- Energy Storage Solutions

- AI in Energy Distribution Market

AI in Energy Distribution Market Size, Share, and Growth Forecast, 2026 - 2033

AI in Energy Distribution Market by Component Type (Solution, Services), AI Technology (Machine Learning & Predictive Analytics, Deep Learning & Neural Networks, Computer Vision & Image Processing, Reinforcement Learning & Autonomous Systems, Misc.), Application (Energy Demand Forecasting, Grid Optimization, Energy Storage, Renewable Integration, Others), End-user, and Regional Analysis for 2026 - 2033

AI in Energy Distribution Market Size and Trends Analysis

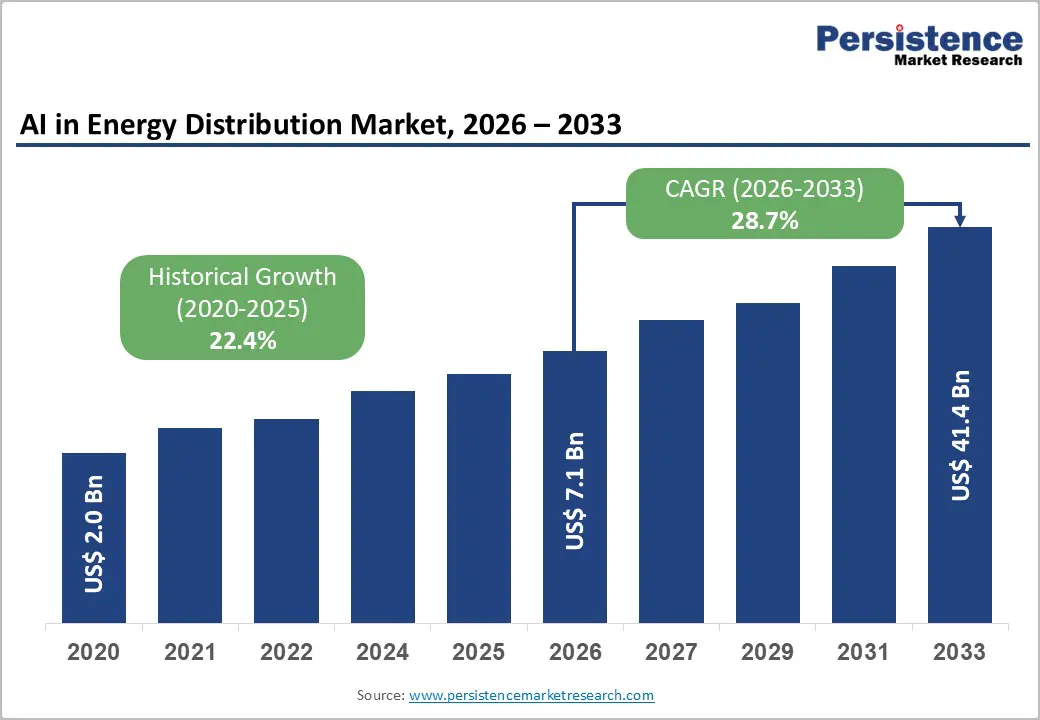

The global AI in energy distribution market size is likely to be valued at US$ 7.1 billion in 2026 and is projected to reach US$ 42.7 billion by 2033, growing at a CAGR of 29.2% between 2026 and 2033.

AI demand in energy networks aligns with the sharp escalation of electricity use in digital infrastructure, with data centre electricity consumption estimated at 415 terawatt hours and projected to approach 945 terawatt hours by 2030, largely driven by AI workloads. Utilities, regulators, and technology firms position AI as a critical lever to manage renewable variability, data centre clustering, and system flexibility, ensuring reliable, affordable, and lower-emission power delivery in the AI in energy distribution market.

Key Industry Highlights:

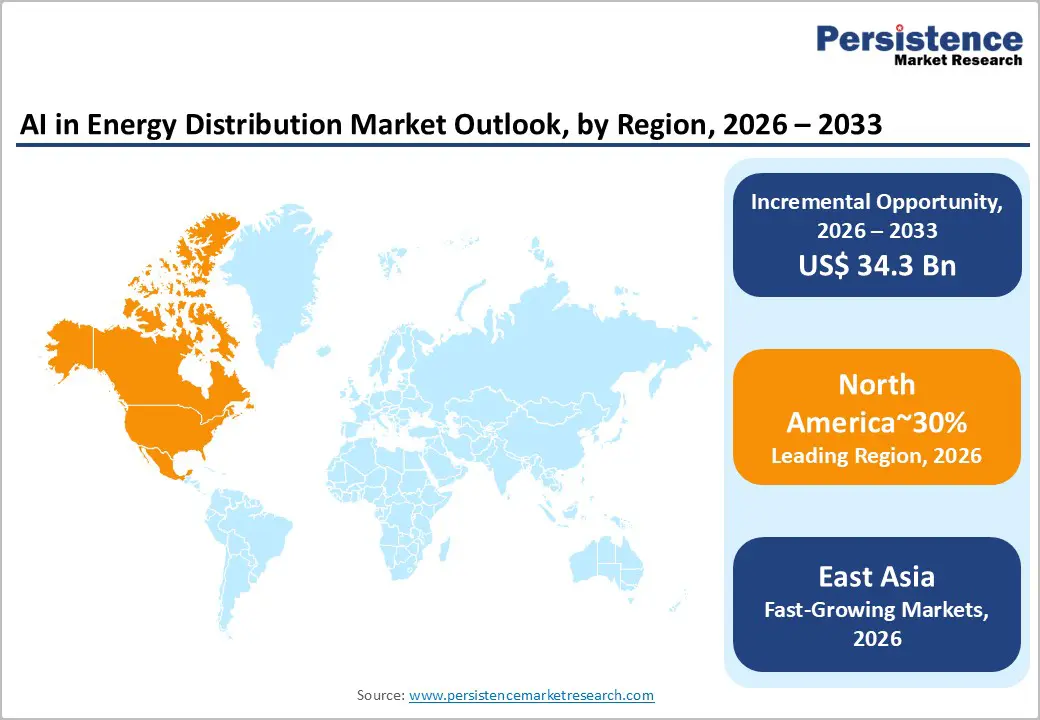

- Regional Leadership: North America leads the Global AI in Energy Distribution market with around 30% share, supported by the world’s highest per-capita data centre electricity use and advanced grid digitalisation programmes.

- East Asia Energy Market Scenario: East Asia holds about 22% share, anchored by China, Japan, and South Korea, where accelerating data centre build-outs and large renewable portfolios drive utility demand for AI-enabled grid optimisation.

- European Policies: Europe accounts for a roughly 25% share, underpinned by a regulatory focus on clean energy, targets for data centre efficiency, and a power mix where renewables and nuclear are set to supply most additional electricity needs.

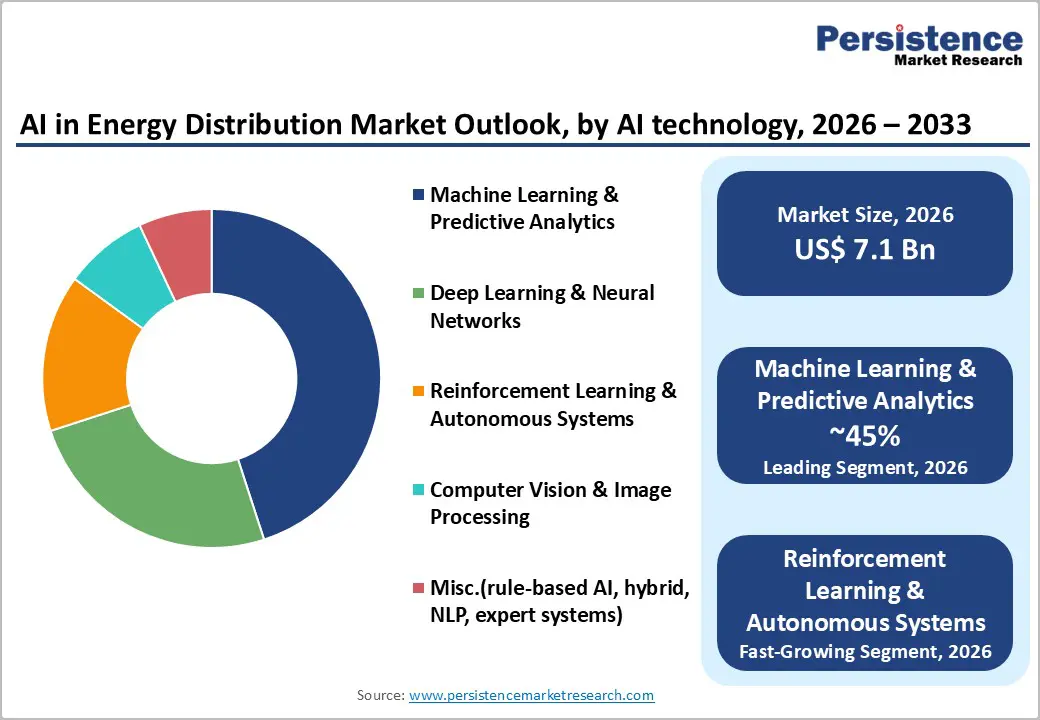

- Technological Dominance: Machine Learning and Predictive Analytics command about 45% share in the AI in Energy Distribution market, reflecting its central role in energy demand forecasting, asset health prediction, and power quality analytics across utility grids.

- Application Leadership: Energy Demand Forecasting is the leading application with around 27% share, as system operators depend on AI to anticipate loads from clustered data centres and electrified end-users and to plan reliable dispatch.

- Opportunity in renewable integration: Renewable Integration represents the fastest-accelerating application cluster, as utilities deploy AI to manage variable wind and solar output, coordinate storage, and minimise curtailment in increasingly decarbonised grids.

| Key Insights | Details |

|---|---|

| AI in Energy Distribution Market Size (2026E) | US$ 7.1 Bn |

| Market Value Forecast (2033F) | US$ 41.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 28.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 22.4% |

Market Dynamics

Drivers - Rise in Electricity Infrastructure Modernisation Requirements

The transition toward decarbonised energy systems necessitates sophisticated artificial intelligence solutions for managing variable renewable generation sources within the AI in Energy Distribution Market. The International Energy Agency projects that renewable generation supporting data centre electricity demand alone will grow by over 450 terawatt hours, demonstrating the scale of integration requirements across broader grid infrastructure. Solar photovoltaic and wind installations exhibit inherent intermittency, with output fluctuations occurring within seconds based on weather patterns, cloud cover, and atmospheric conditions.

Machine learning algorithms analyse weather patterns, historical generation data, and satellite imagery to predict renewable energy production with accuracy improvements of up to 20% compared to conventional forecasting methods. AI-driven systems enable grid operators to anticipate supply variations, automatically adjust dispatchable generation resources, and coordinate energy storage discharge cycles to maintain grid stability. 41% of North American utilities have fully integrated AI, data analytics, and grid edge intelligence, surpassing their own projections that full integration would require up to five years.

The United States targets 44% renewable electricity penetration, creating demand for AI capabilities that process data volumes and respond at speeds that variable renewable integration mandates. These intelligent systems reduce renewable energy curtailment, maximise clean energy utilization, and unlock transmission capacity without requiring new infrastructure construction, with the potential to access up to 175 gigawatts of additional transmission capacity through optimisation algorithms alone.

Infrastructure Modernisation Requirements Across Ageing Electricity Networks

Legacy electricity distribution systems designed for unidirectional power flows from centralised generation facilities lack the digital infrastructure necessary for managing distributed energy resources, bidirectional power flows, and dynamic load patterns characterising modern grids within the AI in Energy Distribution Market. Over 70% of energy sector executives believe AI and grid software are essential to integrating renewables, optimising energy efficiency, and enabling electrification, according to the Siemens Infrastructure Transition Monitor study of 1,400 global leaders. Traditional grid architectures cannot process the massive data streams generated by IoT sensors, smart meters, and grid edge devices deployed across transmission and distribution networks. Artificial intelligence platforms provide comprehensive transparency into grid operations, enabling utilities to detect faults up to 500 times faster than conventional monitoring methods.

Predictive maintenance applications analyse equipment performance data to identify degradation patterns before failures occur, with utilities implementing AI-enhanced systems reporting 60% fewer emergency repairs and 25 to 30% reductions in maintenance costs while minimising equipment breakdowns by 70 to 75%. The concentration of data centres in specific regions exacerbates local grid constraints, with approximately 20% of planned data centre projects facing delays due to connection queue backlogs and transmission equipment shortages. Grid operators leverage AI to monitor transmission lines, isolate faults in real time, and optimise load distribution across substations, creating networks that operate on second-by-second intervals rather than minute-by-minute response time.

Restraint - Substantial Capital Requirements for Technology Implementation and System Integration

The deployment of artificial intelligence solutions within energy distribution networks demands significant financial investment in hardware infrastructure, specialised software platforms, and system integration services that create barriers, particularly for utilities in emerging markets.

Hardware components, including high-performance computing systems, IoT sensors, grid edge devices, and communication networks, require substantial upfront capital allocation. Software development costs prove expensive, particularly when tailored algorithms address specific energy sector requirements, with custom AI solutions commanding premium pricing compared to generic platforms requiring extensive customisation. Integration of AI software with existing information technology systems necessitates modifications to legacy infrastructure, process redesign, and staff retraining initiatives that compound implementation expenses.

Geographically dispersed energy system components located far from central control facilities increase installation costs as technicians travel to remote locations for equipment deployment. Testing complex energy systems requires specialised equipment, dedicated facilities, and highly skilled engineers whose time contributes significantly to project budgets.

Opportunity - Advancement of Autonomous Grid Management Through Reinforcement Learning

Reinforcement learning algorithms enable energy distribution systems to develop optimal operational strategies through continuous interaction with grid environments, learning from outcomes to improve decision-making without explicit programming for every scenario within the AI in Energy Distribution Market. Deep reinforcement learning frameworks optimise energy dispatch strategies to minimise costs and maximise renewable energy source utilisation, demonstrating significant improvements in energy efficiency and operational resilience compared to traditional rule-based methods. These autonomous systems adapt dynamically to variations in energy demand and environmental conditions, continuously enhancing energy allocation strategies through learning to improve resource efficiency and minimise waste.

Proximal policy optimisation agents integrated with transformer architectures for renewable generation forecasting make real-time decisions in simulated environments, advancing smart grid technologies toward zero-carbon energy systems. The Siemens Infrastructure Transition Monitor revealed that 59% of energy sector executives plan major investments in autonomous systems for grids, with AI expected to lower operating costs, enhance reliability, and improve energy efficiency across distribution networks

Autonomous microgrid management applications tailored for remote communities demonstrate how reinforcement learning addresses unique operational challenges in geographically isolated systems. These frameworks optimise microgrid energy dispatch by forecasting renewable generation patterns, coordinating battery storage discharge cycles, and managing backup generation resources to ensure a continuous electricity supply while minimising fossil fuel consumption.

The integration of blockchain technology with deep reinforcement learning provides immutable transparency and secure data management in autonomous energy systems, validating scalable solutions for smart city infrastructure through comprehensive simulations and practical experiments. Companies implementing these advanced methodologies achieve notable enhancements in peak demand management, carbon emission reductions, renewable integration%ages, and data integrity measures that reshape urban energy management

Enhancement of Battery Energy Storage Systems Through Predictive Intelligence

Artificial intelligence applications in battery energy storage management unlock significant value by optimizing charge discharge cycles, predicting degradation patterns, and extending operational lifespans of storage assets supporting renewable energy integration within the AI in Energy Distribution Market. The success of wind and solar generation depends critically on the ability to store energy to meet inconsistent demand fluctuations, with AI-powered battery management systems offering robust, flexible, and sustainable solutions for grid stability.

Machine learning algorithms process large volumes of battery usage data to reveal patterns guiding smarter management decisions, including usage analysis across different conditions, real-time health monitoring to predict failures, and lifecycle assessments evaluating remaining operational duration. Predictive maintenance capabilities enable batteries to signal service requirements before issues arise, reducing downtime, cutting costs through preventive intervention, and prolonging battery lifespan through optimal maintenance schedules.

Real-time adaptive controls allow AI systems to automatically adjust charging speeds based on usage patterns, distribute power efficiently across grid-connected storage assets, and maintain optimal temperature conditions for battery health preservation. AI-driven battery management extends usable lifespan by up to 40% through predictive maintenance and smart charging while reducing range estimate errors by up to 20% for electric vehicle applications. Second-life battery applications repurpose electric vehicle batteries for stationary energy storage benefit from AI monitoring of variable battery conditions, complex management requirements, and safety performance consistency across recycled assets. These cost-effective energy storage solutions reduce electronic waste, support sustainability objectives, and provide grid operators with flexible capacity for managing renewable intermittency and peak demand periods.

Category-wise Insights

AI Technology Analysis

Machine Learning and Predictive Analytics commands the leading position within the AI Technology segment, accounting for 45% market share as the predominant technological approach deployed across energy distribution networks. This dominance reflects the maturity and proven effectiveness of supervised learning algorithms, regression models, and time series forecasting techniques for demand prediction, load forecasting, and equipment performance monitoring applications.

Utilities using AI-enhanced predictive maintenance report 60% fewer emergency repairs, while demand forecasting achieves up to 20% improvement in accuracy compared to conventional statistical methods. Machine learning platforms analyse consumption patterns, historical load data, and environmental variables to generate accurate short-term and long-term demand projections that enable optimal generator dispatch, transmission capacity utilisation, and voltage regulation across distribution networks.

Reinforcement Learning and Autonomous Systems represents the fastest expanding technology category within this segment, driven by growing recognition of autonomous decision-making capabilities for real-time grid optimisation, distributed energy resource coordination, and self-healing network operations.

Application Analysis

Energy demand forecasting maintains the leading application segment position with approximately 27% market share, serving as the foundational use case for AI deployment in energy distribution networks. Accurate demand prediction enables utilities to optimise generation scheduling, minimise reserve capacity requirements, reduce fuel costs, and maintain grid stability through proactive resource allocation. AI systems forecast usage spikes, recommend load adjustments, and automate operational decisions to align generation with consumption patterns more precisely than conventional forecasting methodologies. Machine learning algorithms sift through historical consumption data, weather forecasts, calendar patterns, and economic indicators to identify relationships and trends that human analysts might overlook, providing invaluable information for anticipating future dynamics and adapting to changes ahead of competitors.

Renewable Integration demonstrates the fastest expansion within the application segment as utilities confront mounting challenges of incorporating variable solar and wind generation into distribution networks designed for dispatchable conventional power sources. AI enhances renewable integration by analyzing real time weather conditions, historical trends, and environmental data to predict near term energy production with greater accuracy, cutting uncertainty and boosting grid assimilation.

Regional Insights and Trends

North America AI in Energy Distribution Market Trends

North America commands approximately 30% of Global AI in the energy distribution market, establishing the region as the largest geographic segment driven by substantial data center expansion, aggressive utility modernisation programs, and supportive regulatory frameworks for clean energy transition. The United States hosts 45% of global data centre electricity consumption, with facilities projected to consume more electricity than the combined production requirements of aluminium, steel, cement, chemicals, and all other energy-intensive manufacturing sectors.

Data center electricity demand in the United States is projected to increase by approximately 240 terawatt hours, representing 130% growth from current consumption levels as AI workloads drive accelerated server deployment. This concentration creates substantial local grid stress, with approximately 20% of planned data centre projects facing delays due to lengthy connection queues, transmission line lead times, and generation equipment shortages.

Utilities across North America have responded by accelerating AI adoption for grid management, with 41% achieving fully integrated AI, data analytics, and grid edge intelligence ahead of their own five-year integration timelines, according to Itron's Resourcefulness Report.

ABB invested in Edgecom Energy, a generative AI energy management startup, to enhance AI solutions for industrial and commercial customers through platforms that optimise power demand peaks, reducing energy costs, and improving efficiency across North American markets.GE Vernova released whitepapers outlining pragmatic AI adoption approaches for intelligent energy grids, highlighting how AI enhances grid operations, planning, and energy market management by improving detection, prediction, and optimisation of complex challenges, including distributed generation, intermittent renewables, and extreme weather events

East Asia AI in Energy Distribution Market Trends

East Asia represents approximately 22% of the Global AI in Energy Distribution Market, with China, Japan, and South Korea driving regional adoption through manufacturing sector digitisation, smart city initiatives, and renewable energy integration programs. China accounts for 25% of global data center electricity consumption, with regional demand projected to increase by approximately 175 terawatt hours, representing 170% growth as domestic technology companies expand cloud computing and AI service offerings. Coal currently supplies about 30% of data center electricity in China, though this share varies significantly across provinces, with renewable energy deployment accelerating to reduce the carbon intensity of digital infrastructure. Japan demonstrates strong per capita data center consumption growth, with demand increasing by around 15 terawatt hours, representing 80% expansion as the nation pursues digital transformation across industrial and commercial sectors.

Japan and South Korea together maintain approximately five% of global data centre electricity demand, with renewables and nuclear projected to provide nearly 60% of electricity consumed by data centres, up from 35% currently

Europe AI in Energy Distribution Market Trends

Europe accounts for approximately 25% of global AI in the energy distribution market, with the region demonstrating a strong commitment to decarbonization objectives, data sovereignty requirements, and grid modernisation investments supporting distributed energy resource integration. Europe represents 15% of global data centre electricity consumption, with regional demand projected to grow by more than 45 terawatt hours, representing 70% expansion as digital service providers establish local data center capacity to comply with regulatory requirements and reduce latency for European users. Renewables and nuclear power are positioned to supply most additional electricity required for data center operations, with their combined share rising to 85%, reflecting aggressive renewable deployment targets and continued nuclear capacity utilisation across France, Sweden, and other markets.

Siemens enhanced grid availability for Swiss utility IBC Energie Wasser Chur through its Electrification X IoT suite, providing comprehensive transparency by integrating smart fuses and grid sensors into existing infrastructure, enabling faster fault detection, optimised network performance, and reliable electricity supply to around 40,000 residents. This AI-driven approach supports management of distributed energy feeds, increased loads, and high voltage quality demands, offering a future-proof foundation for energy distribution optimization.

Competitive Landscape

The Global AI in Energy Distribution market exhibits a moderately concentrated competitive landscape, with established global technology giants holding significant influence. At the same time, a mix of mid-tier and niche players adds competitive pressure. Major incumbents such as Siemens AG, ABB Ltd, General Electric Company (GE), Honeywell International Inc., and Schneider Electric SE leverage deep domain expertise, strong R&D, and extensive utility partnerships to maintain leadership positions in AI-enabled grid optimisation, predictive maintenance, and smart distribution solutions.

Alongside these leaders, large IT and software companies like IBM Corporation and Microsoft Corporation also compete by integrating AI, cloud, and analytics into energy distribution platforms, intensifying competition and broadening capabilities. Although the top firms command substantial market share and technological depth, a diverse set of smaller and specialised providers contributes to innovation, making the market not fully oligopolistic but moderately concentrated, with ongoing alliances and technology partnerships shaping competitive dynamics.

Key Industry Developments

- In December 2025, Siemens enhanced grid availability for Swiss utility IBC Energie Wasser Chur using its Electrification X IoT suite, integrating smart fuses and grid sensors to enable real-time monitoring, faster fault detection, and predictive maintenance across the distribution network. The AI-enabled system provides 24/7 operational transparency and supports reliable electricity delivery to approximately 40,000 residents, demonstrating a practical deployment of AI for distribution resilience and performance optimisation.

- In June 2025, GE Vernova released two technical whitepapers outlining a structured AI adoption framework for intelligent grids and introduced its GridOS® Data Fabric platform to unify and contextualise transmission and distribution data. The solution enables utilities to apply AI for fault prediction, distributed generation management, and automated grid optimisation, supporting stepwise progression from decision support to autonomous operations and strengthening reliability in complex distribution environments.

- In January 2025, ABB announced an investment in Edgecom Energy, a generative AI-based energy management startup, to expand AI capabilities for commercial and industrial energy users. The collaboration focuses on optimising demand peaks, reducing energy costs, and improving load efficiency, directly supporting smarter distribution-level energy balancing and demand-side management across North America.

Companies Covered in AI in Energy Distribution Market

- Siemens AG

- Alpiq

- SmartCloud Inc.

- ABB

- General Electric

- Hazama Ando Corporation

- ATOS SE

- AppOrchid Inc.

- Zen Robotics Ltd.

- Honeywell International Inc.

Frequently Asked Questions

The global AI in Energy Distribution Market is projected to be valued at US$ 7.1 Bn in 2026.

The Solution segment is expected to account for approximately 54.0% of the Global AI in Energy Distribution Market by Design type in 2026.

The market is expected to witness a CAGR of 28.7% from 2026 to 2033.

Growth in the AI in Energy Distribution Market is driven by accelerating electricity infrastructure modernisation and renewable energy integration needs, as utilities adopt AI for real-time forecasting, grid optimisation, fault detection up to 500 into faster, predictive maintenance that cuts repairs by 60% and costs by 25-30%, and enhanced capacity utilisation to manage intermittent generation, rising data centre demand, and bidirectional power flows across ageing networks.

Key market opportunities in the AI in Energy Distribution Market include the deployment of reinforcement learning-based autonomous grid and microgrid management systems for real-time, self-optimising energy dispatch and resilience, alongside AI-driven predictive battery energy storage management that enhances charge-discharge efficiency, extends asset lifespan, reduces downtime and costs, and enables higher renewable integration and sustainable grid operations.

Key players in the AI in Energy Distribution Market include Siemens AG, ABB Ltd, General Electric Company (GE), Honeywell International Inc., and Schneider Electric SE.