- Retail

- Smoking Accessories Market

Smoking Accessories Market Size, Share, and Growth Forecast 2026 - 2033

Smoking Accessories Market by Product Type (Grinder, Water Pipes, Rolling Papers & Cigarette Tubes, Vaporizers, Lighters, Other), Distribution Channel (Online, Offline), and Regional Analysis for 2026 - 2033

Smoking Accessories Market Size and Trend Analysis

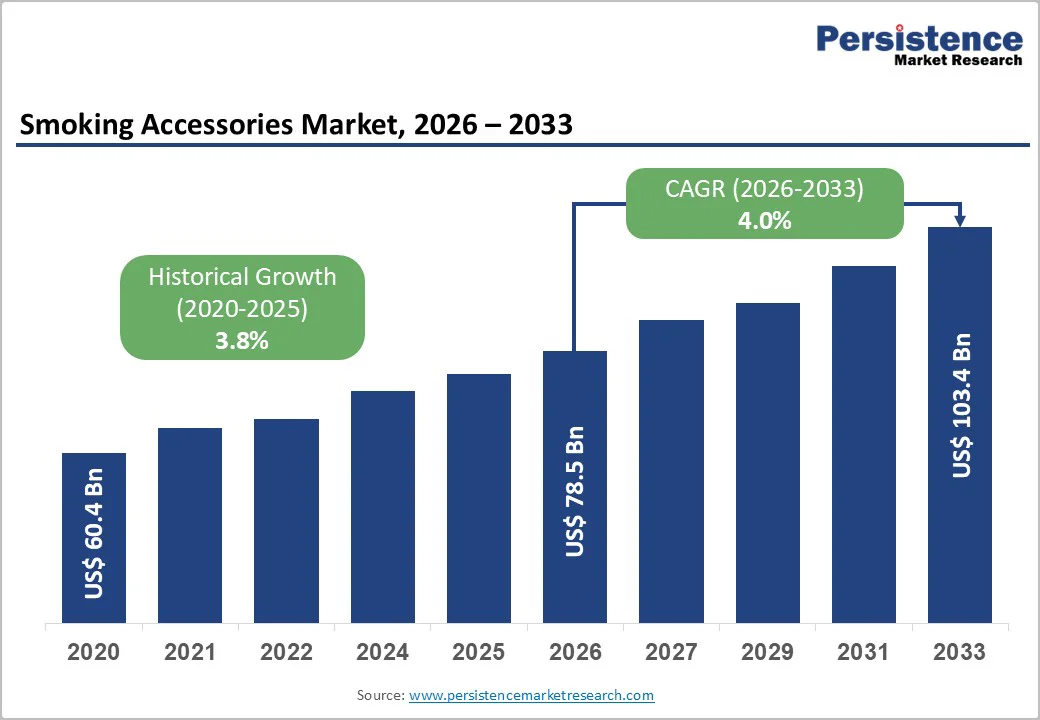

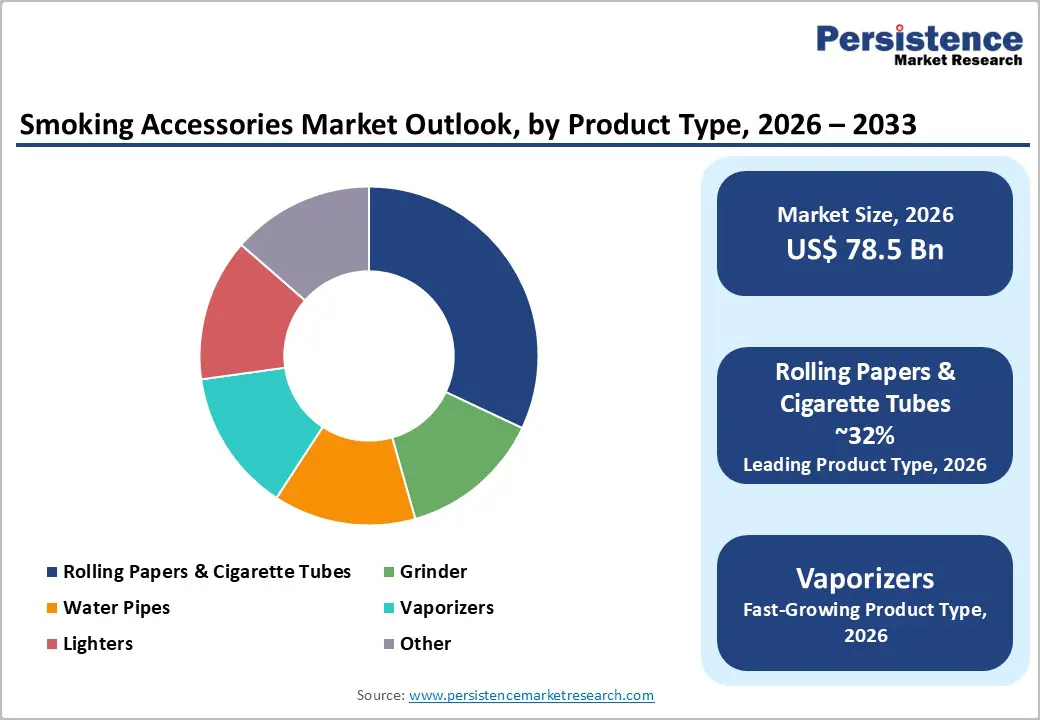

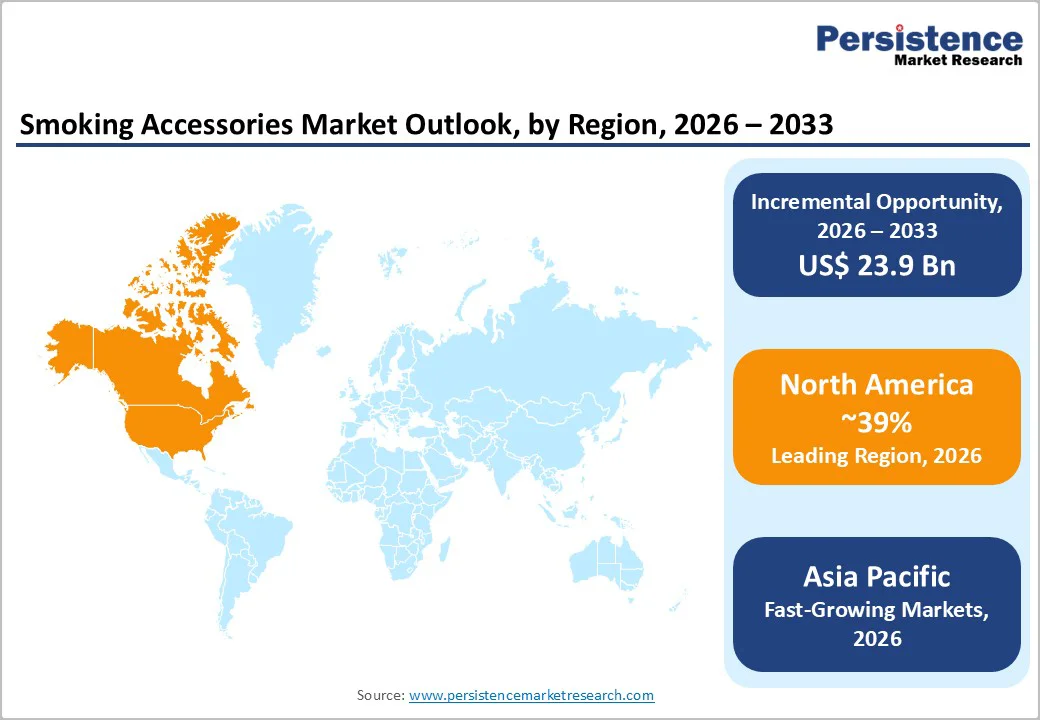

The global smoking accessories market size is likely to be valued at US$78.5 billion in 2026 and is projected to reach US$103.4 billion by 2033, growing at a CAGR of 4.0% between 2026 and 2033.

Rising cannabis legalization worldwide boosts demand for paraphernalia like grinders and vaporizers, alongside sustained tobacco use in emerging markets. The global rise of alternative smoking methods, particularly vaporizers and water pipes, reflects consumers' perception of these products as healthier alternatives to traditional cigarettes.

Key Industry Highlights:

- Regional Leader: North America dominates the global smoking accessories market, with 39% of the market, driven by progressive cannabis legalization across multiple states in the U.S.

- Fastest Growing Region: Asia Pacific fastest growth trajectory positioned to represent the highest CAGR throughout the forecast period, fueled by rising disposable incomes in emerging economies.

- Leading Segment: Rolling Papers & Cigarette Tubes command approximately 32% market share as the dominant product segment, benefiting from universal application across tobacco and cannabis consumption.

- Fastest Growing Segment: Vaporizers represent the fastest-growing product segment, driven by consumer perception of reduced health risks, technological innovations, including temperature control and smartphone connectivity.

- Growth Opportunities: E-commerce channel expansion and sustainable product innovation present the most significant market opportunities, with biodegradable rolling papers, digital distribution platforms, and next-generation vaporizer technology creating substantial revenue potential for forward-thinking manufacturers.

| Key Insights | Details |

|---|---|

| Smoking Accessories Market Size (2026E) | US$78.5 Bn |

| Market Value Forecast (2033F) | US$103.4 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.0% |

| Historical Market Growth (2020 - 2025) | 3.8% |

Market Dynamics

Drivers - Expanding Cannabis Legalization and Regulatory Liberalization

The progressive legalization of cannabis for medical and recreational use across 38 U.S. states, Canada, and select European nations stands as the primary catalyst propelling the smoking accessories market expansion. This regulatory shift has fundamentally transformed market dynamics by creating legitimate retail channels and encouraging substantial product innovation specifically tailored to cannabis consumption.

The National Cannabis Industry Association estimates that legal cannabis sales in the U.S. could reach USD 45 billion by 2025, substantially benefiting the smoking accessories market through increased consumer adoption and retail availability. This shift normalizes accessory purchases, fostering market expansion through diversified consumption methods. The E-Cigarette Market evolution demonstrates a similar regulatory impact, where product acceptance increased significantly following clearer regulatory frameworks. Premium variants gain traction among millennials, enhancing overall category growth.

Rising Consumer Preference for Premium and Sustainable Products

Consumer preferences are shifting dramatically toward premium, customized, and environmentally sustainable smoking accessories, driving market premiumization and innovation. The growing awareness of environmental sustainability has propelled demand for biodegradable rolling papers made from hemp, rice, and organic materials, with manufacturers increasingly adopting recyclable packaging and sustainable production practices.

E-commerce enables customization, with platforms reporting higher growth rates for premium segments. The aesthetic appeal and personalization of smoking accessories have become critical purchasing factors, with consumers willing to pay premium prices for artisanal designs and tech-integrated products. The Tobacco Packaging Market has similarly experienced premiumization trends, with consumers demanding sophisticated packaging that reflects product quality. This trend is particularly pronounced among millennial and Generation Z consumers who prioritize brand identity, sustainability credentials, and social media-worthy product aesthetics

Restraints - Stringent Regulatory Frameworks and Advertising Restrictions

The smoking accessories market faces significant challenges from increasingly stringent regulatory frameworks governing tobacco and cannabis products worldwide. The World Health Organization Framework Convention on Tobacco Control (WHO FCTC), adopted by 183 countries, imposes comprehensive restrictions on tobacco product marketing, packaging, and sales, indirectly impacting smoking accessories distribution.

The U.S. Food and Drug Administration (FDA) regulations mandate strict compliance for tobacco-related products, including disclosure of constituents and emissions, creating compliance burdens for manufacturers and retailers. These measures reduce visibility and sales, particularly offline. These regulatory constraints increase operational costs, restrict marketing innovations, and create market entry barriers, particularly for small and medium enterprises lacking resources for comprehensive regulatory compliance.

Rising Health Awareness Campaigns

Global public health initiatives and anti-smoking campaigns pose considerable challenges to the smoking accessories market by reducing overall smoking prevalence and changing consumer perceptions. The WHO reports that approximately 80% of the world's 1.3 billion tobacco users reside in low- and middle-income countries, where public health interventions are intensifying.

The Smoking Cessation and Nicotine De-Addiction Products Market has witnessed substantial growth as governments worldwide implement comprehensive smoke-free laws, with 79 countries protecting over one-third of the global population through such regulations. Educational campaigns highlighting smoking-related health risks have successfully reduced smoking rates in developed markets, directly impacting demand for traditional smoking accessories. This shifts consumers toward cessation products, pressuring traditional accessory demand despite cannabis offset.

Opportunity - Rapid Expansion of Vaporizer Technology and Next-Generation Devices

The vaporizer segment represents the most promising growth opportunity within the smoking accessories market, driven by technological innovation and consumer perception of reduced health risks compared to traditional combustion methods. E-cigarette batteries and advanced vaporization technology have experienced surging demand, with the emergence of high-wattage mods, precision temperature control features, and customizable vaping experiences attracting technology-savvy consumers.

The vaporizer segment benefits from the health-conscious trend, as consumers increasingly view vaporization as a cleaner alternative that eliminates many combustion byproducts associated with traditional smoking. Market participants can capitalize on this opportunity by investing in research and development for next-generation vaporizers incorporating artificial intelligence for personalized usage patterns, smartphone connectivity for usage tracking, and enhanced battery technologies for extended performance.

Penetration of Emerging Markets Through E-Commerce and Digital Distribution

The rapid digitalization of retail channels presents substantial expansion opportunities for smoking accessories manufacturers, particularly in geographically dispersed and underserved markets across the Asia Pacific, Latin America, and Africa. E-commerce platforms have fundamentally transformed product accessibility, enabling consumers in regions with limited brick-and-mortar specialty stores to access diverse product ranges and international brands.

Companies can leverage social media marketing, influencer partnerships, and targeted digital advertising to build brand awareness and drive online sales, particularly among younger demographics who demonstrate high digital engagement. Furthermore, the online channel facilitates direct-to-consumer business models, enabling manufacturers to capture higher margins while gathering valuable consumer data for product development and personalized marketing strategies, creating competitive advantages in increasingly crowded market segments.

Category-wise Analysis

Product Type Insights

Rolling papers & cigarette tubes dominate the product type category, commanding approximately 32% of the global smoking accessories market share, reflecting their fundamental role as the most frequently purchased consumable accessory. The segment's leadership position stems from multiple factors, including affordability, universal compatibility across tobacco and cannabis applications, and continuous repurchase patterns driven by product consumability. Consumer preferences within this segment are evolving toward premium slow-burning papers, organic and unbleached materials, and ultra-thin formats typically under 10 gsm, reflecting quality consciousness among discerning users.

Innovation in watermarking techniques, refined gum applications, and precision die-cutting has elevated product differentiation beyond basic functionality. The segment benefits from strong brand loyalty, particularly for heritage brands that have established trust through consistent quality, while newer entrants emphasize sustainability credentials through hemp-based and biodegradable formulations that appeal to environmentally conscious consumers.

Distribution Channel Analysis

The offline distribution channel maintains a dominant market position, accounting for approximately 76% of smoking accessories revenue, driven by the tangible nature of purchasing decisions and the importance of physical product evaluation before purchase. Traditional retail formats, including tobacco shops, convenience stores, and specialized cannabis dispensaries, provide essential consumer touchpoints where knowledgeable staff offer product recommendations, and customers can assess product quality, design aesthetics, and build quality firsthand.

Physical retail locations create experiential shopping environments that foster community building among enthusiasts and enable impulse purchases through strategic product placement and cross-merchandising opportunities. However, the online channel is experiencing accelerated growth rates as digital natives increasingly prioritize convenience, broader product selection, and discreet purchasing options, with e-commerce platforms leveraging competitive pricing, subscription models, and direct-to-consumer shipping to capture market share from traditional retail formats.

Regional Insights

North America Smoking Accessories Market Trends

North America maintains undisputed market leadership in the global smoking accessories industry, driven by the U.S.'s pioneering role in cannabis legalization and the region's sophisticated consumer base with high disposable incomes. The legalization of recreational cannabis in multiple states, including California, Colorado, Washington, and Oregon, has created a thriving ecosystem of dispensaries, specialty retailers, and online platforms that collectively generate substantial demand for premium smoking accessories.

Canada's federal legalization of recreational cannabis in 2018 further solidified the region's progressive regulatory environment, fostering market maturity and encouraging product innovation. The region's innovation ecosystem, characterized by strong research and development capabilities, venture capital availability, and consumer willingness to adopt new technologies, has positioned North America as the global hub for next-generation vaporizer technology and smart smoking accessories incorporating digital connectivity and precision control features.

Europe Smoking Accessories Market Trends

Europe represents a sophisticated and mature market for smoking accessories, characterized by well-established tobacco cultures, progressive cannabis policies in select nations, and strong consumer preferences for premium and artisanal products. Germany, the U.K., France, and Spain collectively account for most of the European market revenue, with Germany leading due to its large population, high purchasing power, and liberal attitudes toward smoking accessories.

The European market is significantly influenced by regulatory harmonization efforts under European Union directives, particularly the Tobacco Products Directive, which establishes common standards across member states for tobacco-related products, including certain smoking accessories. The region demonstrates strong consumer preference for sustainability and environmental responsibility, driving demand for eco-friendly smoking accessories, including biodegradable rolling papers, reusable metal components, and products manufactured using ethical supply chains.

Asia Pacific Smoking Accessories Market Trends

Asia Pacific emerges as the fastest-growing regional market for smoking accessories. China dominates the regional market and is expected to maintain leadership through 2030, leveraging its massive domestic consumer base and well-established manufacturing infrastructure that positions Chinese companies as key suppliers to global markets.

Asian manufacturers increasingly produce sophisticated smoking accessories, including precision-engineered grinders, glass water pipes, and electronic vaporizers that compete with Western brands on quality while maintaining price advantages. The ASEAN region, encompassing countries like Thailand, Vietnam, and the Philippines, presents emerging opportunities as economic development accelerates and younger demographics demonstrate increasing interest in lifestyle products, including premium smoking accessories, though regulatory uncertainties remain significant market considerations.

Competitive Landscape

The smoking accessories market exhibits a fragmented competitive structure characterized by the coexistence of multinational tobacco corporations, specialized accessory manufacturers, and numerous artisanal producers catering to niche consumer segments. Major players including British American Tobacco PLC and Imperial Brands leverage their extensive distribution networks, brand recognition, and financial resources to maintain significant market influence, particularly in traditional tobacco accessories.

Research and development investments concentrate on sustainable materials, enhanced user experiences, and technology integration, while key differentiators include proprietary designs, premium materials, celebrity endorsements, and sustainability credentials. Emerging business model trends feature direct-to-consumer e-commerce platforms, subscription box services delivering curated accessory collections, and collaborations with artists and lifestyle brands that position smoking accessories as fashion statements rather than purely functional products.

Key Developments:

- May 2024: Imperial Brands substantially increased investment in newer nicotine and tobacco products, including heated tobacco systems, electronic cigarettes, and nicotine pouches through its Fontem Ventures subsidiary, positioning the company as a major accessory ecosystem participant alongside traditional tobacco product offerings.

- November 2024: British American Tobacco announced expanded distribution partnerships for its smoking accessories line across European markets, strengthening retail presence in Germany, France, and Spain through strategic agreements with major convenience store chains and specialized tobacco retailers.

Top Companies in the Smoking Accessories Market

- British American Tobacco PLC (London, U.K.): Global British American Tobacco PLC stands as a global leader in the smoking accessories market, leveraging its century-long heritage in tobacco products to establish dominant positions across multiple product categories. The company's extensive distribution network spanning 180 markets provides unparalleled retail access, while its brand portfolio includes both premium and value segments that address diverse consumer preferences.

- Imperial Brands (Bristol, U.K.): Imperial Brands represents a formidable competitor in the global smoking accessories market, distinguished by its focused portfolio strategy and strong European market presence. Imperial Brands' expertise in consumer engagement and retail partnerships positions it advantageously for smoking accessories distribution, particularly through its established relationships with convenience stores and tobacco specialty retailers across key European markets, including the United Kingdom, Germany, France, and Spain.

- Republic Technologies International (Illinois, U.S.): Republic Technologies International has established itself as a premier manufacturer of smoking accessories with particular strength in rolling papers and related consumables. The company's brand portfolio features iconic names that command strong loyalty among enthusiasts, while its manufacturing capabilities enable both quality consistency and competitive pricing.

Companies Covered in Smoking Accessories Market

- Bull Brand

- BBK Tobacco & Foods, LLP

- Chongz

- British American Tobacco PLC

- Curved Papers, Inc.

- Univac Furncrafts Pvt. Ltd.

- Imperial Brands

- Republic Technologies International

- Jinlin (HK) Smoking Accessories Co., Ltd.

- Moondust Paper Pvt. Ltd.

- Black Leaf

- Chongz Ltd.

- Empire Glassworks

- RAW Papers

Frequently Asked Questions

Valued at US$78.5 Bn in 2026, projected to US$103.4 Bn by 2033 at 4.0% CAGR during the forecast period, driven by cannabis legalization, premiumization trends, and technological innovation in product categories.

The market is primarily driven by expanding cannabis legalization across multiple countries with 7 nations permitting recreational use and 44 countries allowing medical cannabis, rising consumer preference for premium and sustainable products.

Rolling Papers & Cigarette Tubes at 32% share, attributed to their fundamental role as frequently purchased consumables, universal compatibility across tobacco and cannabis applications, affordability, and growing consumer demand for premium organic and slow-burning paper formats that enhance user experience.

North America leads the global market, with the U.S. capturing 72.8% of the regional market share, driven by progressive cannabis legalization across multiple states, and a sophisticated consumer base with high disposable incomes.

Significant opportunities include rapid expansion of vaporizer technology with advanced features like temperature control and smartphone connectivity, and penetration of emerging markets through e-commerce platforms, particularly in the Asia Pacific.

Major market players include British American Tobacco PLC, Imperial Brands, Republic Technologies International, Curved Papers, Inc., Bull Brand, and Chongz, each leveraging distinct competitive advantages, including brand heritage, manufacturing capabilities, sustainability positioning, and digital distribution networks.