- Food Ingredients & Additives

- Food Grade Phosphate Market

Food Grade Phosphate Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Food Grade Phosphate Market by Category (Ammonium Phosphate, Sodium Phosphate, Potassium, Phosphate, Calcium Phosphate, Others), by Application, and Regional Analysis from 2025 to 2032

Food Grade Phosphate Market Size and Trends Analysis

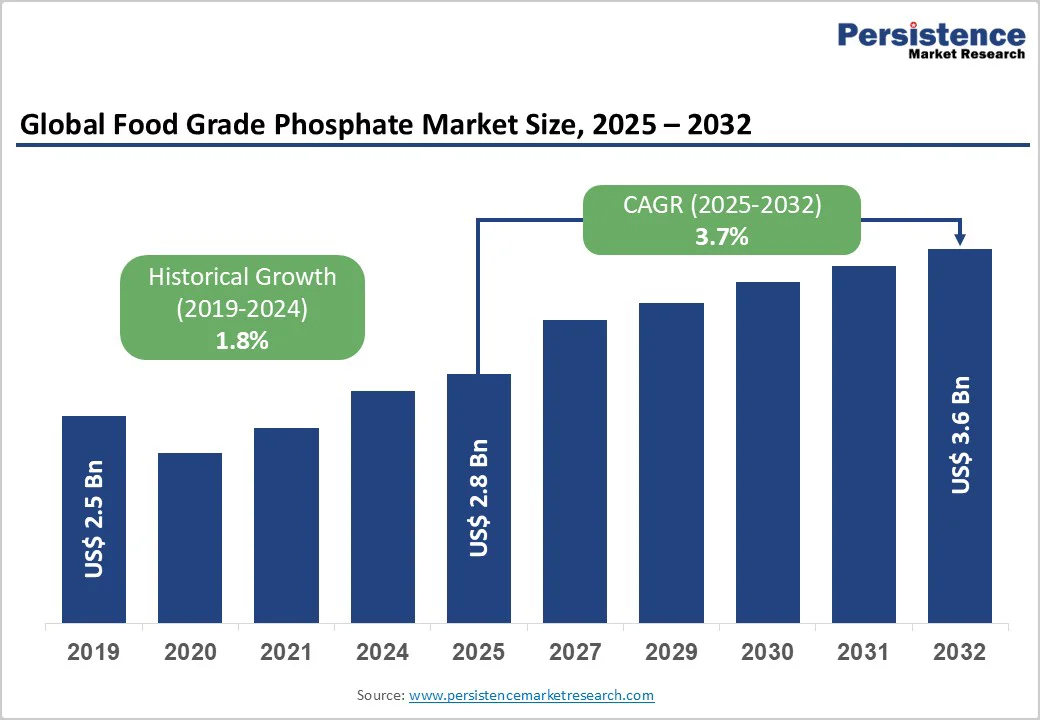

The global food grade phosphate market size is likely to value US$2.8 billion in 2025 and projected to reach US$3.6 billion growing at a CAGR of 3.7% during the forecast period from 2025 to 2032.

The global food grade phosphate market is experiencing steady growth driven by its extensive use as an emulsifier, stabilizer, and preservative in food processing. Food grade phosphates enhance texture, moisture retention, and shelf life in products such as meat, bakery, dairy, and seafood.

Rising consumption of processed and convenience foods, coupled with growing demand for quality enhancement in packaged items, fuels market expansion. Additionally, increasing urbanization, evolving dietary habits, and technological advancements in food manufacturing further strengthen demand.

Key Industry Highlights:

- The growing demand for processed and convenience foods worldwide is the primary driver of the food grade phosphate market.

- Food grade phosphates are widely used in meat and poultry processing to enhance water retention, tenderness, and color stability.

- Food grade phosphates improve multiple attributes such as pH regulation, emulsification, and mineral fortification.

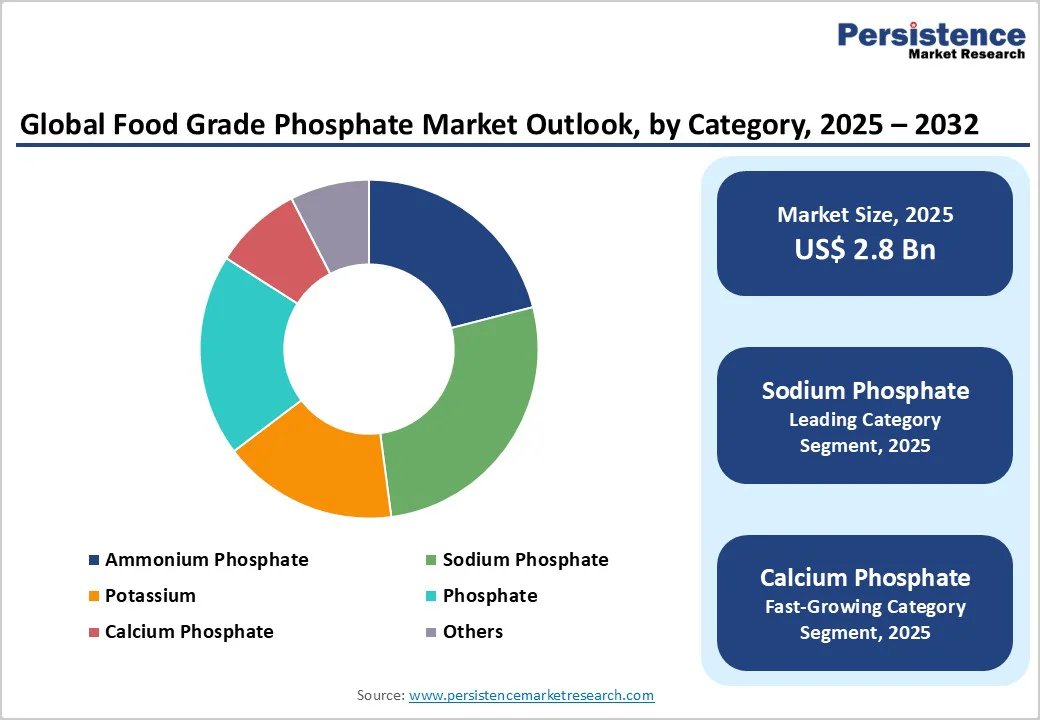

- The sodium phosphate segment holds the highest share in the global food grade phosphate market due to its versatility, functionality, and cost efficiency across multiple food applications.

| Key Insights | Details |

|---|---|

| Food Grade Phosphate Market Size (2025E) | US$2.8 Bn |

| Market Value Forecast (2032F) | US$3.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 1.8% |

Market Dynamics

Driver - Growth of Quick-Service Restaurants (QSRs)

The rapid expansion of Quick-Service Restaurants (QSRs) worldwide has become a key driver for the food grade phosphate market. With increasing consumer demand for ready-to-eat meals, burgers, pizzas, and bakery-based snacks, QSRs rely heavily on processed ingredients such as meat, cheese, and dough that require consistent texture and extended shelf life.

Food grade phosphates play a crucial role in improving moisture retention, tenderness, and emulsification, ensuring product stability during mass production and storage. As global fast-food chains continue expanding into emerging markets and adopting standardized food formulations, the use of phosphates in maintaining product quality, flavor, and freshness has become indispensable.

Restraints - Health Concerns Over Phosphate Intake

Health concerns over phosphate intake have emerged as a major restraint in the food grade phosphate market. Studies indicate that excessive consumption of phosphates, especially through processed foods, can disrupt the body’s mineral balance and contribute to kidney dysfunction, cardiovascular complications, and reduced bone density.

These health risks are particularly significant among individuals with pre-existing renal or metabolic conditions. As consumer awareness grows, regulatory bodies such as the FDA and EFSA are tightening permissible phosphate limits in food formulations.

Food manufacturers are also facing increased pressure to reformulate products and adopt safer or natural alternatives. Consequently, these health-related apprehensions are driving a noticeable shift toward phosphate-free and clean-label products, restraining overall market expansion.

Opportunity - Phosphate Recycling and Sustainability

Phosphate recycling and sustainability presents a transformative opportunity in the food grade phosphate market. As global demand for phosphates grows, traditional mining and production face environmental and resource limitations. By innovating sustainable sourcing methods and recycling phosphates from food processing waste, agricultural by-products, or wastewater streams, manufacturers can reduce ecological impact while ensuring a reliable long-term supply.

Such practices not only minimize reliance on finite natural reserves but also contribute to circular economy initiatives. Additionally, recycled phosphates can be refined to meet stringent food grade standards, supporting regulatory compliance. Growing consumer and industry emphasis on sustainability further enhances the market potential of eco-friendly phosphate solutions, positioning this approach as a key growth driver.

Category-wise Analysis

By Category Insights

The sodium phosphate segment commands the highest share in the global food grade phosphate market due to its versatile functionality, cost-effectiveness, and regulatory acceptance. It acts as an emulsifier, stabilizer, leavening agent, and pH regulator, making it essential across meat, dairy, seafood, and bakery products. Sodium phosphate enhances water retention, texture, and shelf life, ensuring consistent quality in large-scale food production.

Its availability in various forms-mono-, di-, and tri-sodium phosphates-offers flexibility for diverse formulations. Combined with ease of handling, wide industrial adoption, and compatibility with clean-label initiatives, sodium phosphate remains the most widely used and preferred phosphate globally.

By Application Insights

The food and beverages segment holds the highest share in the global food grade phosphate market due to its widespread use across diverse food applications. Phosphates act as emulsifiers, stabilizers, leavening agents, and pH regulators, enhancing texture, moisture retention, and shelf life in products such as dairy, bakery, beverages, and processed foods.

Their multifunctionality ensures consistent quality, improved sensory attributes, and reduced spoilage, which is critical for large-scale food manufacturing. Rising consumer demand for convenience foods, ready-to-eat meals, and clean-label products further drives adoption. The extensive application scope and essential functional benefits make food and beverages the dominant segment globally.

Region-wise Insights

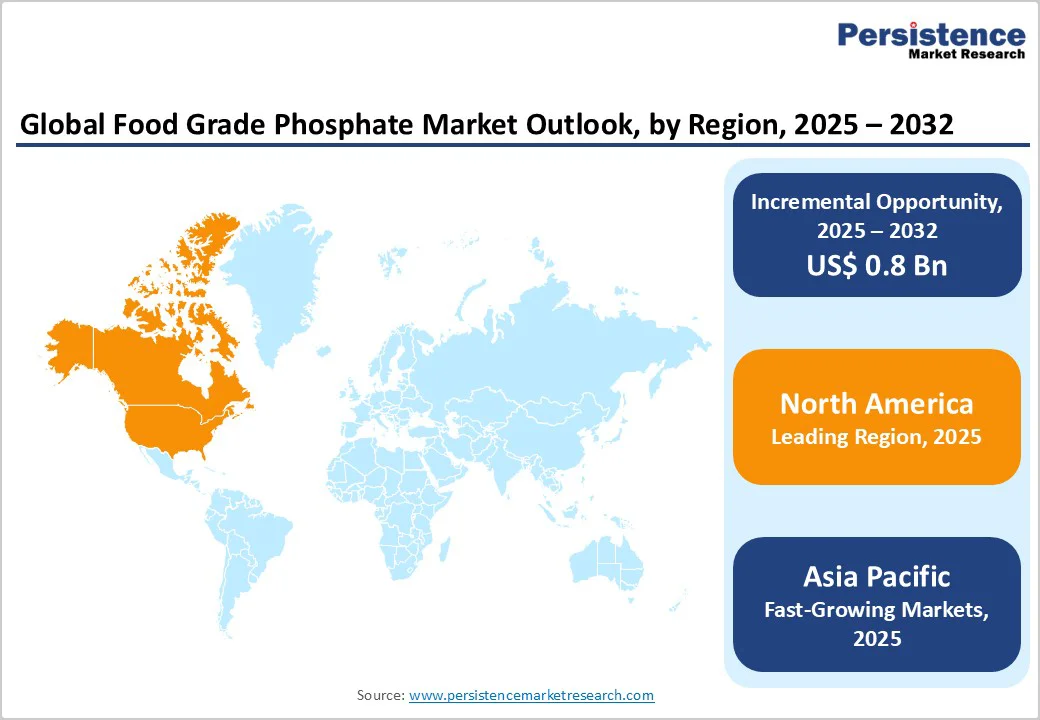

North America Food Grade Phosphate Market Trends

North America, particularly the U.S., leads the global almond flour market due to the region’s high health-conscious consumer base and growing demand for gluten-free, keto, and low-carb products. Almond flour is increasingly used in bakery, confectionery, and snack applications for its nutritional benefits, including high protein, fiber, and healthy fats. Rising awareness of plant-based and clean-label ingredients drives its adoption in both retail and foodservice sectors.

Additionally, well-established almond cultivation, advanced processing infrastructure, and strong distribution networks support consistent supply. Innovation in almond-based products and increasing home-baking trends further reinforce North America’s position as the dominant market.

Asia Pacific Food Grade Phosphate Market Trends

Asia Pacific is emerging as a high-growth region in the global food grade phosphate market, driven by rapid urbanization, rising disposable incomes, and increasing consumption of processed and convenience foods. Countries such as China, India, and Japan are witnessing growing demand for bakery, dairy, meat, and beverage products, which rely on phosphates for texture, emulsification, and shelf-life enhancement.

Expanding food processing industries, coupled with improving cold-chain infrastructure and regulatory support, are facilitating phosphate adoption. Additionally, evolving dietary preferences toward fortified and functional foods, along with rising awareness of clean-label ingredients, position Asia Pacific as a key emerging market with significant growth potential.

Competitive Landscape

The global food grade phosphate market exhibits a highly competitive landscape, characterized by a mix of multinational corporations and regional suppliers striving for market leadership. Companies are investing in product innovation, high-purity formulations, and sustainable sourcing to differentiate their offerings. Strategic collaborations, mergers, and capacity expansions are common to enhance geographic reach and supply reliability.

Key Industry Developments:

- In February 2025, Prayon announced the construction of a new electronic-grade phosphoric acid production unit in Bex, Switzerland. The investment aimed to double production capacity to meet the growing demand for ultrapure phosphoric acid, particularly driven by the reshoring of the rapidly expanding semiconductor market in Europe and the United States.

Companies Covered in Food Grade Phosphate Market

- Prayon S.A.

- ICL

- PhosAgro Group

- Ettlinger Corporation

- Hindustan Phosphates Pvt.Ltd.

- Nutrein Ltd.

- OCP Group

- TKI Hrastnik, d.d.

- Innophos.

- FOSFA

- NutriScience Inoovations LLC.

- Budenheim

- Sulux Phosphates Limited

- Xingfa USA

- Natural Enrichment Industries

- Qingdao Samin Chemical Co., Ltd.

- Aditya Birla Chemicals

- Compagnie Financiere et de Participations Roullier S.A.

- Other

Frequently Asked Questions

The global food grade phosphate market is projected to be valued at US$2.8 Bn in 2025.

Increasing demand for processed, convenience, and ready-to-eat foods drives phosphate use as an emulsifier, stabilizer, and preservative.

The global food grade phosphate market is poised to witness a CAGR of 3.7% between 2025 and 2032.

Enhancing texture, moisture retention, and protein stability in vegan meat, dairy, and egg alternatives.

Prayon S.A., ICL, PhosAgro Group, Ettlinger Corporation, Hindustan Phosphates Pvt.Ltd, and others.