- Automotive Components & Materials

- Automotive Thermostat Market

Automotive Thermostat Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Thermostat Market By Thermostat Type (Electronic, Mechanical and Programmable), Component Type (Single Valve, and Dual Valve), Vehicle Type (Passenger Cars, and Commercial Vehicles) and Regional Analysis for 2025 - 2032

Automotive Thermostat Market Size and Trends Analysis

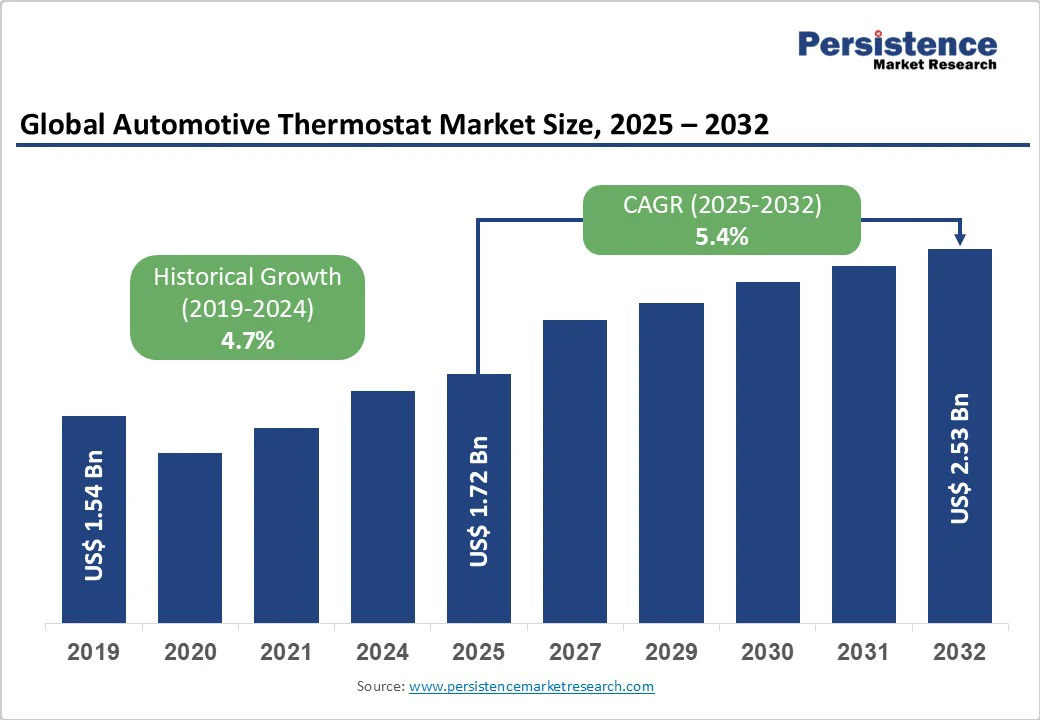

The global automotive thermostat market size was valued at US$ 1.72 billion in 2025 and is projected to reach US$ 2.53 billion by 2032, growing at a CAGR of 5.4% between 2025 and 2032.

This robust growth trajectory reflects the automotive industry's increasing emphasis on thermal management efficiency, driven by stringent emission regulations and rising demand for fuel-efficient vehicles.

Key Industry Highlights:

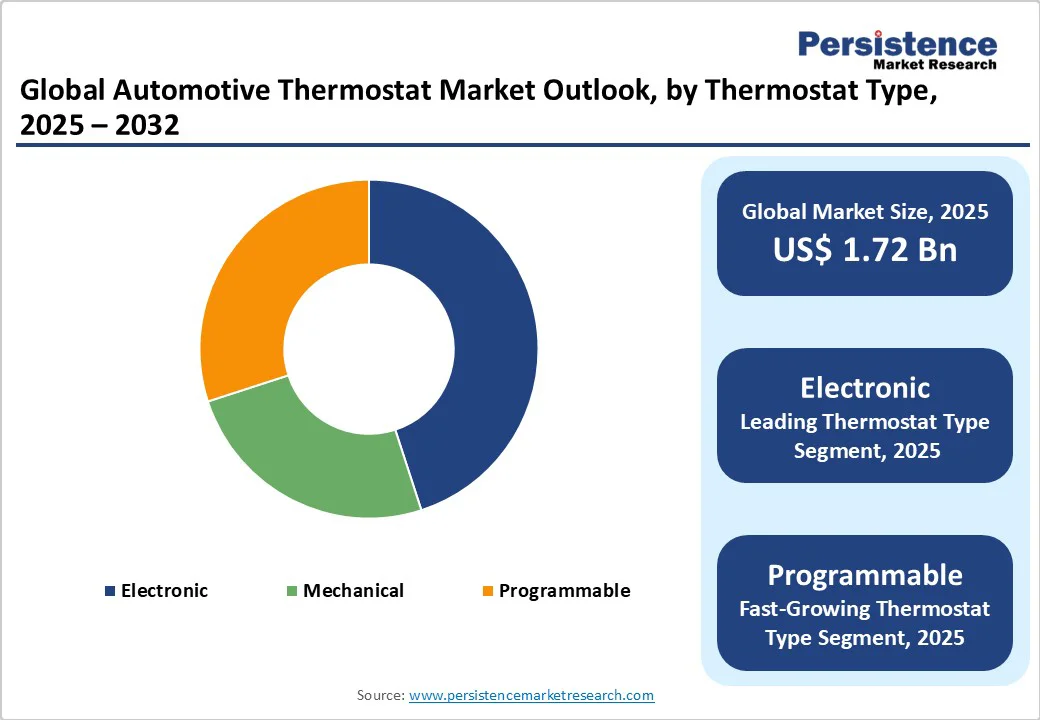

- Product Segments: Electronic thermostats dominate the market with a 54.3% share in 2025, driven by their superior temperature precision, integration with advanced vehicle systems, and compatibility with electronic control units. The programmable thermostat segment is the fastest-growing, supported by rising demand for adaptive and energy-efficient thermal management in modern vehicles.

- Component Segments: Dual valve thermostats lead with a 64.3% share, offering enhanced coolant flow control and efficiency for high-performance engines. Meanwhile, single valve systems record the fastest growth rate, favored for their cost-effectiveness, simpler design, and manufacturing scalability in compact vehicle applications.

- Vehicle Segments: Passenger cars dominate with a 67.4% share, reflecting high global production volumes and increasing integration of smart temperature control systems. Commercial vehicles exhibit the fastest growth, driven by fleet modernization, emission standards, and expansion in the logistics and transportation sectors.

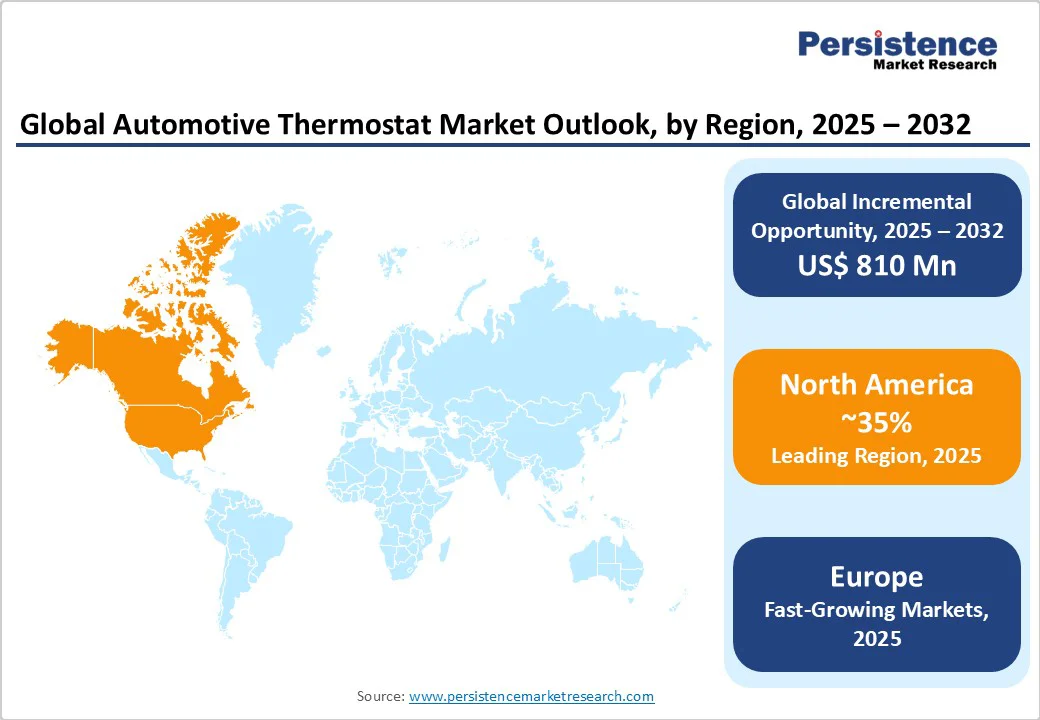

- Regional Leaders: North America remains a key leader, projected to achieve a 6.6% CAGR and reach US$ 1.9 billion by 2032, supported by advanced automotive manufacturing and regulatory compliance. Asia Pacific shows the strongest growth, underpinned by surging vehicle production, rapid electrification, and expanding consumer markets in China and India.

- Strategic Market Developments: The industry is witnessing structural shifts and innovation-led growth MAHLE’s divestiture of its thermostat operations to ADMETOS (May 2024) highlights a strategic pivot toward electrification, while MotoRad’s launch of over 50 new products underscores continuous investment in product diversification and advanced temperature management technologies.

| Key Insights | Details |

|---|---|

| Automotive Thermostat Market Size (2025E) | US$ 1.72 Bn |

| Market Value Forecast (2032F) | US$ 2.53 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Dynamics

Stringent Emission Regulations and Fuel Efficiency Standards

Global automotive emission standards continue to tighten, with regulatory bodies implementing increasingly stringent requirements for vehicle manufacturers. The U.S. Corporate Average Fuel Economy (CAFE) standards and European Union emission regulations mandate significant improvements in fuel efficiency, directly driving demand for advanced thermal management systems.

Automotive thermostats play a crucial role in maintaining optimal engine operating temperatures, which can improve fuel efficiency by up to 15% and reduce harmful emissions by precisely controlling the flow of coolant. According to industry data, nearly 70% of engine-related performance issues are attributed to inefficient temperature control, underscoring the crucial importance of advanced thermostat systems in meeting regulatory compliance requirements.

Rapid Vehicle Electrification and Hybrid Adoption

The global shift toward electric and hybrid vehicles presents significant growth opportunities for sophisticated thermal management solutions. According to the International Energy Agency, global electric vehicle sales surged by 43% in 2020, emphasizing the transition toward greener automotive technologies.

Electric and hybrid vehicles require specialized thermal management for battery systems, power electronics, and motors, creating new applications beyond traditional engine cooling. These advanced powertrain systems demand precise temperature control to optimize battery performance, extend component lifespan, and maintain system efficiency across varying operating conditions.

The integration of thermal management systems in electric vehicles represents a market expansion opportunity valued at over $2 billion through 2032.

Restraint - High Development and Manufacturing Costs

Advanced electronic thermostats and MAP-controlled systems require significant investment in research and development, sophisticated manufacturing processes, and specialized materials. The complexity of modern thermal management systems, particularly those designed for hybrid and electric vehicles, results in higher production costs compared to traditional mechanical thermostats.

Development costs for electronically actuated thermostats can exceed $16,000 per unit for commercial vehicle applications, creating cost barriers for widespread adoption. These elevated costs impact profit margins and may limit market penetration in price-sensitive automotive segments, particularly in emerging markets where cost competitiveness remains paramount.

Supply Chain Vulnerabilities and Raw Material Price Volatility

The automotive thermostat market faces ongoing challenges from supply chain disruptions and fluctuating raw material costs, including specialized metals, electronic components, and manufacturing materials. Global semiconductor shortages have particularly impacted production of electronic thermostats, delaying delivery and forcing manufacturers to redesign products around available components.

Raw material price volatility affects manufacturing cost predictability, making it difficult for suppliers to maintain consistent pricing and profit margins. Additionally, the concentration of manufacturing capabilities in specific geographic regions creates vulnerability to localized disruptions, affecting global supply chains and market stability.

Market Opportunities

Emerging Market Expansion and Urbanization

Rapid economic development in Asia Pacific, Latin America, and Middle East regions presents substantial growth opportunities for automotive thermostat manufacturers. Rising disposable incomes, urbanization trends, and improving road infrastructure drive increased vehicle ownership in these markets. Countries such as India, China, and Brazil are experiencing significant automotive production growth, creating demand for thermal management components.

The expanding middle class in these regions increasingly prioritizes fuel efficiency and vehicle reliability, supporting the adoption of advanced thermostat technologies. Market sizing estimates suggest emerging markets could contribute over $800 million in additional thermostat demand through 2032.

Integration with Smart Vehicle Technologies

The convergence of automotive thermal management with Internet of Things (IoT), connected vehicle platforms, and autonomous driving systems creates new market opportunities. Future thermal management systems will integrate with vehicle telematics, predictive maintenance platforms, and smart grid technologies.

These applications enable remote monitoring, predictive failure analysis, and optimal energy management across vehicle systems. The market opportunity for smart thermal management integration is projected to reach $1.5 billion by 2032, driven by consumer demand for connected vehicle experiences and fleet management efficiencies.

Category Insights

Thermostat Type Analysis

Electronic thermostats hold a dominant 54.3% share in 2025, supported by their superior precision and seamless integration with modern engine management systems. Using advanced sensors and actuators, these thermostats deliver real-time temperature control with faster response and higher accuracy than mechanical variants. Their compatibility with vehicle ECUs enables intelligent thermal optimization based on load, ambient conditions, and driving behavior.

Programmable thermostats represent the fastest-growing segment, driven by the need for adaptive, energy-efficient thermal systems in both passenger and commercial vehicles. These thermostats can be preconfigured to specific driving conditions, improving fuel efficiency and performance. Emerging innovations in machine learning are enhancing their ability to learn vehicle patterns, enabling predictive and self-adjusting temperature regulation.

Component Type Analysis

Dual valve thermostats dominate with a 64.3% share in 2025, owing to their superior coolant flow control and precise thermal management. Featuring two separate valve mechanisms, these systems enable graduated coolant regulation, reducing thermal shock and maintaining consistent engine temperatures across varying loads. The improved mixing of hot and cold coolant supports engine performance and longevity, making dual valve designs preferred in high-performance and commercial vehicle applications.

In contrast, single valve thermostats are the fastest-growing component segment, driven by cost optimization, simplified manufacturing, and adequate thermal performance for standard passenger vehicles. Innovation focuses on enhancing response speed and durability to remain competitive with dual valve systems. This segment benefits particularly from rising demand in emerging markets, where affordability and efficiency are key purchasing considerations.

Vehicle Type Analysis

Passenger cars dominate the automotive thermostat market with a 67.4% share, supported by high global production volumes and steady replacement demand through regular maintenance cycles. Increasing adoption of advanced engine technologies such as turbocharging and direct injection necessitates precise thermal management, while growing consumer focus on fuel efficiency and environmental impact further boosts segment demand.

Commercial vehicles are the fastest-growing segment, driven by expanding logistics operations, e-commerce growth, and fleet modernization initiatives. These applications require durable thermal management solutions capable of sustaining extended operating cycles, heavy loads, and harsh environments. Fleet operators prioritize fuel efficiency and maintenance cost reduction, while regulatory emission standards and telematics-based monitoring systems further accelerate the adoption of advanced thermostat technologies in.

Regional Market Insights

North America Market Analysis

North America represents a significant market valued at US$ 1.1 billion in 2025. The United States dominates regional share, driven by mature automotive infrastructure, stringent emission regulations, and high vehicle ownership rates.

The region benefits from established automotive manufacturing capabilities and significant aftermarket demand supporting consistent revenue streams. Regulatory frameworks including EPA emission standards and CAFE fuel economy requirements drive adoption of advanced thermal management technologies.

The North American market demonstrates strong innovation leadership through partnerships between automotive manufacturers, technology companies, and research institutions. Advanced manufacturing capabilities and consumer preference for premium vehicle features support adoption of electronic and programmable thermostat systems.

The regional market benefits from growing electric vehicle adoption, particularly in California and other progressive states implementing zero-emission vehicle mandates. Investment trends focus on thermal management solutions for battery electric and hybrid electric vehicles, creating new growth opportunities beyond traditional combustion engines.

Europe Automotive Thermostat Market Analysis

Europe maintains a substantial position with Germany leading innovation and manufacturing excellence in automotive thermal management systems. The region's automotive industry traditionally leads technological development, with German manufacturers pioneering advanced engine cooling solutions and electronic thermostat integration.

European Union emission regulations drive continuous innovation in thermal management efficiency, supporting market growth for advanced thermostat technologies. The region benefits from strong automotive export capabilities and established supply chain networks.

Key countries including Germany, France, and the United Kingdom demonstrate consistent growth driven by premium vehicle production and increasing adoption of hybrid powertrains. European manufacturers focus on developing sustainable thermal management solutions aligned with circular economy principles and environmental regulations.

The regulatory environment emphasizes vehicle electrification and emission reduction, creating opportunities for advanced thermostat technologies. Investment patterns reflect growing focus on electric vehicle thermal management and integration with renewable energy systems.

Asia Pacific Market Analysis

Asia Pacific represents the fastest-growing regional market, driven by substantial automotive production capabilities in China, Japan, India, and South Korea. China leads regional production volumes and domestic market demand, benefiting from government support for automotive industry development and electric vehicle adoption incentives.

Japan contributes technological innovation and premium manufacturing capabilities, particularly in hybrid vehicle thermal management systems. India demonstrates rapidly expanding automotive production and growing domestic consumer demand for passenger vehicles.

The region benefits from cost-competitive manufacturing capabilities, established supply chain infrastructure, and growing middle-class consumer base driving vehicle ownership expansion. ASEAN countries contribute growing automotive assembly operations and component manufacturing capabilities.

Investment trends focus on expanding production capacity, developing local supply chains, and supporting electric vehicle infrastructure development. The regional market demonstrates strong growth potential driven by urbanization, infrastructure development, and increasing environmental awareness.

Automotive Thermostat Market Competitive Landscape

The global automotive thermostat market exhibits moderate consolidation with leading players maintaining significant market shares through established distribution networks, technological capabilities, and customer relationships. Major multinational corporations including BorgWarner Inc., MAHLE GmbH, Gates Corporation, and Stant Corporation dominate market leadership positions through comprehensive product portfolios and global manufacturing presence.

Market concentration analysis reveals opportunities for strategic acquisitions and partnerships to enhance geographic coverage and technology capabilities. Regional players compete effectively in specific market segments through specialized applications and cost advantages.

Key Industry Developments

- In February 2025, MotoRad announced over 50 new thermal management products, expanding coverage across European, Asian, and American vehicle brands. The new product release includes advanced thermostat applications for leading vehicle manufacturers, ensuring optimal performance and reliability for modern engines.

- In May 2024, MAHLE finalized the sale of its OEM thermostat business to ADMETOS, transferring approximately 600 employees across six countries under the new BTT Solutions brand. This strategic divestiture reflects MAHLE's focus on electrification and systems for thermal management while maintaining aftermarket thermostat sales under MAHLE and Behr brands

Companies Covered in Automotive Thermostat Market

- BorgWarner Inc.

- AC Delco

- Gates Corporation

- Continental AG

- Hella KGaA Hueck & Co.

- MAHLE GmbH

- MotoRad Ltd.

- Robert Bosch GmbH

- Valeo SA

- Stant Manufacturing, Inc.

- Tama Enterprises Co., Ltd.

- Nippon Thermostat Co. Ltd.

- Other Market Players

Frequently Asked Questions

The Automotive Thermostat market is estimated to be valued at US$ 1.72 Bn in 2025.

A key demand driver for the Electric Two-Wheelers (E2W) market is the growing environmental awareness and stricter emissions regulations, prompting consumers and governments to move away from fossil-fuel powered vehicles toward cleaner, low-carbon transportation.

In 2025, North America region will dominate the market with an exceeding 30% revenue share in the global Automotive Thermostat market.

Among the Equipment Type, Passenger Service Equipment holds the highest share in 2025, surpassing other parts.

The key players in the Automotive Thermostat market are ITW GSE, Textron GSE, Wilcox GSE, Air+MAK Industries, and TLD Group