- Smart Packaging

- Agriculture Packaging Market

Agriculture Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Agriculture Packaging Market by Material Type (Plastic, Biodegradable Films, Others), Application (Fertilizers, Crop Protection Biologics, Others), Product Form, and Regional Analysis for 2026 - 2033

Agriculture Packaging Market Size and Trends Analysis

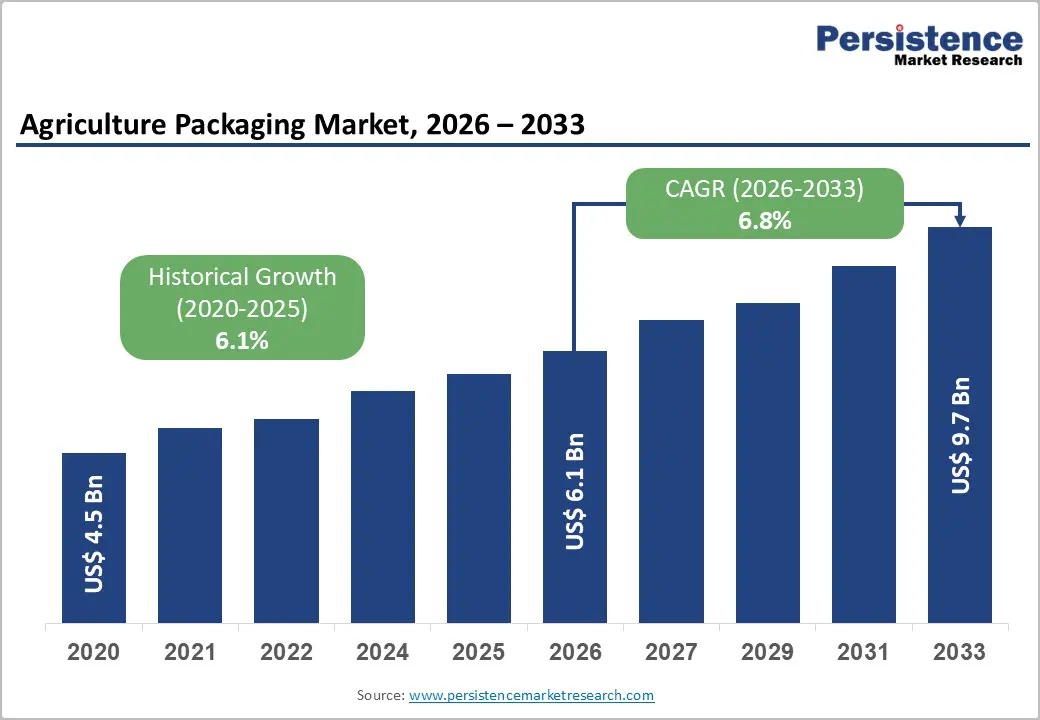

The global agriculture packaging market size is likely to be valued at US$6.1 billion in 2026 and is expected to reach US$9.7 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033, driven by rising agricultural output and fertilizer volumes, stronger demand for shelf-life and post-harvest loss reduction solutions, and regulatory pressure toward recyclable and compostable packaging formats. These factors are accelerating the adoption of advanced flexible films and bulk containers while maintaining steady baseline demand from fertilizers, seeds, and agrochemicals.

Key Industry Highlights

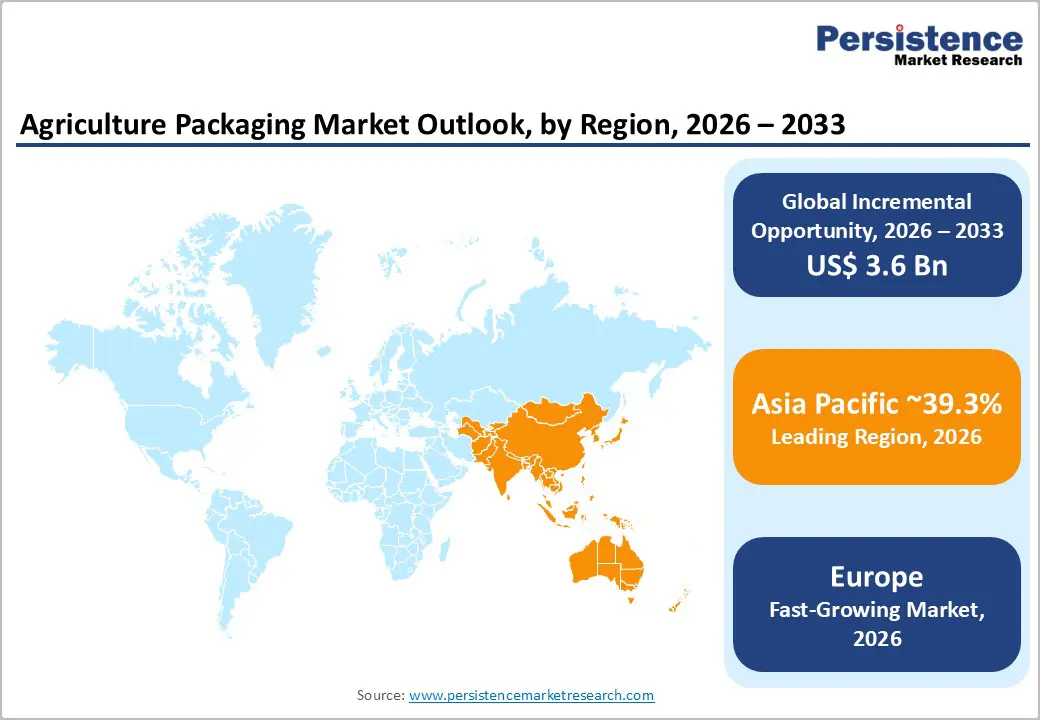

- Leading Region: Asia Pacific is projected to hold 39.3% of the market share, driven by large-scale agricultural production, high fertilizer consumption, and strong horticulture exports.

- Fastest-growing Region: Europe, led by Germany, the U.K., France, and Spain, with growth accelerated by EU PPWR regulations and sustainability-driven packaging adoption.

- Investment Plans: Expansion of flexible-film and FIBC capacity, development of biodegradable film supply chains, retrofitting automated filling lines, and strategic partnerships for recyclable mono-material and compostable packaging formats.

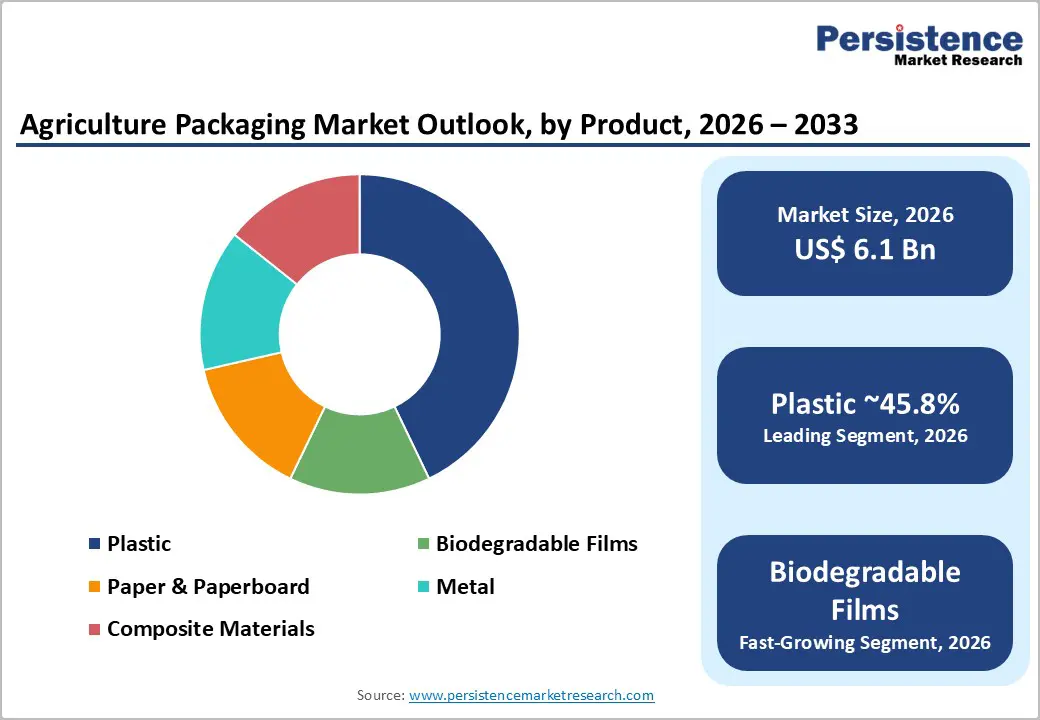

- Dominant Material Type: Plastic is anticipated to hold 45.8% market share, used for fertilizers, seed pouches, mulch films, and bulk liners.

- Leading Application: Fertilizers are anticipated to hold 37.6% market share, supported by multi-wall paper sacks, FIBC, and bulk packaging for industrial and retail distribution.

| Key Insights | Details |

|---|---|

| Agriculture Packaging Market Size (2026E) | US$6.1 Bn |

| Market Value Forecast (2033F) | US$9.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Driving Demand for Bulk Packaging Formats in Fertilizers

Global fertilizer consumption and agricultural output have recovered to pre-pandemic levels, creating robust demand for bulk packaging formats such as FIBC, multi-wall paper sacks, and bulk bags. Fertilizer demand remains high, with nutrient consumption projected at approximately 195-205 million tons, supporting consistent packaging throughput. Bulk packaging provides predictable revenue streams, with manufacturers benefiting from scale economies and capital investment in automated filling and dust-control systems. High-volume fertilizer tonnage ensures durable demand for bags, sacks, and bulk liners, forming the backbone of agricultural packaging.

Regulatory and Corporate Sustainability Targets

Tighter regulations in key markets, including EU packaging rules and state-level restrictions in the U.S., alongside corporate ESG goals, are shifting procurement toward mono-material PE/PP formats, recyclable flexible films, and certified biodegradable films. Compliance with reuse/recycling thresholds and bans on certain hazardous additives is driving the adoption of recyclable and compostable packaging. Suppliers capable of certifying recyclability or compostability are positioned to capture premium pricing opportunities, particularly in mono-material pouches and flexible films for seeds and agrochemicals.

Technological Innovation in Crop Protection Packaging

Advancements in bio-based barrier coatings, multi-layer co-extrusions, and digital traceability solutions are enhancing functional performance, including longer shelf life, reduced spoilage, and improved cold-chain management. Flexible packaging and biodegradable films have shown mid-single-digit CAGR growth, reflecting adoption trends. Packaging converters investing in R&D and validation for barrier films, active packaging, and RFID integration are capturing premium contracts with agrochemical and seed companies focused on product integrity and traceability.

Barrier Analysis - Raw-Material Price Volatility

Polyethylene, polypropylene, paper pulp, and adhesives experience periodic price fluctuations, limiting margin expansion for converters in price-sensitive agricultural segments. Double-digit price spikes in stressed years can reduce converter margins by several percentage points and delay capital investment in premium formats. Consequently, cost-sensitive farmers may resist price increases, slowing adoption of higher-value packaging and encouraging consolidation among low-cost, high-scale suppliers.

Fragmented Procurement and Long Purchase Cycles

While large agribusinesses centralize procurement, many smallholders and regional cooperatives purchase through distributors, necessitating multiple SKUs and low-volume runs. SKU proliferation increases warehousing complexity and per-unit logistics costs, constraining the rapid roll-out of new formats in fragmented markets. Packaging suppliers often rely on partnerships with distributors and local converters to manage these operational challenges.

Opportunity Analysis - Biodegradable and Compostable Films

Demand for biodegradable films in specialty agriculture, including mulch films, seed pouches, and horticulture, is rising due to regulations and farm-level sustainability programs. Adoption of even 5-10% across specialty applications could create a multi-hundred-million-dollar opportunity by 2030. Packaging firms can collaborate with biopolymer producers to scale compostable film lines and secure supply contracts with horticulture and premium produce exporters, creating long-term revenue growth.

Mono-Material Pouches and Recyclable Flexible Formats

The shift toward recyclable mono-material formats presents an opportunity for seeds and agrochemicals. With pouches growing at an 8.93% CAGR, these formats are becoming material revenue drivers. Suppliers can focus on certification, take-back programs, and recycling partnerships to ensure regulatory compliance and deliver convenience for end users, particularly in value-added product segments.

Category-wise Insights

Material Type Insights

Plastic, including polyethylene (PE), polypropylene (PP), and multi-layer flexible films, is expected to account for 45.8% of the market share, making it the leading material type. Plastic is widely adopted due to its cost efficiency, excellent moisture-barrier properties, chemical resistance, and compatibility with automated filling and handling systems. It is extensively used for fertilizers, seed pouches, mulch films, and bulk liners. For instance, multi-wall polypropylene sacks are standard for fertilizers distributed to smallholder retailers, while woven FIBC liners are used in industrial-scale bulk shipments of grains, seeds, and agrochemicals. Plastic’s adaptability allows high-volume manufacturers to leverage standardized formats, achieve operational scalability, and integrate dust-control and stacking solutions, making it indispensable for high-throughput agricultural supply chains.

Biodegradable films are likely to be the fastest-growing material segment. Adoption is driven by regulatory pressure on recyclability and compostability, retailer sustainability mandates, and farm-level circularity programs. These films are increasingly used in specialty applications, including compostable mulch films for vegetable production, horticultural wraps, and certified seed pouches for high-value crops. Pilot programs in Germany, the Netherlands, China, and India have demonstrated commercial potential, with partnerships between biopolymer producers and packaging converters reducing unit costs and enabling scaling of production. This growth reflects the transition of biodegradable films from niche applications to broader commercial deployment, particularly in markets where environmental compliance and premium crop packaging are key purchase drivers.

Application Insights

Fertilizer packaging is anticipated to account for 37.6% of the market share, maintaining its position as the largest application segment by volume and value. Packaging formats include multi-wall paper sacks, woven polypropylene bags, and FIBC bulk containers, designed to withstand high tonnage handling, prevent moisture ingress, and support dust-controlled automated filling. Standardized sizes, such as 25 kg retail paper sacks and 500-1,000 kg FIBC bags for industrial applications, ensure regulatory compliance and operational efficiency. For example, large commercial fertilizer manufacturers in India and the U.S. rely on bulk FIBC systems for transport, while smaller distributors utilize paper sacks for retail channels. The segment’s steady baseline demand is underpinned by fertilizer consumption trends linked to cropping intensity, application rates, and crop diversity, making it a predictable and high-volume driver of agricultural packaging revenue.

The crop protection biologics segment is expected to be the fastest-growing application category. This includes microbial pesticides, biostimulants, and seed treatments, all of which demand specialized packaging to preserve product integrity, protect against light, control moisture, and ensure precise dosing. The high per-unit packaging cost drives innovation in small-format options, such as pouches, sachets, and resealable stand-up pouches, particularly for live microbial products. For instance, resealable foil pouches for seed inoculants in Europe and light-blocking sachets for biostimulants in India and Japan are prime examples. This growth is further fueled by the rising use of biological inputs in sustainable agriculture and tighter regulations on chemical pesticide use, creating lucrative opportunities for packaging suppliers who can guarantee shelf-life, maintain sterility, and comply with international transport standards.

Regional Insights

North America Agriculture Packaging Market Trends - Technology and Compliance-Driven Growth in Seed & Fertilizer Packaging

North America is expected to hold a substantial share of the market, driven by large-scale commercial farms, a mature fertilizer and seed industry, and a dense distribution network. The U.S., as the regional leader, exhibits high packaging demand per hectare, stringent food-contact regulations, and a well-established recycling infrastructure. This environment supports widespread adoption of FIBC bulk containers, multi-wall paper sacks, and flexible pouches for specialty products, including value-added seeds and agrochemicals. Canada contributes to the regional demand through grain and fertilizer packaging, while Mexico is expanding in horticulture export packaging, particularly for fresh fruits and vegetables destined for the U.S. and European markets.

Growth in North America is supported by large volumes of fertilizer and feed, strong demand for value-added seed packaging, and regulatory pressure that encourages the adoption of recyclable mono-material formats. For instance, companies such as Berry Global and Sealed Air have expanded recyclable flexible-film and pouch product lines to meet the FDA and state-level PFAS restrictions. Compliance requirements have created barriers to low-cost entrants, motivating investment in retrofits of automated filling lines, testing laboratories for recyclability certification, and digital traceability systems such as RFID-enabled seed pouches. Strategic partnerships between converters and materials science firms further enhance capabilities, enabling suppliers to secure premium contracts in the specialty agrochemical and seed segments. Recent developments include Amcor’s launch of recyclable mono-material pouches in 2025 and Berry Global’s expansion of its high-barrier flexible film capacity, both of which reinforce North America’s position as a technology-driven and compliance-oriented market.

Europe Agriculture Packaging Market Trends - Policy-Led Innovation and Sustainability in Horticultural Packaging

Europe is likely to be the fastest-growing agricultural packaging region, with Germany, the U.K., France, and Spain serving as the core demand centers for horticultural packaging, seed pouches, and specialized agricultural films. Growth is heavily policy-driven, anchored by the EU Packaging and Packaging Waste Regulation (PPWR), which mandates recyclability thresholds, reuse targets, and limits on hazardous additives. Germany leads in industrial fertilizer packaging and high-performance barrier films, while the U.K. is notable for the rapid adoption of recyclable pouches for horticultural applications. France emphasizes moisture control and modified-atmosphere packaging for fruits and vegetables, and Spain serves as a hub for fresh produce exports, using mulch films and specialty pouches.

Key growth drivers include regulatory enforcement, increasing export quality requirements, and proactive investment by converters in mono-material and compostable technologies. Suppliers that align with PPWR compliance timelines, such as Mondi Group and Amcor Europe, gain first-mover advantages with large retailers and exporters. Capital investments are focused on R&D for mono-polymer laminates, partnerships with recyclers, and cross-border M&A to secure scale, enabling faster adaptation to regulatory changes. Notable regional developments include Mondi’s 2025 expansion of mono-material seed pouch production in Germany, Smurfit Kappa’s recyclable paper-based horticultural packaging trials in France, and RKW Group’s compostable mulch film pilot programs in Spain, all of which reinforce Europe’s growth trajectory while supporting sustainability mandates.

Asia Pacific Agriculture Packaging Market Trends - High-Volume Packaging Expansion and Export-Ready Solutions

Asia Pacific is projected to dominate the market, with a 39.3% share, driven by high agricultural output, substantial fertilizer consumption, and strong horticultural export activity. China, India, and the ASEAN countries account for most of the volume demand, while Japan and South Korea focus on high-value specialty packaging. China’s fertilizer and seed packaging industry is supported by large FIBC and flexible-film manufacturing clusters that serve both domestic and export markets. In India, modernization programs in fertilizer packaging and increasing adoption of pouches for seeds and agrochemicals are expanding market penetration. ASEAN countries are experiencing growth in mulch films and horticultural export packaging, reflecting rising quality standards for fresh produce shipments.

Growth is driven by rising cropping intensity, increased export of fresh produce, and domestic policies aimed at reducing post-harvest losses. Regulatory modernization is uneven, requiring converters that serve export markets to comply with EU and FDA standards, even where local rules are more lenient. Investment is concentrated on capacity expansions for FIBC and flexible films, development of local biodegradable film supply chains, and partnerships to introduce recyclable mono-material pouch technology. Examples include UFlex’s expansion of flexible-film and pouch lines in India for fertilizers and seeds, LC Packaging’s increase in FIBC capacity in China, and pilot programs for compostable films by regional converters in Southeast Asia, all of which strengthen both domestic production and export readiness. These initiatives position Asia Pacific as a high-volume, innovation-driven region while addressing sustainability and post-harvest loss reduction imperatives.

Competitive Landscape

The global agriculture packaging market combines a concentrated value-added flexible film and pouch segment with a fragmented bulk bag and sack supply chain. Leading global players dominate value segments, while numerous regional converters meet low-cost bulk demand. Concentration is higher in compliance-driven regions, where certification and scale are critical. Plastic/flexible film leaders dominate value share, while local manufacturers drive volume in bulk packaging.

Dominant strategies include product innovation, cost leadership, geographic expansion, and sustainability partnerships. Key differentiators include certification, supply reliability, and integrated filling solutions.

Key Industry Developments

- In September 2025, Sealed Air unveiled a new line of smart packaging solutions that utilize IoT technology to monitor the freshness of perishable goods, strengthening its position in supply chain transparency and food safety for agriculture and fresh produce.

- In June 2025, Amcor (AU) announced a partnership with an agricultural technology firm to develop biodegradable packaging solutions tailored to the fresh produce sector, aligning with rising demand for eco-friendly packaging formats.

Companies Covered in Agriculture Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- Sealed Air Corporation

- Berry Global, Inc.

- Sonoco Products Company

- Greif, Inc.

- UFlex

- LC Packaging International

- NNZ Group / ProAmpac

- RKW Group

- Parakh Agro Industries

- Western Packaging

- Huhtamaki Oyj

- DS Smith Plc

- Winpak Ltd.

- Coveris Holdings S.A.

- Klöckner Pentaplast Group

Frequently Asked Questions

The global agriculture packaging market is likely to be valued at US$6.1 billion in 2026.

The agriculture packaging market is expected to reach US$9.7 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

Key trends include the rising adoption of recyclable mono-material pouches and biodegradable films, regulatory-driven compliance (EU PPWR, PFAS limits), increasing demand for bulk and FIBC packaging for fertilizers, growth of specialty packaging for crop protection biologics and seeds, and technology integration for digital traceability, shelf-life enhancement, and active packaging.

By material type, plastic is anticipated to hold 45.8% market share, used for fertilizers, seed pouches, mulch films, and bulk liners.

The agriculture packaging market is projected to grow at a CAGR of 6.8% from 2026 to 2033.

Major players include Amcor plc, Mondi Group, Berry Global, Inc., Sealed Air Corporation, and UFlex.