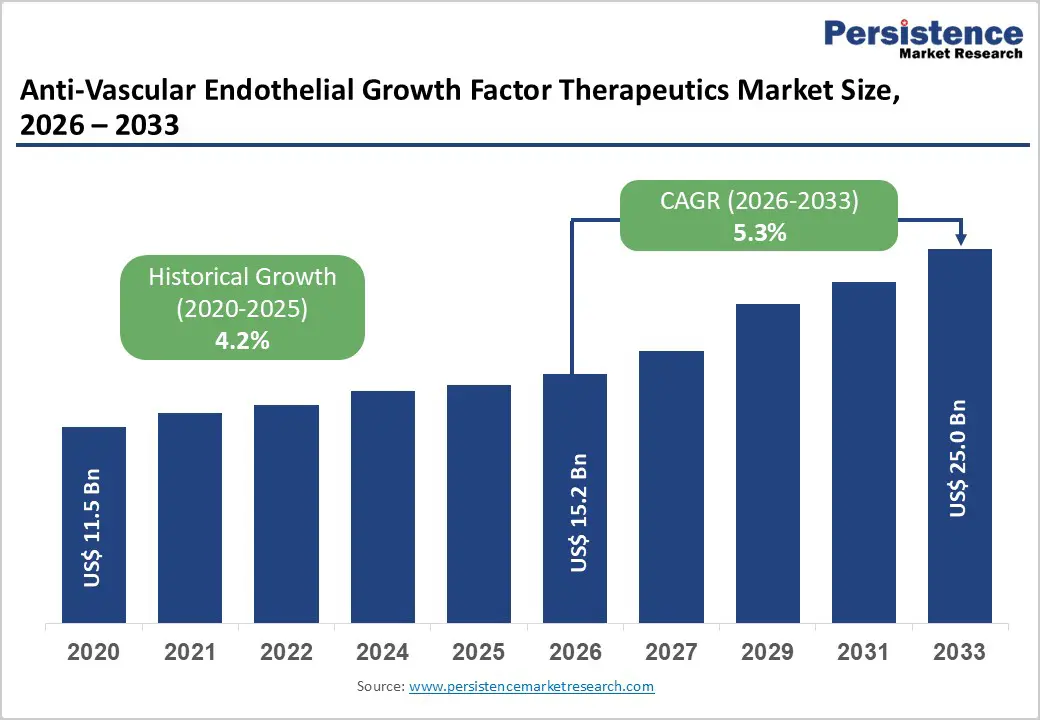

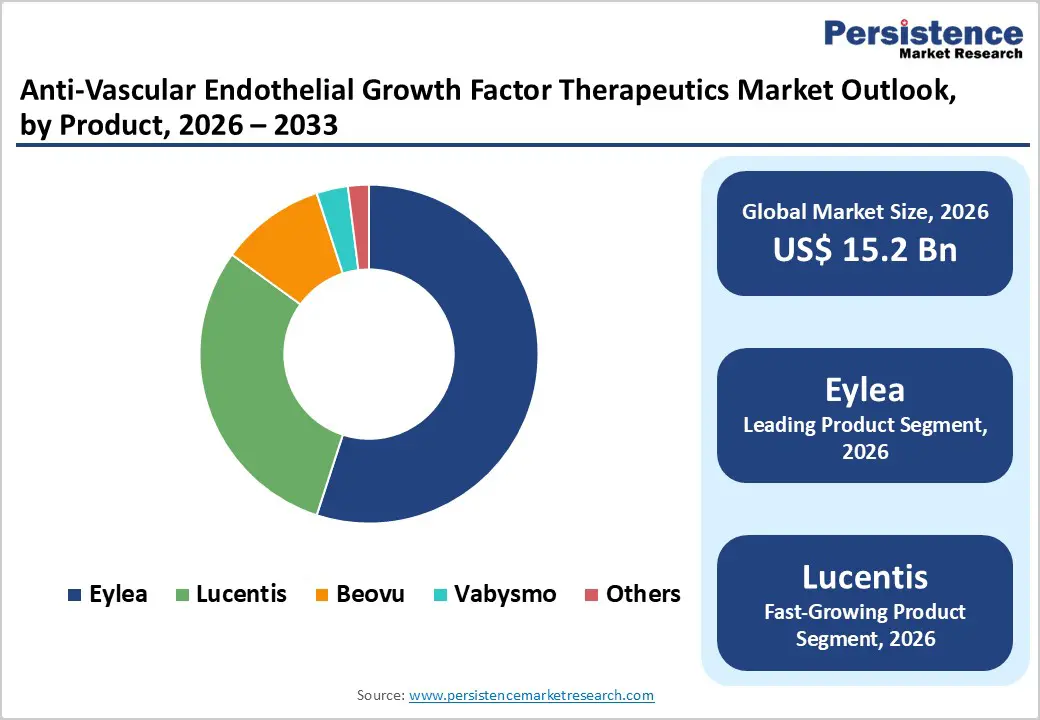

The global anti-vascular endothelial growth factor therapeutics market size is estimated to grow from US$ 15.2 Bn in 2026 to US$ 25.0 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for anti-vascular endothelial growth factor therapeutics is increasing steadily, driven by the rising prevalence of retinal disorders such as age-related macular degeneration, diabetic retinopathy, diabetic macular edema, and retinal vein occlusion. Aging populations, increasing diabetes incidence, and longer life expectancy are significantly expanding the patient base requiring long-term anti-VEGF treatment. Improved awareness of vision-threatening retinal diseases and wider access to ophthalmology services are accelerating diagnosis and treatment initiation across both developed and emerging markets. Anti-VEGF therapies are widely adopted as the standard of care due to their proven clinical efficacy in inhibiting abnormal blood vessel growth and preserving vision. Growing emphasis on early intervention, disease monitoring, and long-term visual outcomes continues to support sustained therapy demand. Expansion of specialty eye hospitals, increasing availability of trained retinal specialists, and rising healthcare expenditure are further strengthening market growth. Technological advancements in biologics, including improved molecular design, extended dosing intervals, and next-generation formulations, are enhancing treatment durability and patient adherence. Additionally, improving reimbursement frameworks and expanding healthcare infrastructure in emerging economies are reinforcing long-term global demand for anti-VEGF therapeutics.

Key Industry Highlights

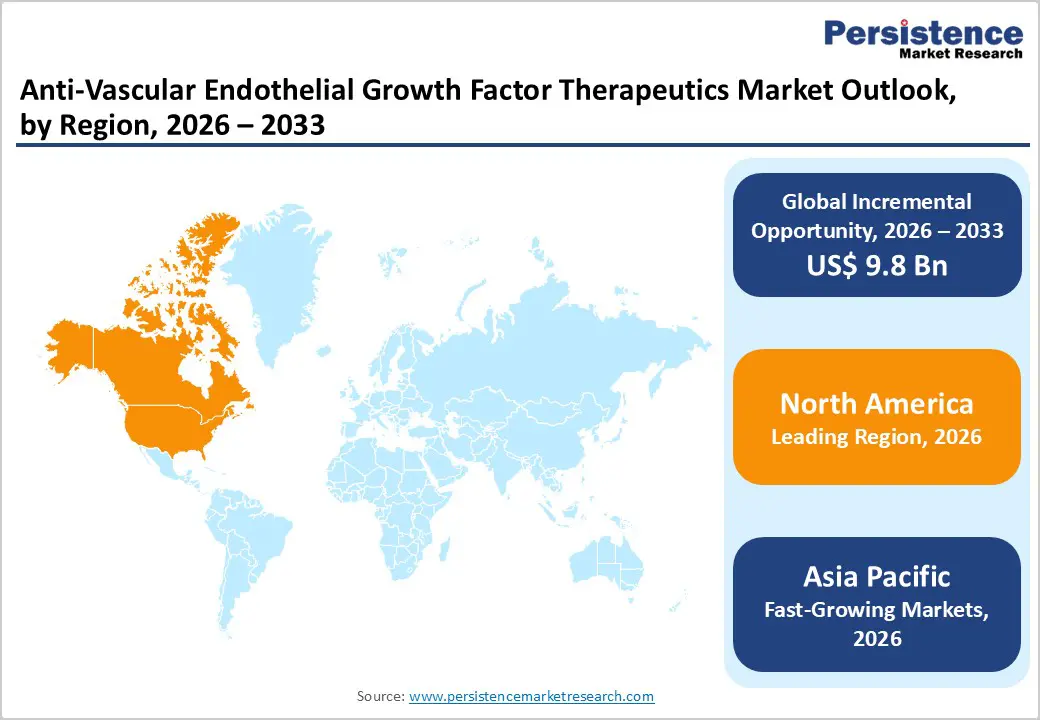

- Leading Region: North America holds the largest share at 47.3%, supported by a high prevalence of retinal disorders, strong reimbursement coverage, advanced ophthalmic infrastructure, early adoption of innovative biologics, and a strong presence of leading pharmaceutical companies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rising diabetes prevalence, rapidly aging populations, increasing healthcare spending, improving access to ophthalmic care, government-supported vision programs, and expanding specialty eye hospital networks.

- Leading Product Segment: Eylea dominates the market due to strong clinical efficacy, extended dosing intervals, broad regulatory approvals, favorable reimbursement, and widespread physician adoption across major retinal indications.

- Fastest-Growing Product Segment: Lucentis is growing rapidly as demand increases for established, clinically validated anti-VEGF therapies, supported by expanding use in emerging markets and growing biosimilar penetration.

- Leading Disease Segment: Age-related macular degeneration remains the top segment, driven by high disease prevalence among elderly populations and the need for continuous, long-term anti-VEGF treatment.

- Fastest-Growing Disease Segment: Diabetic retinopathy is scaling quickly due to the global rise in diabetes cases, earlier screening, and increasing focus on preventing vision loss through timely therapeutic intervention.

| Key Insights | Details |

|---|---|

|

Anti-Vascular Endothelial Growth Factor Therapeutics Market Size (2026E) |

US$ 15.2 Bn |

|

Market Value Forecast (2033F) |

US$ 25.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Dynamics

Driver – Rising Burden of Retinal Disorders, Aging Population, and Advancements in Biologic Therapies

Market expansion is strongly supported by the growing global burden of retinal vascular diseases, including age-related macular degeneration, diabetic retinopathy, diabetic macular edema, and retinal vein occlusion. The rapid increase in elderly populations, particularly in developed economies, has significantly elevated the incidence of chronic vision-threatening conditions that require long-term anti-VEGF treatment. In parallel, the global diabetes epidemic continues to expand the patient pool vulnerable to retinal complications, further reinforcing sustained therapy demand.

Clinical guidelines widely recognize anti-VEGF agents as the standard of care for multiple retinal indications, driving consistent utilization across hospitals and specialized ophthalmology centers. Improvements in early diagnosis through advanced retinal imaging technologies have increased treatment initiation rates, while growing patient awareness has improved adherence to therapy. Additionally, continuous innovation in biologics such as higher binding affinity, improved durability, and reduced injection frequency has enhanced treatment outcomes and physician confidence. Favorable reimbursement coverage in mature markets and expanding access to ophthalmic care in developing regions further support adoption. Together, epidemiological trends, therapeutic efficacy, and healthcare system readiness are creating a strong and durable growth foundation.

Restraints – High Treatment Costs, Injection Burden, and Access Inequalities

Despite strong clinical demand, market growth is constrained by the high cost of branded anti-VEGF biologics, particularly in low- and middle-income countries. Repeated intravitreal injections, often required over extended periods, increase cumulative treatment expenses for patients and healthcare systems, limiting affordability and adherence. In regions with limited reimbursement coverage, out-of-pocket costs remain a significant barrier, leading to delayed or discontinued treatment.

Clinical administration requirements also present challenges, as intravitreal injections must be performed by trained ophthalmologists in controlled medical settings, restricting access in rural and underserved areas. Capacity constraints within public hospitals and long waiting times can further limit timely therapy initiation. Safety concerns related to injection-associated complications, though relatively low, may discourage some patients from continuing long-term therapy. Additionally, strict regulatory approval pathways and pricing pressures imposed by government healthcare authorities can slow product launches and restrict premium pricing strategies. Variability in healthcare infrastructure across regions continues to create uneven treatment penetration, moderating overall market expansion.

Opportunity – Biosimilars, Longer-Acting Therapies, and Emerging Market Penetration

Significant growth potential lies in the expanding availability of biosimilar anti-VEGF agents, which are improving affordability and broadening patient access, particularly in cost-sensitive healthcare systems. As biosimilars gain regulatory approvals and clinical acceptance, they are expected to accelerate treatment uptake while intensifying price competition. Another major opportunity is the development of longer-acting formulations and sustained-release delivery technologies aimed at reducing injection frequency and improving patient compliance.

Emerging economies across Asia Pacific, Latin America, and parts of the Middle East present substantial untapped potential due to rising disease awareness, expanding ophthalmology infrastructure, and improving healthcare coverage. Government-led vision care initiatives and increasing private investment in specialty eye hospitals are strengthening diagnosis and treatment rates. Additionally, pipeline innovation involving dual-pathway inhibitors and next-generation biologics offers opportunities for differentiation and premium positioning. Strategic collaborations between pharmaceutical companies, hospitals, and research institutions are also accelerating clinical development and geographic expansion. As healthcare systems increasingly prioritize outcomes, convenience, and cost efficiency, the anti-VEGF therapeutic landscape is well positioned for long-term structural growth.

Category-wise Analysis

By Product, Eylea Leads Due to Strong Clinical Efficacy, Extended Dosing Interval, and Broad Physician Adoption

Eylea is projected to dominate the global anti-vascular endothelial growth factor therapeutics market in 2026, accounting for a revenue share of 55.0%. Its leadership is primarily supported by strong clinical efficacy across multiple retinal indications, including age-related macular degeneration and diabetic macular edema, along with an extended dosing interval that reduces treatment burden. Favorable real-world outcomes, long-term safety data, and widespread physician familiarity have reinforced its position as a first-line therapy in many treatment protocols. Additionally, extensive global commercialization, strong reimbursement coverage in developed markets, and approvals across diverse geographies have contributed to sustained uptake. Eylea’s ability to address both treatment-naïve and previously treated patients further strengthens its market presence. Continued lifecycle management strategies and expanding use across retinal disorders are expected to sustain its leadership despite increasing competition from newer agents.

By Disease, Age-related Macular Degeneration Leads Due to High Disease Burden and Long-term Treatment Demand

The age-related macular degeneration segment is expected to dominate the global anti-vascular endothelial growth factor therapeutics market in 2026, capturing a revenue share of 46.5%. This dominance is driven by the high prevalence of AMD among aging populations and the chronic nature of the disease, which requires long-term and repeated anti-VEGF treatment. Wet AMD remains one of the leading causes of irreversible vision loss globally, prompting early diagnosis and aggressive therapeutic intervention. Increased awareness, improved access to ophthalmic care, and advancements in diagnostic imaging have further expanded the treated patient pool. Anti-VEGF therapies are widely established as the standard of care for wet AMD, reinforcing consistent demand. Moreover, rising life expectancy and expanding elderly demographics across both developed and emerging markets continue to support sustained growth of this segment.

By End User, Hospitals Lead Due to High Treatment Volumes and Advanced Ophthalmology Infrastructure

Hospitals are projected to dominate the global anti-vascular endothelial growth factor therapeutics market in 2026, accounting for a revenue share of 60.0%. This dominance is attributed to high patient volumes, availability of specialized retina care units, and access to trained ophthalmologists capable of administering intravitreal injections. Hospitals often serve as primary referral centers for complex retinal disorders, including advanced AMD and diabetic retinopathy, driving consistent utilization of anti-VEGF therapies. Integration of ophthalmology departments within multispecialty hospitals enables comprehensive disease management, from diagnosis to follow-up treatment. Additionally, hospitals benefit from stronger reimbursement mechanisms, bulk procurement capabilities, and participation in clinical research programs. While specialty eye clinics are expanding rapidly, hospitals continue to lead due to institutional trust, advanced infrastructure, and their central role in managing severe and chronic retinal conditions.

Region-wise Insights

North America Anti-Vascular Endothelial Growth Factor Therapeutics Market Trends

North America is expected to dominate the global anti-vascular endothelial growth factor therapeutics market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a high prevalence of retinal disorders such as age-related macular degeneration and diabetic retinopathy, supported by an aging population and rising diabetes incidence. Strong awareness of eye health, early diagnosis rates, and widespread access to advanced ophthalmic care have significantly increased treatment uptake. Favorable reimbursement frameworks, including Medicare coverage for anti-VEGF therapies, play a critical role in sustaining demand.

The presence of major pharmaceutical companies and early adoption of innovative biologics further strengthen market leadership. Additionally, robust clinical research activity, rapid regulatory approvals, and frequent introduction of next-generation therapies contribute to sustained growth. High healthcare spending and physician preference for evidence-based treatments are expected to maintain North America’s dominance throughout the forecast period.

Europe Anti-Vascular Endothelial Growth Factor Therapeutics Market Trends

The Europe anti-vascular endothelial growth factor therapeutics market is expected to grow steadily, supported by strong public healthcare systems and high clinical standards across countries such as Germany, the U.K., France, Italy, and Spain. An expanding elderly population and increasing incidence of age-related retinal diseases continue to drive demand for anti-VEGF therapies. Universal healthcare coverage in many European countries facilitates patient access to biologic treatments, although cost-containment measures influence product selection.

Hospitals and specialized ophthalmology centers remain the primary treatment settings, supported by well-established referral networks. The growing adoption of biosimilars is improving affordability and expanding patient reach, particularly in cost-sensitive healthcare systems. Regulatory emphasis on safety, efficacy, and pharmacovigilance supports sustained confidence in approved therapies. As screening programs expand and treatment penetration improves, Europe is expected to maintain stable long-term growth.

Asia Pacific Anti-Vascular Endothelial Growth Factor Therapeutics Market Trends

The Asia Pacific anti-vascular endothelial growth factor therapeutics market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by expanding healthcare infrastructure, rising disease awareness, and improving access to ophthalmic care. Countries such as China, India, Japan, South Korea, and Australia are witnessing rapid growth in diabetic retinopathy and age-related macular degeneration due to aging populations and lifestyle changes.

Increasing government focus on vision care programs and expansion of specialty eye hospitals are significantly improving diagnosis and treatment rates. Growing penetration of health insurance and availability of cost-effective biosimilars are further supporting market accessibility. Additionally, local manufacturing capabilities and strategic entry of global pharmaceutical players are strengthening regional supply chains. With rising disposable incomes and improving healthcare coverage, Asia Pacific is expected to emerge as the fastest-growing regional market.

Market Competitive Landscape

The global anti-vascular endothelial growth factor therapeutics market is highly competitive, with strong participation from companies such as Regeneron Pharmaceuticals, Inc., Bayer AG, Novartis AG, F. Hoffmann-La Roche Ltd., Biogen, and Pfizer, Inc. These players leverage extensive global commercialization capabilities, strong brand recognition, and diversified biologics and ophthalmology-focused portfolios to address the rising demand for effective and durable anti-VEGF therapies across retinal disorders.

Their product offerings emphasize high clinical efficacy, prolonged dosing intervals, improved patient adherence, and favorable safety profiles, supported by advances in biologics engineering and drug-delivery technologies. Continuous innovation in next-generation anti-VEGF agents, lifecycle management strategies, regulatory compliance, and adherence to stringent manufacturing and quality standards remain critical for maintaining competitive positioning in the global anti-VEGF therapeutics market.

Key Industry Developments:

- In October 2025, China Medical System Holdings entered into a distribution agreement with Novartis Pharma Services AG granting exclusive rights to import, distribute, sell, and promote Ranibizumab (Lucentis®) and Brolucizumab (Beovu®) in mainland China (excluding Hong Kong, Macau, and Taiwan), expanding access to these anti-VEGF therapies for retinal diseases including neovascular age-related macular degeneration, diabetic macular edema, and other ocular neovascular conditions.

Companies Covered in Global Anti-Vascular Endothelial Growth Factor Therapeutics Market

- Regeneron Pharmaceuticals, Inc.

- Bayer AG

- Novartis AG

- F. Hoffmann-La Roche Ltd.

- Biogen

- Pfizer, Inc.

- Coherus BioSciences, Inc.

- Amgen, Inc.

- Bausch Health Companies, Inc.

- Viatris, Inc.

- Biogen

- Others

Frequently Asked Questions

The global anti-vascular endothelial growth factor therapeutics market is projected to be valued at US$ 15.2 Bn in 2026.

The market is principally driven by the escalating prevalence of ophthalmic diseases such as age-related macular degeneration, diabetic retinopathy, macular edema and retinal vein occlusion especially among aging populations and global increases in diabetes alongside expanding healthcare infrastructure and ongoing R&D for novel formulations and delivery systems.

The global anti-vascular endothelial growth factor therapeutics market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Expansion into emerging markets through biosimilar adoption and novel long-acting delivery systems offers substantial growth potential.

Regeneron Pharmaceuticals, Inc., Bayer AG, Novartis AG, F. Hoffmann-La Roche Ltd., Biogen, and Pfizer, Inc., are some of the key players in the anti-vascular endothelial growth factor therapeutics market.