- Home Care & Utilities

- Pumps and Trigger Spray Market

Pumps and Trigger Spray Market Size, Share, and Growth Forecast 2026 - 2033

Pumps and Trigger Spray Market by Material Type (Plastic, Metal, Glass, Others), Product Type (Pumps, Trigger Sprays), Capacity/Size (<50 ml, 50-100 ml, 101-250 ml, 251-500 ml, >500 ml), Distribution Channel (Online, Offline), Industry (Personal Care & Cosmetics, Homecare, Industrial & Commercial, Healthcare & Pharmaceuticals, Agriculture & Horticulture, Food & Beverage), by Regional Analysis, 2026 - 2033

Pumps and Trigger Spray Market Size and Trend Analysis

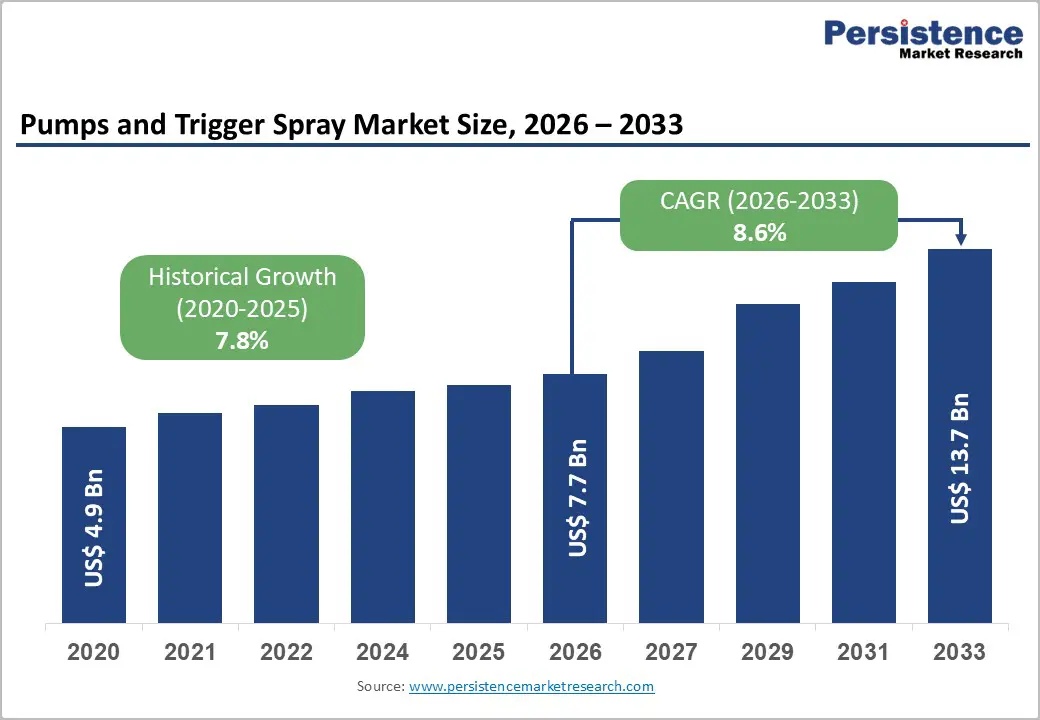

The global pumps and trigger spray market size is expected to be valued at US$ 7.7 billion in 2026 and projected to reach US$ 13.7 billion by 2033, growing at a CAGR of 8.6% between 2026 and 2033.

The market’s robust expansion is fundamentally driven by surging demand from personal care, homecare, and pharmaceutical packaging industries, anchored in rising consumer preference for hygienic, precise, and contamination-free dispensing solutions. Increasing penetration of airless pump technology in premium cosmetics, post-pandemic structural growth in institutional cleaning product consumption, and the progressive adoption of sustainable packaging formats are collectively accelerating market adoption across both developed and emerging economies, ensuring consistent and broad-based demand growth throughout the forecast period.

Key Industry Highlights

- Leading Region: North America leads the global Pumps and Trigger Spray market with approximately 31% revenue share in 2025, driven by the United States’ mature personal care and pharmaceutical packaging sectors, alongside strong homecare product consumption and a robust innovation ecosystem.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, projected to expand at approximately 10.2% CAGR (2026 - 2033), powered by urbanization, rising middle-class disposable incomes, pharmaceutical sector expansion, and growing retail modernization in China, India, and ASEAN markets.

- Dominant Material: The Plastic material segment dominates with approximately 65% share in 2025, driven by cost-efficiency, chemical resistance, design versatility, and widespread adoption across personal care, home care, industrial, and agricultural dispensing applications globally.

- Fastest Growing Segment: Online distribution is the fastest-growing channel, propelled by direct-to-consumer beauty and homecare brand growth, e-commerce platform penetration, and digital-first packaging procurement models requiring innovative, sustainable, and customized pump dispensing formats.

- Key Opportunity: The most significant market opportunity lies in healthcare and pharmaceutical packaging, where escalating demand for precision metering pump systems in nasal spray and topical drug delivery applications, supported by aging population demographics and FDA regulatory expansion, is set to generate substantial incremental revenue through 2033.

| Key Insights | Details |

|---|---|

| Pumps and Trigger Spray Market Size (2026E) | US$ 7.7 Billion |

| Market Value Forecast (2033F) | US$ 13.7 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.6% |

| Historical Market Growth (2020 - 2025) | 7.8% |

Market Dynamics

Drivers - Rising Demand from the Global Personal Care and Cosmetics Industry

The personal care and cosmetics industry represents the most prominent demand driver for pumps and trigger spray packaging. According to Cosmetics Europe, the European cosmetics and personal care market was valued at over €90 billion in 2023, with continued premiumization trends reinforcing volume growth across skincare, haircare, and body care categories. Pumps, particularly airless and metering variants, have become indispensable to this segment as they prevent oxidation of active ingredients, ensure precise dose delivery, and eliminate contamination risks inherent in open-jar formats. The U.S. Bureau of Labor Statistics data confirms that consumer expenditure on personal care products has persistently outpaced general inflation in recent years. As global beauty brands prioritize packaging that preserves formulation efficacy and aligns with clean beauty positioning, advanced pump dispensers remain at the forefront of packaging innovation and volume growth.

Post-Pandemic Structural Expansion of Homecare and Institutional Cleaning Markets

The global homecare and institutional cleaning sector has undergone a durable demand transformation in the wake of the COVID-19 pandemic, creating sustained and broad-based uptake for trigger spray systems. The U.S. Environmental Protection Agency (EPA) documented the registration of over 500 new disinfectant products on its List N between 2020 and 2022, reflecting unprecedented demand for surface cleaning and disinfection solutions. Trigger spray dispensers remain the preferred format across household cleaners, disinfectants, and multi-surface sanitizers owing to their ergonomic design, customizable spray patterns, and unit-cost efficiency. The Cleaning Industry Research Institute (CIRI) further highlights that commercial cleaning product usage experienced measurable structural uplift in healthcare, hospitality, and food service verticals post-pandemic, directly driving bulk-format trigger spray adoption across both B2C and B2B procurement channels.

Restraints

Volatility in Petroleum-Derived Raw Material Prices

The pumps and trigger spray market is meaningfully exposed to fluctuations in the prices of petroleum-derived polymers, particularly Polypropylene (PP), High-Density Polyethylene (HDPE), and Polyethylene Terephthalate (PET), which collectively constitute the primary raw material base for dispensing component manufacturing. The International Energy Agency (IEA) has consistently documented elevated crude oil price volatility since 2021, which directly propagates through polymer feedstock pricing. Such instability compresses manufacturer margins, particularly for mid-tier producers with limited hedging capacity, and complicates multi-year supply contract negotiations with brand owner clients. Concurrent global supply chain disruptions, driven by geopolitical tensions and logistics infrastructure constraints, have intermittently impacted component availability, leading to production schedule delays and elevated inventory costs for pump and spray assembly manufacturers worldwide.

Regulatory Pressure on Single-Use Plastics Constraining Conventional Packaging Formats

Mounting regulatory scrutiny on single-use plastic packaging presents a structural headwind for conventional pump and trigger spray manufacturers. The European Union’s Single-Use Plastics Directive (SUPD) imposes explicit restrictions on certain plastic packaging formats, while ongoing negotiations under the UNEP Global Plastics Treaty signal a coordinated tightening of plastic packaging regulations across signatory nations. Compliance mandates necessitate significant reformulation of materials and capital-intensive redesign of existing product tooling. Smaller manufacturers, in particular, face disproportionate cost burdens in adapting their production lines to meet evolving recyclability and material composition standards, limiting their competitive participation and contributing to accelerated consolidation pressures within the global market landscape.

Opportunity - Surge in Demand for Airless and Sustainable Pump Packaging in Clean Beauty and Premium Cosmetics

The rapid global transition toward sustainable and airless pump packaging presents a high-value commercial opportunity for forward-looking market participants. Airless pump systems materially extend product shelf life by eliminating air exposure, reducing the requirement for chemical preservatives, a critical value proposition in the burgeoning clean beauty segment. The European Bioplastics Association projects that global bioplastics production capacity will grow from 2.18 million tonnes in 2023 to approximately 7.43 million tonnes by 2028, enabling cost-competitive eco-friendly pump component manufacturing at scale. Major global brands including L’Oréal and Unilever have publicly committed to achieving 100% recyclable, reusable, or compostable packaging by 2025, directly stimulating downstream demand for redesigned mono-material and refillable pump dispensing systems. Manufacturers investing proactively in post-consumer recycled (PCR) content integration and refill-compatible pump engineering are strategically positioned to secure premium brand contracts and long-term category leadership.

Expansion of Healthcare and Pharmaceutical Packaging Driving Precision Metering Pump Demand

The pharmaceutical and healthcare packaging sector represents one of the most compelling frontier opportunities for pumps and trigger spray manufacturers. Precision dose dispensing is a non-negotiable requirement across nasal spray drug delivery, topical pharmaceutical applications, and ophthalmic formulations, all of which rely on metering and diaphragm pump technologies. The U.S. Food and Drug Administration (FDA) currently lists over 200 nasal spray drug products in its Orange Book, underscoring the established and growing regulatory framework supporting nasal drug delivery device adoption. Furthermore, the United Nations projects that the global population aged 65 and above will reach 1.6 billion by 2050, structurally elevating demand for user-friendly, reliable, and precise drug dispensing formats. Companies capable of meeting cGMP manufacturing standards for pharmaceutical-grade dispensing components are well-positioned to capture significant incremental revenue as healthcare systems globally expand pharmaceutical access.

Category-wise Analysis

Material Type Insights

The Plastic segment is the dominant material category within the pumps and trigger spray market, accounting for approximately 65% of total market share in 2025. This commanding leadership reflects the inherent performance advantages of plastics, including lightweight construction, manufacturing design versatility, chemical resistance, and favorable unit economics, that make them the preferred material for mass-market personal care, homecare, industrial, and agricultural dispensing applications. Among plastic sub-types, Polypropylene (PP) and High-Density Polyethylene (HDPE) are the most extensively deployed, prized for their mechanical durability, excellent chemical compatibility, and suitability for high-speed injection molding processes. The Plastics Industry Association recognizes packaging as one of the largest global end-use sectors for polymer consumption. While sustainability imperatives are stimulating interest in glass and metal alternatives, the scalability, processability, and established supply chain infrastructure of plastic materials continue to sustain its market-leading position.

Product Type Insights

The Pumps segment leads the product type category, representing approximately 55% of total market share in 2025. This leadership is underpinned by the extensive and diversified application of pump dispensers across premium personal care (airless and metering pumps), pharmaceutical packaging (metering and diaphragm pumps), and industrial fluid handling (pressurized and peristaltic pumps). Airless pump technology, in particular, has achieved exceptional commercial traction within the luxury cosmetics and clinical skincare segments, where preservation of high-value active ingredients is a paramount concern. According to Cosmetics Europe, skincare consistently ranks as the largest category within the European cosmetics market by retail sales value, which directly underpins elevated airless pump dispenser volumes. The breadth and configurational diversity of pump formats, spanning six distinct sub-types, enables broad cross-industry deployment, reinforcing the segment’s sustained market dominance.

Capacity / Size Insights

The 101-250 ml capacity bracket leads the pumps and trigger spray market, capturing approximately 34% of total market share in 2025. This capacity range represents the structural sweet spot between everyday usability, product longevity, and retail packaging convenience across the dominant end-use categories of personal care and homecare. Standard lotion dispensers, skincare serums, shampoos, and household cleaning products are predominantly packaged within this volume range, aligning directly with typical consumer usage cycles and planogram shelf standards established by major retail chains. The Consumer Brands Association has consistently identified packaging convenience and unit value perception as leading purchase decision drivers in the fast-moving consumer goods (FMCG) segment. Continued demand from both premium beauty brands, which favor this format for aesthetic consistency, and value-tier homecare product lines collectively reinforce the entrenched and stable market leadership of the 101-250 ml segment.

Distribution Channel Analysis

The Offline distribution channel retains its position as the market leader within the distribution channel category, accounting for approximately 62% of total market share in 2025. Brick-and-mortar retail formats, encompassing supermarkets, hypermarkets, specialty beauty stores, pharmacy chains, and industrial supply distributors, remain the primary procurement route for pump and trigger spray-dispensed products across both consumer and B2B segments. Physical retail environments offer immediate product accessibility, tactile evaluation, and established replenishment relationships that are especially valued in homecare and personal care purchasing decisions. Leading global retailers including Walmart, Carrefour, and Boots maintain extensive, well-curated product assortments of pump and spray-dispensed goods. Nonetheless, the growing penetration of e-commerce platforms, accelerated by direct-to-consumer brand models in the beauty and homecare segments, is steadily compressing the offline channel’s share dominance, particularly across North American and Western European markets.

Industry Insights

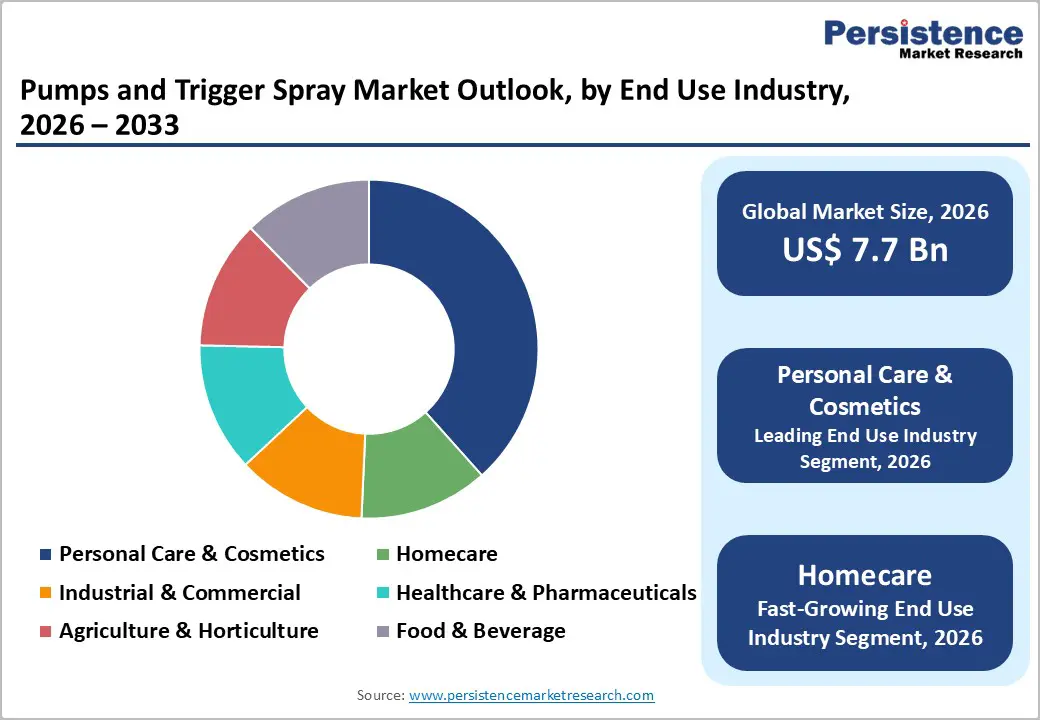

The Personal Care & Cosmetics segment holds the leading position within the end-use industry category, representing approximately 36% of total market share in 2025. This dominance is a direct reflection of the pervasive deployment of pump dispensers across a diverse array of personal care product formats, including skincare serums, facial moisturizers, shampoos, conditioners, body lotions, hair treatments, and liquid foundations. Heightened consumer awareness around hygiene and contamination prevention, structurally reinforced by the COVID-19 pandemic, has further accelerated the adoption of no-touch pump dispensing formats across this category. Global beauty and personal care industry revenues exceeded US$ 500 billion in 2025 and continue to expand on a sustained basis. The concurrent rise of clinical-grade skincare brands investing in precision airless and metering pump formats to preserve active ingredient stability further consolidates the segment’s market leadership through the forecast period.

Regional Insights

North America Pumps and Trigger Spray Market Trends and Insights

North America leads the global pumps and trigger spray market, accounting for approximately 31% of total market revenue share in 2025. The United States is the primary regional engine, supported by a highly mature personal care and cosmetics industry, robust pharmaceutical packaging demand underpinned by precision metering pump adoption, and elevated consumer spending on homecare and surface cleaning products. The U.S. FDA’s stringent regulatory standards for drug delivery device performance have accelerated domestic pharmaceutical manufacturers’ adoption of validated airless and metering pump systems. Innovation remains a defining characteristic of the North American market.

The U.S. Plastics Pact, targeting 100% reusable, recyclable, or compostable plastic packaging through coordinated industry commitments, is actively driving dispensing component manufacturers to develop next-generation mono-material and refillable pump architectures. Canada’s expanding natural and organic beauty market is generating incremental demand for premium pump dispensers, while regulatory restrictions on volatile organic compounds (VOCs) in aerosols, enforced by both the EPA and individual state environmental agencies, continue to shift consumer and industrial procurement preferences toward trigger spray formats as more environmentally responsible dispensing alternatives.

Europe Pumps and Trigger Spray Market Trends and Insights

Europe represents the second-largest regional market for pumps and trigger sprays, driven by a sophisticated regulatory environment, a leading cosmetics manufacturing ecosystem, and progressive sustainability mandates that are actively reshaping product design and material innovation trajectories. Germany, France, the United Kingdom, and Spain collectively account for a disproportionate share of regional pump and trigger spray consumption. The EU Green Deal and the European Union’s Single-Use Plastics Directive (SUPD) are compelling manufacturers and brand owners alike to prioritize recyclable and mono-material dispensing component designs, compressing innovation timelines.

The European Commission’s Circular Economy Action Plan has directly incentivized major personal care brands operating across the region, including those headquartered in France and Germany, to adopt refillable pump packaging formats, generating durable demand for high-cycle-life pump mechanisms. France’s landmark anti-waste legislation (Loi AGEC), which mandates progressive packaging recyclability and refillability targets, is increasingly functioning as a regional regulatory benchmark, with Spain and the Netherlands implementing complementary frameworks. These coordinated and mutually reinforcing regulatory developments are systematically reshaping material sourcing, product design investment, and end-of-life recyclability strategies across the European pump and trigger spray manufacturing value chain.

Asia Pacific Pumps and Trigger Spray Market Trends and Insights

Asia Pacific is the fastest-growing regional market for pumps and trigger sprays, projected to register a CAGR of approximately 10.2% between 2026 and 2033. China, India, and key ASEAN economies, particularly Indonesia, Vietnam, and Thailand, are the central growth contributors, propelled by expanding middle-class populations, accelerating urbanization, and surging domestic consumption of personal care, homecare, pharmaceutical, and agricultural products. China’s National Bureau of Statistics has consistently reported year-on-year increases in cosmetics retail sales, reflecting deepening consumer engagement with premium and functional personal care categories regulated under the National Medical Products Administration (NMPA) framework.

India’s packaging industry is experiencing accelerated capacity growth supported by the central government’s “Make in India” initiative and the Production Linked Incentive (PLI) scheme for pharmaceuticals, which is stimulating localized manufacturing of dispensing components. Southeast Asian markets are benefiting from rapid modern retail infrastructure development, elevating demand for packaged FMCG goods utilizing pump and trigger spray formats. The region’s inherent manufacturing cost advantages, particularly in China and Vietnam, are additionally attracting global brand owners to establish regional dispensing component supply chains, further catalyzing both manufacturing capacity expansion and technology transfer within the Asia Pacific market.

Competitive Landscape

The global pumps and trigger spray market exhibits a moderately consolidated competitive structure, with established multinational players including Silgan Dispensing Systems Corporation, Guala Dispensing S.p.A., AFA Dispensing, and Aptar Group, Inc. commanding significant market revenue shares. Leading companies are investing aggressively in sustainable dispensing technology, particularly mono-material pump architectures, post-consumer recycled (PCR) content integration, and refill-compatible systems, alongside targeted geographic expansion into high-growth Asia Pacific markets. Strategic acquisitions, long-term OEM supply agreements with global cosmetics and pharmaceutical brands, and tooling customization capabilities represent key competitive differentiators. Emerging business model trends include design-for-recyclability platforms and digital dispensing innovation.

Key Developments:

- September, 2025: Silgan Dispensing launched ERA™, a fully recyclable, all-plastic next-generation cosmetic pump engine designed to enhance sustainability and premium performance with high evacuation efficiency for diverse beauty and personal care applications.

- August, 2025: Aptar Beauty introduces a new full-plastic, highly recyclable Trigger Spray Pump (TSP) for the home care market, combining soft actuation, lightweight design, and broad formulation compatibility to enhance sustainability and user experience.

- October, 2024: CLR Brands launches a 22 oz ready-to-use Calcium, Lime & Rust Remover trigger sprayer, complementing its iconic jug to offer convenient cleaning and expand retailer offerings.

Companies Covered in Pumps and Trigger Spray Market

- Guala Dispensing S.p.A.

- Silgan Dispensing Systems Corporation

- AFA Dispensing

- Bramlage Division GmbH & Co. KG

- MJS Packaging

- The Packaging Company

- Klager Plastik GmbH

- Plastopack Industries

- Demareis GmbH

- Burkle GmbH

- Rieke Packaging

- CLC & Sengcze

- Aptar Group, Inc.

- Berry Global Group, Inc.

- Albéa Group

- RPC Group

- Raepak Ltd.

- SeaCliff Beauty Packaging

Frequently Asked Questions

The pumps and trigger spray market is projected to reach US$ 7.7 billion in 2026.

Demand is driven by hygienic dispensing needs, homecare growth, and pharmaceutical spray applications.

North America leads the market, holding about 31% revenue share.

Opportunities include sustainable airless packaging and expanding pharmaceutical metering pump applications.

Major players include Silgan Dispensing, Aptar, Berry Global, Guala Dispensing, and Albéa Group.