- Pharmaceuticals

- Global Ankle Arthritis Treatment Market

Global Ankle Arthritis Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Ankle Arthritis Treatment Market by Drug (Corticosteroids, Non-steroidal Anti-inflammatory Drugs (NSAIDs), Steroids, Analgesics, Pain relievers, Anti-rheumatic drugs), by Route of Administration (Oral, Topical, Intravenous, Parenteral), by Indication, by Distribution Channel, by Regional Analysis, 2026-2033

Market Overview

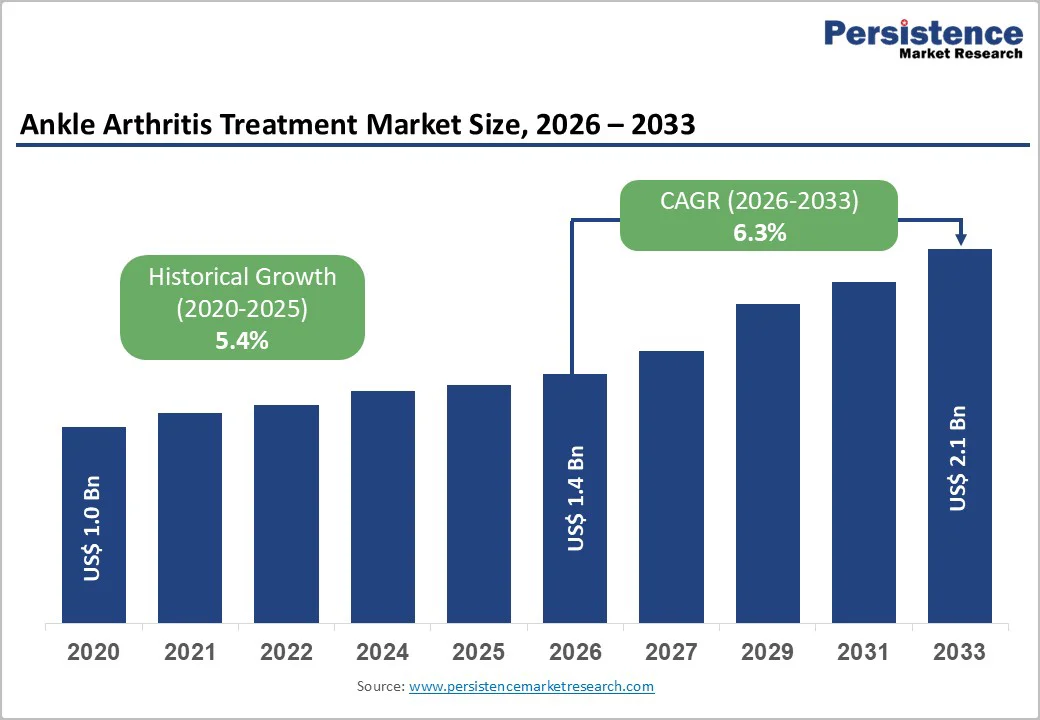

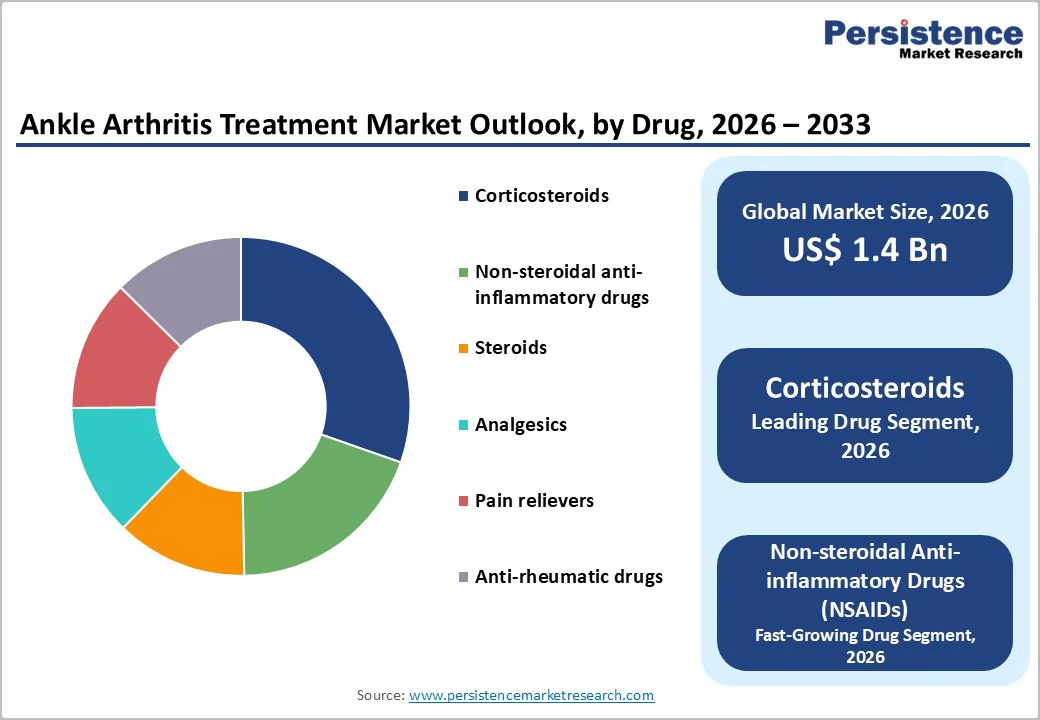

The global ankle arthritis treatment market size is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The rising burden of ankle osteoarthritis and post-traumatic joint damage among aging as well as athletic populations is accelerating demand for pharmacologic pain control and inflammation management across care settings. Increasing recognition that about 3.4% of adults over 50 years live with radiographic ankle osteoarthritis and that up to 70–80% of ankle osteoarthritis is post-traumatic is pushing clinicians to initiate earlier and more aggressive medical management to delay surgery. Clinical guidelines favor stepwise use of NSAIDs, intra-articular corticosteroids, and adjunctive pain relievers, while emerging biologic and orthobiologic options are gaining visibility as payers and providers seek therapies that can reduce disability and preserve function.

Key Industry Highlights

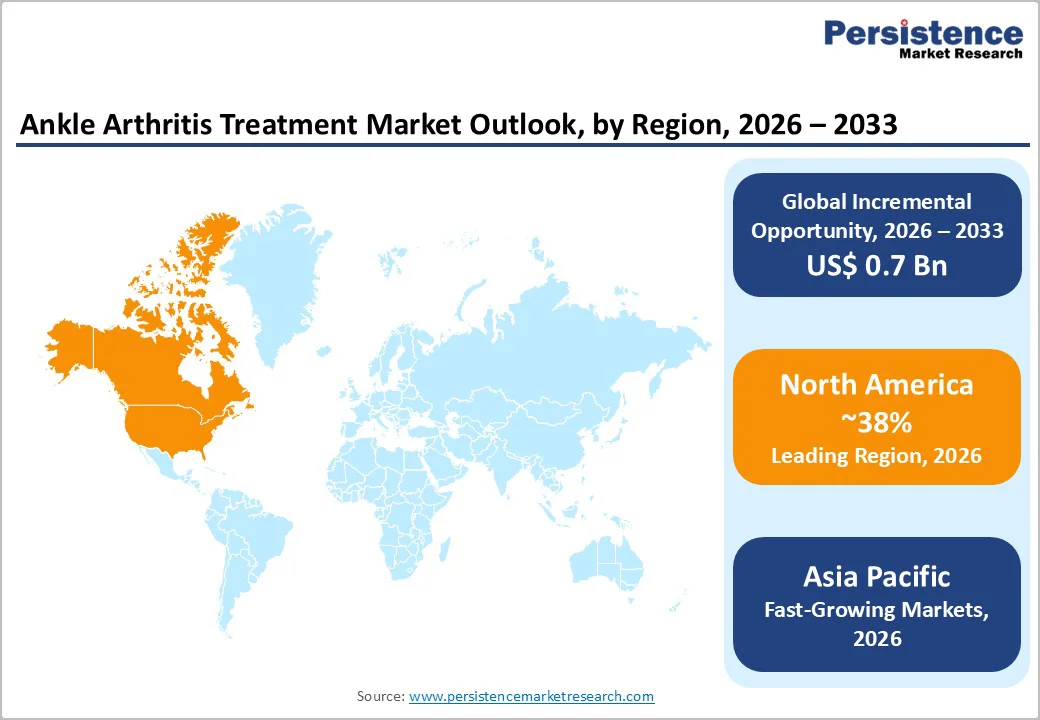

- Leading Region: North America leads the global ankle arthritis treatment market, driven by advanced healthcare infrastructure, a high geriatric population, and strong clinical adoption of corticosteroids and NSAIDs.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by aging populations in China and India, rising prevalence of arthritis, expanding healthcare facilities, and increasing awareness of ankle joint care.

- Dominant Segment: Corticosteroids remain the dominant drug class, supported by high efficacy in reducing inflammation and pain in patients with ankle arthritis, particularly in clinical settings.

- Fastest-Growing Segment: Non-steroidal anti-inflammatory drugs (NSAIDs) represent the fastest-growing segment due to widespread use, favorable safety profile, availability in oral and topical forms, and increasing patient preference for non-invasive treatments.

| Global Market Attributes | Key Insights |

|---|---|

| Ankle Arthritis Treatment Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 5.4% |

Market Dynamics

Driver – Rising prevalence of ankle osteoarthritis and post-traumatic injuries

The foremost growth driver is the escalating clinical burden of ankle osteoarthritis linked to sports, occupational, and accidental injuries. Epidemiological studies estimate the prevalence of symptomatic radiographic ankle osteoarthritis at around 3.4% in the general population, with some cohorts of adults over 50 years reporting radiographic ankle osteoarthritis rates as high as 13.9%. Research also indicates that approximately 70–80% of ankle osteoarthritis cases are post-traumatic, often following recurrent sprains, fractures, or ligament injuries; among retired professional football players, up to 94% of individuals with ankle osteoarthritis report at least one prior ankle injury and over 60% have undergone ankle surgery. This strong causal relationship between injuries and later arthritis translates into sustained demand for pharmacologic therapies to manage chronic pain, inflammation, and stiffness in younger, active patients seeking to maintain mobility and postpone joint fusion or replacement.

Restraints – Safety concerns and adverse effects of long-term pharmacotherapy

Despite their pivotal therapeutic role, long-term use of systemic NSAIDs, corticosteroids, and certain analgesics is constrained by safety concerns that limit dosing and duration. Clinical references caution that chronic oral NSAID exposure increases risks of gastrointestinal bleeding, cardiovascular events, and renal impairment, especially in older adults and those with comorbidities. Use of systemic corticosteroids is typically reserved for short courses or inflammatory arthritides because of associations with osteoporosis, infection, and adrenal suppression; ankle arthritis texts specifically advise against prolonged systemic steroid therapy for purely degenerative disease. Opioid based pain relievers, though less commonly used for ankle arthritis, are tightly regulated due to dependence and overdose risks, further restricting their role. These safety and regulatory barriers often prompt clinicians to undertreat chronic ankle pain or rapidly transition patients to surgical options, tempering potential growth in pharmacologic revenue.

Opportunity – Emergence of biologics and regenerative therapies targeting ankle joints

Growing experience with biologic and orthobiologic approaches in neighboring markets, such as the foot and ankle orthobiologics market, is creating new opportunities to expand ankle arthritis treatment beyond traditional pharmaceuticals. Orthobiologic products, including platelet-rich plasma, bone marrow aspirate concentrates, and synthetic bone substitutes, are increasingly used to enhance joint preservation and delay fusion procedures, supported by evidence that osteoarthritis affects roughly 24% of U.S. adults and is driving the adoption of regenerative solutions in high-value joints. Early-stage research into stem cell-based cartilage repair, growth factor–rich injectables, and targeted biologics for inflammatory ankle arthritis could translate into novel indications and premium-priced therapies over the forecast period. As payers seek to reduce long-term disability costs and hospitalizations, pharmacologic and injectable regenerative therapies that delay or obviate surgery may obtain favorable coverage, creating a high-growth niche within the wider ankle arthritis treatment landscape.

Category-wise Analysis

Drug Analysis

Within the drug category, corticosteroids are expected to remain the leading segment, accounting for approximately 28% of the ankle arthritis treatment market share in 2025. Their dominance stems from the strong clinical role of intra-articular corticosteroid injections in providing rapid, short-term relief of pain and swelling in osteoarthritis and inflammatory ankle arthritis. Clinical literature describes corticosteroid injections as standard options when first-line NSAIDs and simple analgesics fail, with evidence in larger joints showing meaningful pain reduction at one to three months following treatment. Ankle arthritis management resources also note that short courses of oral corticosteroids may be appropriate in cases with prominent inflammatory signs, particularly in rheumatoid or reactive arthritis affecting the ankle. Because corticosteroids can be delivered via multiple routes, oral, intra-articular, and occasionally intravenous, their flexibility across acute flares, chronic pain, and peri-operative settings reinforces their shared leadership over other drug classes such as analgesics and disease-modifying agents.

Distribution Channel Analysis

Hospital pharmacies are expected to constitute the leading distribution channel for ankle arthritis treatments. Hospitals and affiliated orthopedic centers typically manage moderate to severe ankle arthritis, including cases requiring image-guided injections, complex pharmacologic regimens, and perioperative medications. Inpatient and day care settings are where intra-articular corticosteroid injections and intravenous therapies are most administered, and hospital pharmacies control procurement of these sterile injectables, along with associated analgesics and supportive drugs. Additionally, high-volume orthopedic departments in hospitals often serve as referral centers for sports injuries and post-traumatic ankle arthritis, driving intensive use of both systemic and local pharmacologic treatments as part of multidisciplinary care pathways. Although retail and online pharmacies are capturing growing demand for chronic oral NSAIDs and topical formulations, the complexity of advanced treatment regimens helps hospital pharmacies maintain leadership.

Region-wise Insights

North America Ankle Arthritis Treatment Market Trends

North America holds the leading regional position, accounting for an 38% share of the ankle arthritis treatment market in 2025, underpinned by high osteoarthritis prevalence, advanced orthopedic infrastructure, and strong payer coverage for pharmacologic and minimally invasive therapies. In the U.S. alone, about 54.4 million adults have physician-diagnosed arthritis, and osteoarthritis affects roughly 24% of adults, placing significant pressure on health systems to deliver effective pain management and joint preservation strategies across joints, including the ankle. High sports participation and occupational injury rates add to the burden of post-traumatic ankle arthritis, driving frequent use of oral NSAIDs, intra-articular corticosteroids, and adjunctive analgesics in primary care, sports medicine, and orthopedic practices.

Regulatory frameworks such as FDA guidance for injectable corticosteroids and NSAIDs, coupled with robust surveillance of drug safety, support a well-defined therapeutic environment that encourages innovation while protecting patients. North American providers are early adopters of advanced orthobiologic and regenerative approaches for foot and ankle conditions, reflected in the region’s nearly 49% share of the broader foot and ankle orthobiologics market. Integration of telemedicine, remote monitoring apps, and electronic prescribing enables tighter control of chronic ankle pain regimens, while structured physical therapy and injury prevention programs aim to reduce progression to severe arthritis. Together, these factors underpin high pharmaceutical utilization and support the region’s continuing leadership in the ankle arthritis treatment market.

Asia and Pacific Ankle Arthritis Treatment Market Trends

Asia Pacific is poised to be the fastest-growing regional market over 2025–2032, propelled by demographic expansion, rapid urbanization, and rising healthcare investment. Large populations in China, Japan, India, and ASEAN countries are aging, with escalating prevalence of osteoarthritis and lifestyle-related joint injuries that increase demand for ankle arthritis pharmacotherapy. Japan’s high proportion of adults over 65 years, coupled with studies documenting radiographic ankle osteoarthritis prevalence of about 13.9% in older community populations, underscores the region’s substantial burden. In parallel, expanding middle-class participation in sports and physical recreation in China and India is contributing to more ankle sprains and fractures, which are key risk factors for post-traumatic ankle arthritis.

Healthcare infrastructure upgrades and broader insurance coverage in markets such as China’s urban centers, India’s government-sponsored schemes, and ASEAN’s social health insurance systems are improving access to NSAIDs, corticosteroids, and injectable therapies. Asia Pacific also offers significant manufacturing cost advantages, with many multinational and regional pharmaceutical firms operating local plants that produce oral and topical NSAIDs, generic corticosteroids, and pain relievers at competitive prices for domestic and export markets. As awareness of ankle arthritis and musculoskeletal health improves through public health campaigns and digital health platforms, the region is expected to outpace global average growth, particularly in urban hospitals and retail pharmacies catering to active, aging populations.

Market Competitive Landscape

The ankle arthritis treatment market is moderately fragmented, with a mix of global pharmaceutical giants, specialty musculoskeletal companies, and regional generic manufacturers competing across oral, topical, and injectable therapies. Multinational firms such as Pfizer Inc., GlaxoSmithKline Plc., Novartis AG, Johnson & Johnson, Bayer AG, Abbott Laboratories, Sanofi S.A., Eli Lilly, and Horizon Therapeutics Plc. Leverage broad pain and inflammation management portfolios, strong brand recognition in NSAIDs and corticosteroids, and extensive distribution networks spanning hospital and retail pharmacies. Niche players, including Anika Therapeutics Inc., Pharmed Limited, and Almatica Pharma LLC, differentiate through targeted intra-articular products, hyaluronic acid injectables, or combination therapies that address joint pain and function. Competitive strategies center on lifecycle management of established molecules, development of extended release and topical formulations, geographic expansion into high-growth Asia Pacific and Latin American markets, and partnerships with orthopedic specialists to integrate pharmacologic products into comprehensive ankle arthritis care pathways.

Key Industry Developments:

- In July 2025, researchers at Northwest University, China, developed an innovative nano-composite hydrogel system aimed at simultaneously treating inflammation and cartilage damage in osteoarthritis, a major cause of joint disability globally.

Companies Covered in Global Ankle Arthritis Treatment Market

- Pfizer Inc.

- GlaxoSmithKline Plc.

- Novartis Ag

- Johnson & Johnson

- Bayer AG

- Abbott Laboratories

- Sanofi S.A.

- Eli Lilly

- Horizon Therapeutics Plc.

- Anika Therapeutics Inc.

- Pharmed Limited

- Almatica Pharma LLC

Frequently Asked Questions

The global market is projected to be valued at US$ 1.4 Bn in 2026.

Rising prevalence of ankle arthritis, aging population, obesity, sports injuries, increasing awareness, and demand for effective pain and inflammation management.

The global market is expected to witness a CAGR of 6.3% between 2026 and 2033.

Development of targeted biologics, minimally invasive therapies, combination drug formulations, growing geriatric population, and expansion in emerging healthcare markets.

Pfizer Inc., GlaxoSmithKline Plc., Novartis Ag, Johnson & Johnson, and Bayer AG.