- Retail

- Pet Accessories Market

Pet Accessories Market Size, Share, and Growth Forecast 2026 - 2033

Pet Accessories Market by Product Type (Collars, Leashes & Harnesses, Pet Clothing, Bedding & Furniture, Feeding Accessories, Toys & Chew Products, Grooming Accessories, Travel Accessories), Pet Type (Dogs, Cats, Others), Distribution Channel (Pet Specialty Stores, Supermarkets/Hypermarkets, Online Retail, Veterinary Clinics), and Regional Analysis, 2026 - 2033

Pet Accessories Market Size and Trend Analysis

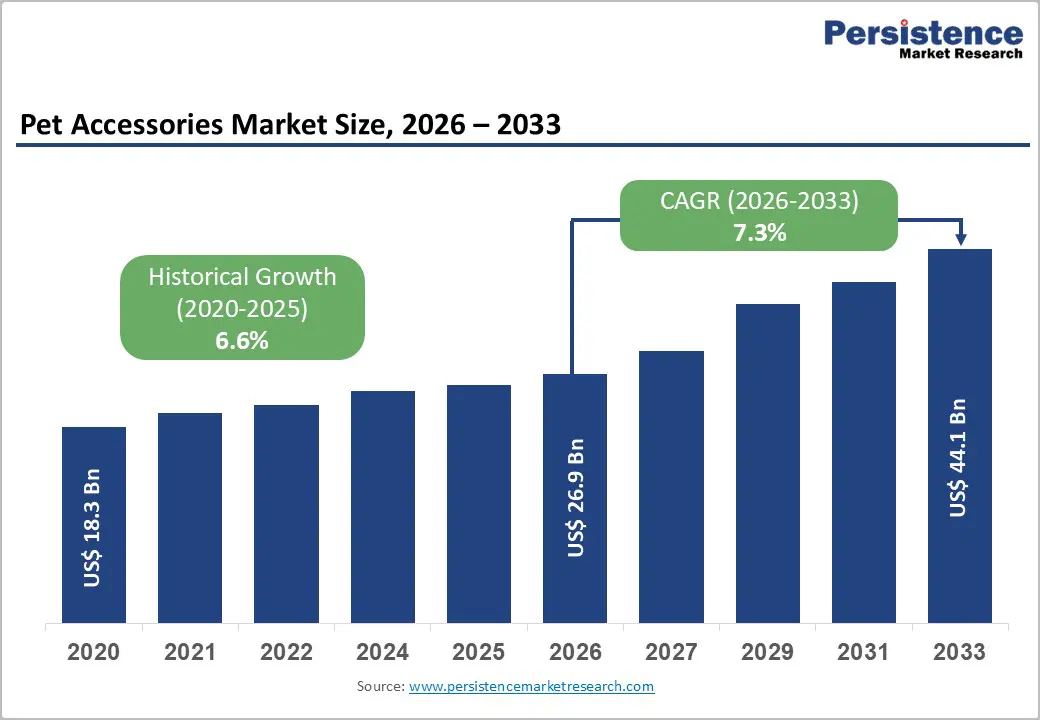

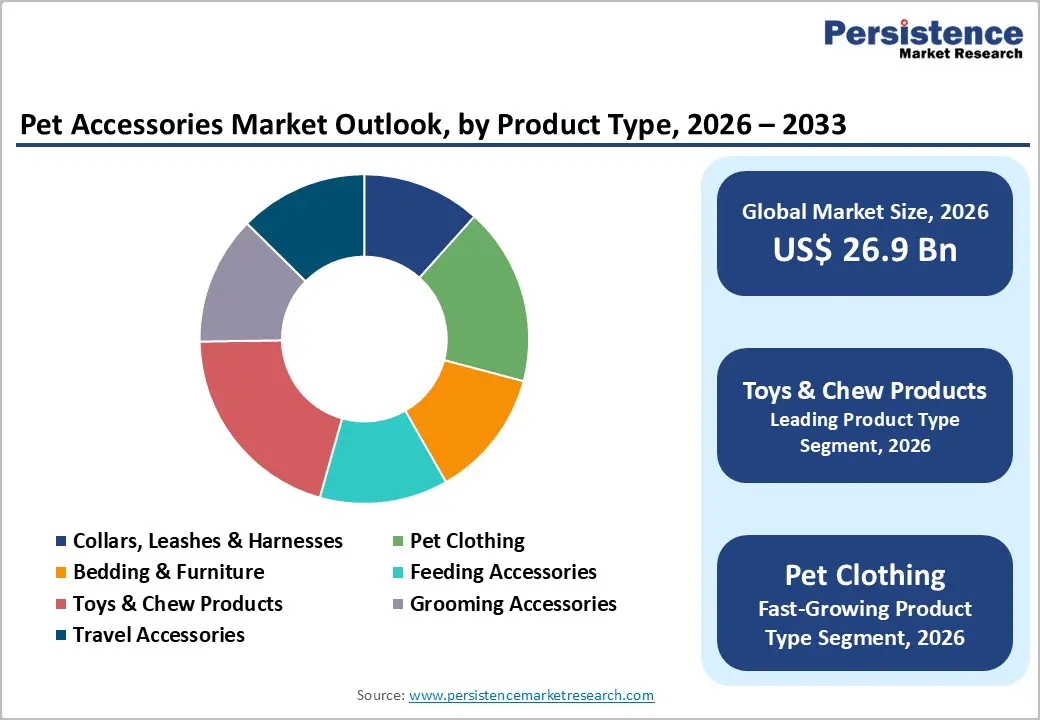

The global pet accessories market is expected to be valued at US$ 26.9 billion in 2026 and is projected to reach US$ 44.1 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

Rising pet ownership in urbanising economies across Asia Pacific and Latin America is generating first-time accessory demand at scale, while pet humanisation is pushing average transaction values higher as owners allocate discretionary spending toward enrichment, comfort, and wellness products.

Key Industry Highlights:

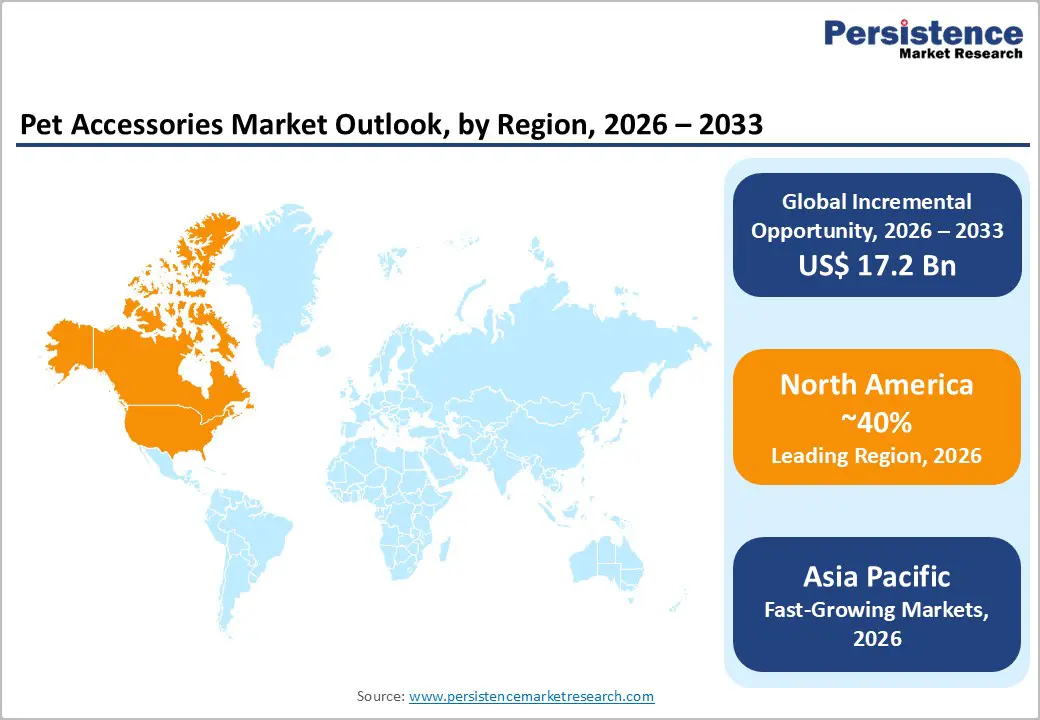

- Leading Region: North America leads the Pet Accessories market with approximately 40% of global revenue in 2026, supported by high pet ownership rates and mature specialty retail infrastructure driving premium adoption.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market through 2033, catalysed by rapid urbanisation, rising disposable incomes, and surging first-time pet adoption across China, South Korea, and India.

- Dominant Category: Toys & Chew Products dominate the product segmentation with 31.0% share in 2026, supported by enrichment-driven pet care norms, high purchase frequency, and AVMA-endorsed behavioural benefits.

- Fastest Growing Category: Pet Clothing is the fastest-growing segment, accelerating above market CAGR through social media virality, influencer pet fashion culture, and normalised seasonal pet dressing among urban millennial consumers.

- Key Market Opportunity: Convergence of IoT technology and sustainability presents the most strategic opportunity through 2033, positioning brands offering connected wellness products and certified eco-friendly materials to capture premium pricing.

Market Dynamics

Drivers - Humanisation of Pets and Premiumisation of Pet Care Spending

Pet humanisation represents the single most powerful demand-side force reshaping the Pet Accessories market today. Owners across North America, Europe, and increasingly East Asia now treat companion animals as family members, which structurally elevates willingness to pay for premium, functional, and aesthetically differentiated accessories. According to the American Pet Products Association (APPA), more than 66% of U.S. households owned a pet as of 2024.

Average annual spending per pet-owning household has risen consistently year over year, with APPA reporting U.S. pet industry expenditure exceeding US$ 147 Billion in 2023. This behavioural shift benefits every category within the pet accessories space from ergonomic feeding stations and orthopedic bedding to fashion-forward pet clothing, and it raises the category's baseline growth floor.

Rising Global Pet Ownership and Urban Pet Population Growth

Sustained, multi-decade increases in global pet ownership, amplified by urbanisation and changing household demographics, are driving accessory demand at a macro level. Younger consumers particularly millennials and Generation Z are adopting pets at higher rates than previous generations, demonstrating stronger brand loyalty and higher online purchase frequency. Regulatory frameworks including European Union animal welfare directives and the updated U.S. Animal Welfare Act guidelines have normalised higher standards of pet care.

In China, the urban pet population surpassed 100 million pets per the China Pet Industry Association, opening a substantial incremental addressable market for international and domestic brands. FEDIAF reports approximately 340 million pets across European households. This expanding ownership base creates compounding growth in recurring accessory categories such as toys, grooming tools, and feeding accessories.

Restraints - High Product Fragmentation and Price Sensitivity in Emerging Markets

The pet accessories market faces price-sensitiveness in emerging markets where unbranded and counterfeit products undercut established players on cost. Consumers in Southeast Asia, Latin America, and Sub-Saharan Africa while growing in number demonstrate significantly lower average spend per pet compared to counterparts in North America or Western Europe, compressing margins for premium-positioned brands and complicating tiered pricing strategies.

The proliferation of low-cost manufacturers, particularly through cross-border e-commerce platforms, intensifies this pressure. The U.S. Consumer Product Safety Commission (CPSC) issued multiple recalls between 2022 and 2024 on counterfeit pet collars and chew toys due to safety hazards.

Supply Chain Complexity and Raw Material Cost Volatility

The pet accessories industry relies on a diverse range of raw materials including synthetic polymers, natural rubber, nylon, cotton, and electronic components for smart accessories, making supply chains inherently complex and susceptible to commodity price swings. Disruptions to global freight logistics during 2021-2023 exposed the vulnerability of manufacturers dependent on single-source suppliers in China and Southeast Asia.

Rising input costs for petroleum-derived materials, as tracked by the World Bank Commodity Markets Outlook, directly affect the profitability of high-volume categories such as leashes, harnesses, and plastic feeding accessories. Brands that have not diversified their supplier base or invested in nearshoring strategies face structurally higher cost-of-goods exposure through the forecast period.

Opportunities - Smart and Connected Pet Accessories Leveraging IoT Technology

The integration of Internet of Things (IoT) technology into pet accessories represents one of the most commercially significant growth frontiers between 2026 and 2033. Products such as GPS-enabled collars, health-monitoring harnesses, automated feeding systems, and activity-tracking devices are moving from niche to mainstream as smartphone penetration deepens globally. The International Telecommunication Union (ITU) reports that global IoT-connected devices surpassed 15 Billion in 2024.

Brands should prioritise investment in proprietary software ecosystems that complement hardware products, since recurring subscription revenue can substantially improve customer lifetime value. Strategic partnerships with veterinary telehealth platforms can further monetise device data, positioning accessory brands as integrated pet wellness providers. Companies establishing early platform lock-in through proprietary apps and ecosystem partnerships will capture the premium tier of this opportunity.

Sustainable and Eco-Friendly Pet Accessories for the Environmentally Conscious Consumer

Consumer demand for sustainable products is accelerating across the pet accessories space, creating a structural opportunity for brands that credibly embed environmental responsibility into their supply chains and product lines. Millennial and Gen Z pet owners now collectively the dominant purchasing cohort, assigning measurable purchasing weight to sustainability credentials, with surveys indicating over 70% prefer eco-conscious pet brands when comparable alternatives exist.

Accessories manufactured from recycled materials, organic cotton, plant-based dyes, or biodegradable composites command pricing premiums and generate stronger brand advocacy. Mid-size and emerging brands should pursue third-party certifications such as Global Organic Textile Standard (GOTS) or B Corp designation to substantiate sustainability claims, aligning with the European Green Deal and evolving regulatory expectations around product environmental disclosure.

Category-wise Analysis

Product Type Insights

The Toys & Chew Products segment accounts for 31.0% of the global Pet Accessories market in 2026, equivalent to approximately US$ 8.34 Billion, making it the dominant product category by a significant margin. This leadership reflects direct alignment with pet humanisation, as owners increasingly regard mental stimulation and physical enrichment as non-negotiable components of responsible pet care, driving consistent repeat purchasing supported by veterinary endorsement from the American Veterinary Medical Association (AVMA).

The fastest-growing segment within the pet accessories framework is Pet Clothing, accelerating on the back of social media culture, influencer-led pet fashion communities, and the normalisation of dressing pets for seasonal and celebratory occasions, particularly among urban millennial owners. Industry participants should monitor this segment closely, as its growth velocity signals a broader premiumisation of lifestyle accessories that could shift category investment priorities among major brands before 2030.

Pet Type Insights

The Dogs segment accounts for 61.0% of the global Pet Accessories market in 2026, equivalent to approximately US$ 16.41 Billion, reflecting the species' longstanding position as the world's most accessorised companion animal. Dogs require a broader and more frequently replenished set of accessories including leashes, collars, harnesses, training aids, and outdoor gear which structurally inflates per-animal accessory spending two to three times higher than feline counterparts across most geographies.

The Cats segment represents the fastest-growing pet type within the Pet Accessories market, driven by rising cat ownership in urban apartments across East Asia and Western Europe, where space constraints favour cats over dogs. Feline-specific product innovation including puzzle feeders, interactive laser toys, and multi-tier cat furniture is elevating per-cat spending. Industry participants should build dedicated cat product lines rather than treating feline accessories as secondary derivations of canine counterparts.

Distribution Channel Insights

Pet Specialty Stores account for 34.0% of the global Pet Accessories market in 2026, equivalent to approximately US$ 9.15 Billion, maintaining leadership through the expertise-driven purchasing environment they provide to health-conscious and premium-oriented pet owners. The channel's dominance is structural specialty store staff deliver product education, personalised recommendations, and cross-category bundling, while chains such as PetSmart and Petco have invested in in-store veterinary services that deepen consumer engagement and basket sizes.

Online retail is the fast-growing distribution channel across the pet accessories competitive landscape, powered by subscription-based repeat purchasing, algorithm-driven discovery, and the global reach of platforms including Amazon, Chewy, and regional marketplaces across Southeast Asia and China. Industry participants should pursue omnichannel strategies that treat digital and physical touchpoints as complementary, leveraging specialty store relationships for product launches while using online channels to capture recurring consumable and replacement accessory revenue.

Regional Insights

North America Pet Accessories Market Trends and Insights

North America dominates the global market with a 40% share in 2025, anchored by high pet ownership penetration, premium product preference, and a mature retail ecosystem. The region has witnessed strong demand for smart collars, orthopedic bedding, and luxury apparel, with the APPA noting record industry expenditure. Sustainability claims, veterinarian endorsements, and subscription-based pet retail are key trends shaping the regional landscape.

U.S. Pet Accessories Market Size

The United States represents nearly 85% of North America's pet accessories market, supported by approximately 86.9 million pet-owning households per APPA 2024 data. High discretionary spending, presence of leading brands such as PetSmart, Chewy, and Petco, and strong demand for premium and smart accessories drive growth. Increasing dog adoption and humanization trends further reinforce the U.S. market leadership.

Europe Pet Accessories Market Trends and Insights

Europe holds the second-largest position, driven by stringent pet welfare regulations, high cat ownership, and rising demand for sustainable accessories. Per FEDIAF, around 340 million pets reside in European households. Countries such as Germany, France, and the U.K. lead premiumization, while eco-friendly product launches under the European Green Deal framework are reshaping consumer purchasing decisions across the region.

Germany Pet Accessories Market Size

Germany holds approximately 22% share of the European market, supported by 34.4 million pets reported by the Zentralverband Zoologischer Fachbetriebe Deutschlands (ZZF) in 2023. High disposable incomes, strong pet specialty retail networks like Fressnapf, and rising demand for ergonomic and sustainable accessories continue to drive growth. Cat-related accessories represent a notable share, given Germany's large feline population.

U.K. Pet Accessories Market Size

The United Kingdom accounts for an estimated 18% of the European market. According to the Pet Food Manufacturers' Association (PFMA), around 38 million pets live in U.K. households as of 2024. Strong e-commerce penetration via Pets at Home and Amazon UK, premium grooming accessory demand, and growing dog-walking culture in urban centers contribute substantially to market expansion in the country.

France Pet Accessories Market Size

France captures approximately 15% of Europe's pet accessories market. FACCO estimates around 77 million pets in France, with cats outnumbering dogs. Demand is driven by premium feeding accessories, designer pet clothing, and travel gear suitable for France's pet-friendly transit policies. Retail chains such as Maxi Zoo and Truffaut play pivotal roles in driving accessory sales nationally.

Asia Pacific Pet Accessories Market Trends and Insights

Asia Pacific is the fastest-growing region for pet accessories, propelled by rapid pet humanization in China, Japan, and Southeast Asia. China alone hosts over 120 million pet dogs and cats per the China Pet Industry Association, generating massive accessory demand. Urbanization, rising middle-class income, and booming e-commerce platforms like JD.com and Tmall are accelerating premium pet accessory adoption across the region.

India Pet Accessories Market Size

India's pet accessories market is among the fastest-expanding in Asia Pacific, with around 32 million pet dogs as estimated by the State of Pet Homelessness Index 2023. Growing nuclear families, urban apartment living, and rising disposable incomes are fueling demand. Domestic retailers like Heads Up For Tails and Supertails, combined with international entrants, are accelerating accessory category penetration nationwide.

Japan Pet Accessories Market Size

Japan accounts for approximately 18% of the Asia Pacific market. According to the Japan Pet Food Association, around 15.9 million dogs and cats reside in Japanese households as of 2023. Aging demographics and small-breed dog preferences drive demand for compact carriers, designer apparel, and orthopedic bedding. Premium brands and Rakuten's strong pet category footprint contribute to consistent market growth.

Southeast Asia Pet Accessories Market Size

Southeast Asia represents an emerging high-growth pocket, with Thailand, Indonesia, and Vietnam leading adoption. Rising urban pet ownership, expanding modern retail, and platforms like Shopee and Lazada are reshaping accessory distribution. The region's pet population has grown notably post-pandemic, with Thailand reporting over 10 million companion animals, supporting sustained demand for collars, leashes, and grooming accessories.

Competitive Landscape

The global Pet Accessories market exhibits a moderately fragmented competitive structure, with a tier of large, diversified players share alongside hundreds of specialist and regional brands competing on product niche, design innovation, or price. Scale advantages accrue primarily in manufacturing, logistics, and retail shelf space, giving established players such as Mars Petcare, Spectrum Brands, and Central Garden & Pet structural cost and distribution advantages. Differentiation, however, remains the more decisive battleground particularly in premium, smart technology, and sustainable sub-categories where brand storytelling and product innovation outweigh distribution reach.

The dominant strategic themes shaping the pet accessories competitive landscape include portfolio diversification into adjacencies, digital-first brand building, sustainability-led repositioning, and acquisition of high-growth niche brands to access underserved consumer segments. Emerging business model shifts particularly DTC (direct-to-consumer) subscription models and IoT-enabled hardware-software hybrids are beginning to disrupt the traditional wholesale-to-retail value chain, rewarding agile brands with recurring revenue potential.

Key Developments:

- In January 2025, Radio Systems Corporation expanded its PetSafe brand portfolio by launching a new line of GPS-enabled smart collars with real-time health monitoring capabilities, targeting premium dog owners in North America and Western Europe seeking integrated wellness management solutions.

- In March 2024, Ruffwear introduced a certified sustainable outdoor gear collection manufactured from 100% recycled ocean plastics, marking the brand's most significant product sustainability milestone and responding directly to growing consumer demand for eco-conscious pet accessories across the outdoor lifestyle segment.

- In October 2024, Spectrum Brands completed a strategic restructuring of its pet accessories division, consolidating product lines under fewer, higher-equity brand identities to improve retail shelf productivity and strengthen its competitive positioning against direct-to-consumer challenger brands gaining share online.

Pet Accessories Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 18.33 Billion |

| Current Market Value (2026) | US$ 26.90 Billion |

| Projected Market Value (2033) | US$ 44.05 Billion |

| CAGR (2026 - 2033) | 7.3% |

| Leading Region | North America (40%) |

| Dominant Product Type | Toys & Chew Products (31.0%) |

| Top-ranking Pet Type | Dogs (61.0%) |

| Top-ranking Distribution Channel | Pet Specialty Stores (34.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 17.15 Billion |

Companies Covered in Pet Accessories Market

- Mars Petcare

- Nestlé Purina PetCare

- Spectrum Brands

- Petmate

- Central Garden & Pet

- Radio Systems Corporation

- Ferplast

- Hagen Group

- Ancol Pet Products

- Ruffwear

- Coastal Pet Products

- PetSafe

- KONG Company

- Hartz Mountain

- Zolux

- Kurgo

- Flexi (Flexi-Bogdahn International)

- Chuckit! (Petmate)

- Trixie Pet Products

- Hunter International

Frequently Asked Questions

The global Pet Accessories market is valued at US$ 26.9 Billion in 2026 and projected to reach US$ 44.1 Billion by 2033, expanding at a 7.3% CAGR driven by pet humanisation and rising ownership.

The primary drivers are pet humanisation and rising global pet ownership, with APPA reporting 66%+ of U.S. households owning pets, alongside EU animal welfare directives elevating baseline pet care standards.

Toys & Chew Products lead with 31.0% share in 2026, equivalent to US$ 8.34 Billion, driven by enrichment-aligned purchasing norms, high replacement frequency, and active endorsement from veterinary professionals.

North America dominates with approximately 40% of global revenue in 2026, supported by high pet ownership density, mature specialty retail, and strong brand ecosystems anchored by PetSmart, Petco, and Chewy.

The biggest opportunity lies at the intersection of IoT-enabled smart accessories and sustainable product design, enabling early movers to command premium pricing, build subscription revenue, and differentiate from commodity competitors.

The leading companies in the Pet Accessories market include Mars Petcare, Nestlé Purina PetCare, Spectrum Brands, Central Garden & Pet, Radio Systems Corporation, KONG Company, Ruffwear, Petmate, Hagen Group, and Ferplast, among others.