- Industrial Goods & Service

- Regenerative Agriculture Market

Regenerative Agriculture Market Size, Share, and Growth Forecast, 2025 - 2032

Regenerative Agriculture Market By Practice Type (Agroforestry, Silvopasture, Others), Application (Soil & Crop Management, Others), End-user (Farmers, Consumer Packaged Goods (CPG) Manufacturers, Others), and Regional Analysis for 2025 - 2032

Regenerative Agriculture Market Share and Trends Analysis

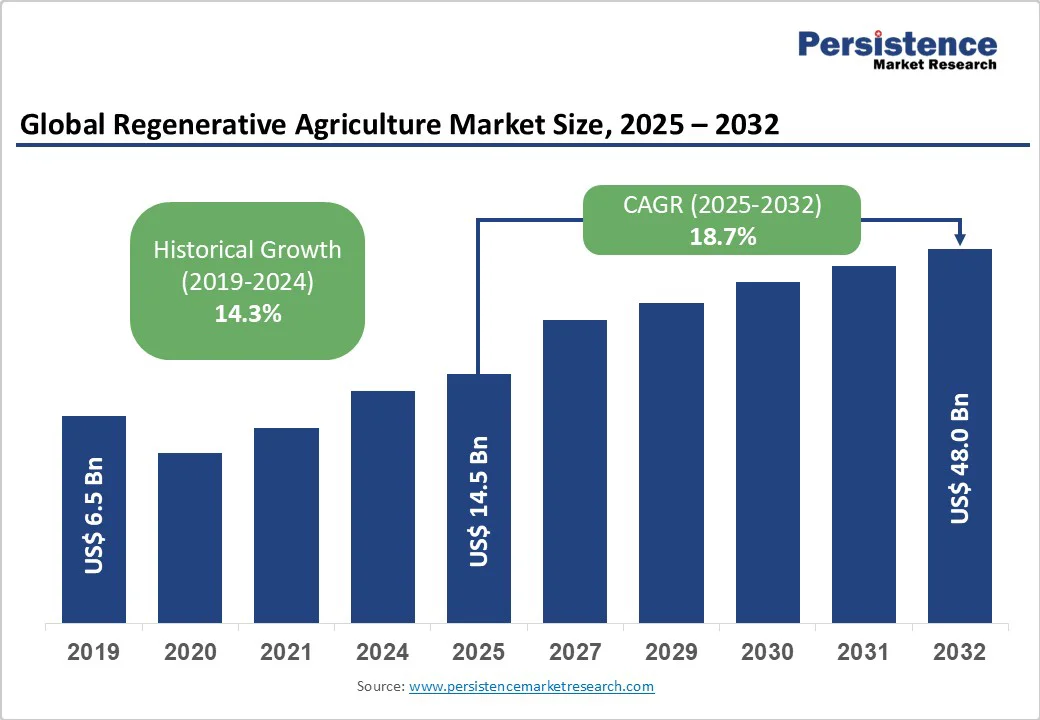

The global regenerative agriculture market is expected to reach US$14.5 billion in 2025. It is estimated to reach US$48 billion by 2032, growing at a CAGR of 18.7% during the forecast period 2025−2032, driven by increased government support, environmental awareness, and farmers' adoption of sustainable practices. Market growth is driven by digital agtech, stronger sustainability policies, and corporate commitments to regenerative sourcing, fueled by the urgent need to restore the soil, boost biodiversity, and sequester carbon for climate and food security.

Key Industry Highlights

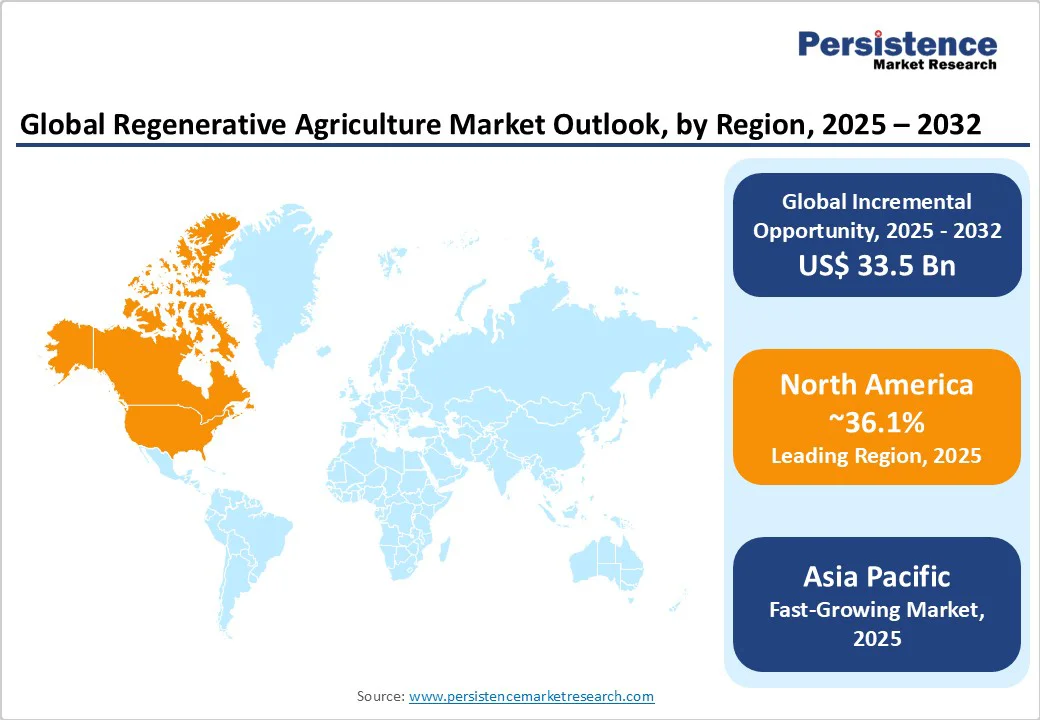

- Leading Region and Fastest-growing Regions: North America is anticipated to hold 36.1% of the market share in 2025, supported by governmental policies and innovation ecosystems, while the Asia Pacific is the fastest-growing regional market at 17.9% CAGR from 2025 to 2032.

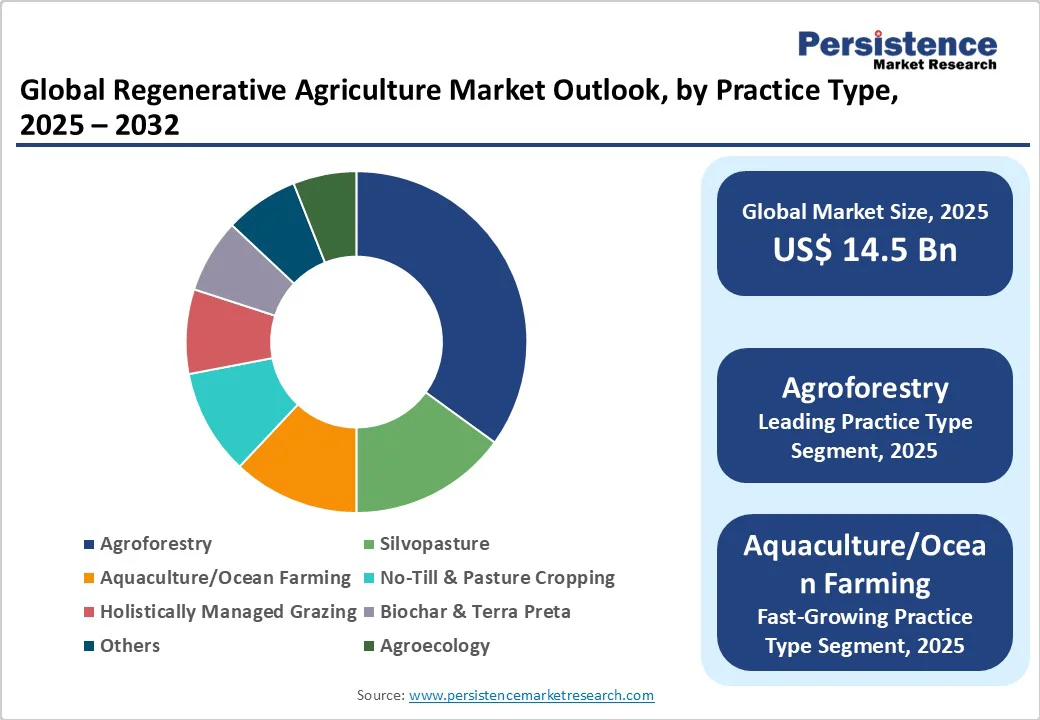

- Dominant Practice Segment: Agroforestry will lead as the largest practice segment in 2025, with a 35% share, while aquaculture/ocean farming is the fastest-growing during 2025-2032.

- Leading Application Segment: Soil & crop management is set to dominate applications, with an estimated 40% share in 2025, whereas the carbon sequestration segment is slated to grow rapidly through 2032.

- Key Strategies: Key market player strategies include technology innovation, expansion through partnerships, and monetization of ecosystem services.

- Key Development: In June 2025, a landmark EARA study of 78 regenerative farms showed they matched conventional yields, while using fewer synthetic inputs and delivering major ecological benefits.

| Key Insights | Details |

|---|---|

|

Regenerative Agriculture Market Size (2025E) |

US$14.5 Bn |

|

Market Value Forecast (2032F) |

US$48.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

18.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

14.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Government Incentives and Policy Push toward Sustainable Agriculture

Governments worldwide are intensifying their focus on sustainable agricultural transitions, notably through financial incentives and supportive policies. For example, the U.S. Department of Agriculture's programs, such as the Environmental Quality Incentives Program, provide direct financial assistance to farmers adopting regenerative practices. European Union (EU) initiatives such as the Common Agricultural Policy further incentivize agroecological approaches by subsidizing regenerative adoption. Supportive policies lower adoption barriers, boost farmer profitability, and align agriculture with climate goals. Growing public funding fuels regenerative transitions, spurring farmer adoption, private investment, and demand for regenerative solutions.

Technological Advancements in Digital Agriculture Platforms

Innovation in technology is accelerating the adoption of regenerative agriculture by enabling precision and transparency. Cutting-edge solutions in remote sensing, AI-driven soil analytics, IoT monitoring, and satellite imaging provide real-time soil health data and yield predictions. These technologies enable farmers to optimize practices such as cover cropping, no-till farming, and nutrient cycling. Crucially, they enable participation in carbon credit and sustainability certification markets through verifiable data reporting. This technological evolution reduces operational costs and environmental impacts while increasing market access for small- to medium-sized farms.

Consumer Demand Shift toward Regenerative-Sourced Products

Rising consumer consciousness regarding environmental and health impacts is shaping the demand landscape. Buyers prefer products linked to regenerative agriculture, which supports biodiversity and improves soil health. Premiumization trends are driving companies across the food, beverage, and apparel sectors to secure regenerative supply chains. Certifications such as Regenerative Organic Certified offer credible market differentiation, attracting investments from consumer packaged goods (CPG) companies, which are projected to be the second-fastest growing end-user segment. This consumer-driven demand incentivizes farmers and distributors to embrace regenerative methods and further stimulates market expansion.

Barrier Analysis - High Initial Investments and Implementation Costs

Despite promising long-term benefits, the upfront capital required for transitioning to regenerative agriculture remains a significant barrier. Farmers often face financial constraints when acquiring digital tools, altering land management practices, and retraining labor forces. The cost-to-benefit ratio varies by farm size and location, with uncertainties about immediate yield improvements generating hesitance. The complexity of aligning diverse regenerative practices with existing supply chains entails financing risks. In some regions, these initial expenditures delay adoption and limit market penetration, constraining growth rates, especially among smallholder farms and in less developed markets.

Regulatory and Certification Complexity

Regulatory frameworks and certification processes for regenerative agriculture are still evolving and lack global standardization. Variability in definitions, measurement protocols, and reporting requirements presents challenges for market actors seeking consistency. Certification programs can be resource-intensive and costly, especially for smaller farms and service providers, potentially limiting access to premium markets and carbon finance opportunities. Fragmented regulatory environments across countries complicate cross-border trade and investment in regenerative products. These uncertainties increase compliance risks, slow market maturation, and introduce competitive pressures on emerging service providers.

Opportunity Analysis - Expansion in Agriculture-dependent Economies

The economies of the Asia Pacific, Latin America, and Africa are heavily dependent on agriculture, presenting expansive opportunities due to extensive degraded soils and increasing food demand. The Asia Pacific market is forecast to grow at a CAGR of 17.9%, propelled by China's and India’s commitments to restore soil health and reduce chemical inputs. Large-scale regenerative initiatives combined with urban consumer demand for sustainable food create fertile ground for market penetration. Investments in education, technology transfer, and localized demonstration farms can unlock this potential, representing multi-billion-dollar opportunities in both input supply and service sectors.

Technological Convergence Enabling Carbon Credit Monetization

Linking regenerative agriculture with carbon markets is enabling farmers and companies to monetize ecological benefits. Digital tools capable of MRV (Measurement, Reporting, and Verification) of soil carbon and biodiversity outcomes provide the foundation for performance-based finance models. As global emissions regulations tighten, market mechanisms to reward soil carbon sequestration are expanding rapidly. This convergence drives the demand for technology-enabled solutions and expert verification services, creating a new revenue stream. Estimates suggest that carbon credit revenues in regenerative agriculture could reach several billion dollars annually by 2030, incentivizing widespread adoption and catalyzing investment in novel management practices.

Innovations in Bio-based Inputs and Agroforestry Systems

Developments in biochar, organic fertilizers, and silvopasture improve soil quality while reducing reliance on synthetic chemicals. Given the predominance of agroforestry in agricultural practices, corporate investment in regenerative sourcing from tree-crop intercropping systems is expanding rapidly. These innovative systems enhance biodiversity and climate resilience, appealing to companies with strong environmental, social, and governance (ESG) mandates. Increasing R&D and scaling of bio-based inputs support more cost-effective, ecologically integrated agriculture, strengthening both sustainability and productivity and opening lucrative revenue channels for input suppliers and technology providers.

Category-wise Analysis

Practice Type Insights

Agroforestry currently leads the practice segment with the highest market share at over 35% in 2025, driven by its utility in maintaining biodiversity and ecosystem services while supporting corporate regenerative supply commitments. It is complemented by techniques such as no-till cropping and silvopasture, which contribute significantly to soil conservation efforts. The aquaculture/ocean farming segment is the fastest-growing, with a forecast CAGR of around 21.3% through 2032, fueled by integration with blue carbon markets and growing interest in marine ecosystem restoration. These practice types are revolutionizing landscape management by combining ecological and economic benefits to create resilient agricultural systems.

Application Insights

The soil & crop management segment is set to dominate applications, accounting for roughly 40% of the regenerative agriculture market share, as these directly impact yield, carbon sequestration, and farmer profitability. Biodiversity enhancement follows closely, especially as ecosystem preservation becomes a key corporate sustainability indicator. Carbon sequestration applications have rapid growth potential, driven by regulatory pressure and the development of the carbon credit market from 2025 to 2032. Operational management services that help farmers optimize regenerative practices are also expanding swiftly due to increasing demand for performance monitoring and ecosystem service valuation.

End-user Insights

Farmers are expected to hold the largest market share of approximately 50% in 2025, motivated by cost savings from reduced input reliance and enhanced soil productivity. The CPG manufacturers segment is the fastest-growing among end users through 2032, driven by commitments to regenerative sourcing for brand differentiation and regulatory compliance. Financial institutions and advisory bodies are emerging segments providing capital and technical support for regenerative transition projects. This end-user diversity reflects a broadening ecosystem around regenerative agriculture encompassing producers, buyers, financiers, and consultants, each with distinct market roles and growth trajectories.

Regional Insights

North America Regenerative Agriculture Market Trends

North America is anticipated to command a 36.1% share of the regenerative agriculture market revenue in 2025 and is expected to retain dominance through 2032 with robust growth fueled by the U.S. agriculture industry. Government incentive programs, grassroots farmer movements, and a mature innovation ecosystem foster widespread adoption. The U.S. regulatory framework supports regenerative practices through the Department of Agriculture (DA) and state-level initiatives. Large agribusinesses driving regenerative supply chains alongside advanced digital agriculture startups strengthen the competitive landscape. Investment trends favor technology platforms and certification services, positioning North America as a global innovation hub and largest revenue contributor.

Europe Regenerative Agriculture Market Trends

Europe is likely to account for approximately 25% of the global market, with Germany, the U.K., France, and Spain as top performers. Regulatory harmonization under the EU’s Common Agricultural Policy and focus on agroecology are accelerating regenerative adoption, backed by strong research institutions and farmer cooperatives. The European Agroforestry Federation facilitates knowledge sharing across member nations, further strengthening implementation. Multi-stakeholder partnerships enhance financial and technical support to farmers. The competition includes established agri-tech companies and emerging players focused on biodiversity and soil health solutions. Investment is prioritizing certification frameworks and traceability innovations that align with ESG mandates.

Asia Pacific Regenerative Agriculture Market Trends

Asia Pacific represents the fastest-growing regional market with a CAGR of about 17.9% projected through 2032, covering China, India, Japan, and ASEAN countries. The region faces significant soil degradation challenges, with large-scale initiatives underway to restore soil fertility and reduce dependency on chemical inputs. Rapid urbanization and rising middle-class consumer awareness are creating a burgeoning demand for sustainable food products. Government policies support regenerative transitions through subsidies, education, and the deployment of technologies. Manufacturing advantages enable local production of cost-effective regenerative solutions. Competitive dynamics include domestic startups adopting digital farming tools and partnerships with global technology providers to scale regenerative systems.

Competitive Landscape

The global regenerative agriculture market landscape is moderately consolidated, with leading players collectively controlling nearly half of the market. Key companies include Cargill, Indigo Ag, Inc., Carbon Robotics, and Ecorobotix SA, which dominate through technological innovation and broad service portfolios. Market concentration is increasing as incumbents expand through mergers and acquisitions (M&A), technology partnerships, and service diversification.

Small and medium players drive niche innovations, especially in precision agriculture and verification services. Competitive positioning revolves around digital solution integration, supply chain partnerships, and certification platforms, with an emphasis on scalable, data-driven sustainability metrics.

Key Industry Developments

- In September 2025, PepsiCo, Unilever, and others launched STEP up for Agriculture, a joint initiative to boost regenerative farming by strengthening farmer-support organizations. The program offers tools, training, funding, and localized advisory services to accelerate the adoption of practices such as cover cropping and soil health improvement.

- In September 2025, ADM announced it had enrolled over 5 million acres in regenerative practices, surpassing its 2024 target and hitting its 2025 goal a year early. Its 2024 efforts cut Scope 3 emissions by over 1 million metric tons and sequestered 363,000 metric tons of CO2 equivalent in soil.

- In September 2025, the AgreenaCarbon Project issued 2.3 million Verified Carbon Units, becoming the first large-scale cropland initiative verified under Verra’s VM0042 standard. Spanning 1.6 million hectares across Europe, the project uses digital MRV to track real, traceable CO2 reductions and soil carbon sequestration from regenerative practices.

Companies Covered in Regenerative Agriculture Market

- Cargill, Incorporated

- Indigo Ag, Inc.

- Carbon Robotics

- Ecorobotix SA

- Terramera Inc.

- Agreed.Earth

- Biotrex

- Ruumi

- Continuum Ag

- Aker Technologies, Inc.

- SATELLIGENCE

- Tortuga Agricultural Technologies, Inc.

- Vayda

- Astanor Ventures

- General Mills, Inc.

Frequently Asked Questions

The regenerative agriculture market is projected to reach US$14.5 Billion in 2025.

The urgent need for soil restoration, biodiversity enhancement, and carbon sequestration to address climate change and food security challenges is driving the regenerative agriculture market.

The regenerative agriculture market is poised to witness a CAGR of 18.7% from 2025 to 2032.

The adoption of sustainable practices by farmers, advances in digital agricultural technologies, stronger policy frameworks promoting sustainability, and robust corporate commitments to regenerative sourcing are key market opportunities.

Cargill, Incorporated, Indigo Ag, Inc., and Carbon Robotics are some of the key players in the regenerative agriculture market.