ID: PMRREP16072| 194 Pages | 12 Jan 2026 | Format: PDF, Excel, PPT* | Consumer Goods

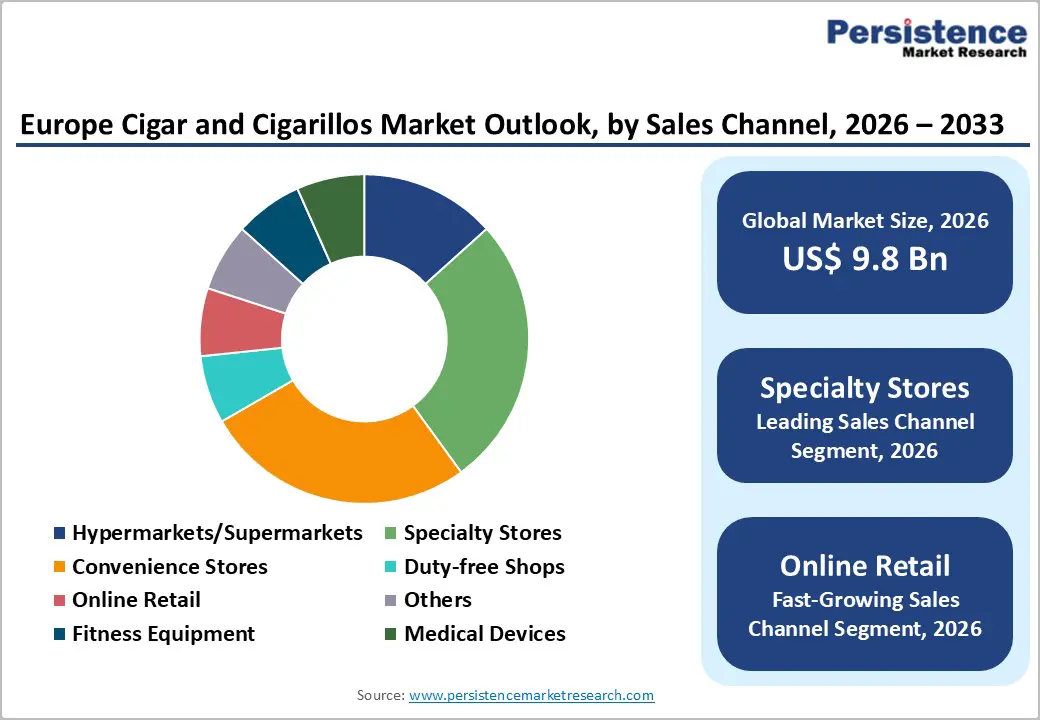

The Europe Cigar and Cigarillos market size was valued at US$ 9.8 billion in 2026 and is projected to reach US$ 17.0 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033. The market is experiencing sustained expansion driven by escalating demand for premium and luxury tobacco products among affluent consumers, diversification of flavor profiles catering to younger demographics, and strategic expansion of distribution channels, particularly through online retail platforms and duty-free establishments.

| Key Insights | Details |

|---|---|

| Europe Cigar and Cigarillos Market Size (2026E) | US$ 9.8 Bn |

| Market Value Forecast (2033F) | US$ 17.0 Bn |

| Projected Growth CAGR (2026-2033) | 8.2% |

| Historical Market Growth (2020-2025) | 7.7% |

Market Growth Drivers

Premium Cigar Premiumization and Luxury Consumption Expansion

The premium cigar segment represents the primary growth catalyst within the European market, driven by affluent consumer segments treating premium cigars as status symbols and luxury goods demonstrating remarkable resilience to economic pressures and consumer budget constraints. Premium cigars are projected to expand to 6.4% CAGR through 2033, substantially outpacing mass-market segment growth rates due to affluent consumers maintaining purchasing patterns during economic uncertainty. Imperial Brands' Backwoods brand exemplifies this premiumization strategy, successfully positioning itself in premium categories within mass-market distribution channels while continuously gaining market share despite economic headwinds and regulatory challenges.

Manufacturers strategically emphasize higher-margin offerings to counterbalance escalating regulatory compliance costs, taxation burdens, and packaging requirements imposed by European Union regulatory frameworks. Cigar lounge culture remains robust across European urban centers, with premium establishments offering sophisticated retail environments and experiential consumption supporting premium product positioning. Rising disposable incomes across European markets including Germany, France, and Spain have enabled broader participation in premium cigar consumption among middle and upper-middle class consumers.

Flavored Cigarillos Adoption and Youth Market Penetration

The flavored cigar segment represents the fastest-growing product category within European markets, driven by manufacturers developing innovative flavored combinations specifically targeting younger adult demographics seeking alternatives to heavily regulated flavored cigarettes now restricted by European Tobacco Products Directive (TPD). Flavored cigars have increased by approximately 50% since 2008 and now account for over 50% of total cigar market consumption, with fruit flavor remaining the most popular category among emerging consumers.

Cigarillos consumption across Europe increased to 13% in 2023, reflecting escalating adoption among younger generations seeking smaller, more affordable alternatives to traditional full-size cigars. Manufacturers are launching innovative flavor fusion products, with Dutch Masters introducing Gotham Cigars featuring flavor combinations such as berry, mint, and java, exemplifying product innovation strategies that capture evolving consumer preferences. Cigars and cigarillos provide regulatory alternatives to cigarettes with characterizing flavors, which were banned throughout European Union member states, creating strategic advantages for cigarillo brands seeking to capture consumers displaced by cigarette flavor prohibitions.

Market Restraints

Stringent European Tobacco Regulatory Framework and Tax Burden

The European regulatory environment imposes substantial compliance obligations, manufacturing constraints, and cost structures limiting market expansion and profitability for manufacturers operating across multiple EU member states. The Tobacco Products Directive (TPD) established comprehensive regulatory requirements including mandatory graphic warning labels covering 65% of package front and back surfaces, strict additive documentation, mandatory plain packaging requirements in certain jurisdictions, and comprehensive track-and-trace systems monitoring all tobacco products from manufacturing through retail distribution.

Tax harmonization efforts and the modernization of the Tobacco Taxation Directive are increasing tax burdens on tobacco products, particularly on mass-market segments where price sensitivity is elevated. The European Union loses approximately 13 billion euros annually to illicit tobacco trade, diverting legitimate market revenues and creating unfair competition from unregulated products. Advertising restrictions prohibit traditional mass-media promotion, constraining brand-building capabilities particularly for emerging brands lacking established market positioning.

Health Awareness and Anti-Smoking Campaign Pressures

Escalating public health campaigns emphasizing smoking-related health risks, government restrictions on smoking in public spaces, and evolving societal attitudes toward tobacco consumption create persistent headwinds for market expansion and consumer adoption. Strict public place smoking bans limit product visibility and consumption occasions, reducing trial opportunities and social normalization of cigar consumption, particularly among younger demographics. Healthcare systems across European nations are implementing aggressive anti-smoking public awareness campaigns highlighting nicotine addiction and health consequences, directly contradicting industry marketing messages. Regulatory pressures from WHO Framework Convention for Tobacco Control (FCTC) implementation across EU member states continue escalating compliance requirements and restricting promotional opportunities.

Market Opportunities

Online Retail Expansion and E-Commerce Channel Development

Digital retail channels represent substantial growth opportunities for European cigar and cigarillos market participants, driven by technological advancements that enable sophisticated age-verification systems, expanded access to product selection, and consumer preference for convenient purchase options that combine discretion with product selection depth unavailable through traditional retail channels. Online cigar retail is projected to expand at 8.8% CAGR, substantially outpacing traditional offline retail channels as digital commerce infrastructure matures and regulatory frameworks develop age-verification protocols satisfying European tobacco control requirements.

E-commerce platforms enable manufacturers to directly reach geographically dispersed consumers across multiple European markets while offering comprehensive product information, expert recommendations, and personalized purchasing experiences supporting premium product positioning. Duty-free retail operations at international airports represent additional high-margin retail channels that capitalize on affluent traveler demographics, with purchasing power supporting premium cigar consumption. Digital marketing strategies leveraging social media, influencer partnerships, and experiential content development enable brands to build sophisticated positioning and community engagement with targeted consumer segments.

Heritage Branding and Sustainable Product Innovation Strategy

European consumers increasingly gravitate toward cigar brands emphasizing heritage, craftsmanship, and sustainable sourcing practices, creating compelling differentiation opportunities for manufacturers developing authentic narratives around product origins, artisanal production methodologies, and environmental stewardship. Premium brands highlighting heritage and family legacy command superior positioning and price realization among affluent consumers treating cigars as cultural artifacts and investment-quality luxury goods.

Sustainable sourcing initiatives that address consumer concerns about environmental impact, deforestation, and agricultural practices create competitive differentiation, particularly among environmentally conscious upper-income segments willing to pay a premium to support sustainable production standards. Organic and naturally flavored cigar options appeal to health-conscious consumers seeking premium products perceived as lower-risk alternatives to conventional tobacco products. Limited-edition releases, collaborative artist collections, and numbered series cigars create scarcity and exclusivit,y driving demand among collectors and enthusiasts.

Product Type Analysis

The Premium Cigar segment commands dominant market positioning, accounting for approximately 58% of total European market revenue despite representing smaller unit volumes compared to mass-market products. Premium cigars are expanding at 6.4% CAGR through 2033, substantially exceeding mass-market growth rates, driven by affluent consumer segments treating premium products as luxury goods and status symbols resistant to price-sensitivity and economic fluctuations. European nations including Switzerland, Netherlands, and Italy demonstrate particularly robust premium cigar demand, supported by wealthy consumer demographics and cultural associations between premium cigars and sophisticated leisure activities.

Premium cigars command substantially elevated price points enabling higher per-unit margins supporting manufacturer investments in product development, marketing, and regulatory compliance. The Mass-Market Cigar segment represents approximately 42% of market revenue, experiencing slower growth driven by escalating taxation, regulatory compliance costs, and consumption volume constraints among price-sensitive consumer segments.

Flavor Analysis

The Flavored Cigarillos segment represents the fastest-growing category, expanding at exceptional rates as manufacturers capitalize on regulatory gaps enabling flavored cigarillos where flavored cigarettes face comprehensive prohibitions under European Tobacco Products Directive. Flavored cigars and cigarillos now represent over 50% of total market consumption, growing approximately 50% since 2008, with fruit flavors commanding approximately 35% of total flavored product demand. Mint, coffee, and chocolate flavors represent secondary flavor categories with meaningful market penetration.

The Unflavored Cigarillos segment maintains approximately 50% of market share, representing traditional consumer preferences and core customer base demonstrating stable consumption patterns. Younger European consumers demonstrate strong preferences for flavored variants, while mature consumers favor unflavored traditional products.

Sales Channel Analysis

The Specialty Stores channel is the dominant retail distribution mechanism for European cigars and cigarillos, accounting for approximately 38% of total market sales through dedicated cigar retail establishments that offer specialized expertise, extensive product selection, and sophisticated retail environments that support premium positioning. Specialty retailers provide expert consultation, product recommendations, and experiential services, including cigar lounge facilities, humidification systems, and consumption education, justifying premium positioning and customer loyalty.

Duty-Free Shops account for approximately 22% of market share, capturing affluent international travelers through airport and cruise terminal retail locations that offer price-advantaged purchasing and premium product access. Online Retail is the fastest-growing sales channel, expanding at an 8.8% CAGR and currently capturing approximately 18% of market sales as digital commerce infrastructure matures. Hypermarkets/Supermarkets, Convenience Stores, and Other Channels collectively represent the remaining market share.

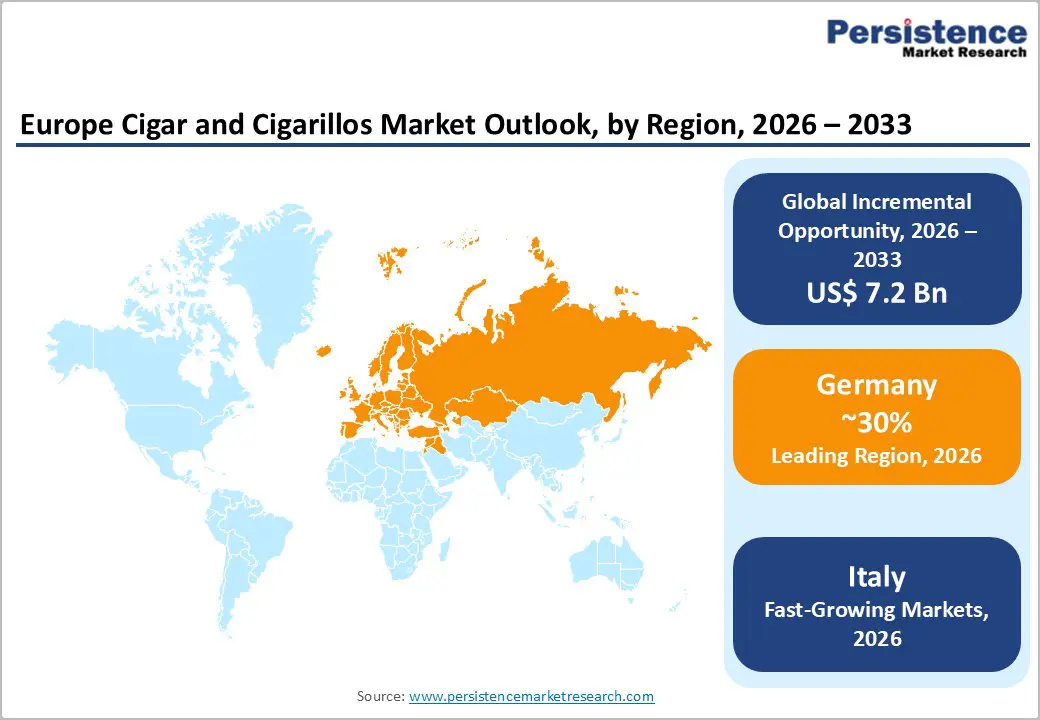

Germany Cigar and Cigarillos Trends

Germany is widely regarded as the largest cigar and cigarillos market in Europe, accounting for around 30% of the regional value share in 2026, owing to its scale, purchasing power, and a deeply entrenched cigar culture. The market benefits from a large adult smoking population and a strong tradition of both premium cigar appreciation and everyday cigarillo consumption. German consumers exhibit a dual-tier demand structure: high-income consumers favor imported hand-rolled cigars from Latin America, while a broader base supports steady volumes of machine-made cigarillos for regular use.

A highly developed retail ecosystem, including specialist tobacconists, cigar lounges, and duty-free outlet enhances accessibility and brand visibility. Although regulatory pressures from the European Union apply uniformly across member states, Germany’s higher disposable incomes and resilient premium segment help offset volume pressures. Premiumization, limited editions, and heritage branding continue to support value growth, reinforcing Germany’s role as the anchor market for Europe’s cigar and cigarillos industry.

France Cigar and Cigarillos Trends

France represents a mature but resilient cigar and cigarillos market, characterized by steady consumption rather than rapid expansion. Historically, France has ranked among Europe’s leading cigar consumers, supported by a strong café culture and an appreciation for leisure-oriented smoking experiences. However, growth is increasingly constrained by high tobacco taxation, strict advertising rules, plain packaging mandates, and rising health awareness, which collectively limit new consumer entry. While overall smoking prevalence is gradually declining, premium cigars and hand-rolled products continue to perform well, particularly among affluent urban consumers.

Specialist tobacconists and cigar lounges play a critical role in sustaining demand, even as mass-market cigarillo volumes stagnate. As a result, France occupies a stagnant-to-moderate growth position, balancing stable demand from loyal consumers with limited upside for expansion. The market’s future trajectory is expected to rely more on value growth through premiumization rather than volume increases, making France a textbook example of a steady, mature European market.

Italy Cigar and Cigarillos Trends

Italy is widely recognized as the fastest growing cigar and cigarillos market in Europe, driven by a unique blend of cultural heritage, premiumization, and expanding lifestyle consumption. The country has a long-standing cigar tradition, most notably with iconic domestic products such as Toscano cigars, which provides a strong foundation for consumer loyalty and cultural relevance. In recent years, growth has accelerated as interest in premium and artisanal cigars, including hand-rolled and small-batch offerings, has increased.

Italian consumers increasingly associate cigar smoking with socializing, gastronomy, and leisure, attracting younger adults compared to other mature European markets. Expansion of specialty retail outlets, cigar lounges, and tourism-linked sales further supports demand. Compared with northern European markets, Italy also shows greater openness to experimentation and brand storytelling, benefiting both local and international producers.

The European cigar and cigarillos market exhibits moderate consolidation with dominance by established multinational tobacco companies including Imperial Brands plc, British American Tobacco, Swedish Match AB, and Philip Morris International leveraging global distribution networks, brand portfolios, and financial resources supporting market expansion. Specialized premium cigar manufacturers including Scandinavian Tobacco Group, and OETTINGER DAVIDOFF maintain competitive positions through specialized expertise, heritage branding, and premium product differentiation.

Competitive strategies emphasize brand portfolio diversification across mass-market and premium segments, strategic product innovation including flavored variants and limited editions, and channel expansion through digital retail and duty-free partnerships. Market leaders invest substantially in regulatory compliance infrastructure, supply chain transparency systems, and sustainability initiatives supporting brand differentiation and premium positioning. Emerging regional manufacturers and smaller specialized producers maintain competitive positions through niche focus, heritage branding, and direct-to-consumer digital strategies.

Key Market Developments

The Europe Cigar and Cigarillos market is projected to reach US$ 17.0 billion by 2033, growing from US$ 9.8 billion in 2026 at a CAGR of 8.2%, driven by escalating premium cigar demand, flavored cigarillos expansion, and online retail channel development.

Primary demand drivers include premium cigar premiumization with 6.4% CAGR growth among affluent consumers treating cigars as luxury status symbols, flavored cigarillos expansion with approximately 50% sales growth since 2008 representing over 50% of market consumption, cigarillos offering regulatory alternatives to banned flavored cigarettes, online retail expansion at 7.38% CAGR, and rising disposable incomes supporting luxury consumption patterns across European markets.

Premium cigars represent the dominant segment with approximately 58% market share, expanding at 6.4% CAGR as affluent European consumers demonstrate continued preference for luxury products resistant to economic pressures, with German, Spanish, and French markets demonstrating particularly robust premium demand.

Germany leads the global cigar and cigarillos market with approximately 30% regional market share, supported by established premium cigar lounge culture, wealthy consumer demographics, robust domestic premium production, and strong celebratory consumption occasions driving sustained premium demand expansion.

Online retail expansion represents the principal market opportunity, expanding at 8.8% CAGR through sophisticated digital commerce platforms offering enhanced age-verification systems, expanded product selection, experiential content, and discretionary purchasing convenience appealing to affluent European consumers across diverse geographic markets.

| Report Attributes | Details |

|---|---|

| Historical Data/Actuals | 2020 - 2025 |

| Forecast Period | 2026 - 2033 |

| Market Analysis Units | Value: US$ Mn Volume: Units |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights | Market Forecast and Trends, Competitive Intelligence & Share Analysis, Growth Factors and Challenges, Strategic Growth Initiatives, Pricing Analysis & Technology Roadmap, Future Opportunities and Revenue Pockets, Market Analysis Tools |

By Product Type

By Flavor

By Sales Channel

By Country

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author