- Industrial Machinery

- Mud Pumps Market

Mud Pumps Market Size, Share, and Growth Forecast 2026 - 2033

Mud Pumps Market by Product Type (Triplex Mud Pumps, Quintuplex Mud Pumps, Duplex Mud Pumps, Others), Power (Electric, Fuel Engines), Application (Onshore Drilling, Offshore Drilling, Others), End-User (Oil & Gas, Mining, Construction, Others), and Regional Analysis, 2026 - 2033

Mud Pumps Market Size and Trend Analysis

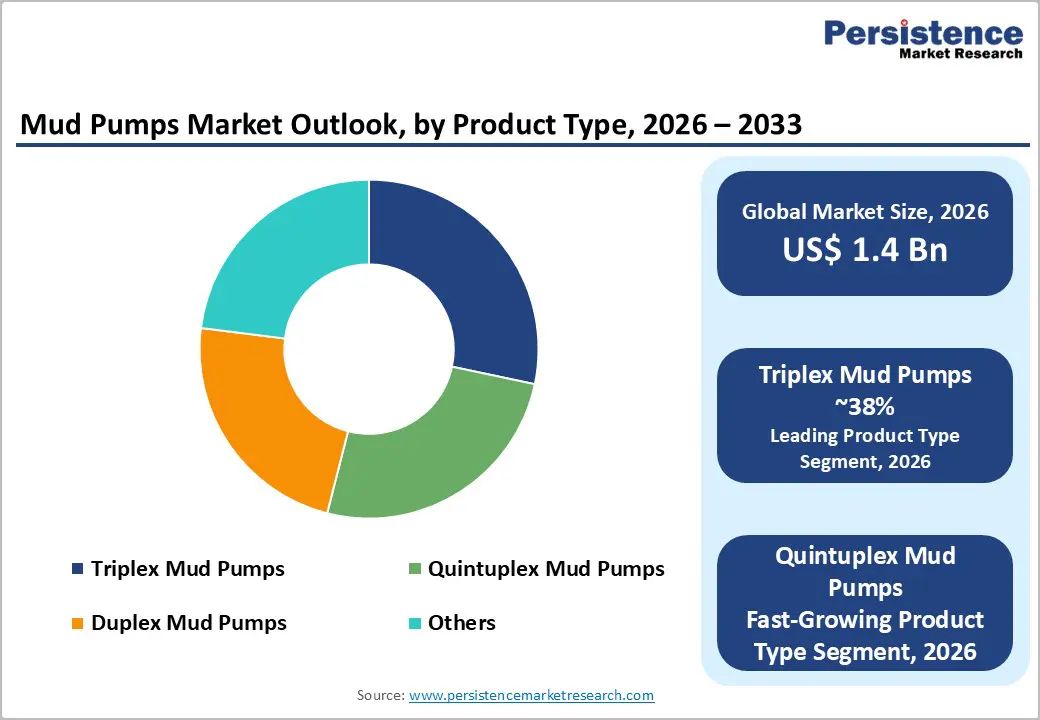

The global mud pumps market size is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. Rising global energy demand is accelerating oil and gas exploration activities, increasing the need for reliable and high-performance drilling equipment such as mud pumps. These pumps play a critical role in maintaining wellbore stability and efficient fluid circulation during drilling operations.

Growth is further supported by increasing rig efficiency, deeper and more complex wells, and ongoing technological upgrades. Notably, the U.S. Energy Information Administration (EIA) highlights record production levels despite lower rig counts, underscoring efficiency-driven adoption of advanced mud pump systems.

Key Market Highlights

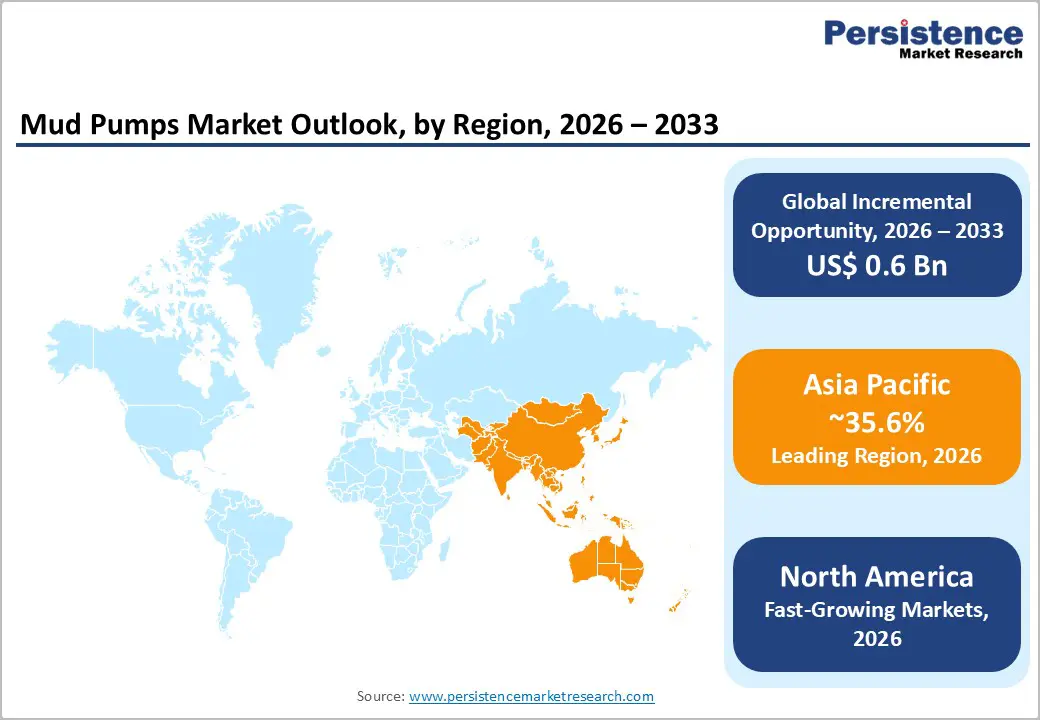

- Leading Region – Asia Pacific leads the Mud Pumps Market with 35.6% share in 2025, supported by strong oil & gas exploration in China and India and cost-efficient regional manufacturing.

- Second-Largest Region – North America holds 31.2% share in 2025, driven by U.S. shale drilling efficiency, advanced pump technologies, and a mature oilfield services ecosystem.

- Leading Product Category – Triplex Mud Pumps dominate the market with a 38% share in 2025, owing to their balanced three-piston design, high-pressure handling, and low maintenance needs.

- Fastest-Growing Product Category – Quintuplex Mud Pumps are the fastest-growing segment, gaining traction in deepwater and high-pressure drilling due to smoother flow delivery and superior operational stability.

- Leading End-user – The oil & gas sector accounts for 47.1% share in 2025, reflecting mud pumps’ critical role in upstream drilling and well construction activities.

- Key Growth Opportunity – Electric mud pumps present a major opportunity as operators shift toward electrified rigs and low-emission systems to meet ESG and regulatory requirements.

| Key Insights | Details |

|---|---|

|

Mud Pumps Size (2026E) |

US$ 1.4 Billion |

|

Market Value Forecast (2033F) |

US$ 2.0 Billion |

|

Projected Growth CAGR(2026-2033) |

5.3% |

|

Historical Market Growth (2020-2025) |

4.9% |

Market Dynamics

Drivers - Rising Oil and Gas Exploration and Drilling Activities Worldwide

Intensifying global oil and gas exploration continues to be a primary driver for the mud pumps market, as these systems are critical for circulating drilling fluids, cooling drill bits, and transporting cuttings to the surface. Sustained drilling activity across onshore and offshore fields keeps demand stable, even amid rig count fluctuations, as operators prioritize continuous and efficient drilling operations.

Moreover, efficiency-focused drilling strategies are reinforcing equipment investments. Advancements in rig productivity and deeper well development require high-performance, reliable mud pumps to maintain well integrity. Increased focus on maximizing output per rig has resulted in consistent procurement of advanced pump systems, supporting long-term contracts and recurring demand for manufacturers and service providers.

Technological Advancements Enhancing Mud Pump Performance

Ongoing technological advancements in mud pump design are significantly boosting market growth by improving pressure handling, durability, and operational reliability. Modern mud pumps now feature enhanced triplex and quintuplex configurations, advanced metallurgy, and ceramic liners, enabling superior performance in high-temperature and high-pressure drilling environments while minimizing wear and unplanned downtime.

These innovations help operators reduce maintenance costs and improve drilling efficiency, particularly in complex and deepwater projects. Improved pump lifespans and higher flow consistency translate into lower total cost of ownership, encouraging upgrades and replacements. As drilling environments become more demanding, technologically advanced mud pumps are increasingly viewed as essential assets rather than optional equipment.

Restraints - Volatility in Crude Oil Prices Impacting Exploration Investments

Fluctuating crude oil prices remain a key restraint for the mud pumps market, as periods of low pricing directly affect upstream exploration and drilling budgets. When oil prices fall below economically viable thresholds, operators often delay or cancel drilling programs, leading to reduced demand for drilling equipment, including mud pumps, across both onshore and offshore projects. This uncertainty disrupts procurement cycles and capital planning for operators and equipment suppliers alike. Reduced rig activity translates into fewer new pump installations and lower aftermarket demand, pressuring manufacturers’ revenues and margins. Prolonged price volatility also increases cautious spending behavior, making market growth highly sensitive to short-term commodity price movements.

Stringent Environmental Regulations on Drilling Equipment

Stringent environmental regulations pose another significant restraint, particularly for diesel-powered mud pumps that generate higher emissions. Regulatory frameworks in North America and Europe increasingly mandate lower exhaust emissions and noise levels, compelling operators to invest in costly retrofits or cleaner alternatives to meet compliance standards. These requirements raise overall operating and capital costs, discouraging equipment upgrades in highly regulated regions. In some environmentally sensitive zones, restrictions on conventional fuel-powered equipment limit deployment altogether. As a result, regulatory pressures slow market penetration, extend replacement cycles, and create additional compliance-related challenges for both manufacturers and drilling operators.

Opportunities - Expansion in Offshore and Deepwater Drilling Ventures

The expansion of offshore and deepwater drilling activities presents a strong growth opportunity for the mud pumps market, as such projects require high-capacity, durable pumping systems capable of operating under extreme pressure and temperature conditions. Offshore developments in regions such as the Gulf of Mexico, the North Sea, and offshore Brazil continue to demand technologically advanced mud pumps to ensure drilling stability and safety.

As deepwater exploration gains momentum, operators increasingly prefer high-performance quintuplex and advanced triplex pumps for improved flow control and reliability. These systems command higher margins and longer service contracts, allowing manufacturers to strengthen revenue streams while supporting complex offshore drilling programs worldwide.

Shift Toward Sustainable and Electric Mud Pump Solutions

The gradual shift toward electric mud pumps represents a significant opportunity, driven by global decarbonization initiatives and stricter emission standards. Electric-driven systems offer higher energy efficiency and lower emissions compared to traditional diesel-powered pumps, making them well-suited for modern, electrified drilling rigs.

Growing emphasis on ESG compliance is encouraging adoption across oil & gas, mining, and construction sectors. As power grids integrate more renewable energy, electric mud pumps align with sustainability goals while reducing operating costs. Policy incentives and regulatory support further accelerate demand, enabling suppliers to capture long-term growth in environmentally friendly pump solutions.

Category-wise Analysis

Product Type Insights

Triplex mud pumps dominated the market with an estimated 38% share in 2025, supported by their balanced three-piston configuration that delivers stable flow rates and reduced pulsation. Their ability to handle high pressures with consistent performance makes them the preferred choice across most onshore and offshore oil & gas drilling operations. Lower maintenance requirements and strong compatibility with modern rigs further reinforce their leadership position.

Quintuplex mud pumps represent the fastest-growing product category, driven by increasing demand for higher flow rates and smoother delivery in complex drilling environments. As well as becoming deeper and more technically demanding, operators are increasingly adopting quintuplex systems for enhanced efficiency, reliability, and reduced vibration, particularly in offshore and high-pressure drilling projects.

Power Insights

Fuel engine-driven mud pumps held a leading 60% market share in 2025, primarily due to their widespread use in remote and off-grid drilling locations. Diesel-powered systems offer strong mobility, high torque, and operational independence, making them ideal for offshore platforms and rugged onshore terrains where stable electrical infrastructure is unavailable.

Electric mud pumps are emerging as the fastest-growing power segment, supported by rising electrification of drilling rigs and sustainability initiatives. Improved grid access, hybrid rig designs, and lower operational emissions are driving adoption. These pumps offer quieter operation, higher energy efficiency, and reduced maintenance, positioning them as a preferred choice for future-ready and environmentally conscious drilling operations.

Application Insights

Onshore drilling accounted for approximately 70% of the market share in 2025, driven by extensive shale development and conventional oilfield operations worldwide. Onshore projects benefit from easier equipment transportation, faster setup, and lower operational costs compared to offshore drilling, sustaining high demand for mud pumps across mature and emerging producing regions.

Offshore drilling is the fastest-growing application segment, fueled by rising investments in deepwater and ultra-deepwater exploration. Increasing energy demand and depletion of shallow reserves are pushing operators offshore, where high-capacity and high-pressure mud pumps are essential. Technological advancements and improved project economics are further accelerating growth in offshore mud pump deployments.

End-user Insights

The oil and gas sector led the market with around 47.1% share in 2025, as mud pumps are indispensable for upstream drilling and well construction activities. Their critical role in fluid circulation, pressure control, and wellbore stability makes them essential across exploration and production operations, supporting consistent demand from national and international oil companies.

Mining and geothermal drilling constitute the fastest-growing end-user segment, driven by increasing demand for minerals, metals, and renewable energy resources. Deeper mining operations and expanding geothermal projects require robust fluid circulation systems, creating new opportunities for mud pump suppliers beyond traditional oil and gas applications.

Regional Insights

North America Mud Pumps Market Trends and Insights

North America accounted for approximately 31.2% of the global mud pumps market in 2025, driven primarily by strong U.S. shale drilling activity and advanced upstream infrastructure. Despite moderate rig counts, operators continue to achieve higher output through efficiency-driven drilling, sustaining steady demand for high-performance mud pumps. The region benefits from a mature oilfield services ecosystem and strong adoption of technologically advanced pumping systems.

Looking ahead, growth is supported by continuous innovation in pump design, automation, and materials. Digital monitoring, higher-pressure capabilities, and durability enhancements are gaining traction as operators focus on productivity per well rather than rig expansion. Ongoing investment in unconventional resources and replacement demand for upgraded equipment will continue to underpin North America’s stable market position.

Europe Mud Pumps Market Trends and Insights

Europe represents a technologically mature mud pumps market, supported by sustained offshore drilling activity in the North Sea, particularly across the UK, Norway, and Germany. The region emphasizes equipment reliability and safety, with strict operational standards shaping procurement decisions. Adoption is steady as operators focus on maintaining output from existing offshore assets.

The European mud pumps market is expected to grow at a CAGR of 5.9%, driven by energy security concerns and gradual offshore redevelopment projects. Increasing regulatory pressure is accelerating the shift toward electric and low-emission pump systems. As sustainability and compliance become central priorities, demand for modernized, efficient mud pumps is expected to rise across both offshore and select onshore operations.

Asia Pacific Mud Pumps Market Trends and Insights

Asia Pacific held an estimated 35.6% share of the global mud pumps market in 2025, reflecting its strong position as the largest and most dynamic regional market. Rapid industrialization, rising energy consumption, and expanding oil and gas exploration in China and India are key demand drivers. Cost-competitive manufacturing capabilities further strengthen the region’s market footprint.

The region is witnessing fast adoption of mud pumps across onshore shale, conventional fields, and emerging offshore projects. Increasing foreign direct investment, national energy security initiatives, and infrastructure expansion are supporting long-term growth. As the drilling activities continue to intensify alongwith advancing domestic equipment manufacturing, Asia Pacific is expected to remain the fastest-growing and most competitive regional market.

Competitive Landscape

The global mud pumps market demonstrates a highly consolidated competitive structure, with a small group of leading players collectively accounting for over half of global revenues. These companies maintain their dominance through strong research and development capabilities, extensive global service networks, and long-term relationships with major drilling operators. Product reliability, high-pressure performance, and aftersales support remain key competitive differentiators.

Market participants are increasingly focusing on innovation-led strategies to sustain their positions. Emphasis is growing on digital integration, modular designs, and hybrid pump systems that enhance efficiency and support sustainability goals. Strategic expansions, including capacity additions and offshore-oriented offerings, are further shaping competitive dynamics and raising entry barriers for smaller manufacturers.

Key Developments:

- In March 2024, EZG Manufacturing launched the Mud Hog® Pump MPC 240, designed for high-throughput grouting applications. The system integrates automated mixing with pumping capabilities and delivers a capacity of up to 240 bags per hour, improving jobsite productivity and consistency.

- In November 2025, Baker Hughes highlighted a global decline in active rig counts, prompting major operators to prioritize drilling efficiency. This shift accelerated upgrades to high-performance and energy-efficient mud pumps, supporting sustained output despite reduced rig activity across key producing regions.

- In 2025, NOV introduced advanced triplex mud pumps featuring ceramic liners engineered for extended wear life. These enhancements improve durability and reliability in harsh drilling environments, reduce maintenance frequency, and support high-pressure operations in both onshore and offshore applications.

Companies Covered in Mud Pumps Market

- National Oilwell Varco (NOV)

- Schlumberger Limited

- Weatherford International plc

- Halliburton Company

- Baker Hughes Company

- Gardner Denver, Inc. (Ingersoll Rand)

- Flowserve Corporation

- Honghua Group Limited

- American Block Inc.

- Bentec GmbH Drilling & Oilfield Systems

- TSC Group Holdings Limited

- China National Petroleum Corporation (CNPC)

- Shandong Kerui Petroleum Equipment Co., Ltd.

- Jereh Group

- Mud King Products, Inc.

Frequently Asked Questions

The global Mud Pumps Market is expected to reach US$ 1.4 Billion in 2026, driven by sustained drilling activity.

Rising oil and gas exploration and efficiency-driven drilling operations continue to drive demand for advanced mud pump systems.

Asia Pacific leads with a 35.6% share in 2025, supported by strong exploration activity in China and India and cost-efficient manufacturing.

The shift toward electric mud pumps presents a key opportunity amid electrified rigs, ESG compliance, and emission-reduction mandates.

Leading players include NOV, Halliburton, Schlumberger, and Weatherford.