- Technology

- Access Control Market

Access Control Market Size, Share, and Growth Forecast, 2026 – 2033

Access Control Market by Offering (Hardware, Software, Services), Technology (Biometric Access Control, Keypad Access Control, Host-Based Access Control, Card-Based Access Control, Wireless Access Control), End-User (Businesses & Enterprises, Financial Institutions, Hospitality & Entertainment, Retail & Customer-Facing, Government & Public Services, Residential, Education & Research, Healthcare & Life Sciences, Energy & Utility Infrastructure, Transportation & Logistics, Others), and Regional Analysis for 2026-2033

Access Control Market Share and Trends Analysis

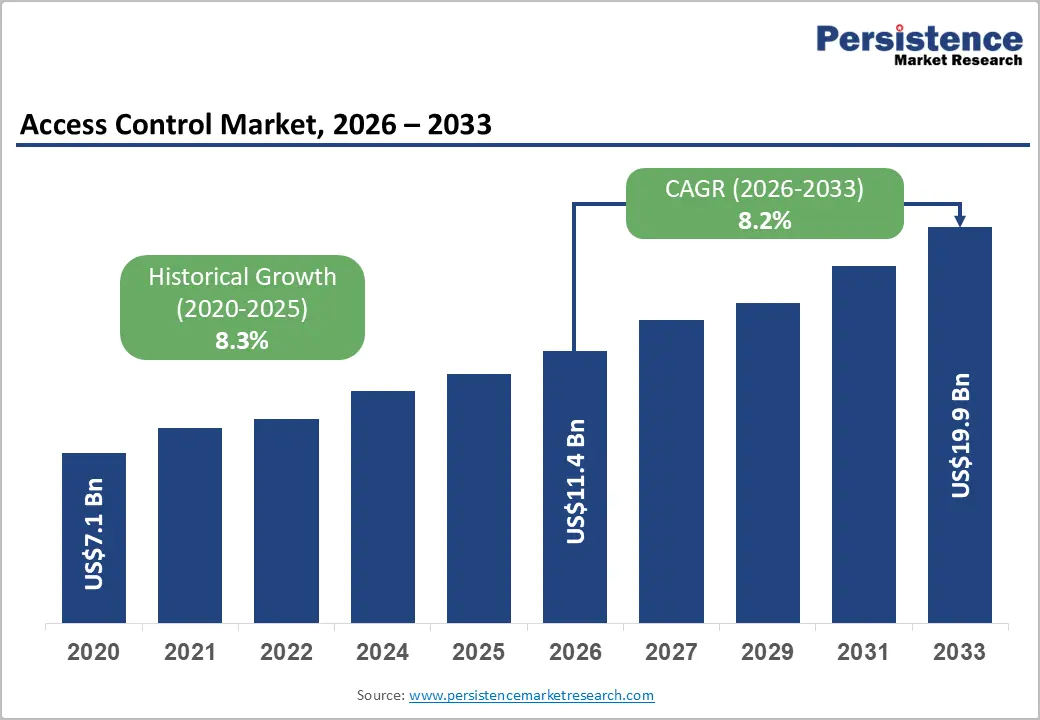

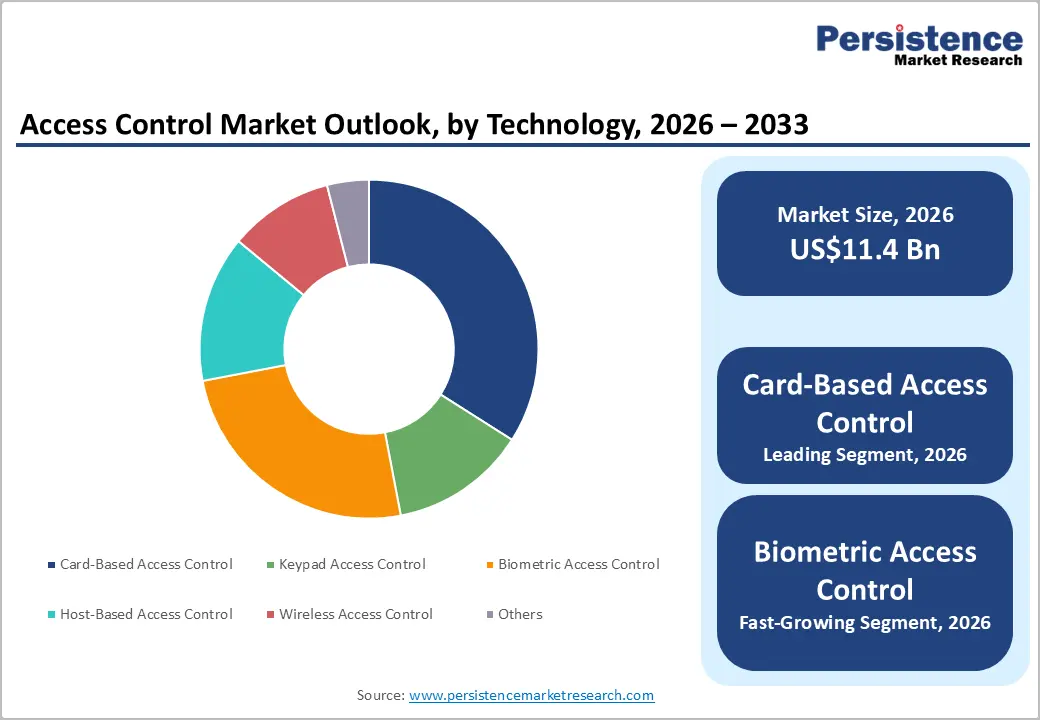

The global access control market size is likely to be valued at US$ 11.4 billion in 2026, and is projected to reach US$ 19.9 billion by 2033, growing at a CAGR of 8.3% during the forecast period 2026−2033. This market is positioned for sustained expansion as organizations across commercial, public, and residential environments prioritize structured security governance, identity verification, and controlled physical and digital entry.

Market growth is primarily driven by urban population density, increased asset digitization, and rising institutional accountability requirements, which collectively elevate demand for secure access management frameworks. Heightened awareness regarding unauthorized access risks has accelerated adoption across enterprises, public infrastructure, and critical facilities, reinforcing access control as a foundational component of security architecture. Technological integration acts as a decisive catalyst, with biometric authentication, wireless connectivity, and centralized software platforms improving system reliability and operational efficiency.

Key Industry Highlights

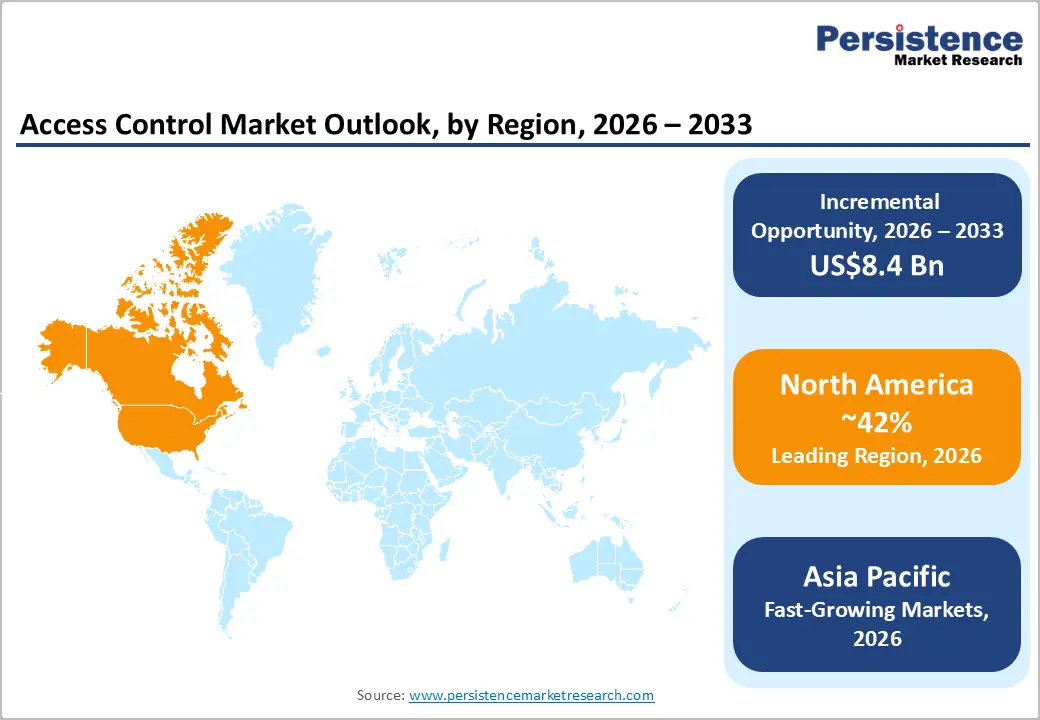

- Dominant Region: North America is projected to account for approximately 42% of the market in 2026, driven by widespread adoption of integrated, cloud-based, and hardware-centric security systems.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing market through 2033, driven by rising adoption of scalable, cloud-enabled, and AI-integrated security systems across commercial and public infrastructure.

- Leading End-User: Businesses and enterprises are expected to dominate in 2026, with a projected 34% share, driven by the growing need for efficient workforce management and asset protection solutions.

- Fastest-growing End-User: Government and public services are projected to be the fastest-growing segment through 2033, driven by infrastructure modernization and tightening public safety mandates.

- January 2026: AllKey biometric technology from Fingerprint Cards was deployed in a server rack access control solution for data centers in India, enabling biometric authentication at the individual rack level.

| Key Insights | Details |

|---|---|

| Access Control Market Size (2026E) | US$ 11.4 Bn |

| Market Value Forecast (2033F) | US$ 19.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Urbanization and Infrastructure Security Requirements

Rapid urban expansion concentrates populations, assets, and critical services into dense environments, where risk exposure increases with scale and proximity. Mixed-use developments, transit hubs, data centers, and public venues operate with continuous footfall and interdependent systems, creating demand for controlled movement, identity assurance, and real-time visibility across facilities. Vertical construction and shared infrastructure increase the number of access points per square meter, thereby increasing the need for standardized credentialing and centralized policy enforcement to sustain operational continuity. A single planning metric underscores the structural shift: the United Nations Department of Economic and Social Affairs (UNDESA) estimates that 68% of the global population will reside in urban areas by 2050, signaling sustained pressure on city systems and reinforcing investment in structured access governance to protect people, information, and assets at scale.

Security expectations for modern infrastructure align with regulatory scrutiny, service-uptime targets, and public-trust obligations. Transportation networks, utilities, healthcare campuses, and commercial complexes integrate digital platforms, automation, and remote operations, which expand attack surfaces and compliance requirements. Decision-makers prioritize solutions that integrate physical entry control with identity lifecycle management, auditability, and analytics to support risk-based decision-making and incident response. Interoperability with building management systems and cybersecurity frameworks supports resilience goals while reducing friction for authorized users. Capital allocation favors platforms that scale across portfolios, adapt to evolving threats, and support sustainability objectives through touchless authentication and energy-aware operations.

Cybersecurity Vulnerabilities in Connected Systems

Rising digitization of physical security infrastructure expands exposure to cyber threats, transforming connected authentication and monitoring systems into attractive targets for malicious actors. Network-enabled controllers, smart readers, and centralized software platforms continuously exchange sensitive credentials and operational data, increasing the likelihood of intrusion through weak endpoints or misconfigured networks. Breaches originating from poorly secured access nodes can cascade into enterprise information systems, disrupting operations and triggering regulatory investigations. Senior stakeholders view this convergence of physical and digital risks as a material business concern, thereby slowing the approval of deployments that rely heavily on connectivity and remote management features. Confidence in system resilience becomes a decisive factor, and unresolved cyber risk directly translates into postponed investments.

Complex technology ecosystems intensify this restraint. Interoperability across multiple vendors introduces uneven security standards, fragmented update cycles, and limited accountability for end-to-end protection. Many organizations lack the specialized expertise to monitor threats across hybrid physical-digital environments, increasing the risk of prolonged, undetected incidents. Liability considerations, cyber insurance premiums, and stricter internal governance reviews elevate total ownership costs and extend decision timelines. Risk committees often mandate extensive testing, network segmentation, and compliance validation before approval, redirecting focus from expansion toward risk containment.

Smart Infrastructure and Building Automation Convergence

Integration of advanced building systems with access solutions enhances operational efficiency, optimizes costs, and strengthens security. Converged platforms enable real-time coordination among heating, ventilation, & air conditioning (HVAC), lighting, surveillance, and entry control, thereby enabling dynamic responses to occupancy patterns, emergency situations, and energy management protocols. Centralized data from multiple subsystems provides actionable insights for predictive maintenance, risk mitigation, and resource allocation. The capability to manage access permissions based on contextual information, such as location, role, and time, enhances security protocols while supporting seamless user experiences across commercial, residential, and industrial environments. This convergence also reduces infrastructure redundancy, streamlines installation, and lowers long-term operational expenditures by consolidating hardware and software ecosystems into unified management frameworks.

Integration creates opportunities for advanced analytics, artificial intelligence (AI)-driven decision-making, and adaptive security measures. Systems can detect anomalies, track movement trends, and trigger automated responses, ensuring compliance with regulatory standards and organizational policies. Interoperable platforms allow scalable deployment across multi-site facilities, supporting future upgrades and technology adoption without major disruptions. Converged solutions empower stakeholders to implement flexible access strategies aligned with occupancy dynamics, business objectives, and sustainability goals.

Category-wise Analysis

Offering Insights

Hardware is poised to lead with a forecasted 46% of the access control market revenue share in 2026, owing to foundational deployment requirements across all access control installations. Physical components such as readers, controllers, locks, and biometric devices form the core of system architecture, providing the essential interface between users and secured spaces. Initial infrastructure investment prioritizes reliable hardware to ensure security integrity, minimize downtime, and support long-term operational continuity. Demand is driven by new construction projects, modernization of existing facilities, and the systematic replacement of aging mechanical locking systems. Regulatory frameworks for critical infrastructure, such as data centers, healthcare facilities, and government sites, further reinforce procurement of high-quality hardware as a non-negotiable aspect of robust security strategy.

Software is anticipated to be the fastest-growing segment between 2026 and 2033, fueled by demand for centralized management, analytics, and remote access control capabilities. Software platforms facilitate credential lifecycle management, enforce policy compliance, generate audit reports, and integrate seamlessly with enterprise resource and building management systems. Cloud-based deployment models enhance scalability, reduce reliance on on-site servers, and allow multi-location management from centralized interfaces. Increasing emphasis on data-driven security optimization, real-time monitoring, and automated threat detection is accelerating adoption. Enterprises are leveraging advanced analytics and artificial intelligence features within software solutions to improve decision-making, operational efficiency, and adaptive access strategies.

Technology Insights

Card-based access control systems are likely to be the leading segment with a projected 38% market share in 2026, due to established adoption, cost efficiency, and operational familiarity. These systems enable scalable credential issuance, management, and revocation while maintaining compatibility with existing security infrastructure. Integration with legacy hardware and software reduces installation complexity and capital expenditure, making them suitable for commercial, institutional, and industrial facilities. Standardizing protocols and simplifying staff training enhances operational efficiency. Continuous technological advancements, such as contactless and smart card technologies, further drive adoption. Widespread acceptance across enterprises ensures consistent demand and positions the segment as a core component of access management strategies.

Biometric access control systems are expected to grow the fastest between 2026 and 2033, driven by improved authentication accuracy and reduced credential misuse. Innovations in fingerprint scanning, facial recognition, iris detection, and multimodal biometric systems improve reliability and user convenience. Organizations increasingly prioritize identity assurance to prevent unauthorized access, safeguard sensitive information, and comply with regulatory requirements. Integration with mobile and cloud-based platforms expands flexibility, enabling remote enrollment and real-time monitoring. Heightened security awareness, risk mitigation strategies, and adoption in critical infrastructure, healthcare, and financial environments accelerate growth, positioning biometric systems as a future-ready solution for secure and efficient access control.

End-User Insights

Business and enterprise environments are expected to hold a dominant position, accounting for an anticipated 34% of the access control market share in 2026, driven by workforce management requirements and asset protection priorities. Corporate facilities rely on structured access governance to monitor employee movement, manage visitor entry, and maintain compliance with internal and external audit standards. Integration with enterprise resource planning systems, human resources platforms, and security operations enhances operational efficiency and reporting capabilities. Digital transformation initiatives, including smart office solutions and IoT-enabled monitoring, reinforce adoption by enabling centralized management, real-time analytics, and adaptive security measures.

Government and public services are forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by infrastructure modernization and public safety mandates. Upgrades in smart public facilities, transportation hubs, and administrative buildings drive the adoption of advanced access control systems. Regulatory compliance, citizen safety protocols, and national security requirements further encourage investment in secure, scalable solutions. Integration with surveillance, emergency response, and digital identity systems enhances operational oversight. A growing focus on technological modernization, efficient facility management, and secure public services is accelerating growth, positioning government and public services as a strategic growth segment within the access control landscape. For example, in March 2025, Indian Railways introduced access control and permanent holding areas at 60 major stations, allowing only passengers with confirmed tickets to enter the platforms as part of enhanced crowd-management measures.

Regional Insights

North America Access Control Market Trends

North America is expected to account for approximately 42% of the access control market sales in 2026, reflecting a strong preference for integrated security solutions across corporate, healthcare, and critical infrastructure facilities. Dominance is supported by substantial investment in advanced building automation systems, which enable seamless integration of entry control with surveillance, alarm management, and environmental monitoring platforms. Organizations prioritize centralized management and real-time monitoring to ensure operational continuity, reduce security gaps, and comply with strict regulatory frameworks covering data protection, facility safety, and workforce management. High adoption of cloud-based access control platforms enhances scalability, supports multi-site deployment, and reduces dependency on on-site infrastructure, reinforcing operational efficiency. Corporate and institutional facilities consistently favor hardware systems, such as controllers, readers, and biometric devices, as foundational investments for long-term security architecture. Early adoption of smart access technologies, including mobile credentials and multi-factor authentication, also contributes to sustained leadership by enabling the faster adoption of analytics-driven decision-making and predictive maintenance.

A critical factor driving dominance is the concentration of large enterprises, financial hubs, and technology centers that require sophisticated identity management and secure access governance. Adoption is influenced by demand for compliance reporting, audit readiness, and integration with enterprise resource systems, creating a preference for comprehensive software-enabled access solutions. Growth in facility modernization, retrofitting legacy systems, and upgrading high-security installations reinforces market leadership, while regulatory mandates for secure data centers, government facilities, and healthcare environments sustain long-term procurement. Investment in research, innovation, and strategic partnerships with technology vendors ensures early access to advanced biometric, AI-powered, and cloud-integrated access solutions, thereby establishing a competitive advantage in implementation, scalability, and operational resilience across diverse sectors.

Europe Access Control Market Trends

Europe is expected to maintain a significant position in the access control market, owing to high adoption of advanced building automation, regulatory rigor, and a focus on integrated security frameworks. Growth is supported by corporate offices, healthcare facilities, and government establishments investing in centralized entry management systems that provide real-time monitoring, audit trails, and compliance reporting. The increasing adoption of cloud-based solutions and mobile credentials enables enterprises to streamline operations across multi-site facilities while reducing dependence on legacy infrastructure. Sustainability initiatives and energy-efficient building designs further encourage integration of access control with lighting, HVAC, and environmental management systems, enhancing operational efficiency. Strong presence of technology vendors offering AI-enabled analytics, predictive maintenance, and behavior-based monitoring strengthens market positioning and drives adoption across both new and retrofit projects.

High regulatory standards governing data protection, workplace safety, and critical infrastructure security are a key driver of the deployment of advanced access solutions. Enterprises prioritize identity verification, multi-factor authentication, and seamless integration with enterprise resource and human resource platforms to ensure compliance and operational continuity. The modernization of legacy mechanical locking systems, coupled with the expansion of commercial, institutional, and high-security installations, is accelerating demand for interoperable access systems. Investment in research, development, and partnerships with technology innovators fosters early adoption of biometric, cloud-integrated, and intelligent access solutions. Growing awareness of the convergence of cyber-physical security and operational risk management positions Europe as a stable, technologically mature market with steady growth potential for advanced access control technologies over the coming decade.

Asia Pacific Access Control Market Trends

Asia-Pacific is projected to be the fastest-growing regional market for access control systems between 2026 and 2033, driven by rapid urbanization, large-scale industrialization, and the modernization of commercial and public infrastructure. Expanding smart city initiatives and integrated facility management programs are driving adoption of automated entry control solutions that combine hardware, software, and analytics for real-time monitoring. Organizations are prioritizing scalable and interoperable systems capable of managing multi-site operations, complex credential hierarchies, and diverse user groups. Mobile-based and cloud-enabled access platforms reduce reliance on on-premises infrastructure, accelerate deployment across new developments, and enable remote administration. Demand is further reinforced by enterprises seeking AI-driven analytics, predictive maintenance, and behavior-based monitoring to optimize operational efficiency and strengthen security frameworks.

Heightened regulatory emphasis on identity verification, workplace safety, and critical facility protection is a key driver of growth, mandating the implementation of modern access systems across government offices, healthcare centers, transportation networks, and educational institutions. The expansion of multinational corporate operations and industrial parks increases the need for centralized credential management, compliance reporting, and seamless integration with enterprise and human resource systems. Replacement of aging mechanical systems with technologically advanced solutions further accelerates adoption. Rising awareness of cyber-physical security convergence, operational optimization, and risk mitigation positions the market for sustained rapid growth, establishing a strong foundation for long-term investment and deployment of advanced access control technologies across multiple sectors.

Competitive Landscape

The global access control market structure reflects moderate fragmentation, shaped by the coexistence of multinational technology providers and a wide base of regional and niche specialists. Market structure supports competitive intensity without concentration dominance, as leading participants command meaningful cumulative share through diversified and integrated portfolios rather than single-solution leadership. Bosch Security and Safety Systems, Honeywell International Inc., Johnson Controls, Assa Abloy AB, Thales Group, and NEC Corporation anchor the competitive landscape through end-to-end offerings that combine hardware, software, analytics, and system integration capabilities. These organizations benefit from established distribution networks, strong brand credibility, and long-standing relationships with enterprise, infrastructure, and government clients.

Competitive positioning in the market emphasizes breadth of technology, compliance capability, and service scalability as core decision criteria for buyers. Leading players invest heavily in biometric authentication, mobile credentialing, cloud-based access management, and artificial intelligence-enabled monitoring to address complex security environments. Service scalability supports large, multi-site deployments, particularly in smart buildings, transportation hubs, and critical infrastructure, where centralized control and real-time visibility are operational priorities. Compliance capability remains a decisive factor, as access control solutions must align with data protection, identity governance, and safety standards across multiple jurisdictions. While global leaders set technology benchmarks, regional specialists remain competitive through cost efficiency, localized customization, and faster implementation cycles.

Key Industry Developments

- In January 2026, Indra Group was awarded a major long-term contract by Transport for London (TfL) to operate, maintain, develop, and expand the ticketing and access control systems across London’s entire public transportation network through 2034. The scope includes the management of fare gates, ticket vending machines, validators, retail sales terminals, back-office systems, and cybersecurity across buses, metros, trams, and ferries.

- In November 2025, Amazon Web Services (AWS) introduced attribute-based access control (ABAC) for Amazon S3 general-purpose buckets, allowing organizations to use tags to automatically manage and simplify permissions for users, roles, and resources at scale.

- In September 2025, Accenture acquired Canadian identity and access management firm IAMConcepts to strengthen its cybersecurity services and expand advanced IAM solutions across key critical infrastructure industries in Canada.

Companies Covered in Access Control Market

- Bosch Security and Safety Systems

- Honeywell International Inc.

- Johnson Controls

- Assa Abloy AB

- Thales Group

- NEC Corporation

- Dormakaba Holding AG

- HID Global

- Identiv

- 3M

- STANLEY Convergent Security Solutions, Inc.

- Secom Co., Ltd.

- Paxton Access Ltd.

- Matrix Comsec Pvt. Ltd.

- ZKTeco India

- BioEnable Technologies Pvt Ltd.

- Spectra Technovision (India) Pvt. Ltd.

- Intellicon Private

Frequently Asked Questions

The global access control market is projected to reach US$ 11.4 billion in 2026.

Mounting asset and workforce security concerns, rapid digital transformation, increasing smart infrastructure adoption, and stricter regulatory compliance requirements across commercial, industrial, and public sectors are factors driving this market.

The market is poised to witness a CAGR of 8.3% from 2026 to 2033.

Key market opportunities include expansion of cloud-based and mobile access solutions, growing adoption of biometric authentication, integration with smart buildings and Internet of Things (IoT) systems, and rising demand from critical infrastructure and data centre security projects.

Some of the key market players include Bosch Security and Safety Systems, Honeywell International Inc., Johnson Controls, Assa Abloy AB, and Thales Group.