ID: PMRREP15961| 365 Pages | 14 Nov 2025 | Format: PDF, Excel, PPT* | Healthcare

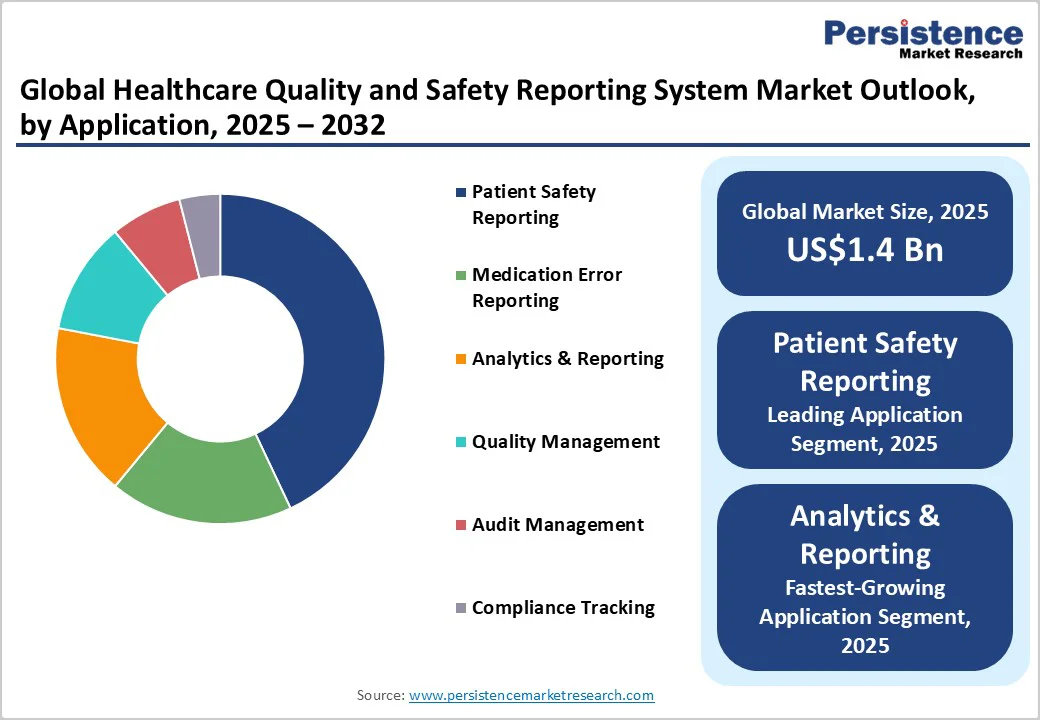

The global healthcare quality and safety reporting system market size is likely to be valued at US$1.4 Billion in 2025, and is estimated to reach US$3.0 Billion by 2032, growing at a CAGR of 12% during the forecast period 2025−2032, driven primarily by increasing regulatory pressures on healthcare reporting standards and a growing focus on patient safety optimization. Key growth drivers include the adoption of digital healthcare, compliance mandates from bodies such as The Joint Commission and CMS, and AI- and cloud-enabled real-time analytics. Rising medical errors and value-based reimbursement models are also driving investment in advanced quality and safety platforms that enhance clinical decisions and patient outcomes.

| Key Insights | Details |

|---|---|

|

Healthcare Quality and Safety Reporting System Market Size (2025E) |

US$1.4 Bn |

|

Market Value Forecast (2032F) |

US$3.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12% |

|

Historical Market Growth (CAGR 2019 to 2024) |

12.5% |

Healthcare regulatory bodies internationally are intensifying mandates around quality reporting and patient safety documentation, substantially driving system adoption. The Joint Commission in the U.S. has expanded its reporting requirements for adverse event monitoring, while the CMS is increasingly tying reimbursement rates to compliance with patient safety metrics. Globally, guidelines from the World Health Organization (WHO) and European Medicines Agency (EMA) focus on incident reporting transparency and medical device vigilance, further pressuring healthcare providers to implement comprehensive reporting systems.

Substantiating this regulatory thrust are the estimates released by the U.S. Department of Health and Human Services that state that preventable medical errors result in approximately 251,000 deaths annually, prompting calls for enhanced surveillance. Broadly, the evolving healthcare regulatory environment is accelerating adoption by making quality and safety outcomes central to financial viability and accreditation processes. This momentum ensures not only compliance but also fosters a culture of continuous quality improvement and accountability within healthcare ecosystems, thereby compelling healthcare organizations to upgrade legacy systems or adopt next-generation solutions equipped with integrated AI and automated reporting technologies.

The initial implementation costs for quality and safety reporting systems remain prohibitive, especially for small and mid-sized healthcare providers in emerging markets. The total cost of ownership includes not only software licensing but also infrastructure upgrades, workforce training, and integration with existing electronic health record (EHR) systems, generating significant budgetary burdens. Studies estimate that the upfront capital expenditure for these systems ranges between US$150,000 and US$500,000, depending on system complexity and deployment type, with ongoing maintenance adding to the initial costs annually. Further compounding the challenge is the technical complexity related to integration with heterogeneous legacy healthcare IT infrastructure, necessitating specialized IT expertise and often resulting in implementation delays exceeding several months.

As a result, a large percentage of healthcare providers either postpone or scale back quality system investments due to budget constraints or anticipated operational disruptions during deployment. The lack of interoperability standards across different healthcare systems exacerbates integration costs and operational inefficiencies, limiting the scalability of solutions. This restraint impacts market growth by slowing penetration rates in resource-constrained environments and prolonging the modernization timelines for established healthcare facilities, necessitating vendors to focus on modular, cloud-based, and lower-cost deployment options to mitigate barriers.

Emerging markets across Asia Pacific, Latin America, and the Middle East are presenting lucrative opportunities for the healthcare quality and safety reporting system market growth, facilitated by rapidly expanding healthcare infrastructure and increasing digital health investments. Countries in these regions are witnessing rising government healthcare expenditure, alongside initiatives to improve patient safety standards, aligning with global benchmarks. Cloud-based deployment models specifically unlock cost-effective scalability and accessibility, eliminating the need for heavy upfront capital investments and enabling rapid adoption in smaller hospitals and rural clinics.

Strategic factors driving this opportunity include digital health policy reforms promoting interoperability and data sharing, popularization of mobile health technologies, and increasing NGO-driven patient safety programs. Cloud adoption also supports real-time data analytics, AI integration, and compliance reporting with minimal infrastructure overhead. Vendors investing in localized offerings with multi-language support and region-specific compliance features are poised to capitalize on this market expansion, while collaborations with regional government healthcare authorities will accelerate adoption and regulatory alignment.

In 2025, cloud-based deployment is set to be the dominant segment with an estimated 62.5% of the healthcare quality and safety reporting system market revenue share, reflecting healthcare providers’ increasing preference for flexible, scalable, and cost-efficient delivery models. Cloud solutions offer significant advantages in minimizing upfront capital expenditures and accelerating adoption cycles, especially among outpatient clinics and emerging market hospitals that face budget and IT staffing constraints.

The fastest-growing deployment segment from 2025 to 2032 is also cloud-based, propelled by ongoing digital transformation initiatives, greater investments in cyber-security enabling broader cloud acceptance, and evolving regulatory requirements encouraging interoperability and data transparency. Cloud infrastructure providers are enhancing healthcare-specific offerings with compliance certifications, such as the Health Insurance Portability and Accountability Act (HIPAA) of the U.S. and the General Data Protection Regulation (GDPR) of the EU, multi-region data hosting, and AI-powered analytics capabilities, thus widening their usage and integration across healthcare quality and safety applications.

Patient safety reporting is poised to lead the market in 2025, commanding an estimated 45% revenue share. This dominance is anchored by the urgent need for healthcare providers to monitor, document, and reduce adverse events and medical errors that may jeopardize patient health and violate regulatory mandates. Patient safety modules typically focus on incident and near-miss reporting workflows, root-cause analysis, and compliance dashboarding, and they have become foundational components of digital quality programs across hospitals and outpatient service settings.

The analytics and reporting segment is slated to be the fastest-growing application area from 2025 to 2032. Healthcare organizations are increasingly investing in advanced predictive risk management tools, integrating AI and machine learning (ML) to proactively identify potential safety threats before they escalate into adverse events. Analytics solutions deliver granular, actionable insights to clinicians and administrators, optimizing resource allocation and clinical decision-making. Regulatory environments are also encouraging more standardized and comprehensive reporting, further fueling the adoption of sophisticated analytics capabilities beyond traditional incident reporting.

Hospitals are expected to represent the largest end-user segment in 2025 with an approximate 55% market revenue share. This leadership is driven by the complexity and scale of hospital operations, high patient volumes, and stringent regulatory scrutiny. The relatively larger IT budgets and multi-disciplinary care models of hospitals necessitate advanced safety reporting systems that integrate with broad clinical and administrative workflows, supporting a wide range of safety monitoring and quality assurance functions.

The ambulatory surgical centers are forecasted as the fastest-growing end-user segment from 2025 to 2032. This growth trajectory is fueled by the rising volume of outpatient procedures due to healthcare cost-containment efforts, technological advancements enabling minimally invasive surgeries, and increasing regulatory focus on safety compliance in non-hospital surgical settings. These centers are adopting dedicated reporting systems that offer tailored functionalities supporting their unique workflows, regulatory reporting obligations, and patient safety objectives, representing an emerging growth frontier for vendors.

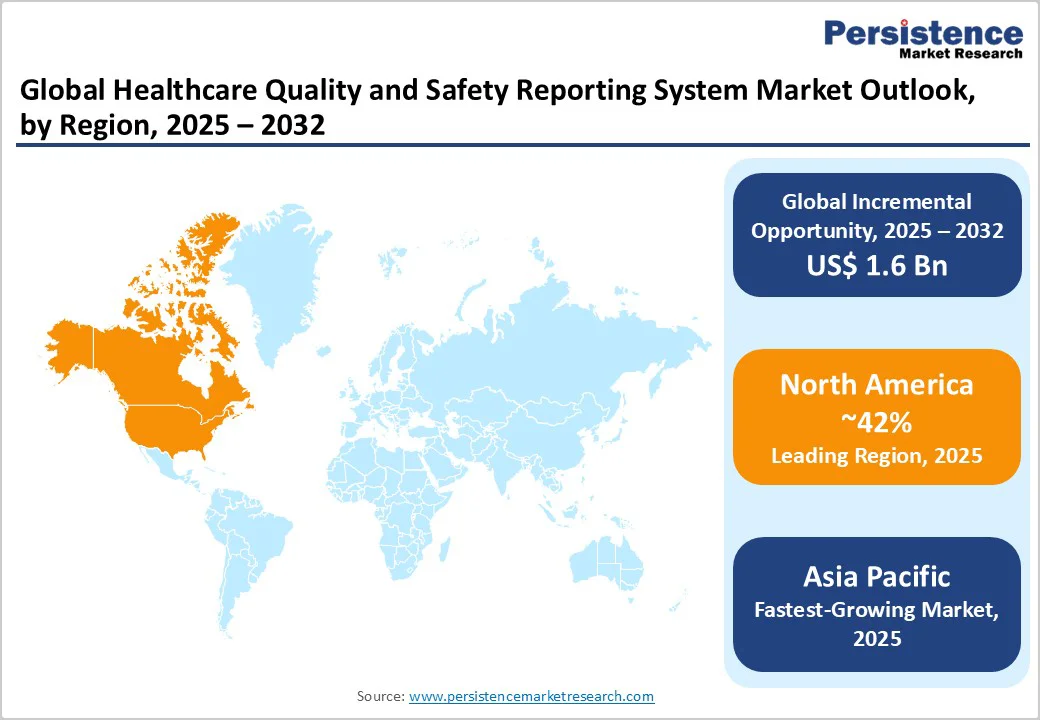

North America is anticipated to dominate with 42% of the healthcare quality and safety reporting system market share in 2025. The region’s dominance is underpinned by the U.S. healthcare sector’s mature IT infrastructure, comprehensive regulatory frameworks such as the HIPAA and the Health Information Technology for Economic and Clinical Health (HITECH) Act, and the influence of patient safety organizations, including The Joint Commission.

Through the forecast period up to 2032, North America is projected to maintain strong growth, bolstered by a vibrant innovation ecosystem encompassing AI, predictive analytics, and patient-centered care models. Leading healthcare IT vendors and startups are actively collaborating with hospitals and policymakers to pilot integrated quality systems that ensure regulatory compliance while enhancing clinical outcomes. Regional investment trends are focused on acquiring or partnering with analytics and cloud service providers to accelerate technology dissemination and scalability.

Europe is set to secure a 25% market share in 2025, driven by Germany, the U.K., France, and Spain, which are channeling investments in healthcare digitalization and patient safety initiatives. The EU’s harmonized regulatory frameworks, such as the Medical Device Regulation (MDR) and Patient Safety and Quality Directives, have standardized reporting requirements and improved data interoperability across member states. This regulatory harmonization has facilitated easier adoption across services, promoting integration of safety reporting software with national healthcare information systems.

The regional market’s growth forecast between 2025 and 2032 signals ongoing investments in hospital digital transformation and value-based care programs. European healthcare providers increasingly adopt integrated quality management suites that encompass real-time monitoring, compliance tracking, and reporting automation. Strategic partnerships between vendors and national health services foster co-development of localized solutions supporting regulatory nuances and language diversity. Regional competitive landscape favors vendors offering comprehensive, modular platforms aligned with public healthcare priorities, positioning the region as a model for multi-country interoperable quality reporting.

The Asia Pacific market is predicted to grow at the highest CAGR of approximately 13.9% from 2025 to 2032. Economic growth and improving healthcare infrastructure development in China, India, and ASEAN countries drive this momentum. Dedicated government initiatives aimed at improving patient safety standards, reducing hospital-acquired infections, and digitizing health services create fertile conditions for system adoption. The region’s heterogeneous regulatory environment has necessitated adaptable quality reporting solutions covering diverse operational and compliance needs.

Multinational vendors are leveraging joint ventures and acquisitions of local players to navigate regulatory variations and accelerate penetration. Cloud-based deployment models are particularly favored, thanks to lower upfront costs and scalable access for a range of healthcare providers. Investment opportunities are flourishing in telemedicine integration, AI-driven analytics tailored to regional priorities, and the development of regional healthcare data exchange frameworks, positioning Asia Pacific as both a growth engine and an innovation incubator.

The global healthcare quality and safety reporting system market landscape exhibits moderate consolidation. Leading players such as Quantros LLC, The Patient Safety Company, Riskonnect, Datix Ltd., and PowerHealth Solutions have established dominant positions, controlling nearly half of the market revenues, powered by integrated platform offerings, extensive client bases, and strong brand presence. These firms invest heavily in R&D to introduce AI-enhanced analytics, cloud migration solutions, and user-friendly interfaces aimed at expanding adoption in hospitals and outpatient sectors.

While market concentration is significant, a competitive fringe of specialized vendors focuses on emerging markets, modular product suites, and niche application areas where customization and agility are valued. The competitive dynamics are further intensified by continuous technology innovation and shifting healthcare compliance regulations, which mandate upgraded capabilities, creating ongoing opportunities for new entrants and technology partnerships. The balanced market structure allows innovation-driven firms to capture emerging client needs without excessive monopolization risks.

The global healthcare quality and safety reporting system market is projected to reach US$1.4 Billion in 2025.

Increasing regulatory pressures on healthcare reporting standards, a steady rise in medical error rates at healthcare facilities, and a growing focus on patient safety optimization are driving the market.

The healthcare quality and safety reporting system market is poised to witness a CAGR of 12% from 2025 to 2032.

Accelerated adoption of digital healthcare initiatives, mandated quality compliance protocols from bodies such as The Joint Commission, and integration of advanced technologies such as AI and cloud computing, which enable real-time analytics and proactive risk mitigation, are lucrative market opportunities.

Quantros LLC, The Patient Safety Company, Riskonnect, Inc., and Datix Ltd. are some of the key players in the market.

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2019 – 2024 |

|

Forecast Period |

2025 – 2032 |

|

Market Analysis |

Value: US$ Bn |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Deployment Mode

By Application

By End-user

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author