- Industrial Goods & Service

- Waste Management Equipment Market

Waste Management Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Waste Management Equipment Market By Equipment Type (Trucks, Compactors, Dumpsters, Screeners, Conveyors, Shredders, Others), Waste Type (Hazardous Waste, Non-Hazardous Waste), Application (Industrial Waste, Municipal Waste, Others), and Regional Analysis for 2025 - 2032

Waste Management Equipment Market Share and Trends Analysis

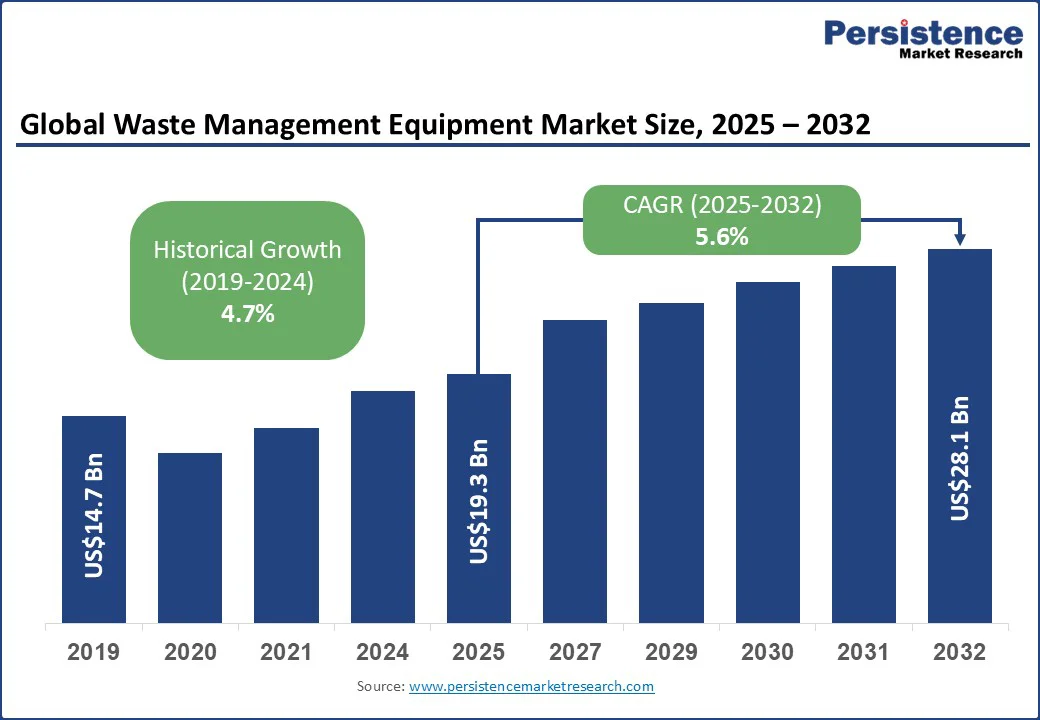

The global waste management equipment market size is likely to be valued at US$19.3 billion in 2025, and is estimated to reach US$28.1 billion by 2032, growing at a CAGR of 5.6% during the forecast period 2025−2032, driven primarily by increasing urbanization and stringent environmental regulations worldwide.

This growth is supported by accelerating demand for efficient waste collection and recycling systems amid rising municipal and industrial waste generation, combined with continuous technological innovation in equipment design, enhancing operational efficiency.

Government initiatives targeting sustainable waste handling and increased private sector investments in waste recycling modernization underpin this upward trajectory, shaping a resilient market environment for equipment manufacturers and service providers.

Key Industry Highlights

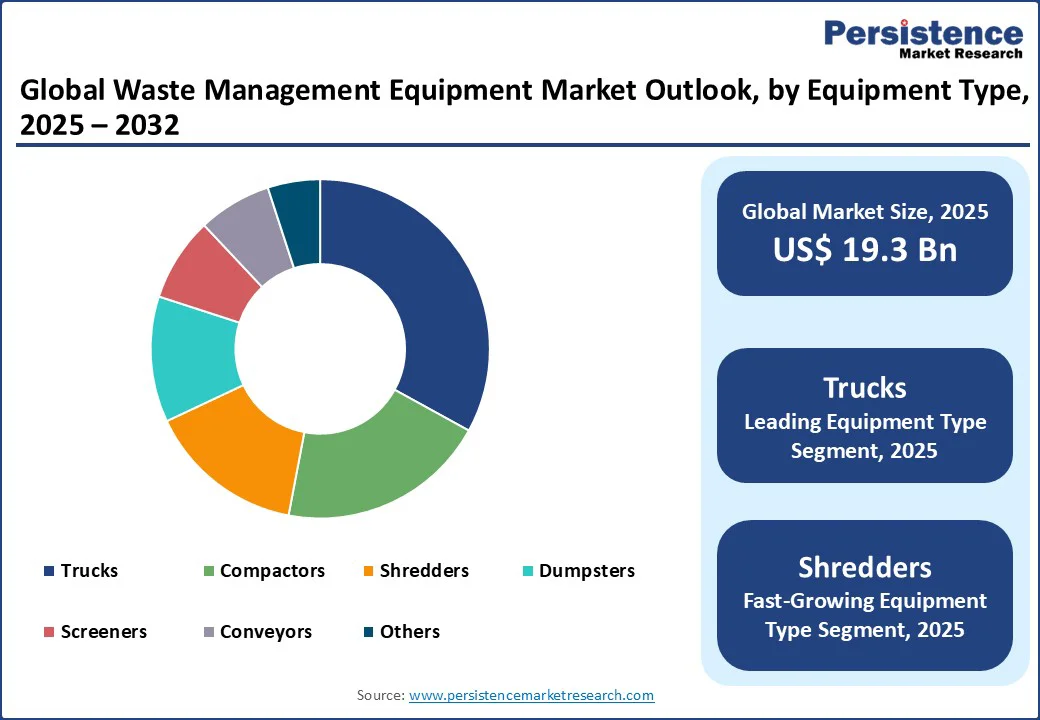

- Dominant & Fastest-growing Equipment Types: Trucks are set to dominate with a share of around 35% in 2025; shredders are the fastest-growing equipment type through 2032, driven by increasing recycling demands.

- Leading & Fastest-growing Applications: Municipal waste is expected to lead with approximately a 60% market share in 2025, while the industrial waste segment is projected to grow fastest during 2025-2032.

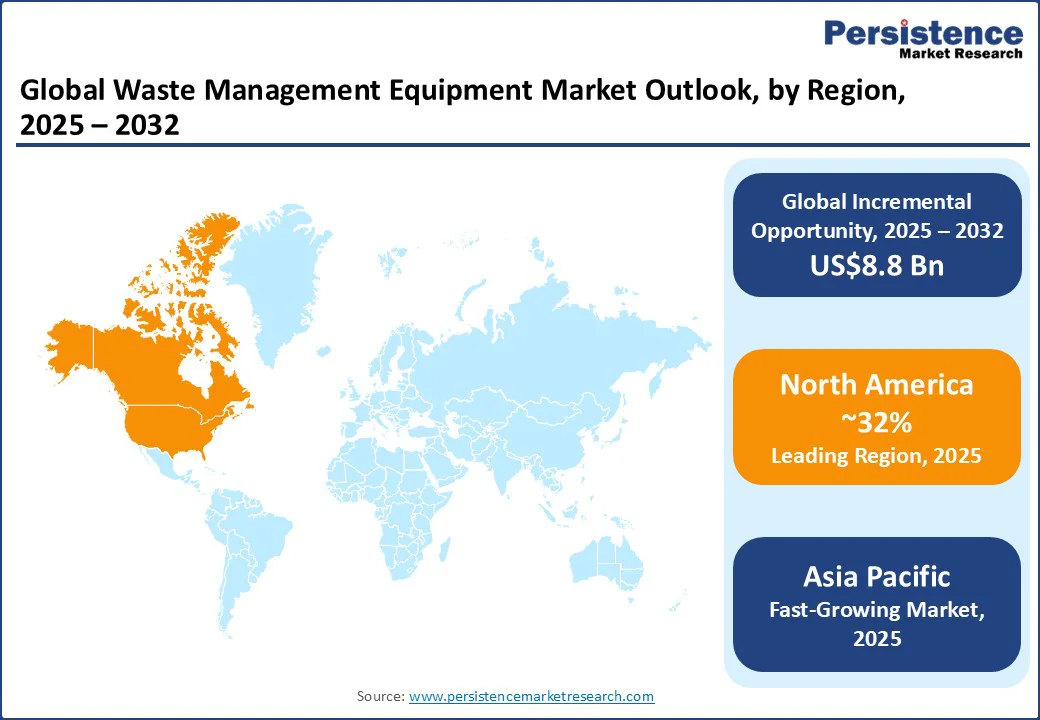

- Dominant Region: North America is expected to hold a 32% market share in 2025, driven by robust waste disposal regulations.

- Fastest-growing Regional Market: Asia Pacific is the fastest-growing regional market, owing to rapid urbanization and massive municipal waste generation.

- Strategic Initiatives include emission-reducing trucks, AI-enabled sorting acquisitions, and IoT partnerships that enhance operational intelligence.

- September 2025: ZenRobotics and U.S. Conveyor secured a repeat order to boost metal recovery using AI-powered robots in legacy recycling systems.

| Key Insights | Details |

|---|---|

|

Waste Management Equipment Market Size (2025E) |

US$19.3 Bn |

|

Market Value Forecast (2032F) |

US$28.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Unprecedented Generation of Urban Waste

Urban population growth has led to a significant increase in waste production, compelling municipalities to continually upgrade their waste management infrastructure. According to the World Bank, global urban waste generation is expected to increase from 2.01 billion tons in 2016 to 3.4 billion tons by 2050. This surge necessitates the deployment of efficient collection trucks, compactors, and sorting equipment to handle the volume and complexity of waste streams.

The growing middle class in the Asia Pacific and Latin America is also increasing consumer waste generation, creating novel operational challenges and demands. Enterprises investing strategically in scalable and technologically advanced equipment are poised to capitalize on volume-driven market expansion, particularly in regions where municipal budgets align with infrastructure modernization mandates.

To tackle the huge volumes of waste, governments worldwide are implementing increasingly rigid regulations targeting waste reduction and proper disposal. For instance, the European Union's (EU) Circular Economy Action Plan mandates enhanced recycling and reuse of materials by 2030, supporting waste diversion from landfills. Similarly, the U.S. Environmental Protection Agency (EPA) continues to enforce standards aimed at reducing landfill dependence and emissions from incineration. These policies are driving the demand for advanced waste management equipment, such as compactors and advanced sorting systems, elevating operational requirements for collection and processing.

Fragmented Regulatory Landscape and Compliance Complexity

The market growth is hindered by a fragmented and evolving regulatory landscape across regions. Disparate standards and enforcement levels complicate product development, increase certification costs, and extend time-to-market for manufacturers. While North America and Europe enforce strict emissions and safety standards, many emerging markets lack clearly defined or consistently applied regulations, which challenge global players aiming for scalable, compliant product portfolios.

Frequent regulatory updates further burden manufacturers, requiring constant product redesign and retesting, which strains R&D budgets and slows innovation deployment. Although waste management equipment supports environmental sustainability, its production and end-of-life processes carry significant ecological footprints. High energy use in steel and electronics manufacturing, and the limited recyclability of certain components, raise sustainability concerns.

As regulations increasingly focus on lifecycle emissions, manufacturers must adopt eco-design and circular economy principles, which can increase production complexity and cost. These factors can impact pricing competitiveness and delay widespread market adoption, creating operational and reputational risks.

Development of Circular Economy and Extended Producer Responsibility (EPR) Programs

Emerging and expanding circular economy policies worldwide present significant growth avenues for waste management equipment suppliers. Extended producer responsibility (EPR) regulations require manufacturers and importers to manage post-consumer waste, thereby increasing demand for advanced recycling and sorting technologies. Markets such as the EU are enhancing EPR scopes to include plastics and electronics, with compliance deadlines approaching. This regulatory thrust is driving municipal and commercial investments in state-of-the-art recycling infrastructure, including optical sorters, grinders, and compactors, which enable higher recovery rates and improved material quality. Equipment providers capable of customizing solutions to align with evolving EPR frameworks can capture lucrative contracts and long-term service agreements, positioning themselves as integral partners in circular value chains.

The growing complexity and scale of waste challenges are also stimulating increased private sector involvement via public-private partnerships (PPPs) and outsourcing models globally. Governments are leveraging private expertise and capital to upgrade waste management infrastructure and expand service coverage, especially in rapidly urbanizing regions.

PPP arrangements facilitate risk-sharing, innovation incentives, and enhanced operational efficiencies through the deployment and maintenance of specialized equipment. Market players with comprehensive service offerings encompassing advanced equipment supply and operational performance guarantees stand to gain substantial competitive advantages.

Category-wise Analysis

Equipment Type Insights

The trucks segment remains the cornerstone of the market, accounting for about 33% of the market share in 2025. Their integral role in waste transport pipelines across municipal and commercial settings sustains steady demand. Technological enhancements, such as automated bin-lifting mechanisms and real-time tracking systems, ensure productivity and regulatory compliance, thereby reinforcing segment dominance. The growing emphasis on environmental sustainability is prompting electrification efforts within fleet vehicles, opening avenues for innovation and market disruption.

Shredders, in contrast, are rapidly expanding, driven by increased demands for sorting efficiency to segregate recyclable materials from mixed waste streams, thereby lowering landfill dependency and improving downstream processing. Technical advancements, including sensor-based sorting and modular designs, are enhancing throughput and adaptability, thereby enticing investments from recycling centers and waste-to-energy operators. While compactors maintain a strong market position due to their volume reduction capabilities, the intersection of sorting and compacting functionality is emerging as a key focus for innovation.

Waste Type Insights

Non-hazardous waste equipment is expected to continue dominating the market, with a roughly 68% market share in 2025, reflecting the volume dominance of municipal solid waste, commercial refuse, and similar sources. Growth in this segment is largely driven by urban population influxes and evolving municipal waste management policies that mandate higher recycling and composting rates. The segment also benefits from relatively stable investment cycles and broad application scopes.

Hazardous waste equipment is expected to grow at a robust forecast CAGR through 2032, driven by increasing regulatory scrutiny on medical, chemical, and electronic waste streams. Heightened public and insurer focus on environmental and health impacts is stimulating upgrades in secure collection trucks, sealed compactors, and specialized shredders. These trends accentuate segmentation and procurements for safety-optimized machinery with compliance certification, reinforcing growth potential amid tightening hazard protocols.

Application Insights

The municipal waste segment is expected to secure around 58% of the revenue share in 2025, primarily driven by the expansion of urban waste volumes, which necessitate systematic collection, sorting, and disposal infrastructure. Municipal investments in smart city initiatives and waste-to-resource projects further fuel equipment modernization. The evolving focus on sustainability, including bans on single-use plastics and the diversion of organic waste, is sharpening municipal equipment demand profiles.

Industrial waste applications exhibit one of the fastest growth trajectories for the 2025-2032 period. Industrialization, particularly in the Asia Pacific and Latin America, coupled with increasing corporate sustainability commitments and environmental compliance mandates, is propelling this segment. The demand for heavy-duty shredders, grinders, and compactors designed to manage a diverse range of industrial waste types is rising sharply, driven by regulatory fines and reputational risks associated with mismanagement. Industry-specific customization and service integration provide competitive differentiation in this expanding segment.

Regional Insights

North America Waste Management Equipment Market Trends

North America is poised to capture an estimated 32% of the market share in 2025, driven by the well-established waste infrastructure and progressive legislative framework of the U.S. The regional market is experiencing steady growth, driven by EPA initiatives that emphasize landfill reduction and resource recovery, and supported by increasing municipal budgets earmarked for infrastructure revitalization.

The U.S. innovation ecosystem, facilitated by collaborations between equipment manufacturers and technology firms, is rapidly transitioning fleets to electrification and integrating AI-powered sorting solutions, fostering operational excellence. Investment activity includes significant public-private partnerships to finance modernization projects in large metropolitan areas, enhancing market resilience amid evolving sustainability drivers. Competitive intensity remains elevated, with incumbents leveraging digital transformation and after-sales services to maintain leadership.

Europe Waste Management Equipment Market Trends

Europe is forecast to stabilize at around a 27% market share in 2025, spearheaded by Germany, France, the U.K., and Spain, which collectively enforce harmonized regulatory policies under the European Green Deal. The EU prioritizes circular economy principles, mandating higher recycling rates and incentivizing waste-to-energy projects, which are supported by substantial public funding.

This growth is supported by increasing public acceptance of smart waste systems and investments in automated sorting facilities that utilize cutting-edge optical sorters and AI technologies. Market dynamics are characterized by strategic mergers among equipment providers aimed at consolidating technological capabilities and geographic reach. The regulatory emphasis on reducing greenhouse gas emissions and extending adherence timelines contextualizes equipment demand patterns, fostering sophisticated market segmentation.

Asia Pacific Waste Management Equipment Market Trends

The Asia Pacific is the fastest-growing regional market for recycling infrastructure, driven by substantial fiscal incentives. India and Southeast Asia are following suit, spurred by growing environmental awareness and the integration of international best practices. Manufacturing hubs within the region supply cost-competitive equipment domestically and internationally, enhancing market accessibility and shaping competitive dynamics.

The regulatory environment is undergoing modernization, with increasing enforcement and alignment with global environmental standards anticipated. Foreign direct investment and joint ventures between local and multinational companies underscore expansion and innovation prospects in the region.

Competitive Landscape

The global waste management equipment market is moderately consolidated, with the top five players accounting for an estimated 45% share. Leading companies such as Hino Motors, Volvo Group, Caterpillar Inc., Komatsu Ltd., and Terex Corporation dominate through diversified portfolios ranging from collection trucks to specialized sorting systems.

Market concentration enables scale economies and R&D investments while allowing space for niche players focusing on technology innovation. Competitive positioning is driven by product development velocity, after-sales services, and geographic expansion strategies, requiring continuous adaptation by suppliers to evolving customer and regulatory demands.

Key Industry Developments

- In August 2025, Declaration Partners acquired a majority stake in CP Group, aiming to boost innovation, automation, and AI-driven efficiency in waste sorting.

- In May 2025, TANA launched the Hammerhead, a high-capacity mobile shredder that processes solid waste up to 50% faster than previous models. Featuring a 40 rpm rotor, high torque, and advanced control systems based on Shark technology, it’s available in mobile and stationary versions with diesel or electric options. The design ensures lower emissions, flexible operation, and simplified maintenance through shared components with other TANA models.

- In April 2025, Sebright Products Inc. partnered with Germany’s H&G Unternehmensgruppe to become the exclusive North American distributor of H&G’s auger compactors and select waste equipment. The collaboration merges H&G’s advanced technology with Sebright’s service excellence to boost waste disposal efficiency, cut transport costs by 50%, and support sustainability goals.

Companies Covered in Waste Management Equipment Market

- Hino Motors, Ltd.

- Volvo Group

- Caterpillar Inc.

- Komatsu Ltd.

- Terex Corporation

- Linde plc

- Faun GmbH & Co.

- Hitachi Construction Machinery Co., Ltd.

- John Deere

- JCB Ltd.

- Doosan Infracore

- Greenstar Recycling Technologies

- New Way Trucks

- Bearcat Manufacturing, Inc.

- Liebherr Group

Frequently Asked Questions

The global waste management equipment market is projected to reach US$19.3 Billion in 2025.

Surging urbanization, stringent environmental regulations worldwide, and rising municipal and industrial waste generation are driving the market.

The waste management equipment market is poised to witness a CAGR of 5.6% from 2025 to 2032.

Continuous technological innovation in equipment design, enhancing operational efficiency, government initiatives targeting sustainable waste handling, and increased private sector investments in waste recycling modernization are key market opportunities.

Hino Motors, Ltd., Volvo Group, and Caterpillar Inc. are some of the key players in the waste management equipment market.