- Industrial Goods & Service

- Controlled Environment Agriculture (CEA) Market

Controlled Environment Agriculture (CEA) Market Size, Share, and Growth Forecast, 2026 - 2033

Controlled Environment Agriculture (CEA) Market by Technology (Hydroponics, Aeroponics, Aquaponics, Soil/Substrate-Based Systems, Hybrid Systems), Facility Type (Vertical Farms, Controlled Plant Factories, Greenhouses, Container/Modular Farms, Rooftop/Indoor Farms, Others), Crop Type (Leafy Greens, Herbs & Microgreens, Fruit Vegetables, Berries, Flowers & Ornamentals, Medicinal Plants, Seedlings & Transplants), and Regional Analysis for 2026 - 2033

Controlled Environment Agriculture (CEA) Market Share and Trends Analysis

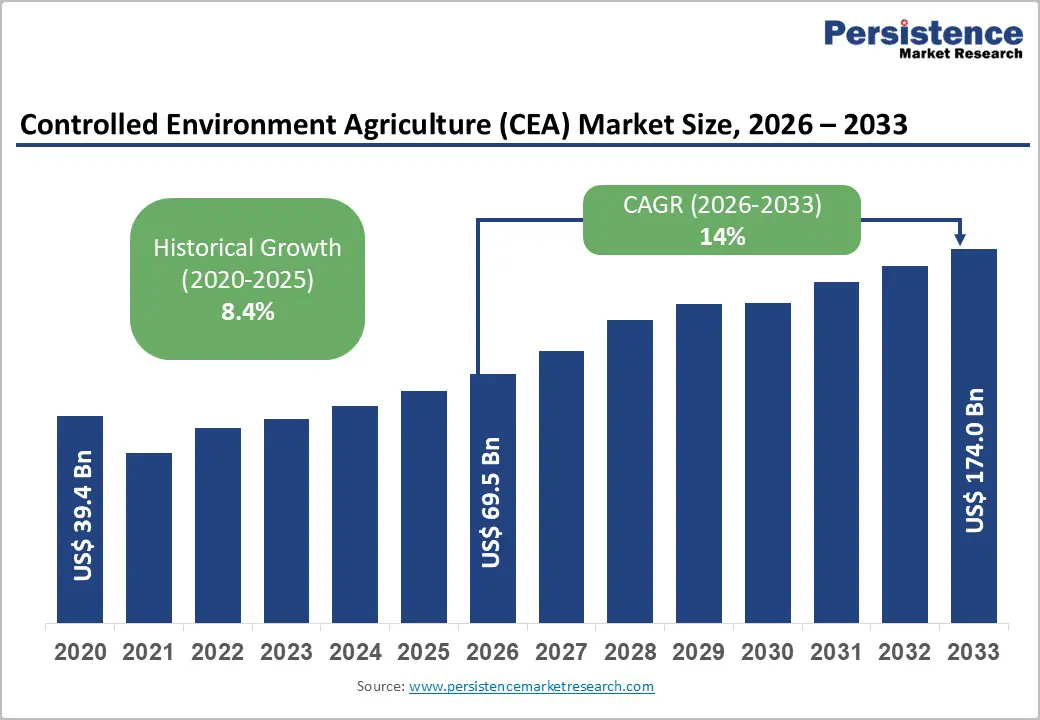

The global controlled environment agriculture (CEA) market size is likely to be valued at US$ 69.5 billion in 2026, and is projected to reach US$ 174.0 billion by 2033, growing at a CAGR of 14% during the forecast period 2026 - 2033.

The market is entering a sustained expansion cycle as structural pressure on arable land and accelerating urbanization are reshaping food production models. Urban population growth is intensifying demand for a stable, year-round supply of fresh produce, while retailers and foodservice operators are prioritizing traceability and local sourcing of crops. CEA platforms are improving output per square meter through precision control of temperature, humidity, carbon dioxide concentration, and nutrient delivery, thereby strengthening yield reliability relative to open-field agriculture.

Technologies such as multi-layer vertical cultivation racks, light-emitting diode (LED) grow lighting, and automated climate control are forming the operational backbone of modern facilities. Investment patterns are shifting accordingly, with agritech companies, institutional investors, and retail chains expanding capital allocation toward scalable indoor production models. Automation systems, Internet of Things (IoT) sensor networks, and predictive analytics platforms are reducing labor intensity and improving crop-forecasting accuracy. These capabilities are lowering operational volatility and enabling data-driven crop planning, which is becoming critical for long-term supply contracts.

Key Industry Highlights

- Dominant Facility Type: Greenhouses are expected to account for approximately 45% of CEA market revenues in 2026, reflecting their scalability, lower capital intensity.

- Fastest-growing Facility Type: Multi-level vertical farms are projected to expand at the highest CAGR of approximately 15% during 2026 - 2033, supported by urban land constraints and automation-driven cost optimization.

- Technology Leadership: Hydroponics is expected to account for nearly 48% of revenue in 2026, driven by water-use efficiency and modular deployment across greenhouse and indoor systems.

- Fastest-growing Technology: Aeroponics is expected to grow the fastest between 2026 and 2033, driven by improved nutrient delivery precision and accelerated crop cycles.

- Regional Dominance: North America is projected to account for approximately 37% of the market in 2026, driven by advanced agritech infrastructure and strong institutional investment.

- Fastest-growing Market: Asia Pacific is expected to be the fastest-growing market through 2033, with a projected CAGR of 15%, driven by the increasing deployment of smart greenhouses and vertical farming systems.

- December 2025: Agroz Group successfully cultivated Japanese strawberries in its AI-enabled vertical farming systems and plans to begin commercial distribution in Malaysia by mid-2026.

| Key Insights | Details |

|---|---|

| Controlled Environment Agriculture (CEA) Market Size (2026E) | US$ 69.5 Bn |

| Market Value Forecast (2033F) | US$ 174.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Urbanization-Driven Local Food Security

Urban population growth is concentrating food consumption within metropolitan areas while arable land per capita is steadily declining. This structural imbalance is increasing pressure on cities to secure reliable supplies of fresh produce through localized production systems. Across North America, Europe, and the Asia-Pacific region, municipal authorities and national governments are supporting the deployment of CEA to reduce reliance on long-distance imports and strengthen food security planning. Consumers in dense urban centers are increasingly purchasing pesticide-free and locally cultivated vegetables such as leafy greens and culinary herbs. This behavioral shift is accelerating demand for hydroponic cultivation and vertically integrated indoor farming facilities that produce stable year-round yields. Policy frameworks that prioritize domestic food resilience, along with public and private capital directed toward urban farming infrastructure, are reinforcing this transition toward controlled production environments.

Localized CEA production is strengthening supply chain stability by reducing exposure to transport disruptions and climate variability. Shorter distribution distances are improving product freshness and reducing spoilage rates, thereby increasing the attractiveness of long-term procurement agreements with supermarket groups and foodservice operators. Urban food consumption is continuing to rise in parallel with net metropolitan population growth, and this dynamic is supporting predictable demand expansion. These capabilities enhance bargaining power in high-density cities, where buyers prioritize reliability and traceability. As metropolitan markets expand, CEA facilities located near consumption hubs are strengthening competitive advantage and reinforcing long-term revenue stability.

Technology Convergence in Automation and IoT

CEA adoption is accelerating as automation systems, sensor networks, and integrated control platforms become more advanced and cost-effective. Precision climate regulation involves maintaining stable temperature, humidity, and carbon dioxide levels, whereas automated nutrient dosing systems deliver precise input quantities to plant roots. Artificial intelligence (AI)-powered yield forecasting tools are improving the accuracy of crop planning and reducing output variability. These technologies optimize the use of lighting electricity, irrigation water, and fertilizer inputs while simultaneously reducing manual labor requirements. As a result, operators are improving unit economics and are expanding production beyond high-margin niche crops into commercially scaled vegetables and selected fruit varieties. This technological maturity is strengthening the business case for CEA in mainstream retail supply chains rather than limiting it to specialty produce segments.

The operational benefits are becoming measurable. Automated data collection and analytics are reducing input waste and increasing consistency in harvest cycles, which is improving gross margins and inventory predictability. Facilities that integrate centralized control software are scaling production more efficiently across multiple sites, thereby enabling standardized cultivation protocols. This predictability is attracting institutional capital, as investors are prioritizing stable yield performance and transparent operating metrics. Public agencies and industry associations are incorporating digital agronomy and smart farming frameworks into research grants and modernization programs. Funding mechanisms are increasingly favoring systems that meet sustainability reporting standards and traceability requirements. As regulatory expectations for environmental performance tighten, digitally integrated CEA facilities are positioning themselves to comply more effectively and secure long-term growth opportunities.

High Capital Intensity and Payback Uncertainty

Specialized facilities for controlled-environment agriculture operations, particularly multi-tier vertical farms and fully enclosed plant factories, require substantial upfront capital. Developers are investing heavily in LED grow lighting, heating, ventilation, & air conditioning (HVAC) systems, environmental sensors, and automated control infrastructure. In addition, project developers are incurring costs related to site preparation, reinforced flooring, insulation systems, and grid connectivity upgrades. Skilled agronomists, data engineers, and technical maintenance staff are also increasing fixed operating expenditures. As a result, total project costs are increasing before revenue is generated. The investment recovery period is typically extended over multiple years and remains sensitive to electricity pricing, yield consistency, and contract stability. Facilities that fail to reach optimal capacity utilization are experiencing prolonged breakeven timelines, which are increasing financing risk for lenders and equity partners.

Capital intensity is becoming more pronounced in regions with elevated electricity tariffs or import duties on critical components, such as climate-control equipment and LED systems. These structural cost burdens are constraining participation among small & medium-sized enterprises (SMEs) that lack access to low-cost financing. In Europe and North America, where energy pricing structures vary widely across jurisdictions, profitability is closely tied to local utility rates and the integration of renewable energy. Without favorable power purchase agreements or on-site generation capacity, operators are facing margin compression relative to open-field agriculture for commodity crops. This dynamic limits CEA's competitiveness outside premium produce categories unless operators secure long-term supply contracts or leverage policy incentives. Strategic cost modeling, energy-sourcing optimization, and phased capacity expansion are therefore becoming essential to sustainable project development.

Energy Consumption and Resource Efficiency Trade-Offs

CEA facilities deliver consistent, year-round production yet consume substantial electricity, particularly in systems that rely heavily on artificial illumination and HVAC. Continuous operation of LED grow lights, dehumidification systems, and temperature-control equipment is driving a high baseline power demand. When operators are not integrating renewable energy sources or waste-heat recovery technologies, operating expenses are rising materially and are compressing gross margins. Academic research published in Nature indicates that, in certain regions, indoor farming systems consume significantly more energy per kilogram of produce than conventional agriculture when facilities are not optimized for efficiency. These findings underscore that design quality, energy sourcing strategy, and system integration directly influence financial performance and environmental credibility.

Exposure to electricity price volatility and grid instability is increasing operational risk for CEA operators. Markets with access to subsidized renewable power, favorable feed-in tariffs, or strong energy efficiency incentives are creating a more supportive cost environment for indoor cultivation. Conversely, regions that rely on expensive, fossil-fuel-based electricity or imported heating fuels face higher breakeven thresholds, particularly in colder climates where heating loads are substantial. Operators in these markets are increasingly investing in combined heat and power systems, solar photovoltaic integration, and thermal energy storage to stabilize cost structures. Until energy optimization technologies achieve wider commercial maturity and cost reductions, power consumption will remain a structural constraint on scalability. Strategic energy procurement planning and infrastructure partnerships are, therefore, becoming central components of long-term competitiveness in the CEA industry.

Scaling Premium and High-Value Crop Production

Probably one of the greatest advantages of CEA systems is that they can facilitate structured expansion into premium and high-value crop categories such as culinary herbs, microgreens, berries, and medicinal plants. These crop types are commanding higher price realization in metropolitan retail channels and regulated pharmaceutical supply chains due to quality sensitivity and traceability requirements. CEA platforms are standardizing light intensity, temperature gradients, humidity levels, and nutrient composition, which is improving uniformity in flavor profile, nutritional density, and visual quality. This controlled production model reduces variability and supports compliance with food safety and pharmaceutical standards. Even under moderate adoption scenarios, premium crop portfolios are projected to account for a double-digit share of overall CEA revenues by 2030, reflecting strong pricing power relative to commodity vegetables.

The commercial potential is increasingly actionable as operators form structured partnerships with foodservice brands, specialty grocers, and wellness-focused retail chains. Buyers prioritize year-round availability, pesticide-free cultivation, and consistent sensory attributes, which controlled systems deliver more reliably than open-field farming. Advanced data analytics and phenotype-optimized cultivation protocols are improving yield predictability and enabling crop customization in response to market demand. Facilities that are leveraging AI-driven growth modeling and real-time performance monitoring are scaling premium portfolios more efficiently while protecting margins. As consumer health awareness rises and traceability standards tighten, high-value crop specialization is strengthening revenue resilience and offering a differentiated position within competitive urban markets.

Policy-Enabled Adoption and Public Funding for Resilience

National and regional policy frameworks are increasingly prioritizing food system resilience, climate adaptation, and sustainable agricultural transformation, and this shift is expanding deployment pathways for CEA. Governments are introducing subsidies for the adoption of agritech, offering tax incentives for energy-efficient infrastructure, and allocating public funding through research and development programs. These measures are lowering capital risk for private investors and are improving the financial viability of technologically advanced farming systems. In several jurisdictions, controlled-environment agriculture systems are being integrated into long-term food security strategies to reduce dependence on imported fresh produce and strengthen domestic supply reliability. Regulatory clarity regarding sustainability standards, water-efficiency targets, and emissions reporting is further shaping project design and operational benchmarks. As a result, policy alignment is reducing uncertainty and is encouraging institutional capital to participate in structured CEA investments.

This regulatory evolution is accelerating capacity expansion in regions that rely heavily on food imports and are seeking greater food sovereignty, including parts of the Middle East, East Asia, and Southern Europe. Clearly defined incentive schemes are improving access to concessional financing, development bank support, and public-private partnerships. In these markets, CEA facilities are moving beyond pilot projects and are scaling into medium-sized commercial operations that serve national distribution networks. Stable policy frameworks are enabling cost competitiveness through subsidized utilities, land grants, or infrastructure co-investment. These supportive conditions are expanding the addressable market beyond major metropolitan centers and enabling operators to balance quality, yield consistency, and price competitiveness.

Category-Wise Analysis

Technology Insights

Hydroponics is expected to be the leading technology, capturing an estimated 48% of the CEA market revenue share in 2026. Hydroponic systems deliver nutrients through water-based solutions rather than soil, enabling precise control over plant nutrition and resource consumption. Operators are adopting hydroponics because it improves yield stability, reduces water usage compared to conventional cultivation, and scales efficiently across leafy greens, herbs, and selected vegetable crops. The technology is serving as a practical transition pathway for greenhouse operators who are modernizing facilities without shifting to enclosed indoor production entirely. It is also forming the foundation of a large number and variety of vertical farm operations. A well-established supplier ecosystem for nutrient formulations, environmental sensors, and automation software is reinforcing hydroponics as the default commercial standard. Its relative operational simplicity compared with emerging alternatives supports continued global adoption and predictable performance across diverse climates.

Aeroponics is projected to be the fastest-growing cultivation technology through 2033. Aeroponic systems deliver nutrients in a fine mist directly to plant roots, significantly improving oxygen exposure and accelerating growth cycles. This method enhances water efficiency and reduces fertilizer waste, making it attractive for high-value crops and research-driven production models. As sensor precision improves and automated mist delivery systems become more affordable, aeroponics is expanding beyond experimental applications into scaled commercial facilities. Integration with predictive analytics platforms and root-zone monitoring tools is allowing operators to fine-tune nutrient delivery in real time. For urban producers seeking maximum yield per square meter and tighter input control, aeroponics is emerging as a differentiated pathway to improve operational efficiency and competitive positioning.

Facility Type Insights

Greenhouses are poised to dominate in 2026, accounting for approximately 45% of the controlled environment agriculture market revenue. Modern greenhouse structures, including advanced glass and polycarbonate installations, are integrating supplemental LED systems, automated ventilation, and precision irrigation without requiring the full capital intensity of enclosed vertical facilities. This hybrid approach enables operators to enhance productivity while maintaining cost efficiency. Commercial growers are continuing to favor greenhouses because they are scalable, operationally familiar, and compatible with established crop portfolios such as tomatoes, cucumbers, and sweet peppers. Existing supply chains for greenhouse inputs and distribution channels are supporting steady expansion across temperate climates.

Multi-level vertical farms are set to register the highest CAGR of about 15% between 2026 and 2033. These stacked cultivation systems are utilizing artificial lighting and tightly controlled indoor environments to maximize output per square meter, which is particularly valuable in densely populated urban areas where land availability is limited. Automation platforms, IoT-enabled climate monitoring, and AI driven crop management are compressing labor intensity and enhancing operational precision. Investors are increasingly targeting vertical farm models that align with integrated retail supply chains, including in-store cultivation and direct-to-consumer distribution strategies. As system efficiencies improve and technology costs moderate, vertical farms are expected to become more economically competitive with conventional greenhouses, supporting sustained above-average growth over the forecast period.

Regional Insights

North America Controlled Environment Agriculture (CEA) Market Trends

North America is anticipated to command an estimated 37% of the controlled environment agriculture market share in 2026. The market here benefits from advanced agricultural technology infrastructure, established greenhouse supply chains, and strong integration between producers and large retail networks. The United States is contributing the majority of regional revenue, supported by extensive greenhouse modernization, significant venture capital funding for vertical farming companies, and federal as well as state-level research incentives. Consumer preference for pesticide-free and locally cultivated produce is continuing to strengthen demand, particularly in suburban corridors and high-density metropolitan areas. Retail chains are expanding procurement contracts with CEA operators to ensure consistent year-round supply, which is reinforcing revenue stability and encouraging capacity expansion.

Adoption dynamics, however, vary across states due to differences in electricity pricing, labor availability, and renewable energy policy frameworks. States with supportive renewable portfolio standards and stable grid infrastructure, including California and parts of the Northeastern United States, are experiencing faster facility deployment. Operators in these markets are leveraging solar integration, long-term power purchase agreements, and automation systems to manage cost structures. Partnerships focused on supply chain digitization are improving traceability and inventory forecasting, which is strengthening competitive positioning in foodservice and grocery segments.

Europe Controlled Environment Agriculture (CEA) Market Trends

Europe is steadily expanding its footprint, with Western European economies driving most of the deployment. The region is likely to account for nearly 32% of the CEA market share in 2026, supported by structured regulatory frameworks focused on sustainable agriculture, climate adaptation, and urban food resilience. Germany, France, and the United Kingdom are prioritizing greenhouse modernization, digital monitoring systems, and IoT-enabled climate control to reduce dependency on imported vegetables. Operators are upgrading legacy greenhouse assets with energy-efficient LED lighting and advanced insulation systems to improve productivity while managing rising input costs. These modernization efforts are strengthening food security objectives and are supporting consistent year-round domestic supply in temperate climates.

High electricity and heating costs remain a structural consideration across the region, particularly in Northern Europe. However, operators are increasingly deploying heat recovery systems, combined heat and power units, and renewable integration strategies to stabilize operational expenses. European Union sustainability reporting requirements and circular agriculture policies are encouraging institutional investors to participate in CEA projects that demonstrate measurable environmental performance. Adoption rates vary across member states due to differences in subsidy structures, permitting processes, and national agricultural strategies. As a result, market penetration is progressing unevenly between Western Europe and parts of Southern and Eastern Europe.

Asia Pacific Controlled Environment Agriculture (CEA) Market Trends

Asia Pacific is set to emerge as the fastest-growing regional market for controlled environment agriculture through 2033, exhibiting a CAGR of roughly 16%, powered by rapid urban expansion, constrained arable land availability, and rising household incomes that are increasing demand for premium fresh produce. China and Japan are leading large-scale deployment of vertical farming systems and technologically advanced greenhouses to strengthen domestic food supply and reduce exposure to climate volatility. India is gradually expanding adoption through pilot smart greenhouse initiatives and hydroponic commercial farms serving metropolitan clusters. National development strategies across these countries are emphasizing agricultural technology modernization, including hydroponic cultivation, sensor-based crop monitoring, and data-driven yield optimization platforms. Government-backed innovation funds and agricultural transformation programs are providing capital support and regulatory clarity, which are lowering barriers to entry for commercial operators.

Supply chain modernization is further accelerating adoption. Cold chain expansion, digital traceability systems, and strategic partnerships with international agritech firms are enhancing production reliability and distribution efficiency. Urban consumers are prioritizing food safety, pesticide reduction, and consistent quality, which is reinforcing demand for controlled production environments. Operators are increasingly integrating AI-driven crop analytics and IoT-enabled environmental control systems to improve output consistency in dense metropolitan regions.

Competitive Landscape

The global controlled environment agriculture market structure is moderately fragmented, with participation from greenhouse automation manufacturers, vertically integrated indoor farming operators, and modular cultivation system providers. No single company is controlling a dominant global share, although concentration is gradually forming around hydroponic equipment suppliers and integrated automation platform developers. Established greenhouse technology firms are leveraging decades of operational expertise, while newer agritech companies are building differentiated value propositions around fully enclosed vertical farming and data-driven crop management. This structure is creating a competitive landscape where scale advantages are emerging in procurement, system integration, and long-term supply contracts, yet regional specialization remains significant.

Competitive positioning is increasingly defined by technological depth and ecosystem integration. Firms are investing in IoT-enabled climate control, AI-based growth optimization, and predictive analytics platforms that enhance yield stability and input efficiency. Strategic alliances with retail chains, foodservice operators, and logistics partners are improving supply chain synchronization and strengthening recurring revenue streams. At the same time, research and development expenditure is rising in areas such as advanced environmental sensors, energy management systems, and automated nutrient delivery technologies. Traceability compliance and energy efficiency performance are becoming procurement criteria for institutional buyers, which is compelling technology providers to prioritize measurable sustainability outcomes. As competitive intensity increases, companies that combine automation expertise with energy optimization capabilities are likely to secure stronger long-term positioning in both developed and emerging markets.

Key Industry Developments

- In November 2025, Amsterdam-based Source.ag raised US$ 17.5 million in a Series B round, led by Astanor Ventures with participation from seed breeder Enza Zaden and grower cooperative Harvest House. The company’s AI platform for CEA is now deployed in over 300 greenhouses across 18 countries, helping growers improve yield forecasting, automate irrigation, and optimize production efficiency.

- In October 2025, Premier Tech Growers and Consumers expanded its PRO-MIX® AGTIV® product lineup for CEA growers, combining traditional growing media with biological enhancements to support root development, nutrient uptake, and crop resilience. The new formulations, including PRO-MIX® NAX, NAO, and FVCO alongside established blends, are designed to meet diverse crop needs from leafy greens and herbs to tomatoes, cucumbers, peppers, and strawberries.

- In October 2025, the University of Wyoming launched the Controlled Environment Agriculture (CEA) Network, a new initiative designed to accelerate workforce development, research, and innovation in the expanding CEA sector, providing hands-on training, industry partnerships, and technology testing opportunities. The network is part of the Wyoming Innovation Partnership, bringing together academic, industry, and community stakeholders to build a collaborative ecosystem.

Companies Covered in Controlled Environment Agriculture (CEA) Market

- Bowery Farming Inc.

- Gotham Greens Holdings LLC

- AeroFarms LLC

- Infarm GmbH

- BrightFarms Inc.

- Priva Holding BV

- Heliospectra AB

- Kalera Inc.

- Freight Farms Inc.

- Sky Greens Pte Ltd.

- Urban Crop Solutions NV

- AgriCool SAS

- AgriTech Solutions

- Green Sense Farms Holdings Inc.

- Terra Firma Capital Partners Limited

Frequently Asked Questions

The global controlled environment agriculture (CEA) market is projected to reach US$ 69.5 billion in 2026.

Increasing deployment of vertical farms, hydroponic systems, and automated greenhouse infrastructure are driving the market.

The market is poised to witness a CAGR of 14% from 2026 to 2033.

Advent of advanced systems such as multi-layer vertical cultivation racks and automated climate control, channeling of capital toward scalable indoor production models, and integration of automation systems, IoT sensor networks, and predictive analytics platforms with farming operations are unlocking key market opportunities.

Bowery Farming Inc., Gotham Greens Holdings LLC, AeroFarms LLC, and Infarm GmbH are some of the key players in the market.