- HVAC

- Air Curtains Market

Air Curtains Market Size, Share, and Growth Forecast, 2026 – 2033

Air Curtains Market by Product Type (Non‑Recirculating, Recirculating, Heated, Others), Airflow Capacity (Up to 500 m³/h, 500–1000 m³/h, 1000–1500 m³/h, Above 1500 m³/h), Application (Commercial, Industrial, Residential, Others), and Regional Analysis for 2026–2033

Air Curtains Market Share and Trends Analysis

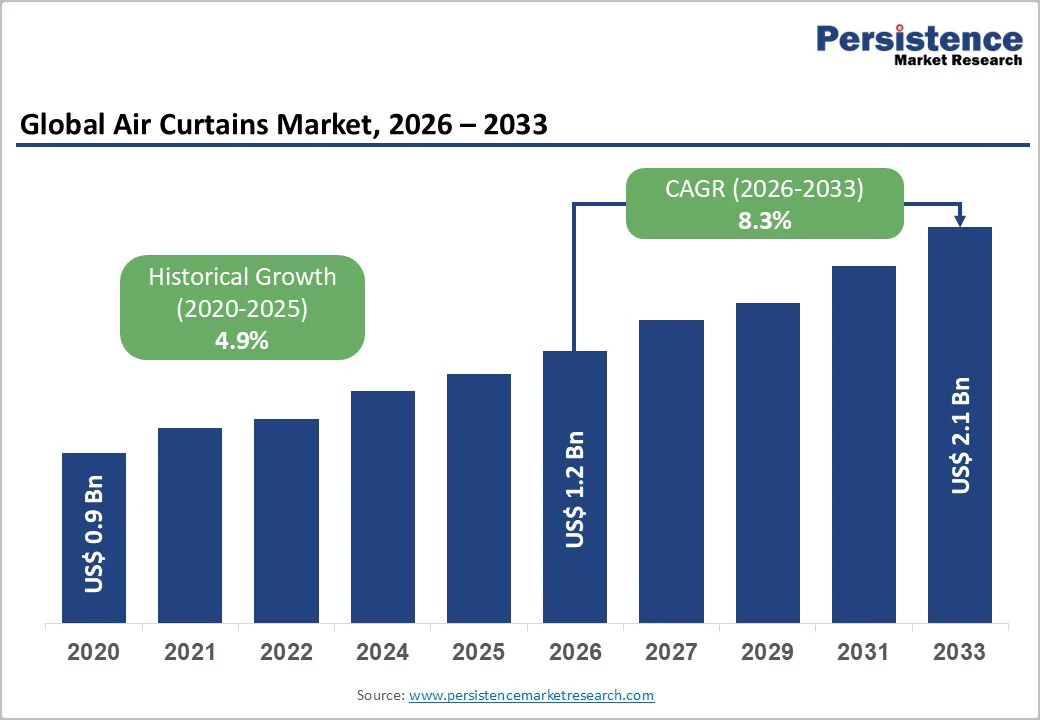

The global air curtains market size is likely to be valued at US$ 1.2 billion in 2026, and is projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 8.3% during the forecast period 2026-2033. The market is expanding due to intensifying energy-efficiency mandates, increased adoption of commercial air curtains in retail and hospitality, and strong infrastructure development in emerging economies. Regulatory pressure to reduce heating, ventilation & air conditioning (HVAC) energy losses and maintain indoor air quality further reinforces market adoption. Organizations across commercial, industrial, and residential sectors increasingly deploy air curtain system solutions to reduce operational costs and limit air infiltration.

Key Industry Highlights

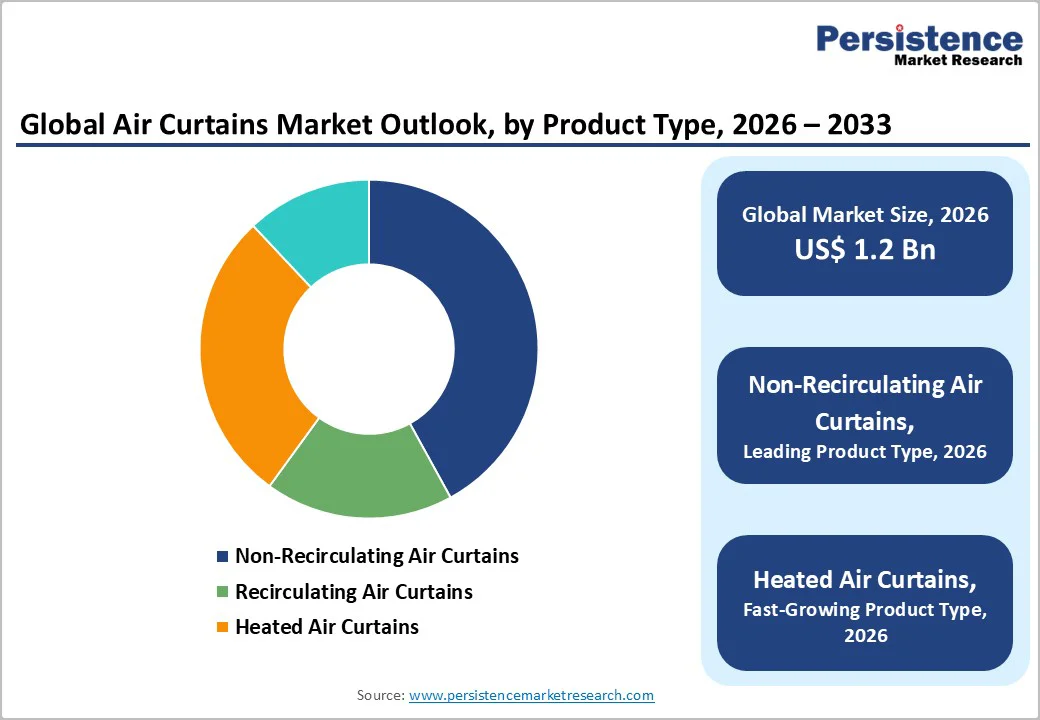

- Leading & Fastest-growing Products: Non-recirculating air curtains are expected to dominate with around 42% market revenue share in 2026, while heated air curtains are projected to grow the fastest with an estimated 12% CAGR through 2033.

- Dominant Airflow Capacity: The 500–1000 m³/h segment is anticipated to hold the largest share at about 42% in 2026, as they efficiently manage moderate door heights while maintaining indoor temperature stability.

- Leading Application: Commercial applications are likely to dominate with an estimated 48% market revenue share in 2026, owing to high foot traffic and stringent indoor air quality requirements in commercial spaces.

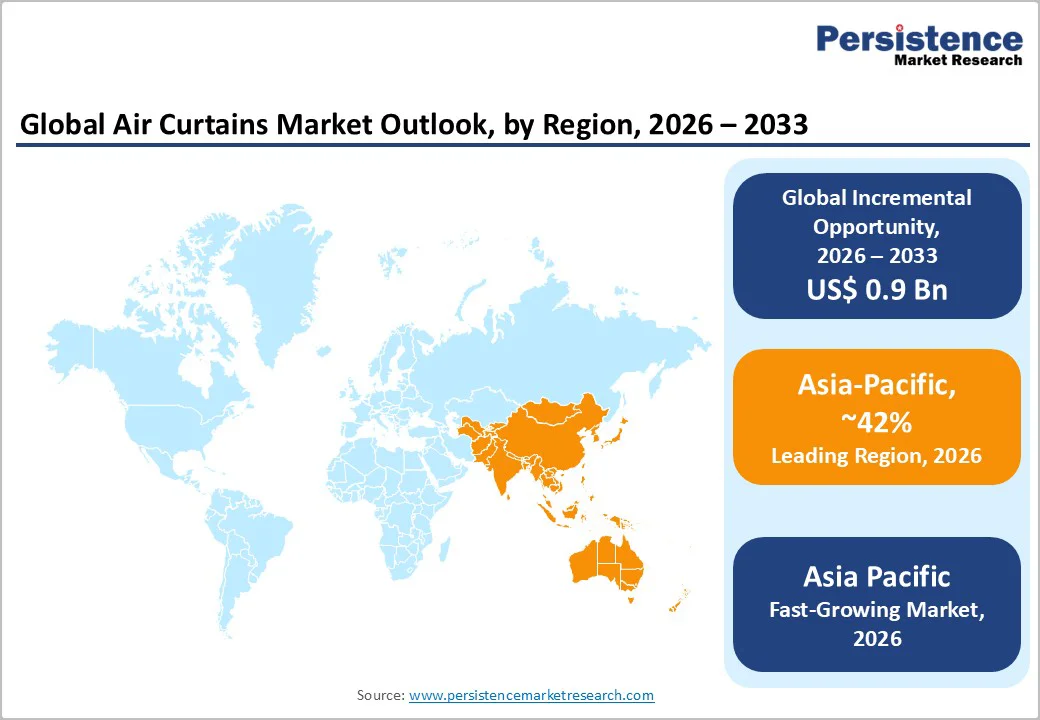

- Regional Leadership: Asia Pacific is anticipated to lead the market with approximately 42% share in 2026, underpinned by rapid infrastructure expansion and industrial growth.

- Key Opportunity: Investment in high-capacity air curtains used in cold-chain and logistics infrastructure can deliver promising returns, owing to the global expansion of temperature-controlled supply chains.

| Key Insights | Details |

|---|---|

| Air Curtains Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3 % |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9 % |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory and Operational Priorities Accelerating Air Curtain Adoption

Growing regulatory emphasis on energy efficiency and indoor climate control is a primary driver for air curtain system adoption in commercial and industrial facilities. Stricter HVAC performance benchmarks encourage building owners to install solutions that minimize conditioned-air loss and improve thermal separation. High-traffic areas in retail, logistics, and industrial spaces experience significant energy escape through door openings, making door air barriers and high-airflow air curtains practical for reducing HVAC load while maintaining stable indoor temperatures. Recent technological advancements, such as the Airtècnics Clever PRO controller, demonstrate how IoT-enabled automation optimizes airflow, enhances energy efficiency, and supports compliance with evolving operational standards.

Increasing attention to indoor air quality and hygiene can also stoke the demand for air curtain systems in healthcare, food processing, and pharmaceutical facilities. Units with higher jet velocity and optimized airflow capacity help limit airborne particles, insects, and contaminants, ensuring safe and comfortable environments. Large industrial and commercial spaces benefit from temperature uniformity that protects workers and equipment, while regulatory and operational priorities collectively accelerate adoption and position air curtains as integral to modern building management strategies.

High Initial Investment and Limited Awareness Hindering Wider Adoption

The air curtains market growth is challenged by the high upfront expenditure required for installation, retrofitting, and integration with existing HVAC systems. Larger commercial and industrial units often demand structural adjustments and specialized electrical work, increasing the overall capital cost. Maintenance requirements to retain optimal airflow and motor efficiency add to operational spending, creating barriers for small enterprises. Although long-term energy savings exist, the initial financial burden remains a significant deterrent. This cost sensitivity slows uptake in sectors with tight budgets or low modernization incentives.

Awareness gaps in developing economies have further restricted the market’s growth potential, particularly where decision-makers lack clarity on the measurable benefits of airflow-based climate separation technologies. Traditional physical barriers continue to dominate due to limited technical exposure and insufficient industry education. The absence of clearly defined building guidelines and a shortage of skilled technicians also limits deployment, especially for advanced or high-capacity systems. As a result, the combination of economic constraints and knowledge limitations continues to narrow the adoption window across emerging commercial and industrial environments.

Expanding Scope for Cost-Efficient, Awareness-Driven Market Penetration

Growing interest in energy-saving technologies presents a strong opportunity for air curtain manufacturers to reposition their solutions as long-term, cost-efficient investments. With businesses increasingly focused on reducing HVAC load and improving climate control, streamlined installation packages and modular system designs can help lower initial costs and attract price-sensitive buyers. Enhanced product efficiency, simplified retrofitting options, and bundled service plans further strengthen the value proposition for commercial and industrial facilities. As companies seek practical ways to optimize indoor environments, well-priced and performance-driven systems can unlock new adoption segments.

Rising emphasis on hygiene, comfort, and operational efficiency across retail, healthcare, logistics, and hospitality is also expected to generate novel opportunities for product education and market penetration. Demonstrations, training initiatives, and region-specific awareness programs can highlight measurable benefits of airflow-based separation technologies and smart controls. By bridging knowledge gaps and enhancing technician skills, suppliers can accelerate adoption in developing regions. This combination of cost efficiency, smart performance, and awareness-driven strategies positions the market for broader penetration and sustained growth across diverse end-use sectors.

Category-wise Analysis

Product Type Insights

The non-recirculating segment is expected to account for an estimated 42% of the air curtains market revenue share in 2026, owing to their simple structure, lower cost, and adaptability across diverse commercial buildings. Their widespread adoption in retail outlets, transport hubs, hospitality facilities, and healthcare centers is driven by consistent indoor temperature maintenance without complex installation. Standardized door formats and modular designs further facilitate deployment in new construction and retrofit projects. Recent launches such as Systemair AB’s ultra-low-noise Air Curtain Unit that demonstrates how non-recirculating systems are adapted for noise-sensitive commercial spaces like hotels and offices, expanding usability beyond traditional industrial environments.

Heated air curtains are projected to be the fastest-growing, expanding at about 12% CAGR from 2026 to 2033, primarily due to their adoption in colder regions for heat retention and energy savings. Facilities across Europe and North America increasingly leverage heated variants to reduce HVAC load and maintain comfort at high-traffic entrances. Integration of Rosenberg Ventilatoren I-Series EC fans into heated models exemplifies energy-efficient, high-performance operation, improving airflow and reducing noise. Energy-efficiency programs and winterization requirements continue to accelerate installations in shopping centers, transport hubs, and hospitality establishments, making heated systems a key growth driver within the product landscape.

Airflow Capacity Insights

The 500–1000?m³/h segment is anticipated to lead the market with an estimated 38% revenue share in 2026, offering balanced performance for mid-sized retail stores, institutional buildings, and commercial spaces. These systems efficiently manage moderate door heights while maintaining indoor temperature stability with reasonable energy use. Their versatility across malls, clinics, schools, and restaurants reinforces adoption in markets seeking dependable, cost-effective solutions. Enhanced mid-range airflow performance is exemplified by Mars Air Systems AirStream Series, which features variable-frequency drives and smart control integration for energy optimization and remote monitoring in commercial and institutional buildings.

High-capacity systems exceeding 1500?m³/h are expected to register the fastest growth at approximately 13% CAGR between 2026 and 2033, driven by their wide utilization across industrial, logistics, and large manufacturing applications. These units protect wide or tall door openings against heat loss, dust, and particulate intrusion while maintaining workflow efficiency. Expansion in cold-chain logistics, automated warehouses, and heavy-duty industrial facilities has amplified demand for high-velocity air barriers. Rosenberg Ventilatoren PlugFan 2025 series illustrates efficiency upgrades for industrial high-capacity units, boosting airflow performance and noise reduction for large-scale facilities.

Application Insights

The commercial sector is expected to remain the dominant application, holding an estimated 48% of the air curtains market revenues in 2026, fueled by deployment of these systems across retail chains, hotels, airports, malls, and public transit facilities. High foot traffic and stringent indoor air quality (IAQ) requirements make air curtain systems critical for climate stability and contaminant control. Commercial real estate expansion and regulatory emphasis on IAQ reinforce adoption, while low-noise products like Systemair AB’s ultra-quiet air curtains encourage uptake in noise-sensitive offices and hospitality environments.

The industrial segment is projected to grow the fastest at roughly 10% CAGR during the 2026-2033 forecast period, supported by the increasing use of air curtains in manufacturing plants, warehouses, cold-storage units, and food-processing facilities. Industries rely on air curtains to maintain temperature consistency, support hygiene standards, and protect processes from external particles. Expansion in logistics networks, automation-driven factories, and modernized production environments further strengthens adoption. Their role in safeguarding workflow efficiency and energy performance makes industrial environments a key contributor to future market acceleration.

Regional Insights

North America Air Curtains Market Trends

North America is likely to remain a mature and well-established market for air curtains, led by the United States, with an estimated 34% market share in 2026. Market growth is supported by stringent HVAC efficiency standards, strong commercial real estate development, and government initiatives promoting energy-saving building technologies. Commercial facilities, logistics centers, retail chains, and industrial complexes heavily rely on consistent indoor climate control, while Canada drives additional demand for heated air curtains during severe winter months.

Investment trends focus on IoT-enabled air curtain systems, automation compatibility, and high-performance motors, improving operational efficiency and energy savings. Regulatory frameworks such as ASHRAE standards provide market stability. Infrastructure modernization in public transit, healthcare, and industrial facilities opens new deployment opportunities. Rising cross-border e-commerce and warehouse automation further increase demand for industrial-grade models. North America remains a key regional market, combining steady demand with high adoption of innovative, energy-efficient air curtain technologies, advanced controls, and smart integration solutions for commercial and industrial applications.

Europe Air Curtains Market Trends

Europe is a regulation-driven and mature market, projected to hold around 21% of the air curtains market share in 2026, with strong adoption across Germany, the U.K., France, and Spain. Growth is supported by energy-efficiency directives, country-level building codes, and increasing commercial and industrial demand. Colder climates drive adoption of heated air curtains, while sustainability goals encourage variable-speed and energy-efficient models in both retrofits and new construction.

Industrial growth is bolstered by urban infrastructure upgrades, public transportation projects, and cross-border logistics corridors. Harmonized regulations across member states simplify market expansion, and innovation emphasizes sustainability, advanced controls, and integration with intelligent building management platforms. Mandatory energy-efficiency policies ensure consistent adoption despite economic fluctuations. Europe represents a stable and resilient market, with opportunities across retail, healthcare, transportation, and industrial sectors, offering a favorable environment for manufacturers to deploy energy-efficient and smart air curtain technologies to meet diverse commercial and industrial application needs.

Asia Pacific Air Curtains Market Trends

Asia Pacific is predicted to dominate with an estimated 42% market share in 2026, as well as register the highest CAGR of approximately 13% through 2033. Rapid urbanization, large-scale commercial and industrial development, and increasing adoption of energy-efficient building technologies drive demand across China, India, Japan, and ASEAN countries. China leads manufacturing of air curtain components, while India and Southeast Asia see strong adoption in retail, hospitality, and logistics sectors.

Regional air curtains market growth is further bolstered by strengthening cold-chain infrastructure, e-commerce warehousing, and food-processing industries, boosting demand for industrial and high-airflow air curtain systems. Manufacturers increasingly focus on motor efficiency, noise reduction, and smart control technologies. Government policies promoting indoor air quality and energy performance enhance market prospects. Massive infrastructure investments, expanding organized commercial formats, and industrial modernization across Asia Pacific make it the primary growth engine for this market, ensuring sustained adoption of smart, energy-efficient, and high-performance air curtain solutions across commercial and industrial applications.

Competitive Landscape

The global air curtains market structure is moderately consolidated, led by major HVAC manufacturers such as Mars Air Systems, Panasonic, Mitsubishi Electric, Systemair, and Berner International. These companies benefit from strong engineering expertise, extensive distribution networks, and broad product portfolios that include heated, non-heated, commercial, and industrial models. Investments in energy-efficient motors, IoT-enabled controls, EC technology, and low-noise designs support their competitive strength. Their focus on sustainability, regulatory compliance, and smart building integration enhances product differentiation. Strong after-sales service and multi-channel presence further reinforce leadership. Continuous innovation enables them to cater to diverse sectors such as retail, healthcare, logistics, and manufacturing.

Alongside global leaders, regional and mid-sized manufacturers compete through localized customization, faster installation, and cost-effective offerings. These players focus on budget-friendly commercial applications and maintain strong relationships with distributors and contractors. The rise of smart buildings and demand for indoor air hygiene has opened opportunities for new entrants specializing in automation and sensor-based airflow optimization. Digital sales channels are improving visibility for smaller brands, while energy-efficiency regulations are driving product upgrades. Companies emphasizing eco-friendly materials, reduced power consumption, and advanced airflow control are gaining a competitive edge.

Key Industry Developments

- In November 2025, Kolkata airport added around 170 high-powered air curtains at terminal entry, exit, aerobridge, and shuttle-bus gates as part of a wider vector-control drive. Alongside stricter enforcement to keep curtains switched on, authorities are intensifying fogging, grass trimming, larvicide spraying, and use of guppy fish, while trying to maintain an indoor temperature near 22°C to discourage mosquito activity.

- In July 2025, Berner launched a redesigned Intelliswitch™ control across its Architectural Series, incorporating touchscreen interface, smart-app connectivity, and BMS integration. The upgrade enables real-time monitoring, adaptive airflow control, and enhanced energy savings, positioning Berner as a leader in smart, connected air?curtain solutions for commercial and institutional buildings.

- In May 2025, Airtècnics introduced six new industrial air?curtain models featuring 170?W EC fans. The updated series delivers 13% higher airflow, quieter operation, and improved energy efficiency for doors up to 5?m, strengthening the company’s presence in industrial and commercial installations. This launch reinforces Airtècnics’ focus on energy-efficient, high-performance solutions tailored to modern facility requirements.

Companies Covered in Air Curtains Market

- Panasonic Corporation

- Mitsubishi Electric Corporation

- Systemair AB

- Mars Air Systems

- Berner International

- Toshiba Carrier Corporation

- Rosenberg Ventilatoren GmbH

- Airtecnics

- Thermoscreens Ltd.

- Luft System

- Teplomash

Frequently Asked Questions

The global air curtain market is projected to reach US$ 1.2 billion in 2026.

Strong regulatory focus on HVAC efficiency, widespread demand for indoor climate control, and implementation of energy-saving initiatives are driving the market.

The market is poised to witness a CAGR of 8.3% from 2026 to 2033.

Major opportunities lie in heated air curtains, high-airflow systems, IoT-enabled smart controls, sustainable energy-efficient solutions, and integration with modern HVAC and building management systems.

Mars Air Systems, Berner International, Panasonic, Mitsubishi Electric, and Systemair are some of the key players in the market.