- Semiconductor Materials & Components

- 3D Laser Scanner Market

3D Laser Scanner Market Size, Share, and Growth Forecast 2026 - 2033

3D Laser Scanner by Product Type (Terrestrial 3D Laser Scanners, Handheld 3D Laser Scanners, Mobile 3D Laser Scanners, Airborne 3D Laser Scanners), by Component (Hardware, Software, Services), by Application (Surveying & Mapping, Reverse Engineering, Quality Inspection, BIM & Architecture, Facility Management, Digital Twin, Forensics, Heritage Preservation), End-user, and Regional Analysis, 20262033

3D Laser Scanner Market Size and Trend Analysis

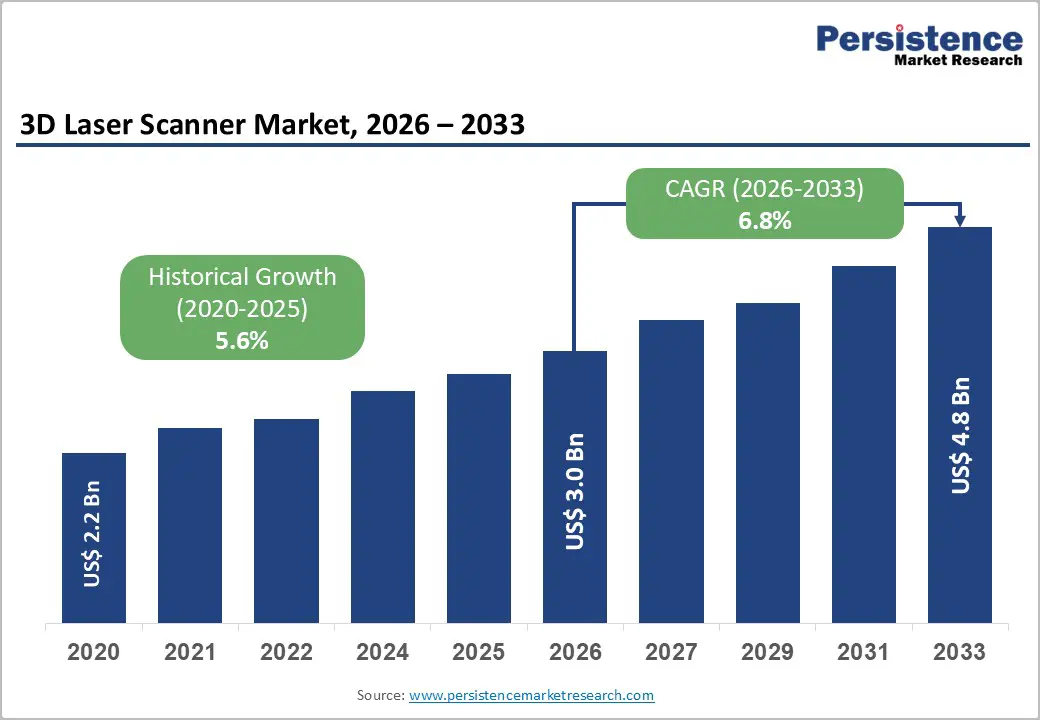

The global 3D laser scanner market is likely to be valued at US$ 3.0 billion in 2026 and is expected to reach US$ 4.8 billion by 2033, growing at a CAGR of 6.8% during the forecast period from 2026 to 2033. The expansion of the 3D laser scanner market is fundamentally driven by accelerating adoption across multiple high-value industries seeking precision measurement and digital documentation capabilities.

Key Market Highlights

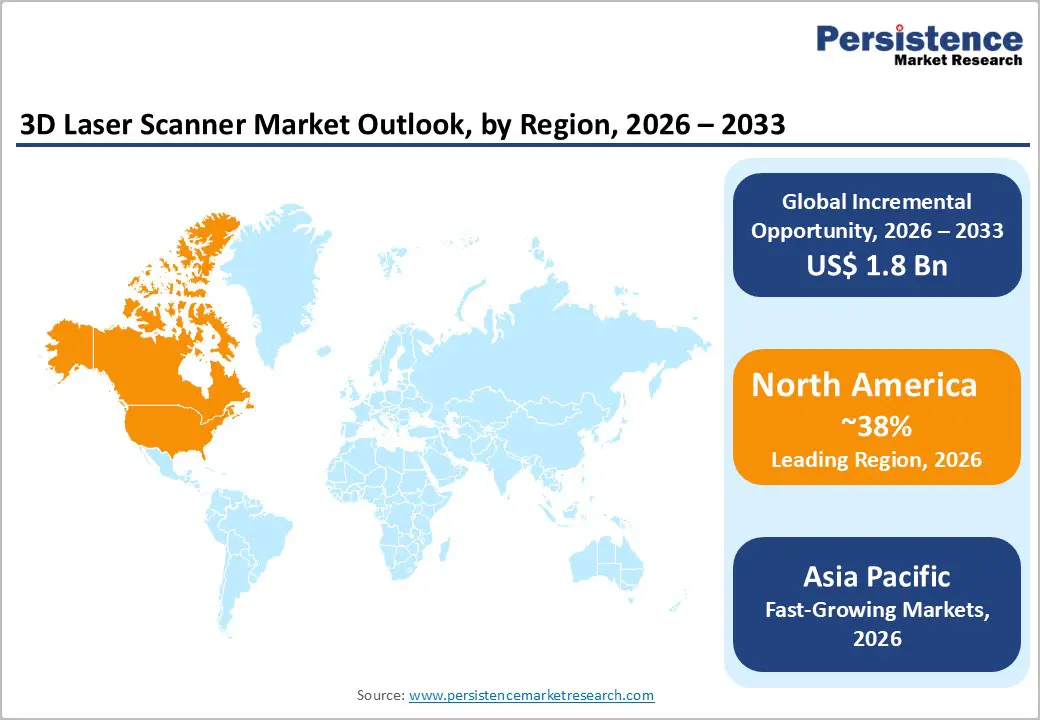

- Leading Region: North America dominates the global market with 38% share, supported by mature industrial adoption, stringent regulatory frameworks, and leadership by major equipment manufacturers establishing regional innovation centers supporting continuous technology advancement in scanning precision and data processing capabilities.

- Fastest-Growing Region: Asia Pacific emerges as fastest-growing region projected to expand at 9.5% annually through 2033, driven by China's smart manufacturing initiatives, India's infrastructure modernization, and government smart city programs creating sustained demand for large-scale surveying and mapping applications supporting urban development and industrial automation.

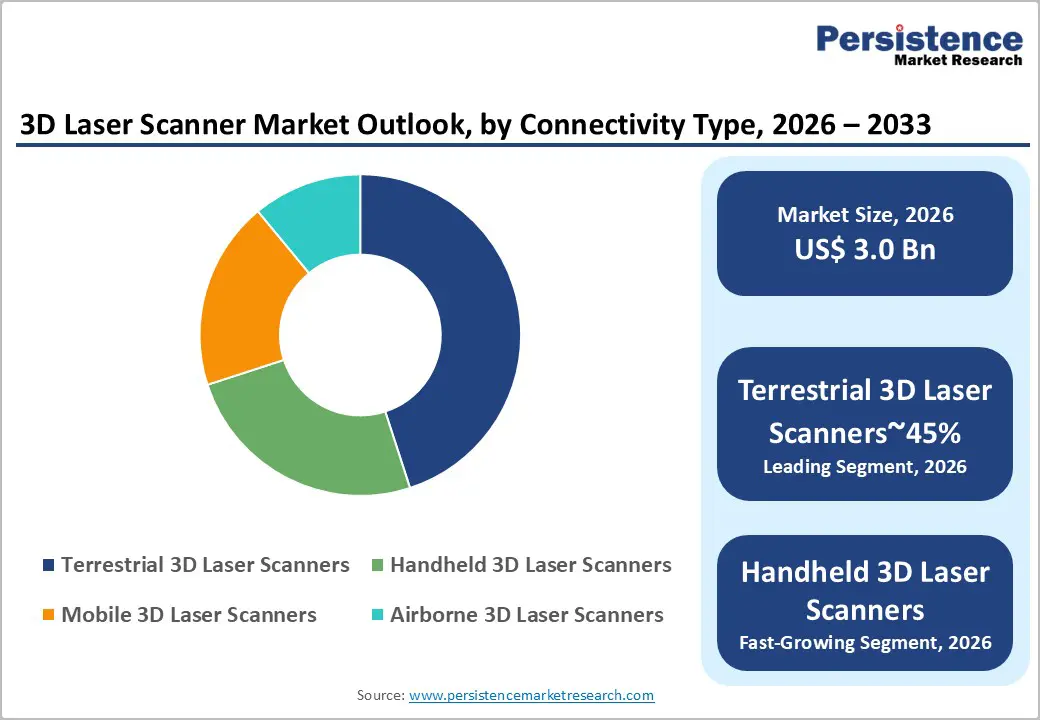

- Leading Segment: Terrestrial 3D Laser Scanners dominate product mix with 45% market share due to superior millimeter-level accuracy characteristics, established software ecosystems, and proven performance across heritage preservation, construction documentation, and infrastructure asset inventory applications requiring comprehensive spatial detail.

- Fastest-Growing Segment: SLAM-based handheld scanners represent fastest-growing product category expanding at approximately 18% annually, enabled by advances in simultaneous localization and mapping algorithms, blue laser technology, and miniaturization supporting rapid adoption within construction sites, infrastructure inspection, and emergency response scenarios requiring mobile spatial data capture.

- Key Opportunity: Quality Inspection and Reverse Engineering applications represent primary growth opportunity with 13% annual expansion driven by zero-defect manufacturing initiatives, aerospace quality certification mandates, and healthcare prosthetics customization requiring automated dimensional verification and AI-powered defect detection supporting Industry 4.0 manufacturing transformation.

| Key Insights | Details |

|---|---|

| 3D Laser Scanner Market Size (2026E) | US$ 3.0 Billion |

| Market Value Forecast (2033F) | US$ 4.8 Billion |

| Projected Growth CAGR(2026-2033) | 6.8% |

| Historical Market Growth (2020-2025) | 5.6% |

Market Dynamics

Drivers - Rising Industry 4.0 adoption is driving demand for high-precision 3D laser scanning to enable digital twins and smart factory optimization

Digital twin technology is transforming how organizations manage assets across manufacturing, construction, and facility operations, significantly increasing demand for high-precision 3D laser scanning systems. These systems provide accurate baseline spatial data required to build reliable digital replicas of physical environments. As companies adopt Industry 4.0 frameworks, comprehensive facility documentation becomes essential for real-time monitoring, predictive maintenance, and automated optimization processes.

Integration of 3D laser scanning with IoT systems and cloud-based analytics enables continuous performance tracking and operational improvement. Many manufacturing facilities using laser-supported digital twins report productivity improvements of 15%, along with longer equipment life and lower maintenance costs, which strongly justify capital investment. This trend is especially strong in automotive and aerospace industries, where strict tolerance verification, complex geometry validation, and regulatory certification demand highly accurate spatial measurement technologies for consistent supply chain compliance.

Large-scale infrastructure expansion and smart city programs are accelerating adoption of advanced 3D spatial data capture technologies worldwide

Large-scale infrastructure development projects, including transportation systems, smart city programs, and renewable energy installations, are significantly boosting demand for fast and accurate spatial data collection technologies. Traditional surveying methods often fail to meet the compressed timelines of modern infrastructure projects, making 3D laser scanning a preferred solution. Governments across Asia Pacific and emerging economies are heavily investing in urbanization and infrastructure modernization, creating long-term demand for advanced surveying and mapping technologies.

Smart city initiatives rely heavily on high-resolution 3D spatial data for traffic planning, utility coordination, public safety, and emergency response systems. Studies show that infrastructure projects using 3D laser scanning reduce rework costs by 40–60% and shorten completion timelines by 30%. These measurable efficiency gains create strong financial justification, accelerating adoption among both public authorities and private infrastructure developers.

Restraints - High equipment costs, software expenses, and skilled labor requirements continue to limit 3D laser scanner adoption among smaller organizations

High initial investment remains a major barrier to adoption of professional 3D laser scanning systems, particularly for small and medium-sized enterprises. Terrestrial scanners typically cost between US$100,000 and US$500,000 or more, excluding essential software licenses, training, and calibration expenses. Beyond equipment purchase, organizations must invest in skilled personnel, ongoing maintenance contracts, and periodic recalibration to maintain measurement accuracy. Over time, total cost of ownership can reach two to three times the initial hardware cost.

Advanced scanning software platforms require technical expertise to manage large point cloud datasets, execute accurate registrations, and optimize scanning workflows. For organizations lacking in-house geospatial specialists, this operational complexity creates significant adoption challenges, limiting market penetration among cost-sensitive and non-specialized users.

Rising point cloud data volumes and strict geospatial regulations increase storage, security, and interoperability challenges for scanning users

The rapid increase in point cloud data volumes presents major challenges for organizations adopting 3D laser scanning technologies. Terrestrial scanners can generate 1–2 gigabytes of data per session, while airborne or large-scale surveys may produce terabytes of information. Managing storage, processing, and long-term archival of such data strains IT infrastructure, especially for smaller firms.

In addition, strict data privacy regulations such as GDPR and emerging geospatial data governance frameworks impose compliance obligations on organizations handling sensitive spatial information. These requirements increase cybersecurity costs and administrative complexity. The lack of standardized data formats across scanning vendors further complicates operations, often resulting in vendor lock-in. This interoperability challenge restricts flexibility for organizations managing multi-vendor datasets across different regions and project environments.

Opportunities -SLAM-enabled handheld scanners are transforming field data collection by enabling faster, cost-efficient, and accessible 3D mapping operations

The integration of SLAM (Simultaneous Localization and Mapping) technology into handheld and wearable 3D laser scanners is significantly expanding market accessibility. These portable systems allow non-specialist users to capture accurate point cloud data quickly, often achieving centimeter-level accuracy within minutes. SLAM-based scanners operate independently of GPS, enabling reliable performance in indoor environments, underground locations, and dense urban areas where traditional surveying methods struggle.

The handheld scanning segment is growing at approximately 18% annually as use cases expand across construction documentation, infrastructure inspection, and emergency response. Organizations report 50% reductions in field data collection time compared to conventional terrestrial systems. Improved cost-per-scan economics and higher throughput are supporting service-based business models, creating strong opportunities for surveying, construction, and industrial inspection providers.

AI-powered laser scanning is reshaping quality inspection through automated defect detection and predictive manufacturing quality assurance systems

AI-powered 3D laser scanning solutions are increasingly transforming quality control processes across automotive, aerospace, and precision manufacturing industries. These systems enable automated inspection workflows that support zero-defect manufacturing goals while reducing manual inspection labor costs by 70%. Machine learning models trained on historical defect data can detect anomalies in real time during scanning, allowing immediate corrective action.

The integration of laser scanning with computer vision and deep learning enables automated tolerance checks, surface defect identification, and dimensional verification without human intervention. This shift moves quality assurance from post-production inspection to predictive, in-process monitoring. Healthcare applications present strong growth potential, including prosthetics manufacturing, dental restoration, and surgical planning, where patient-specific scanning improves outcomes and shortens production timelines from weeks to days.

Category-wise Analysis

Product Type Insights

Terrestrial 3D laser scanners are dominant accounting for approximately 45% share in 2025, supported by their superior accuracy and long-standing use in professional surveying and construction applications. These tripod-mounted systems typically deliver 1–3 mm accuracy, making them ideal for as-built documentation, infrastructure assessment, and heritage preservation projects. The segment benefits from decades of technological maturity, well-established software ecosystems, and trusted performance standards.

Despite the emergence of mobile and handheld alternatives, terrestrial scanners remain difficult to replace in applications requiring extremely high precision and dense point cloud detail. Structural monitoring, forensic investigation, and complex architectural verification continue to rely heavily on terrestrial systems, as mobile technologies cannot yet consistently match their accuracy and data quality within comparable operational conditions.

Component Insights

Hardware represents the largest component segment, accounting for approximately 55% of total market revenue. This includes laser scanner units, tripods, mounting systems, optical modules, and environmental sensors. The segment remains capital intensive due to the use of advanced laser technology, precision optics, and high-quality mechanical components. Hardware growth is supported by innovations such as blue laser diodes, improved surface detection capabilities, and ongoing miniaturization enabling portable designs.

Software and services together contribute about 45% of market revenue and are gaining increasing importance. Advanced software platforms support point cloud processing, data visualization, BIM integration, and automated analytics. As organizations focus more on extracting value from spatial data, software-driven workflow automation is becoming a critical differentiator beyond hardware capabilities alone.

Application Insights

Surveying and mapping represent the largest application segment, holding nearly 35% market share. These applications support land surveys, civil engineering projects, infrastructure mapping, and urban planning initiatives. Regulatory requirements for accurate spatial documentation in construction and environmental assessment create stable, long-term demand. BIM and architectural applications are expanding at annual growth rates of 9%, driven by widespread adoption of scan-to-BIM workflows for design coordination and as-built documentation.

Quality inspection is the fastest-growing application area, growing at 11% annually. Automotive, aerospace, and medical device manufacturers increasingly rely on laser scanning for automated inspection, tolerance verification, and regulatory documentation, driven by strict quality standards and zero-defect production objectives.

End-user Insights

Construction and infrastructure end users account for approximately 40% of total market share, making them the largest consumer group. These users rely on 3D laser scanning for project planning, progress tracking, and compliance documentation. Growth is supported by global investments in smart cities, transportation networks, and renewable energy infrastructure. Manufacturing represents around 28% of market share and is the fastest-growing end-user segment, expanding at 10% annually.

Applications include reverse engineering, mold validation, automated inspection, and production optimization aligned with Industry 4.0 goals. Aerospace and defense account for about 12% of market share but demonstrate the highest willingness to invest in premium scanning systems due to safety-critical and regulatory-driven accuracy requirements.

Regional Insights

North America 3D Laser Scanner Market Trends

North America leads the global market with approximately 38% share, supported by a strong industrial base and advanced technology adoption. The United States contributes nearly 70% of regional demand, driven by widespread use of BIM workflows across construction and facility management sectors. Regulatory requirements related to safety documentation, building codes, and aerospace quality standards create sustained demand for professional scanning services.

Leading manufacturers such as Hexagon AB, FARO Technologies, and Trimble have established innovation hubs in the region, driving advancements in AI-enabled processing, cloud collaboration, and autonomous scanning systems. Early adoption of SLAM-based handheld scanners and drone-integrated LiDAR solutions further strengthens North America’s position as a technology leader and premium market.

Europe 3D Laser Scanner Market Trends

Europe accounts for approximately 28% of global market share, led by Germany, the United Kingdom, France, and Spain. Strong industrial manufacturing, strict construction regulations, and emphasis on measurement accuracy support consistent demand. Germany’s advanced manufacturing sector heavily utilizes terrestrial laser scanning for plant modernization and industrial documentation.

The region also shows strong adoption in heritage preservation, where non-invasive scanning supports restoration of historical and UNESCO-listed sites. EU-wide digital documentation standards and harmonized BIM regulations are driving broader adoption of 3D scanning technologies. Additionally, Europe is witnessing rapid uptake of handheld and mobile scanners as construction firms seek productivity improvements and reduced labor dependency across complex multi-discipline projects.

Asia Pacific 3D Laser Scanner Market Trends

Asia Pacific is the fastest-growing regional market, projected to expand at 9.5% annually through 2033. Rapid industrialization, large-scale infrastructure development, and government-backed smart city initiatives are key growth drivers. China holds an estimated 22% global market share, supported by extensive urban construction, high-speed rail projects, and manufacturing modernization programs.

Laser scanning is increasingly used in automotive, electronics, and semiconductor production for quality control and automation. Japan and South Korea demonstrate strong demand driven by advanced manufacturing standards. India represents a high-potential emerging market, with rising infrastructure investment and smart city programs supporting 7% annual growth as local scanning capacity and affordability improve.

Competitive Landscape

The global 3D laser scanner market is moderately consolidated, with leading players such as Hexagon AB, FARO Technologies, Trimble Inc., Topcon Corporation, and Carl Zeiss AG collectively holding the largest market share. High entry barriers exist due to significant R&D investment requirements, sensor technology complexity, and global distribution needs. Market participants compete through technology innovation, industry-specific solutions, and integrated software ecosystems.

Differentiation strategies include blue laser technology, advanced SLAM algorithms, and cloud-based collaboration tools. Emerging mid-market competitors focusing on handheld and mobile scanning are increasing competitive pressure by offering lower-cost and easy-to-use solutions. Strategic partnerships with BIM platforms and analytics providers further strengthen customer retention and create long-term switching cost advantages.

Key Market Developments

- In February 2025, Topcon Corporation and FARO Technologies announced a strategic partnership to jointly develop and distribute integrated laser scanning solutions that combine both companies’ geospatial positioning and reality capture expertise, targeting construction, surveying, mapping, architecture, forensics, and BIM applications through enhanced product and channel alignment.

- In May 2024, FARO introduced the FARO Orbis, a hybrid mobile and stationary 3D laser scanning system designed for broader market reach, with hybrid SLAM and Flash technology enabling efficient reality capture that balances mobility with performance and supports use by construction contractors and field service teams.

- In January 2025, Leica Geosystems released the BLK360 G2, an updated imaging laser scanner with significantly faster capture speed, improved point cloud quality, expanded HDR imaging, and integrated VIS technology for automated alignment, enhancing productivity and competitiveness of its established scanner portfolio.

Companies Covered in 3D Laser Scanner Market

- Hexagon AB

- FARO Technologies, Inc.

- Trimble Inc.

- Topcon Corporation

- Nikon Metrology

- Creaform

- RIEGL Laser Measurement Systems GmbH

- Zoller + Fröhlich GmbH (Z+F)

- Perceptron, Inc.

- 3D Digital Corporation

- Maptek Pty Ltd

- Kreon Technologies

- ShapeGrabber Inc.

- Surphaser

- Carl Zeiss AG

- Leica Geosystems

- Teledyne Technologies

- GOM GmbH

Frequently Asked Questions

The global 3D Laser Scanner market is expected to reach US$ 4.8 billion by 2033, growing at a 6.8% CAGR from 2026.

Market growth is driven by digital twin adoption, smart city development, regulatory quality requirements, and rising use of portable SLAM-based scanning systems.

Terrestrial 3D laser scanners dominate the market due to their high accuracy, reliability, and strong adoption in surveying and infrastructure documentation.

North America maintains market leadership with approximately 38% global share driven by mature industrial adoption, stringent regulatory frameworks, and prominent equipment manufacturers that establish regional innovation centers supporting continuous technology advancement.

SLAM-based handheld scanners and AI-driven quality inspection systems represent the highest-growth opportunities in the market.

Leading companies include Hexagon AB, FARO Technologies, Trimble Inc., Topcon Corporation, Carl Zeiss AG, and Leica Geosystems.