- Construction & Engineering

- Industrial Flooring Market

Industrial Flooring Market Size, Share, and Growth Forecast, 2025 - 2032

Industrial Flooring Market By Material Type (Epoxy Flooring, Polyurethane Flooring), Flooring Structure (Heavy-Duty Industrial Flooring, Medium-Duty Industrial Flooring), Application, End-user, and Regional Analysis for 2025 - 2032

Industrial Flooring Market Size and Trends Analysis

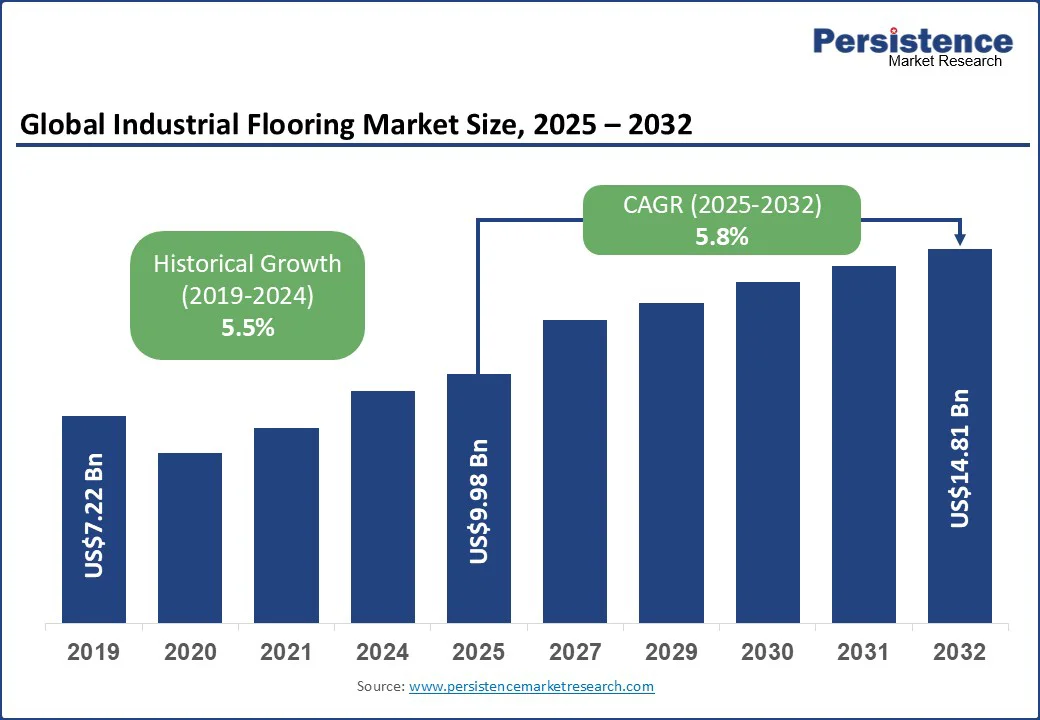

The global industrial flooring market size is projected to rise from US$9.98 Bn in 2025 to US$14.81 Bn by 2032. It is anticipated to witness a CAGR of 5.8% during the forecast period from 2025 to 2032.

The industrial flooring market is a critical segment of the construction and manufacturing industry, providing durable, chemical-resistant, and safe flooring solutions for facilities such as warehouses, factories, food processing units, and pharmaceutical plants.

Rapid industrialization, stricter safety and hygiene regulations, and the growing need for durable surfaces capable of withstanding heavy machinery, high foot traffic, and chemical exposure will drive market demand. Rising investments in infrastructure, along with technological advancements in epoxy, polyurethane, and polished concrete flooring systems, are further fueling market growth in both developed and emerging economies.

Key Industry Highlights

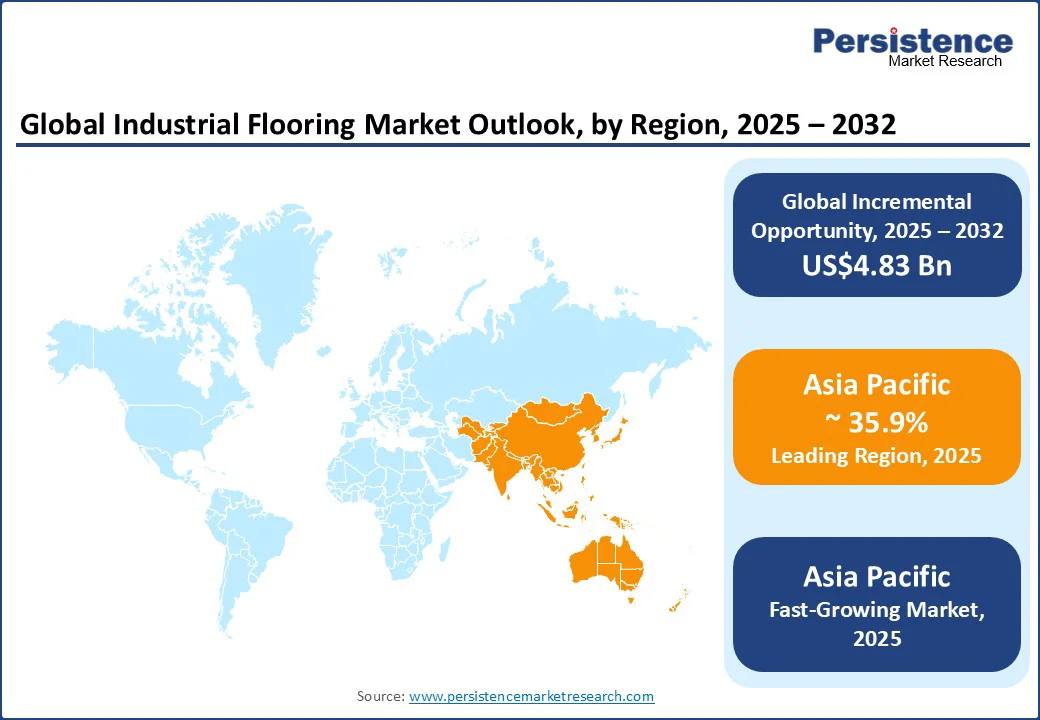

- Leading and Fastest-growing Region: Asia Pacific is expected to dominate the market with a 35.9% share, driven by industrialization in China and India and capacity expansions in pharmaceutical and electronics manufacturing.

- Investment Plans: Significant capital inflows are directed toward sustainable flooring technologies and domestic manufacturing capacity; several U.S. resinous flooring plants and Asian SPC flooring factories are set to come online by 2026.

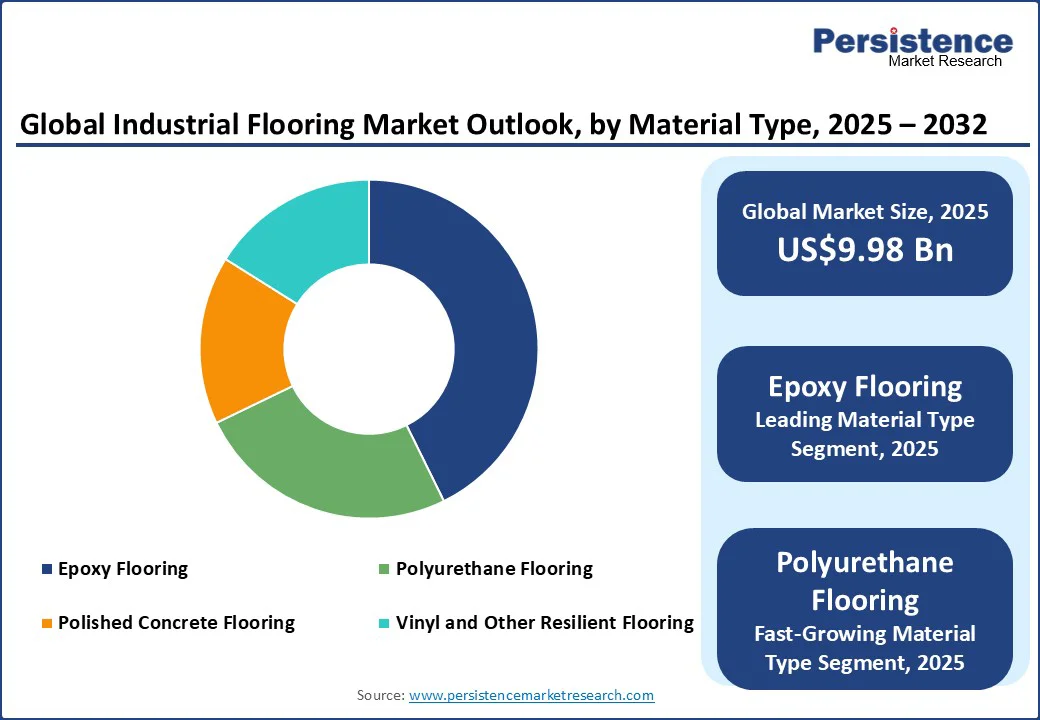

- Dominant Material Type: Epoxy flooring is projected to hold approximately 42.5% share in 2025, due to its durability, cost-effectiveness, and the rising use in heavy-duty applications such as logistics hubs and automotive facilities.

- Leading Flooring Structure: Medium-duty industrial flooring (2-4 mm) is expected to hold around 45% share, supported by demand in food processing, pharmaceutical production, packaging units, and general manufacturing facilities.

|

Global Market Attribute |

Key Insights |

|

Industrial Flooring Market Size (2025E) |

US$9.98 Bn |

|

Market Value Forecast (2032F) |

US$14.81 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Dynamics

Driver - Rising Demand for Specialized Resinous Flooring in Healthcare, Chemicals, and Time-Sensitive Industrial Facilities

The key growth driver for the industrial flooring market is the rising adoption of chemical-resistant epoxy containment flooring in sectors such as chemicals, food processing, and pharmaceuticals. These flooring systems provide a monolithic, impermeable surface that prevents seepage during chemical spills, ensuring regulatory compliance and safe operations in hazardous environments.

The healthcare industry is also emerging as a strong demand center with the growing use of seamless, jointless resinous flooring in cleanrooms, laboratories, and surgical facilities. These solutions support stringent hygiene protocols, facilitate sterilization, and align with global cleanroom standards, thereby making them increasingly indispensable in medical infrastructure.

Another major driver is the increasing uptake of cost-efficient retrofitting solutions, particularly light-duty industrial flooring systems with thicknesses below 300 µm. Such options are gaining traction in older manufacturing plants and warehouses where budget-conscious operators seek durability without extensive downtime or substrate modification.

In addition, fast-curing methyl methacrylate (MMA) flooring is witnessing robust adoption in time-sensitive sectors such as retail, cold storage, and food services. Its quick installation and return-to-service within hours meet the operational demands of facilities that cannot afford prolonged shutdowns, reinforcing its role as a high-value flooring solution.

Restraints - Installation Complexities and Skilled Labor Gaps Limiting Seamless Industrial Flooring Adoption

A key challenge in the industrial flooring market is the reluctance to replace vinyl tile flooring. Many facilities continue to favor cost-effective vinyl tiles over advanced resinous systems as vinyl tiles are significantly cheaper both in terms of material costs and installation labor, making them a more budget-friendly option.

Another technical bottleneck is the dependency on concrete moisture-mitigation epoxy membranes to counteract excessive slab moisture emissions. These protective barriers are crucial for preventing adhesive failures, blisters, efflorescence, and microbial growth; however, their complex installation and compatibility requirements add constraints, especially in retrofit scenarios.

The growing shortage of skilled labor and qualified installers, particularly those experienced with multi-coat epoxy or MMA systems, is expected to hamper the market, resulting in project delays, improper installations, and quality inconsistencies.

Many existing facilities face issues with legacy concrete substrate unevenness, where older floors with dips, cracks, or disjointed surfaces complicate retrofits. Fixing these imperfections requires meticulous prep work, specialized leveling compounds, and added labor, further discouraging facility managers from upgrading to industrial-grade systems.

Opportunity - Smart, Sustainable, and High-Performance Flooring Systems Creating Next-Gen Growth Avenues

A rapidly emerging opportunity exists at the intersection of bio-based epoxy floor coatings and the booming electric vehicle (EV) charging station sector. As the demand for EVs grows, China is expected to install 3.6 million charging points by 2025. As a result, operators are increasingly seeking floor systems that are chemical- and UV-resistant, eco-friendly, and capable of meeting sustainability goals in demanding outdoor and high-traffic environments.

The rapid growth of hyperscale data centers is driving demand for conductive epoxy systems. These systems are crucial for managing server-rack loads and electrostatic discharge (ESD), which are essential for protecting sensitive hardware, presenting a significant niche opportunity with high growth potential.

The integration of sensor-embedded smart flooring for predictive maintenance and self-healing antimicrobial epoxy coatings is driving growth, particularly in vertical farms and healthcare settings. These specialized formulations combat microbial proliferation and resist moisture-induced pH fluctuations, and also extend performance life through autonomous micro-repair, crucial for rinse-intensive, controlled-environment applications.

The rise of sensor-embedded smart flooring systems is transforming floors from passive surfaces into strategic, data-driven assets. These floors, equipped with IoT-enabled load, moisture, and vibration sensors, allow for proactive maintenance and safety monitoring in critical areas such as high-traffic warehouses, cold storage corridors, and cleanrooms.

Category-wise Analysis

Material Type Insights

The epoxy flooring segment is expected to dominate, holding an approximately 42.5% market share in 2025. Its leadership is driven by superior resistance to chemicals, abrasion, and heavy loads, along with its seamless finish that ensures durability and ease of maintenance.

These qualities make epoxy the preferred choice in diverse environments such as manufacturing plants, chemical facilities, warehouses, and cleanrooms where operational efficiency and long service life are critical. The combination of performance, cost-effectiveness, and versatility continues to reinforce epoxy’s dominant market position.

The polyurethane flooring segment is the fastest growing. Unlike epoxy, polyurethane offers greater flexibility, thermal shock resistance, and exceptional abrasion tolerance, making it well-suited for food and beverage facilities, pharmaceuticals, and high-traffic production areas.

Its ability to withstand temperature fluctuations and mechanical stress gives it a competitive edge in industries where operational environments are more demanding, which explains its rapid adoption and growth trajectory. At tank wash facilities, polyurethanes such as the FPX 9520 Solvented CRU formula withstand constant moisture, abrasive cleaners, and thermal cycling, making them ideal for challenging industrial zones.

Flooring Structure Insights

Medium-duty flooring (2-4 mm) is projected to lead with the largest market share at around 45% in 2025. This thickness range balances durability with cost efficiency, making it widely adopted across applications, such as food processing, pharmaceutical production, packaging units, and general manufacturing facilities. It is durable enough to handle frequent foot and equipment traffic, yet economical, making it the most practical choice for industries that require hygienic, resilient flooring without incurring the higher costs of heavy-duty alternatives.

The heavy-duty flooring segment (>4 mm) is the fastest-growing. Its appeal lies in the ability to withstand extreme load conditions, chemical exposure, and high-impact activities. Heavy-duty flooring is increasingly chosen for warehouses handling forklifts, automotive assembly units, and chemical processing facilities, where performance and longevity are non-negotiable. The rise in global infrastructure investments, growth of automated logistics hubs, and expansion of heavy manufacturing are all contributing to the accelerated uptake of heavy-duty flooring systems.

Regional Insights

Asia Pacific Industrial Flooring Market Trends - Manufacturing Expansion and Data-Center Development Fueling Market Growth

Asia Pacific is projected to be the largest and fastest-growing region with a market share of 35.9% in 2025. Growth is fueled by rapid industrialization, large-scale manufacturing expansion, and strong investments in e-commerce and logistics infrastructure. China continues to dominate, with widespread adoption of epoxy systems for factories, industrial parks, and cleanrooms.

The surge in semiconductor and EV battery plant construction has created niche demand for conductive and ESD epoxy flooring solutions, essential for protecting sensitive equipment. India is emerging as a high-growth market, where food processing, pharmaceutical production, and industrial parks are fueling demand for both epoxy and polyurethane floors. Increasingly, facility owners are investing in complete flooring system upgrades that include surface preparation, moisture mitigation, and resinous coatings to ensure compliance and performance.

The region’s rapid pace of construction and its emphasis on cost-effective and durable flooring solutions make it the global growth engine for industrial flooring. For instance, in November 2024, Flowcrete Asia introduced a carbon-fiber-free ESD epoxy floor using single-walled carbon nanotubes for more consistent conductivity and better aesthetics, addressing the hotspots and discoloration issues linked with traditional carbon-fiber flooring.

North America Industrial Flooring Market Trends - E-commerce Expansion and Cold-Chain Infrastructure Driving Flooring Demand

North America represents a mature yet steadily growing market, where the focus has shifted toward performance-driven solutions rather than basic material supply. The rising adoption of heavy-duty epoxy and fast-curing MMA flooring is evident across warehouses, cold storage facilities, and pharmaceutical plants, particularly as companies prioritize rapid installation, chemical resistance, and long-term durability.

In the U.S., the surge in e-commerce fulfillment centers and automated warehouses has increased the demand for resinous systems designed to withstand forklift traffic, minimize downtime, and support hygienic operations. Leading suppliers such as Sherwin-Williams and Sika are responding with case-specific flooring systems that highlight metrics such as return-to-service hours and lifecycle performance.

In Canada, retrofit activity is accelerating, especially in food and pharmaceutical facilities, where seamless, hygienic flooring solutions are being adopted to meet stringent standards. This retrofit wave, combined with expanding cold-chain logistics, positions Canada as one of the fastest-growing markets in the region.

Europe Industrial Flooring Market Trends - Hygiene Standards and Sustainability Shaping Flooring Choices

In Europe, the market is characterized by premium specifications, stringent hygiene requirements, and a growing emphasis on sustainability. Resinous systems are widely adopted in food processing plants, pharmaceutical facilities, and cleanrooms, where buyers require certified hygienic floors with documented performance on VOC levels and durability.

Germany leads the region, with strong demand from automotive assembly lines, chemical facilities, and precision manufacturing plants. Here, thick epoxy and polyurethane floors are preferred for their ability to withstand heavy mechanical loads, chemical exposure, and long operational lifecycles.

In the U.K., the market is being shaped by healthcare refurbishments, pharmaceutical cleanroom retrofits, and upgrades in food and beverage processing plants. Projects are increasingly awarded to suppliers and contractors that can deliver fast installation, jointless finishes, and proven hygienic performance.

As European buyers continue to demand both sustainability credentials and operational reliability, suppliers that provide low-VOC, traceable resin solutions with certified installation support are expected to maintain a competitive edge. For instance, at Volac’s dairy processing plant in West Wales (U.K.), approximately 1,576 m² of Stonhard Stonclad GS epoxy was installed across four floors, topped with Stonkote HT4 for enhanced chemical resistance, abrasion protection, and slip safety.

Competitive Landscape

The global industrial flooring market is moderately fragmented, with global leaders such as Sika AG, BASF SE, RPM International Inc., Sherwin-Williams, and Mapei S.p.A., competing alongside regional players that specialize in tailored installation and project-specific solutions.

These companies are actively expanding their portfolios of resinous and hybrid flooring systems, focusing on performance attributes such as chemical resistance, rapid curing, and hygiene compliance. Strategic acquisitions, partnerships with contractors, and targeted investments in emerging markets are common approaches to strengthening market presence.

Innovation is also shaping competition, with key players investing in sustainable, low-VOC formulations and digital tools for project design and lifecycle management. Regional specialists in Asia Pacific and Europe are leveraging faster turnaround times and localized technical expertise to capture niche opportunities, particularly in manufacturing, cleanrooms, and food processing facilities. As end-users increasingly prioritize speed, compliance, and long-term durability, suppliers that combine material innovation with reliable installation support are gaining a competitive edge.

Key Industry Developments

- In April 2025, Epoxy Flooring McKinney announced its expanded Commercial Solutions Portfolio for North Texas. This newly developed range of industrial-grade epoxy formulations targets high-traffic commercial and retail environments, emphasizing faster installation, superior chemical and impact resistance, and compliance with VOC and slip-resistance standards.

- In July 2024, Sherwin-Williams Protective & Marine Coatings rolled out a specialized flooring system developed specifically for EV battery manufacturing facilities. The new system was designed to resist harsh chemicals, control electrostatic discharge (ESD), and enhance slip resistance.

Companies Covered in Industrial Flooring Market

- Sika AG

- BASF SE

- RPM International Inc. (Stonhard, Tremco, Flowcrete brands)

- Mapei S.p.A.

- Sherwin-Williams Company

- Fosroc International Ltd.

- Ardex Group

- CEMEX S.A.B. de C.V.

- Pervious Concrete Inc.

- Nichiha Corporation

- Altro Group Plc

- Tikkurila Oyj (now part of PPG Industries)

- Beckers Group

- Asian Paints PPG Pvt. Ltd.

- Berger Paints India Ltd.

- König + Co. GmbH

- Flowcrete Group (part of RPM International)

- Huntsman International LLC

- 3M Company (Industrial Coatings & Flooring Solutions)

- AkzoNobel N.V.

Frequently Asked Questions

The global industrial flooring market size is estimated at US$9.98 Bn in 2025.

By 2032, the market is projected to reach US$14.81 Bn.

The market is witnessing strong momentum in eco-friendly epoxy flooring, rapid-cure polyurethane systems, and hybrid flooring technologies, and growing adoption of anti-microbial coatings in cleanrooms.

The epoxy flooring segment dominates with over 42.5% share in 2025, favored for its durability and chemical resistance.

The market is expected to expand at a CAGR of 5.8% from 2025 to 2032, driven by increasing demand from manufacturing, pharmaceuticals, and advanced warehousing facilities.

Key players include Sika AG, BASF SE, RPM International Inc. (Tremco & Stonhard brands), Mapei S.p.A., and Sherwin-Williams.