- Medical Devices

- Pressure Guidewires Market

Pressure Guidewires Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Pressure Guidewires Market by Product (Flat Tipped Pressure Guidewires, and Flexible Tip Pressure Guidewires), by Technology (Pressure Wire Technology, and Optical Fiber Technology), by End-user (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

Pressure Guidewires Market Share and Trends Analysis

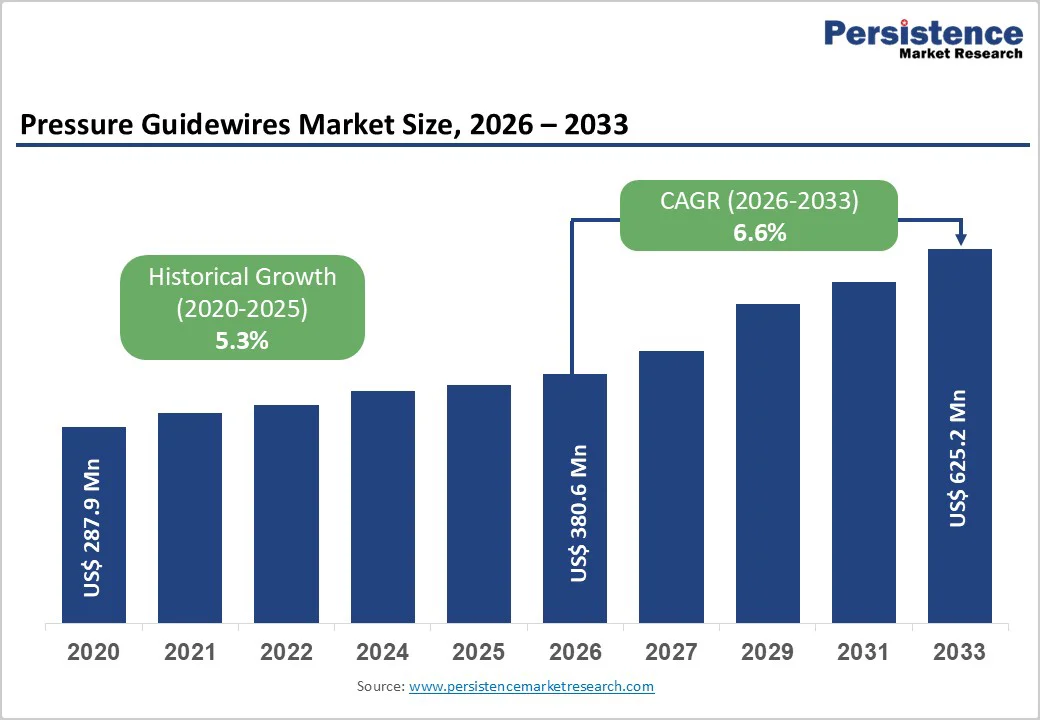

The global pressure guidewires market size is estimated to grow from US$ 380.6 million in 2026 to US$ 625.2 million by 2033, growing at a CAGR of 6.6% from 2026 to 2033.

The global demand for pressure guidewires is increasing steadily, driven by the rising prevalence of coronary artery disease, growing volumes of percutaneous coronary interventions (PCI), and wider clinical adoption of physiology-based lesion assessment techniques such as fractional flow reserve (FFR) and instantaneous wave-free ratio (iFR).

Increasing use of advanced catheterization techniques, improved integration of imaging, and greater emphasis on evidence-based decision-making in interventional cardiology are driving sustained market growth.

Key Industry Highlights

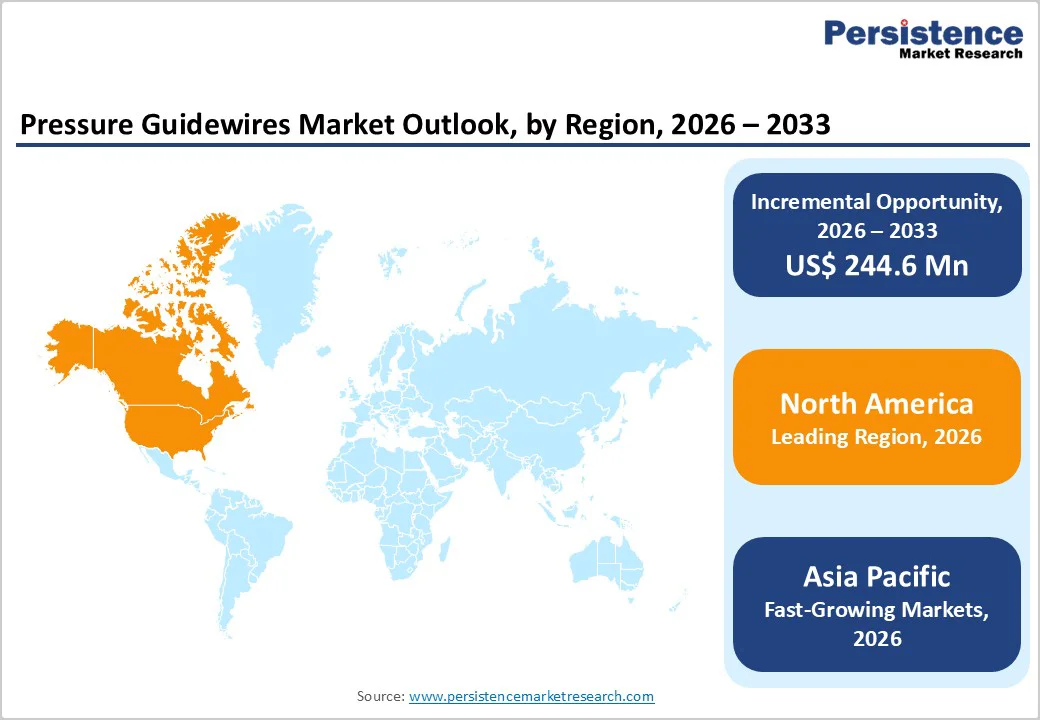

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high PCI volumes, early adoption of coronary physiology assessment, and the strong presence of leading pressure guidewire manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large cardiovascular disease patient base, rapid growth in cardiac catheterization laboratories, improving healthcare infrastructure, and rising investments in interventional cardiology services.

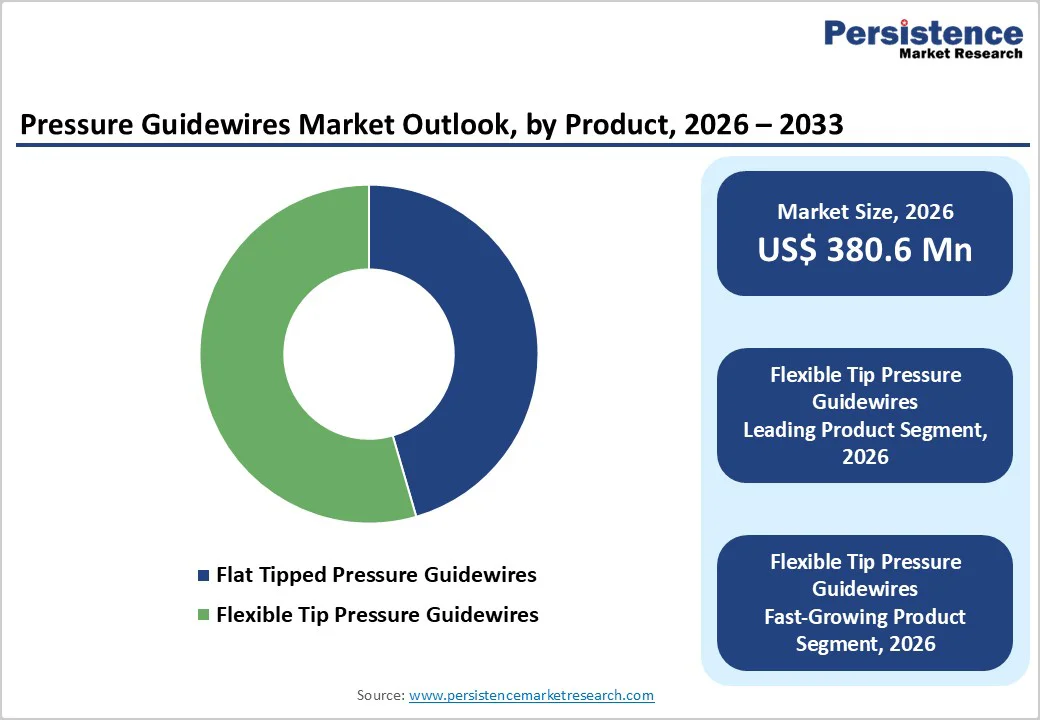

- Leading Product Segment: Flexible tip pressure guidewires dominate the market due to their superior deliverability, ease of navigation in complex coronary anatomy, and broad applicability across routine and complex PCI procedures.

- Fastest-Growing Product Segment: Flat-tipped pressure guidewires are expanding rapidly as demand for cost-effective solutions in standard diagnostic assessments and routine coronary physiology measurements increases.

- Leading Technology Segment: Pressure wire technology remains the top segment, driven by its widespread clinical adoption, established reimbursement pathways, and strong clinical evidence supporting its use in coronary lesion assessment.

- Fastest-Growing Technology Segment: Optical fiber technology is scaling quickly as demand rises for higher signal precision, improved measurement stability, and advanced integration with next-generation imaging and cath lab systems.

| Key Insights | Details |

|---|---|

| Pressure Guidewires Market Size (2026E) | US$ 380.6 Mn |

| Market Value Forecast (2033F) | US$ 625.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Dynamics

Driver - Rising Cardiovascular Disease Burden and Advancing Guidewire Technologies

The rising global prevalence of cardiovascular disease, particularly coronary artery disease (CAD), is a primary driver of sustained demand for pressure guidewires. Increasing incidence of atherosclerosis, aging populations, sedentary lifestyles, and higher rates of diabetes and hypertension are driving growth in percutaneous coronary interventions (PCI) worldwide.

For instance, according to the Centers for Disease Control and Prevention (CDC), cardiovascular disease remains a major public health burden in the United States. A heart attack occurs approximately every 40 seconds, translating to nearly 805,000 cases annually. Of these, around 605,000 are first-time heart attacks, while about 200,000 occur in individuals with a prior history of myocardial infarction.

As interventional cardiology increasingly shifts toward physiology-based decision-making, pressure guidewires are becoming essential tools for accurate lesion assessment using fractional flow reserve (FFR) and instantaneous wave-free ratio (iFR).

These techniques enable clinicians to determine the functional significance of coronary stenoses, optimize stent placement decisions, reduce unnecessary interventions, and improve long-term patient outcomes, thereby strengthening clinical adoption across both complex and routine PCI procedures.

Additionally, continuous technological advancements are significantly enhancing the clinical utility and adoption of pressure guidewires. Innovations in miniaturized sensor technology, improved signal stability, and enhanced wire flexibility are enabling better navigation through complex coronary anatomies while maintaining measurement accuracy.

Integration with advanced imaging platforms and cath lab systems is improving procedural efficiency and real-time data interpretation.

Additionally, developments in optical fiber-based pressure sensing and wireless connectivity are reducing signal drift, enhancing reproducibility, and supporting digitally integrated workflows. These advancements collectively increase physician confidence, improve procedural outcomes, and reinforce the role of pressure guidewires as a standard of care in modern interventional cardiology.

Restraints - Cost Barriers and Limited Penetration in Emerging Markets

High device and procedure costs remain a significant restraint on the global pressure guidewires market. Advanced pressure guidewires incorporate sophisticated sensor technologies, high-precision materials, and proprietary software integration, all of which contribute to premium pricing.

In addition to the cost of the guidewire itself, hospitals and catheterization laboratories must invest in compatible consoles, imaging systems, and maintenance, increasing the overall procedural expense.

In cost-sensitive healthcare systems, particularly those operating under fixed reimbursement frameworks, these high upfront and per-procedure costs can limit routine use of pressure guidewires, even when their clinical value in optimizing PCI outcomes is well recognized.

These cost-related challenges are further amplified in emerging and lower-resource markets, where adoption remains limited. Many healthcare facilities in developing regions face budget constraints, inconsistent reimbursement policies, and uneven access to advanced catheterization infrastructure. Limited availability of trained interventional cardiologists and supporting technical staff also restricts wider implementation.

As a result, coronary interventions in these markets often rely solely on angiography rather than on physiology-based assessment. Without targeted pricing strategies, reimbursement reforms, and infrastructure investments, the penetration of pressure guidewires in emerging economies is likely to remain constrained, slowing overall market expansion despite rising cardiovascular disease prevalence.

Opportunity - Shift Toward Outpatient Care and Digital Integration

The expansion of ambulatory surgical centers (ASCs) represents a significant growth opportunity for the pressure guidewires market. Healthcare systems globally are increasingly shifting select cardiac diagnostic and interventional procedures from inpatient hospitals to outpatient and ambulatory settings to reduce costs, improve patient throughput, and enhance procedural efficiency.

This transition is driving demand for compact, easy-to-use, and highly reliable pressure guidewire systems that can be seamlessly integrated into smaller cath lab environments. Manufacturers are responding by developing streamlined platforms with simplified setup, faster calibration, and reduced procedural complexity, making pressure-based coronary assessment more accessible in outpatient care models.

Moreover, integration with digital and artificial intelligence (AI) platforms is opening new avenues for product differentiation and clinical value creation. Advanced pressure guidewires are increasingly being paired with digital analytics, cloud-based data management, and AI-assisted decision-support tools to enhance real-time interpretation of physiological data.

These technologies support improved workflow efficiency, reduce operator variability, and enable more standardized clinical decision-making across care settings. AI-driven insights can also assist in lesion assessment, procedural planning, and post-procedure analysis, strengthening clinical confidence.

Together, the rise of ASCs and digital integration is accelerating the adoption of next-generation pressure guidewire systems and supporting long-term market expansion.

Category-wise Analysis

By Product Insights

The flexible-tip pressure guidewire segment is projected to dominate the global pressure guidewire market in 2026, accounting for a revenue share of 40.7%. This dominance is primarily driven by their extensive use in routine and complex percutaneous coronary interventions (PCIs), including in tortuous and calcified coronary anatomies.

Flexible tip designs provide superior deliverability, enhanced trackability, and reduced vessel trauma, making them the preferred choice for accurate physiological lesion assessment using FFR and iFR. Rising volumes of coronary artery disease cases, increasing adoption of physiology-guided PCI, and growing procedural complexity are reinforcing demand.

Continuous innovation in wire coatings, tip flexibility, and torque control is further improving procedural efficiency and supporting sustained segment leadership.

By Technology Insights

The pressure wire technology segment is projected to dominate the global pressure guidewires market in 2026, accounting for 42.7% of revenue. This leadership is driven by the widespread clinical adoption of electronic pressure sensor-based guidewires, which offer reliable signal stability, high measurement accuracy, and strong clinical validation.

These systems are widely used to assess coronary physiology in both diagnostic angiography and interventional procedures. Increasing physician familiarity, strong guideline support, and broad compatibility with existing cath lab infrastructure continue to support adoption.

High PCI volumes, repeat utilization in complex coronary disease management, and expanding access to advanced cardiac diagnostics in emerging markets further strengthen the segment’s market position.

By End-user Insights

The hospitals segment is projected to dominate the global pressure guidewires market in 2026, accounting for 48.2% of revenue. This dominance is driven by high volumes of diagnostic and interventional cardiology procedures performed in hospital-based catheterization laboratories.

Hospitals are typically equipped with advanced imaging systems, integrated hemodynamic monitoring platforms, and specialized interventional cardiology teams required for complex coronary physiology assessments. Strong investment in cath lab infrastructure, access to skilled operators, and comprehensive post-procedural care capabilities further reinforce their leading role.

Long-term procurement contracts, centralized purchasing, and preference for premium pressure guidewire systems also contribute significantly to hospital-led revenue generation.

Regional Insights

North America Pressure Guidewires Market Trends

North America is expected to dominate the global pressure guidewires market, with a 47.3% value share in 2026, led primarily by the United States. The region benefits from a highly developed healthcare infrastructure, a high prevalence of coronary artery disease, and strong adoption of physiology-guided PCI.

Advanced cath lab capabilities, early adoption of innovative pressure-sensing technologies, and widespread availability of specialized cardiac centers contribute to high procedural volumes. In addition, favorable reimbursement policies for FFR- and iFR-guided interventions support the routine use of premium pressure guidewire systems across hospitals and specialty cardiac centers.

Market growth in North America is further supported by the rapid integration of digital hemodynamic platforms, real-time data analytics, and advanced imaging technologies that enhance diagnostic accuracy and procedural outcomes.

A strong presence of leading global manufacturers, ongoing product innovation, and extensive physician training programs drive adoption of next-generation pressure guidewire solutions. Academic-clinical collaborations and well-established regulatory frameworks also facilitate faster commercialization of advanced technologies, ensuring sustained market leadership.

Europe Pressure Guidewires Market Trends

The Europe pressure guidewires market is expected to grow steadily, driven by an aging population, the rising burden of cardiovascular disease, and the increasing use of evidence-based coronary physiology assessment.

Countries such as Germany, the U.K., France, Italy, and the Nordic region demonstrate consistent procedure volumes supported by strong public healthcare systems and broad access to interventional cardiology services. Growing emphasis on guideline-directed PCI and optimization of revascularization strategies further supports pressure guidewire utilization across the region.

Growth is also supported by increasing adoption of advanced pressure-sensing technologies aimed at improving diagnostic confidence and reducing unnecessary stent placement.

Supportive regulatory frameworks, expanding public healthcare funding, and close collaboration between academic institutions and medical device manufacturers continue to strengthen the regional market. Integration of digital cath lab systems and standardized clinical protocols is further enhancing workflow efficiency and patient outcomes across European healthcare systems.

Asia Pacific Pressure Guidewires Market Trends

Asia Pacific pressure guidewires market is expected to register a relatively higher CAGR of around 8.7% between 2026 and 2033, driven by expanding healthcare infrastructure and rapidly increasing cardiac procedure volumes.

Large patient populations, rising prevalence of coronary artery disease, and growing awareness of advanced interventional cardiology techniques are fueling demand across countries such as China, India, Japan, and South Korea. Improving access to catheterization laboratories and increasing penetration of private hospitals and specialty cardiac centers are further accelerating market growth.

Additionally, government-led healthcare modernization initiatives, rising investments in cardiovascular care, and expanding training programs for interventional cardiologists are supporting adoption.

Cost-competitive manufacturing, growing local production, and strategic localization by global manufacturers are improving affordability in price-sensitive markets. Gradual adoption of physiology-guided PCI and digital cath lab technologies is strengthening long-term growth prospects across the Asia Pacific.

Competitive Landscape

The global pressure guidewires market is highly competitive, with strong participation from companies such as Abbott, Boston Scientific Corporation, Koninklijke Philips N.V., Biotronik, MicroPort Scientific Corporation, and Cook.

These players leverage extensive global distribution networks, strong brand recognition, and continuous innovation in pressure-sensing technologies, guidewire design, and integrated catheterization laboratory solutions to address evolving clinical needs in coronary physiology assessment.

Their portfolios focus on improving measurement accuracy, signal stability, deliverability, and compatibility with existing cath lab infrastructure, enabling widespread adoption across diagnostic and interventional cardiology procedures.

Rising demand for physiology-guided PCI, minimally invasive cardiac interventions, and outpatient cardiac care is driving ongoing product innovation and portfolio expansion. Manufacturers are increasingly prioritizing advancements in sensor miniaturization, flexible and hydrophilic-coated wire designs, and digital integration with hemodynamic and imaging platforms.

Strategic priorities include expanding physician training and education programs, enhancing technology interoperability, pursuing geographic expansion in high-growth emerging markets, and strengthening partnerships with hospitals and cardiac centers to reinforce competitive positioning and support long-term market growth.

Key Industry Developments:

- In December 2025, Koninklijke Philips N.V. announced an agreement to acquire SpectraWAVE, a company specializing in technologies that support the diagnosis and treatment of coronary artery disease, though the financial terms of the transaction were not disclosed. SpectraWAVE develops an intravascular imaging system for coronary arteries and offers an AI-enabled solution that derives fractional flow reserve from a single coronary angiogram, enabling clinicians to make more informed, physiology-based treatment decisions.

- In July 2024, Haemonetics Corporation announced that it had received CE Mark certification and completed the first commercial procedures in Europe using its SavvyWire® Pre-Shaped Pressure Guidewire. SavvyWire is the world’s first and only sensor-guided 3-in-1 pressure guidewire developed for Transcatheter Aortic Valve Implantation (TAVI), combining predictable wire performance with real-time hemodynamic measurement and integrated left ventricular (LV) pacing capabilities to enhance procedural efficiency and clinical workflow.

Companies Covered in Pressure Guidewires Market

- Abbott

- Boston Scientific Corporation

- Koninklijke Philips N.V

- Biotronik

- Microport Scientific Corporation

- Cook

- Terumo Medical Corporation

- Insight Lifetech

- ACIST Medical Systems

- Haemonetics Corporation

- Opsens Solutions

- Arrotek

- Meril Life Sciences Pvt. Ltd.

- Others

Frequently Asked Questions

The global pressure guidewires market is projected to be valued at US$ 380.6 Mn in 2026.

The global pressure guidewires market is driven by the rising prevalence of coronary artery disease, increasing adoption of physiology-guided PCI (FFR/iFR), and growing volumes of minimally invasive cardiac interventions.

The global pressure guidewires market is poised to witness a CAGR of 6.6% between 2026 and 2033.

Key opportunities lie in expansion into ambulatory surgical centers, rapid adoption in emerging markets, and integration of pressure guidewires with digital, AI-enabled, and advanced imaging platforms.