- Industrial Machinery

- Pumps Market

Pumps Market Size, Share, and Growth Forecast, 2025 - 2032

Pumps Market By Product Type (Centrifugal Pumps, Positive Displacement Pumps), Operation Mode (Electrical, Mechanical), End-user Industry (Oil & Gas, Water & Wastewater Management, Mining, Agriculture, Chemicals & Petrochemicals, Others), and Regional Analysis for 2025 - 2032

Pumps Market Share and Trends Analysis

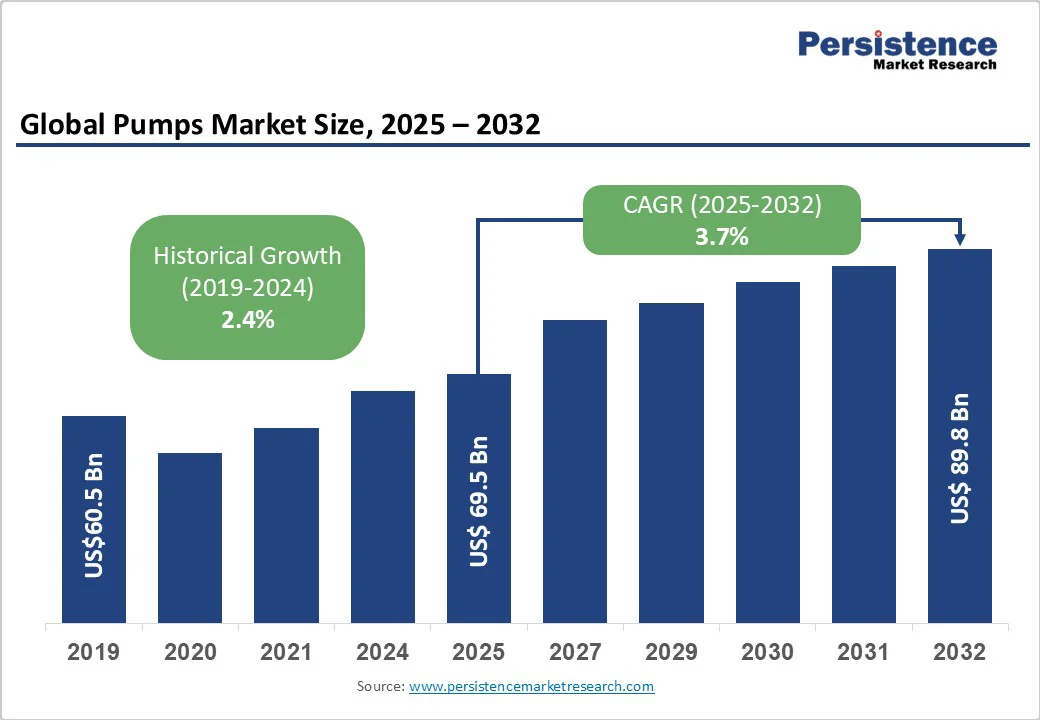

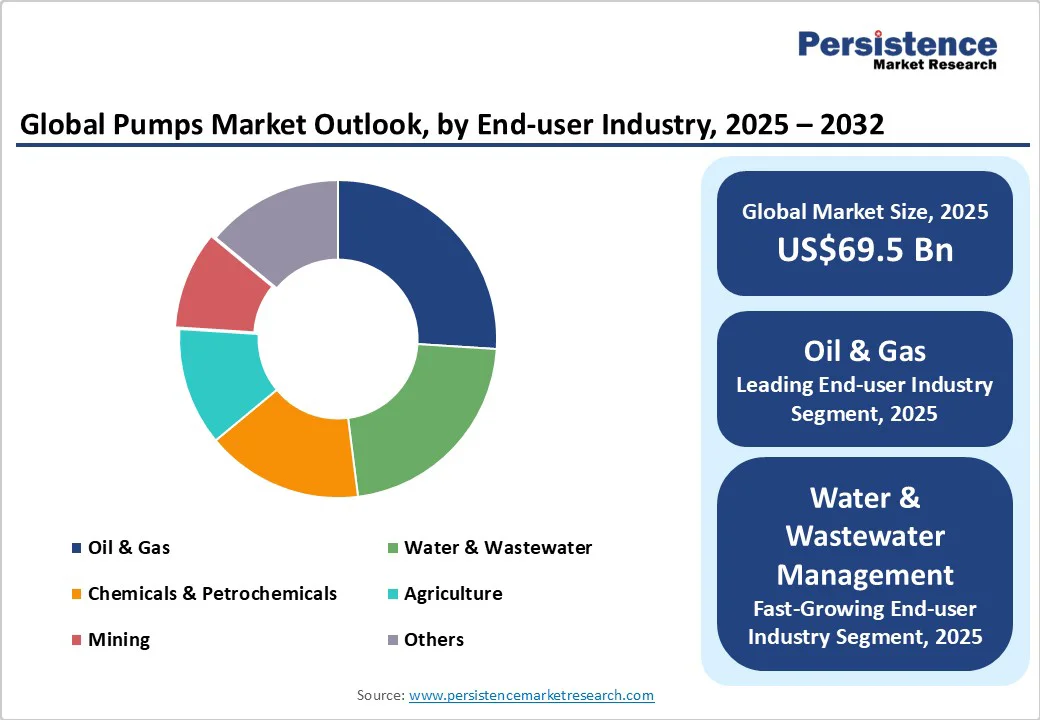

The global pumps market size is likely to be valued at US$69.5 Billion in 2025, and is estimated to reach US$89.8 Billion by 2032, growing at a CAGR of 3.7% during the forecast period 2025−2032, driven primarily by rising industrial automation and increasing infrastructure development worldwide. Market expansion is fueled by technological innovations that improve pump efficiency and regulatory pressures favoring energy-saving equipment. Key sectors such as oil & gas, water and wastewater, and chemical industries are playing a central role in keeping demand steady.

Key Industry Highlights

- Leading & Fastest-growing Product Types: Centrifugal pumps will maintain market leadership with roughly 64% share in 2025, while positive displacement pumps are set to grow the fastest at about 4.5% CAGR through 2032.

- Dominant & Fastest-growing End-user Industries: The oil & gas industry is slated to dominate with a 26% estimated market share in 2025, whereas water & wastewater management is the fastest-growing end-use sector, projected to post a CAGR of around 5% during 2025-2032.

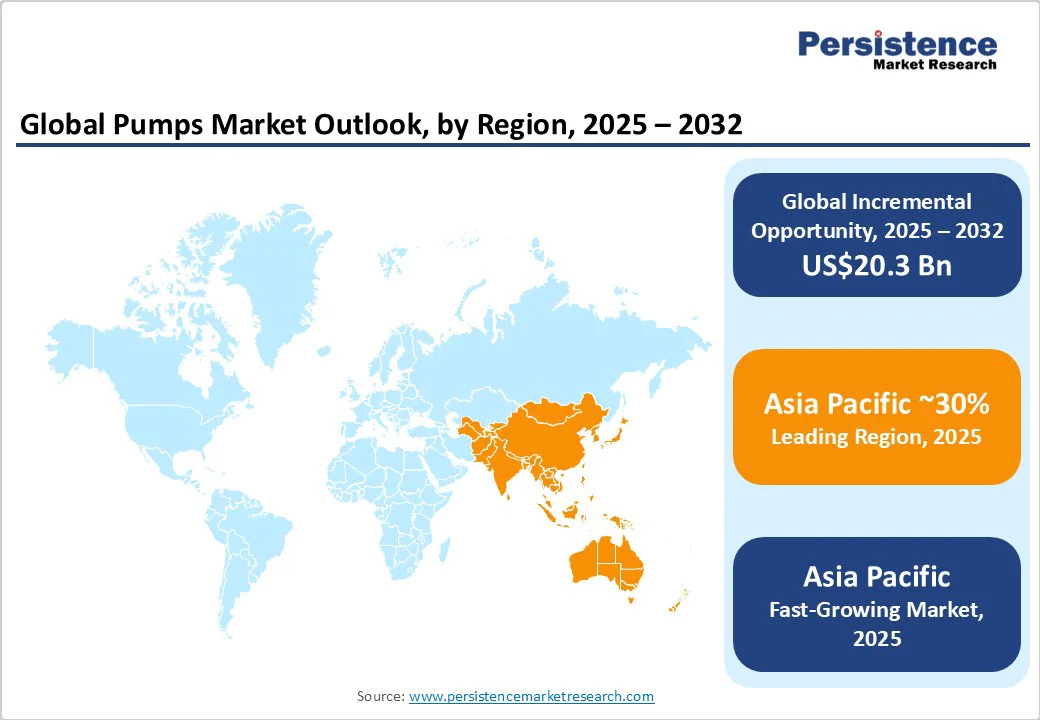

- Leading & Fastest-growing Regions: Asia Pacific is anticipated to lead with approximately 30% market share in 2025, and is also poised to exhibit the highest CAGR through 2032, driven by infrastructure modernization and manufacturing advantages.

- Dominating Segment by Operating Mode: Electrical pumps are predicted to dominate with a 72% market share estimated for 2025, whereas mechanically driven pumps will grow fastest at nearly 3.8% CAGR, serving off-grid needs.

- June 2025: EVHACS and Mitsubishi Electric collaborated to develop the world’s first combined electric vehicle (EV) charger and heat pump solution, aiming to optimize energy efficiency by simultaneously managing EV charging and building heating or cooling needs.

| Key Insights | Details |

|---|---|

|

Pumps Market Size (2025E) |

US$69.5 Bn |

|

Market Value Forecast (2032F) |

US$89.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Automation Generating Massive Demand for Pumps

Rapid industrialization in emerging and developed economies continues to fuel the demand for automated pumping solutions. Pumps optimized for process control, such as variable frequency drive (VFD) enabled centrifugal pumps, are increasingly replacing conventional units, primarily driven by efficiency and reliability requirements. According to the International Federation of Robotics, industrial robot installations increased by 10% in 2024 alone, highlighting automation adoption that indirectly boosts pump deployment in manufacturing and processing plants. This trend is particularly notable in the oil & gas sector, where technological upgrades aim to reduce downtime and enhance productivity, directly elevating demand for advanced pumping systems.

Governments worldwide are implementing stricter energy consumption and emission policies, compelling industries to adopt resource-optimized technology. The U.S. Department of Energy estimates that pumps consume approximately 20% of electrical energy in the industrial sector, making them a critical focus area for energy conservation. Regulations such as the Ecodesign Directive of the European Union (EU) mandate minimum efficiency performance standards (MEPS) that pump manufacturers must meet, incentivizing innovation. Energy-efficient pump technologies, including electronically commutated motors (ECM) and precision impeller designs, are therefore witnessing heightened demand.

Prohibitive Upfront Expenditure Inhibiting Adoption among SMEs

Initial procurement and installation costs of advanced pump systems remain significant barriers, particularly for small and medium enterprises (SMEs). High upfront investment cost relative to conventional pumps slows adoption in price-sensitive segments, especially in developing economies where budget allocation for capital expenditures is constrained. According to surveys by the International Finance Corporation (IFC), over 60% of SMEs in emerging markets prioritize cost over operational efficiency when choosing equipment. Consequently, market penetration of premium energy-efficient and smart pumps is limited in these demographics, which constrains overall market growth despite long-term operational savings potential.

Furthermore, recent geopolitical tensions, pandemic-related logistics challenges, and raw material price volatility are disrupting the global supply chain for pump components. Critical raw materials such as stainless steel and rare earth elements used in advanced motor manufacturing have faced shortages and price surges of up to 15%-20% since 2023, affecting production costs and timelines. These challenges have prolonged manufacturer lead times, reduced flexibility in meeting sudden demand spikes, and posed risks to just-in-time supply models dominant in industrial sectors. Extended shipping durations and cost increases for freight exacerbate final product pricing, lowering competitiveness, especially for exporters targeting emerging markets.

Urban Infrastructure Investments in Developing Markets to Open New Business Avenues

The unprecedented rate of urbanization, along with government-led infrastructure initiatives, is expanding pump demand in the developing economies of Asia Pacific, Latin America, and parts of Africa. The Asian Development Bank (ADB) projects over US$1 Trillion in infrastructure spending in Asia alone between 2025 and 2030, targeting water supply, wastewater treatment, and energy sectors where pumps are essential. These investments are likely to create sizable market opportunities. Critical unmet needs include affordable, reliable, and energy-efficient water management pumps to cater to expanding municipal populations. Penetration of localized and modular pumping solutions tailored to infrastructural challenges presents actionable growth potential for market players willing to innovate and customize.

On the technology front, pumps embedded with IoT connectivity, predictive maintenance, and remote operation features are rapidly transforming the market landscape. Smart pumps are being widely deployed across key sectors such as oil & gas, power generation, and chemical processing. Digitalized pumping solutions enable real-time performance monitoring, fault detection, and energy optimization, addressing critical operational challenges and reducing downtime. Adoption is further accelerated by policy incentives promoting digital transformation in industrial equipment.

Category-wise Analysis

Product Type Insights

Centrifugal pumps are the prevailing product type in the market, projected to hold a dominant revenue share of approximately 64% by 2025. Their extensive adoption across numerous industries results from their operational advantages, including high efficiency at handling large liquid volumes, relatively simple mechanical design, and adaptability to various fluid types, particularly low-viscosity liquids. The continuous improvements in impeller designs, such as multi-blade and mixed-flow technologies, are enhancing energy efficiency and performance consistency, leading to increased preference in water treatment, oil & gas, chemical processing, and power generation sectors. The ability of centrifugal pumps to operate seamlessly with VFDs aligns with evolving automation needs, contributing to sustained market leadership.

In contrast, positive displacement pumps are forecasted to experience the fastest growth from 2025 to 2032. This growth is fueled by the growing demands in industries requiring precise flow control, including the pharmaceutical, food & beverage, and specialty chemical sectors. Recent advances in sealing technologies and composite materials have enabled positive displacement pumps to handle abrasive and viscous fluids more effectively, expanding their application scope. This segment's inherent capability to maintain a constant flow rate irrespective of pressure changes differentiates it in process-critical applications, positioning it for accelerated growth amidst increasingly stringent regulatory and quality requirements globally.

Operation Mode Insights

The electrical pumps segment is anticipated to secure the largest revenue share in 2025, commanding about 72% of the market. The driving force behind this dominance stems from widespread industrial electrification, strict regulatory policies promoting energy-efficient machinery, and technological progress enabling the integration of smart controls and variable-speed drives. Electrical pumps are preferred in modern facilities due to their superior energy management capabilities and ability to interface with automation systems, enhancing operational efficiency and reducing downtime. Public and private sector energy conservation initiatives across large economies, supported by government incentives, are accelerating the adoption of electrical pump systems, further consolidating their market position.

Mechanically operated pumps are expected to register the highest CAGR over the forecast period, sustaining relevance particularly in off-grid or remote applications where a stable electrical supply is limited or unreliable. Advances in fuel-efficient mechanical drive technologies, including hybrid configurations combining mechanical and electrical systems, are expanding their utility across mining, agriculture, and certain chemical processing contexts. Emerging markets, where infrastructure development remains in progress, rely extensively on mechanically driven pumps due to lower dependency on electrical grids. These operational characteristics maintain a consistent demand base for mechanical pumps even as electrification advances, particularly within remote and developing regions.

End-user Industry Insights

The oil & gas industry is set to continue as the largest end-use segment for pumps, accounting for an estimated 26% share of the market in 2025. This dominance is attributable to the extensive use of pumps across upstream extraction, midstream transportation, and downstream refining operations, where handling chemically aggressive and multiphase fluids demands specialized pumping solutions. Ongoing exploration activities, depletion of mature fields necessitating enhanced recovery technologies, and regulatory mandates on emission controls sustain demand. The focus of the sector on reliability, safety, and environmental compliance promotes the adoption of technologically advanced pumps with corrosion-resistant materials and integrated monitoring systems, thereby supporting sustained market value and growth.

The water & wastewater management sector is identified as the fastest-growing end-use industry segment, projecting a high CAGR through 2032, due to rapid urbanization, increasing global demand for potable water, and reinforced regulatory frameworks on wastewater discharge standards. Investment surges in municipal infrastructure, particularly in Asia Pacific and parts of Latin America, underscore this growth, with governments expanding treatment facilities and water distribution networks. The demand for energy-efficient and smart pumping systems equipped with remote monitoring and preventive maintenance capabilities is intensifying to optimize operational costs and comply with sustainability agendas, making this segment highly attractive for future investments.

Regional Insights

Asia Pacific Pumps Market Trends

Asia Pacific is set to dominate the market with an approximate share of 30% in 2025, and is also likely to be the fastest-growing regional market, propelled by rapid urbanization, expansive infrastructure investments, and the expansion of manufacturing hubs in China, India, Japan, and ASEAN countries. Substantial government spending on clean water projects, energy infrastructure, and agricultural modernization is fueling demand for water treatment pumps, industrial centrifugal pumps, and irrigation systems.

China’s ongoing initiatives to upgrade aging water systems and India’s ambitious clean water access programs are key growth drivers alongside favorable demographics and increasing industrial activity. The regional market also benefits from manufacturing advantages, including lower labor and production costs, enabling competitive pricing and rapid scaling of pump supplies domestically and for export. Regulatory frameworks are evolving to incorporate energy efficiency and environmental protection, complementing technological adoption in both local and global enterprises. Investments focusing on capacity expansion, local R&D facilities, and digital transformation are highly active, enabling manufacturers to effectively target both mature and emerging use cases with tailored pump solutions to meet diverse regional needs.

North America Pumps Market Trends

North America is anticipated to dominate with approximately 28% of the market share in 2025. This leadership is largely driven by the U.S., which boasts a mature industrial base, advancements in automation, and a stringent regulatory environment emphasizing energy efficiency and environmental stewardship. Frameworks such as the U.S. Energy Policy Act and initiatives of the Environmental Protection Agency (EPA) are catalyzing upgrades to existing pumping infrastructure with energy-efficient technologies. The technological innovation ecosystem of North America, complemented by robust government investments in water infrastructure, smart city projects, and oil & gas modernization, provides a competitive advantage to manufacturers operating in the region.

The regulatory environment here incentivizes retrofit projects and the incorporation of renewable energy-powered pumping systems, further driving market expansion. Regional competitive dynamics are shaped by key multinational players focusing on technology leadership and sustainability commitments, with enhanced investments in digital service platforms for predictive maintenance and asset management reflecting an integration of hardware and software for comprehensive client solutions.

Europe Pumps Market Trends

Europe is forecasted to hold approximately 25% market share in 2025, led by industrial powerhouses such as Germany, the U.K., France, and Spain. These countries are characterized by established manufacturing sectors and harmonized regulatory regimes under the EU that enforce standardized energy efficiency and emissions targets, as well as circular economy principles. Such regulatory coherence facilitates smoother market operations and accelerates the adoption of cutting-edge, green pump technologies.

Germany’s significant capital investments in renewables and wastewater treatment plants drive sectoral demand for pumps, while the U.K.’s emphasis on resilient water infrastructure upgrades complements this dynamic. Cross-border collaboration within the EU facilitates technological diffusion and innovation, benefiting manufacturers and end-users alike. The competitive landscape in Europe blends multinational corporations with specialized niche players that focus on application-specific pumps, particularly catering to high-purity and chemical processing needs. Investment focus is increasingly directed toward the digitalization of pump systems, combining enhanced monitoring and maintenance capabilities to align with evolving environmental and operational efficiency standards.

Competitive Landscape

The global pumps market structure is moderately consolidated, with leading players collectively accounting for an estimated 50% of the overall market revenue. Major multinationals such as Xylem Inc., Grundfos Holding A/S, Flowserve Corporation, KSB SE & Co. KGaA, and Sulzer Ltd. hold dominant positions driven by extensive product portfolios, global reach, and technological innovation capabilities.

Market concentration differs by region; North America and Europe are more consolidated, while Asia Pacific is fragmented. Competitive advantages stem from innovation, quality, and sustainability. New entrants target niche or digitalized offerings, using strategic integration to challenge established players.

Key Industry Developments

- In October 2025, MHI Thermal Systems launched the ETI-W centrifugal heat pump, delivering 90°C hot water using industrial waste heat. With 640?kW capacity, low-GWP refrigerant, and compact design, it boosts energy efficiency and reduces CO? emissions in industrial settings.

- In September 2025, Jetson introduced the Jetson Air, a smart home heat pump system offering one-day installation at half the typical cost. It integrates with existing ductwork, features real-time monitoring, and optimizes efficiency via software, reducing energy use and emissions.

- In August 2025, Lumo launched a Pump Automation feature within its smart valve platform, enabling specialty crop growers to automate irrigation from pump to plant. It improves scheduling, reduces labor, minimizes risks, and enhances crop yield and quality by leveraging real-time data.

Companies Covered in Pumps Market

- Xylem Inc.

- Grundfos Holding A/S

- Flowserve Corporation

- KSB SE & Co. KGaA

- Sulzer Ltd.

- Pentair plc

- Ebara Corporation

- Atlas Copco AB

- Weir Group PLC

- SPX FLOW, Inc.

- Torishima Pump Mfg. Co., Ltd.

- Ingersoll-Rand plc

- Dover Corporation

- Franklin Electric Co., Inc.

- Flowrox Oy

Frequently Asked Questions

The global pumps market is projected to reach US$69.5 Billion in 2025.

Rising industrial automation, increasing infrastructure development worldwide, and regulatory pressures favoring energy-saving equipment are driving the market.

The pumps market is poised to witness a CAGR of 3.7% from 2025 to 2032.

Technological innovations that improve pump efficiency, growing adoption of smart pumps, and environmental regulations aimed at reducing carbon footprint are key market opportunities.

Xylem Inc., Grundfos Holding A/S, and Flowserve Corporation are some of the key players in the pumps market.