- Transportation & Logistics

- Air Freight Forwarding Market

Air Freight Forwarding Market Size, Share, and Growth Forecast, 2026 - 2033

Air Freight Forwarding Market by Cargo Type (General Cargo, Special Cargo), Service Type (Freight, Express, Mail, Other Services), Destination (Domestic, International), Industry (E-commerce & Retail, Automotive, Healthcare & Pharmaceuticals, Manufacturing, Perishable Goods, High-Tech & Electronics, Others) and Regional Analysis for 2026 - 2033

Air Freight Forwarding Market Size and Trends Analysis

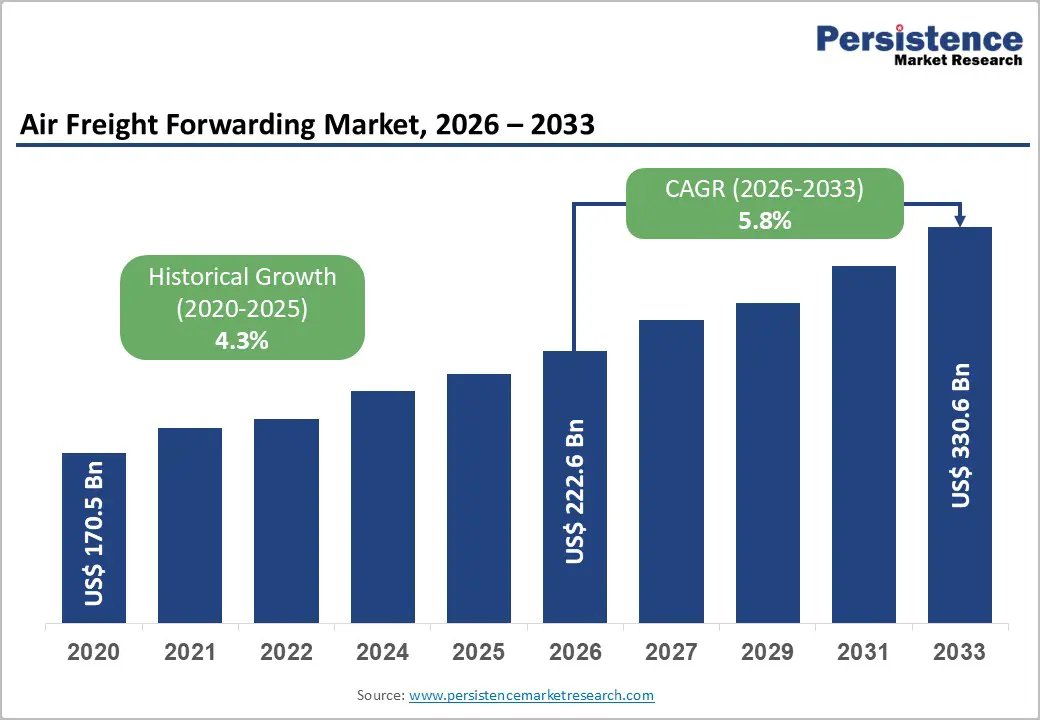

The global air freight forwarding market size was valued at US$ 222.6 billion in 2026 and is projected to reach US$ 330.3 billion by 2033, growing at a CAGR of 5.8 percent between 2026 and 2033. This robust growth trajectory is driven by e-commerce penetration, which requires expedited cross-border logistics solutions; pharmaceutical cold-chain requirements, which demand temperature-controlled air transport; and global manufacturing networks, which necessitate time-sensitive component delivery.

Key Industry Highlights:

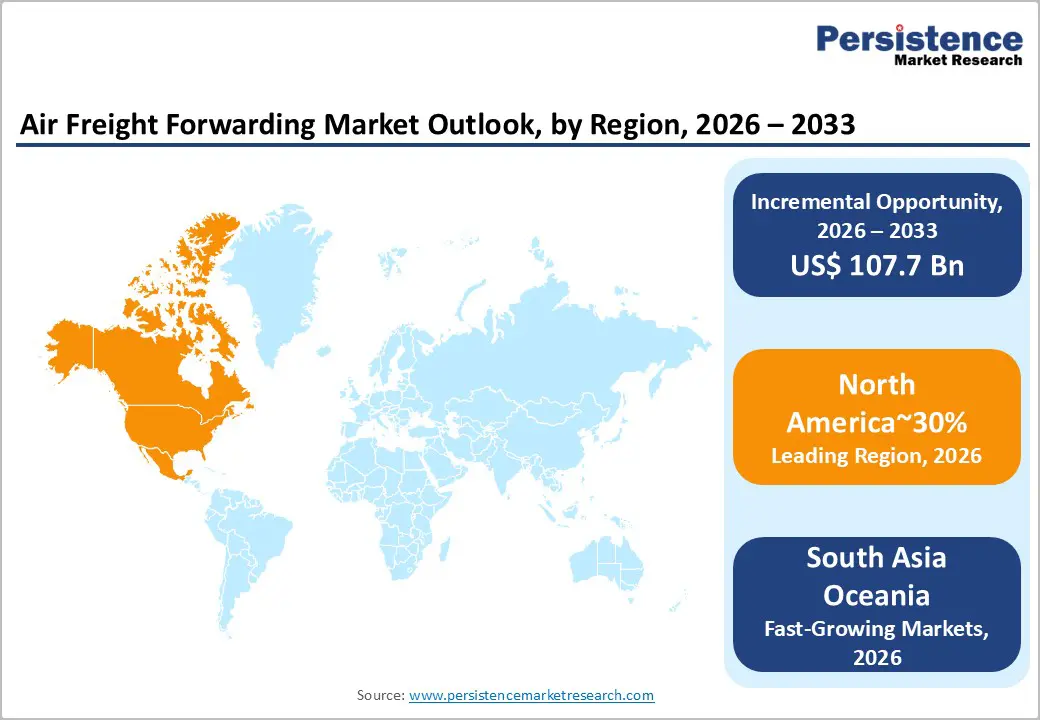

- Regional Leadership: North America leads the Global Air Freight Forwarding Market with a 30% share, driven by robust e-commerce penetration, advanced pharmaceutical manufacturing clusters, and a diversified industrial base that supports high-value air cargo flows.

- Emerging Asia-Pacific Hub: East Asia accounts for 22% of the market, led by China’s dominant manufacturing export base, intra-regional trade, and growing air cargo volumes to North America and Europe, positioning the region as a central hub for manufacturing and distribution.

- European Market Scenario: Europe accounts for 25% share, fueled by automotive supply chain integration, advanced pharmaceutical clusters, and sophisticated e-commerce logistics infrastructure supporting intra- and extra-EU trade.

- Leading Cargo Segment: General Cargo dominates with 65% share, encompassing manufactured goods, industrial components, consumer merchandise, and standard shipments moving through global supply chains under ambient conditions.

- Fastest-Growing Cargo Segment: Special Cargo is the fastest-growing, driven by pharmaceuticals, perishables, lithium batteries, aerospace components, and high-value shipments requiring cold chain, hazmat, and specialised handling.

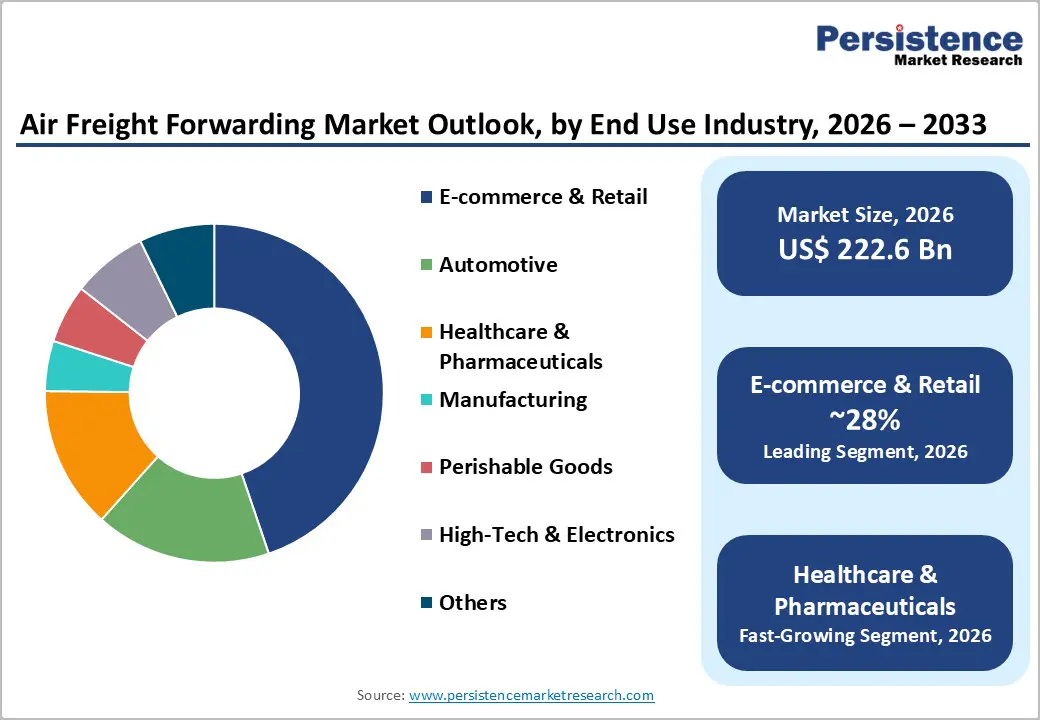

- Leading Industry: E-commerce & Retail holds 28% share, propelled by cross-border online shopping, marketplace fulfillment, omnichannel inventory distribution, and demand for expedited international delivery.

| Key Insights | Details |

|---|---|

|

Air Freight Forwarding Market Size (2026E) |

US$ 109.7 Bn |

|

Market Value Forecast (2033F) |

US$ 245.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.4% |

Market Dynamics

Drivers - E-commerce Trade Expansion and Cross-Border Logistics Requirements

Global e-commerce penetration and cross-border online retail growth constitute primary demand drivers for the Air Freight Forwarding Market, as digital commerce platforms require expedited international delivery capabilities. According to the International Air Transport Association, global air cargo volumes are expected to reach approximately 71.6 million tonnes in 2026, reflecting sustained demand for time-sensitive goods and industrial exports across international trade corridors.

The global air cargo market experienced steady tonnage growth of 4 percent year over year through November 2025, with strong demand particularly evident on routes such as Asia Pacific to Europe and the Americas, intra-Asia Pacific, and Europe-Asia, driven by ongoing requirements for time-sensitive goods and industrial exports. The European Union introduced a flat customs duty of EUR 3 on low-value consignments from 2026, potentially impacting e-commerce flows and affecting capacity allocation across air freight lanes.

In July 2025, global air cargo demand measured in Cargo Tonne Kilometres increased by 5.5 percent year over year, marking a clear recovery from June's 0.6 percent growth rate, with the international air cargo segment seeing a 6.0 percent increase and Asia Pacific leading with 11.0 percent growth. The rise in e-commerce shipments, especially during peak shopping seasons, has prompted airports and logistics operators to invest in specialised infrastructure and services, with e-commerce and perishables becoming critical drivers influencing air freight demand in the EU in 2024. For the Air Freight Forwarding Market, e-commerce expansion creates systematic demand for integrated forwarding services encompassing customs clearance, last-mile coordination, real-time shipment visibility, and returns management capabilities, positioning air freight forwarders as strategic enablers of global digital commerce infrastructure rather than transactional capacity brokers.

Pharmaceutical and Healthcare Supply Chain Specialization

The pharmaceutical industry's stringent cold chain requirements and regulatory compliance mandates create substantial demand for specialised air freight forwarding services, ensuring product integrity throughout international transportation. The Middle East and Africa are positioned as key drivers of global air cargo growth, largely due to their strategic positioning as transhipment hubs for e-commerce, perishables, pharmaceuticals, and electronics.

In Africa, demand for air cargo is driven by the need to transport perishables and pharmaceuticals quickly and efficiently across the continent and beyond, reflecting the critical role of air transport in healthcare logistics. The Comprehensive Economic Partnership Agreement between India and Oman is expected to enhance bilateral trade and air cargo flows between the two regions, with pharmaceuticals representing a key commodity category. In 2023, the air cargo industry carried 57.4 million tonnes of freight, marking a 4.0 percent increase from the previous year, with international freight growing 4.3 percent compared to 2022, surpassing pre-pandemic levels of 2019 by 0.1 percent, highlighting the sector's ability to maintain global trade, especially in sectors reliant on time-sensitive and high-value shipments, including pharmaceuticals.

Non-scheduled freight services accounted for 20 percent of total freight operations in 2023, up from 15 percent in 2019, becoming indispensable, especially during disruptions in global supply chains when scheduled services face capacity constraints, offering flexibility by providing dedicated capacity, particularly valuable for pharmaceutical shipments requiring guaranteed temperature control and departure certainty. The air freight forwarding market benefits from pharmaceutical industry growth through premium pricing for validated cold chain services, long-term contract relationships with pharmaceutical manufacturers and distributors, and differentiated technical capabilities, including GDP-compliant handling, temperature monitoring, and regulatory documentation expertise that create barriers to entry and support margin preservation despite competitive market dynamics.

Manufacturing Supply Chain Resilience and Just-in-Time Inventory Models

Global manufacturing networks' adoption of just-in-time inventory strategies and supply chain resilience initiatives drives systematic air freight forwarding demand for expedited component delivery and production continuity assurance. In the Americas, US exports, particularly from the industrial and aerospace sectors, remain strong, supporting sustained air freight volumes despite softening import demand following peak seasonal periods. Asia Pacific's air cargo sector continues to outperform, with demand in the region growing 8 percent year over year in the last two weeks of November 2025, driven by the steady expansion of Asia's manufacturing base and increasing exports, particularly to the US and Europe.

In 2023, the Asia Pacific led air freight growth with a remarkable 13.7 percent increase in scheduled Freight Tonne Kilometres, driven by carriers like Cathay Pacific, China Southern Airlines, and Air China, reflecting the region's dominance in global manufacturing and distribution. Intra-Asia Pacific trade accounted for 17 percent of global market share in 2023, with the Asia Pacific to North America route contributing 15 percent and the Asia Pacific to Europe route representing 13 percent of total international air freight, underscoring Asia's role as a central hub for manufacturing and distribution.

In December 2025, global air cargo capacity grew by 2 percent year over year, marking a reversal from declining trends seen in earlier months, though overall capacity increase was not sufficient to completely offset the decline in freighter availability, creating challenges for air cargo providers to meet surging demand, especially on high-volume trade routes. For the Air Freight Forwarding Market, manufacturing sector requirements create opportunities for value-added services, including vendor consolidation, kitting and assembly, emergency shipment coordination, and integrated logistics solutions that extend beyond traditional freight booking into comprehensive supply chain orchestration, enabling forwarders to capture a larger share of customer logistics budgets and establish strategic partnership relationships rather than transactional service provision.

Restraints - Fuel Cost Volatility and Operating Expense Pressures

Air freight forwarding profitability faces persistent pressure from jet fuel price volatility and operating cost escalation, with carriers passing through fuel surcharges, creating pricing unpredictability for shippers and margin compression for forwarders. In July 2025, jet fuel prices fell 9.1 percent year over year, marking the fifth consecutive annual decline, though prices increased 4.3 percent month over month, demonstrating continued volatility despite the overall downward trend.

As a result of fuel dynamics, cargo yields or freight rates softened by 2.0 percent year over year in July 2025, although they showed a minor increase of 0.8 percent month over month, indicating pricing pressure on forwarders caught between customer rate commitments and carrier cost structures. Cargo Load Factor decreased by 0.7 percentage points compared to June 2024, indicating a slight softening in capacity utilisation despite increased demand, suggesting market conditions where excess capacity prevents rate recovery. These fuel cost fluctuations and yield pressures compound in competitive market environments where forwarders lack pricing power with large volume customers, forcing absorption of carrier rate increases while maintaining competitive customer pricing, thereby compressing margins and limiting profitability, particularly for small and mid-sized forwarders without diversified service portfolios or high-margin specialised offerings.

Opportunity - Digital Platform Integration and End-to-End Visibility Solutions

The convergence of air freight forwarding with digital logistics platforms, real-time tracking technologies, and predictive analytics creates differentiated service offerings addressing customer demands for shipment visibility, proactive exception management, and data-driven decision support. Digital technologies, including IoT sensors for real-time location and condition monitoring, blockchain-based documentation management ensuring tamper-proof chain of custody records, and artificial intelligence-powered route optimization algorithms enable forwarders to deliver outcome-based service level agreements guaranteeing delivery windows and product integrity rather than traditional best-effort transportation arrangements.

E-commerce shipments have become a driving force in the air cargo sector, leading to increased demand for flexible, non-scheduled services capable of meeting fast-paced, on-demand logistics needs of global retailers, with this shift highlighting changing landscape where speed and flexibility are becoming more critical than ever in catering to evolving consumer demands. For the Air Freight Forwarding Market, digital platform integration creates opportunities for recurring revenue streams through technology subscription fees, premium pricing for enhanced visibility and analytics services, and strategic differentiation enabling customer retention in competitive environments where traditional freight brokerage functions face commoditization pressure, particularly valuable for e-commerce customers requiring integration with order management systems and automated customs clearance workflows.

Category-wise Analysis

Cargo Type Insights

General cargo dominates likely to account for a 65% market share in 2026. This segment includes high-tech electronics, automotive parts, industrial machinery components, consumer goods, textiles, and general commercial products moving through global supply chains under ambient temperature conditions using standard air freight packaging and handling protocols.

Special cargo represents the fastest-growing cargo type segment, encompassing temperature-controlled pharmaceuticals, dangerous goods requiring hazmat certification, oversized and heavy machinery, live animals, and high-value shipments demanding enhanced security protocols. This segment benefits from increasing pharmaceutical trade requiring validated cold chain logistics, fresh produce exports from emerging agricultural economies, lithium battery shipments supporting electronics manufacturing, and aerospace component movements demanding specialised packaging and handling expertise.

Industry Insights

E-commerce and retail hold approximately 28.0% market share in 2026, establishing its position as the dominant Industry for air freight forwarding driven by cross-border online shopping, marketplace seller fulfillment, and omnichannel retail inventory distribution requiring expedited international delivery. This sector demands comprehensive forwarding solutions encompassing last-mile coordination, customs brokerage for low-value consignments, returns logistics management, and peak season capacity guarantees supporting promotional events and shopping holidays.

The rise in e-commerce shipments, especially during peak shopping seasons, has prompted airports and logistics operators to invest in specialized infrastructure and services, with e-commerce becoming a critical driver influencing air freight demand. E-commerce shipments have become a driving force in the air cargo sector, leading to increased demand for flexible, non-scheduled services capable of meeting fast-paced, on-demand logistics needs of global retailers.

Regional Insights and Trends

East Asia Air Freight Forwarding Market Trend

East Asia commands approximately 22% of the Global Air Freight Forwarding Market, with China serving as the dominant manufacturing export hub, driving outbound air freight volumes to North America and Europe, while intra-regional trade supports consistent forwarding activity across Southeast Asia, Japan, and South Korea. Asia Pacific led air freight growth in 2023 with a remarkable 13.7 percent increase in scheduled Freight Tonne Kilometres, driven by carriers like Cathay Pacific, China Southern Airlines, and Air China, reflecting the region's dominance in global manufacturing and distribution. Asia Pacific's air cargo sector continues to outperform, with demand in the region growing 8 percent year over year in the last two weeks of November 2025, driven by the steady expansion of Asia's manufacturing base and increasing exports, particularly to the US and Europe.

In July 2025, the international air cargo segment witnessed a 6% rise in the cargo tonne kilometres in the Asia Pacific region, leading with 11.0 percent growth, demonstrating the region's sustained momentum. Intra-Asia Pacific trade accounted for 17 percent of global market share in 2023, representing the largest single trade corridor, while Asia Pacific to North America contributed 15 percent and Asia Pacific to Europe represented 13 percent, highlighting Asia's role as a central hub for manufacturing and distribution.

North America Air Freight Forwarding Market Trends

North America accounts for approximately 30% of the global market, representing the largest market driven by robust e-commerce penetration, advanced pharmaceutical manufacturing clusters, and a diversified industrial base generating consistent air freight demand across multiple end-use industries. The region benefits from established logistics infrastructure, including major cargo gateways, sophisticated customs clearance processes, and a mature forwarding industry with comprehensive service capabilities. US exports, particularly from the industrial and aerospace sectors, remain strong, supporting sustained air freight volumes despite softening import demand following peak seasonal periods.

Air cargo imports to the US from Asia have softened as the peak seasonal demand period passed, though industrial and aerospace export strength maintains balanced trade lane utilisation. In Canada, despite earlier export-driven GDP growth, the air cargo market faces a slowdown in export activity due to cautious inventory purchasing and subdued industrial demand, with weakening new export activity contributing to lower-than-expected tonnage, pointing to challenges that may persist into early 2026.

Europe Air Freight Forwarding Market Trends

Europe accounts for approximately 25% of the global market, driven by advanced pharmaceutical manufacturing clusters, automotive supply chain integration, and sophisticated e-commerce logistics infrastructure serving both intra-European and intercontinental trade. In 2024, the European Union witnessed 8.7% increase in air freight and mail transport compared to 2023, with a total of 14.3 million tonnes carried, primarily driven by intra-EU transport growing 9.1 percent while extra-EU transport remained stable with only 0.1 percent increase. Among EU countries, Hungary, Czechia, Greece, and Cyprus led growth with Hungary experiencing a remarkable 65.9% increase, while Germany, Belgium, Spain, France, Italy, the Netherlands, and Turkey each handled over 1 million tonnes of freight and mail. Frankfurt Main emerged as the busiest EU airport for air freight handling 2.0 million tonnes, followed closely by Paris Charles de Gaulle at 1.9 million tonnes, with notable growth at Budapest Liszt Ferenc seeing 65.7% increase and Zaragoza growing 39.6%. Extra-EU transport dominated long-distance freight over 2,000 km, with 99% total transport in this category in both 2023 and 2024, reflecting the importance of international trade for time-sensitive and high-value goods. Extra-EU air freight transport accounted for 83.3 percent of total freight and mail in 2024, with Eastern Asia seeing a 12.8 percent increase in transport volumes compared to 2023, making it the largest market for EU export and import traffic, while North America and Central America saw decreases.

Competitive Landscape

The global air freight forwarding market is predominantly consolidated, with a few dominant players, including DHL Global Forwarding, Kuehne + Nagel, DB Schenker, C.H. Robinson, and XPO Logistics, holding significant market shares. These companies leverage their vast global networks, extensive fleets, and integrated service offerings to maintain leadership. There is room for smaller players, like Expeditors International and DSV Panalpina, who focus on regional markets and niche services. Despite the rise of tech-driven companies offering advanced digital freight solutions, the market remains largely oligopolistic, with the larger players maintaining control through scale, infrastructure, and innovation in areas like sustainability and green logistics.

Key Industry Developments

- In Dec 2025, DHL Global Forwarding has expanded its partnership with Air France KLM Martinair Cargo (AFKLMP), signing a new framework agreement focused on emission reduction rights. This agreement is built on their 2022 partnership, emphasising the development of market-ready book-and-claim models for sustainable air freight solutions. As part of the deal, DHL has signed a work order for 35,000 metric tons of CO2e WTW (Well-to-Wheel) emission reduction rights. This collaboration aims to accelerate the adoption of sustainable aviation fuels (SAF) and digital verification processes, positioning DHL as a leader in emission-reduced air freight. The partnership aligns with DHL's GoGreen program and its goal to increase the use of SAF to 30% by 2030. The agreement strengthens the long-term commitment to decarbonising the air freight sector and is seen as a model for the industry.

- In Jan 2026: DHL Global Forwarding launched an innovative multi-modal logistics service combining truck and air transport to move goods from China to Europe. This hybrid service picks up goods from Chinese manufacturers, transports them by truck to Tashkent, Uzbekistan, and then transfers them to DHL freighter aircraft for onward delivery to Istanbul, Turkey. The service is designed for large-volume, bulky shipments with a transit time of 9 to 11 days, offering cost savings compared to traditional air freight. Customers have reported six-digit savings while maintaining reliable lead times. This new service offers an alternative to traditional ocean-air or rail-truck integrations, providing agility and cost efficiency amidst rising demand for China-Europe trade.

Companies Covered in Air Freight Forwarding Market

- Air France-KLM S.A.

- AirFreight.com

- C.H. Robinson Worldwide, Inc.

- CEVA Logistics

- DB Schenker

- DHL International GmbH

- DIMOTRANS Group

- DSV

- FedEx

- GEODIS

- Kuehne+Nagel

- Nippon Express Co., Ltd.

- Rhenus Group

- United Parcel Service, Inc.

Frequently Asked Questions

The global air freight forwarding market is projected to be valued at US$ 222.6 Bn in 2026.

The General Cargo segment is expected to account for approximately 65% of the Global Air Freight Forwarding Market by Cargo type in 2026.

The market is expected to witness a CAGR of 5.8% from 2026 to 2033.

E-commerce expansion, cross-border trade growth, pharmaceutical cold chain needs, and just-in-time manufacturing supply chains are the primary drivers of the Air Freight Forwarding Market, fueling demand for expedited, reliable, and value-added international logistics services.

Integration of digital logistics platforms for real-time visibility and analytics, coupled with expanding trade opportunities in emerging markets such as Africa, Southeast Asia, and the Middle East, represents the key market opportunities in the Air Freight Forwarding Market.

Key players in the Air Freight Forwarding Market include DHL Global Forwarding, Kuehne + Nagel, DB Schenker, C.H. Robinson, and XPO Logistics.