- Food Ingredients & Additives

- Food Enzymes Market

Food Enzymes Market Size, Share, and Growth Forecast, 2025 - 2032

Food Enzymes Market By Source (Microbial Enzymes, Plant-derived Enzymes) Enzyme Type (Carbohydrases, Proteases), Application, and Regional Analysis for 2025 - 2032

Food Enzymes Market Size and Trends Analysis

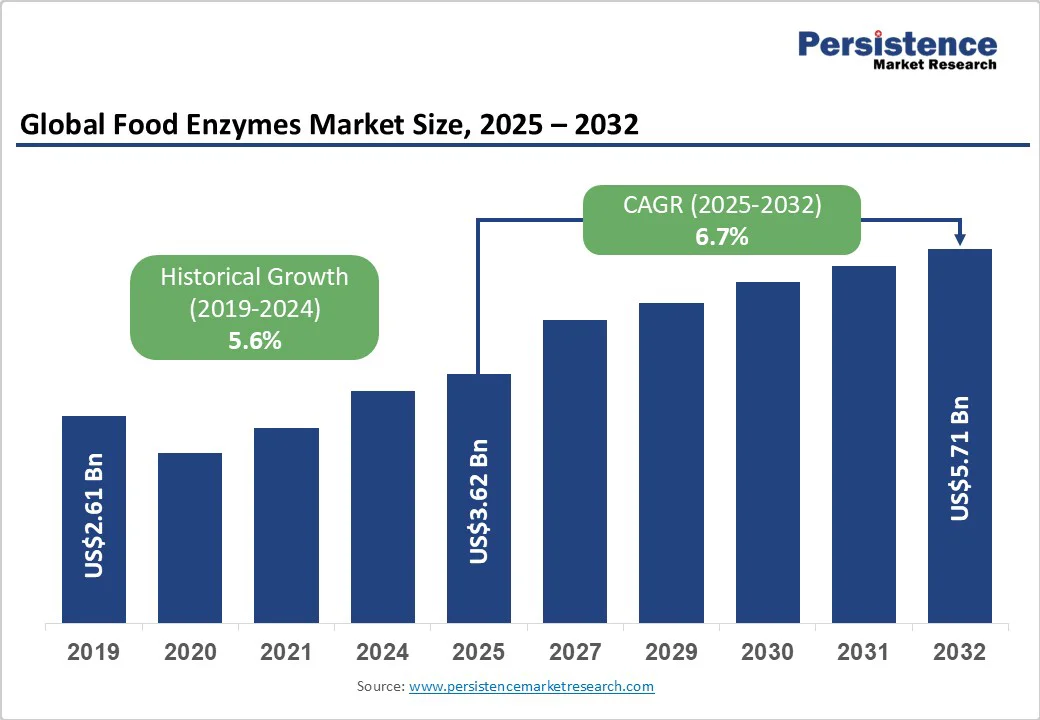

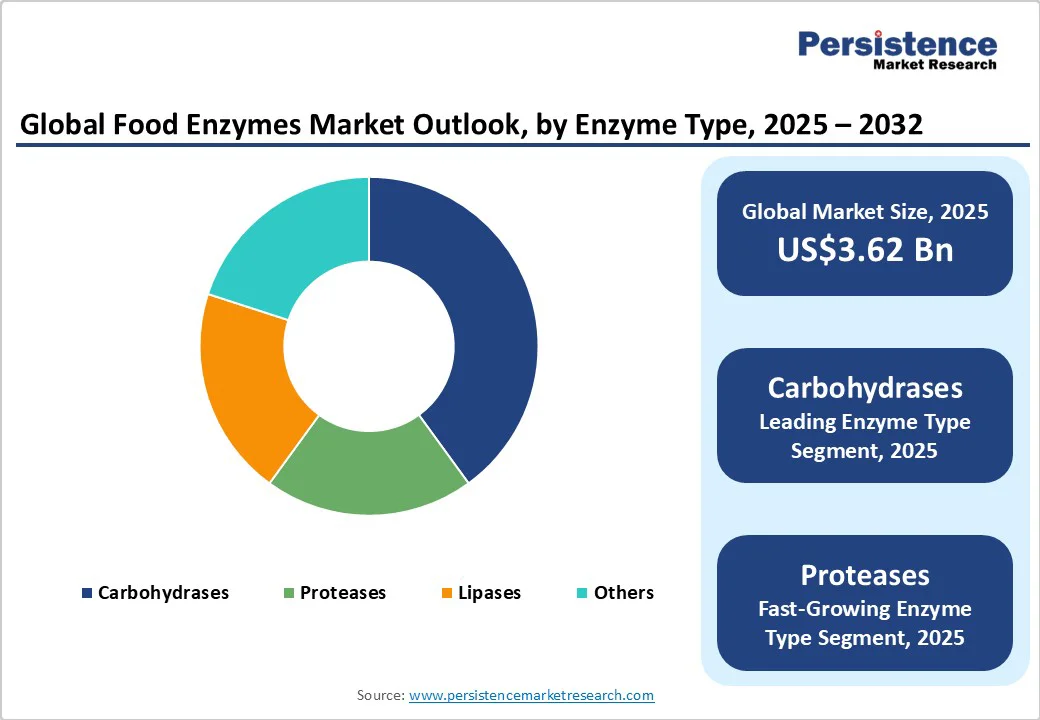

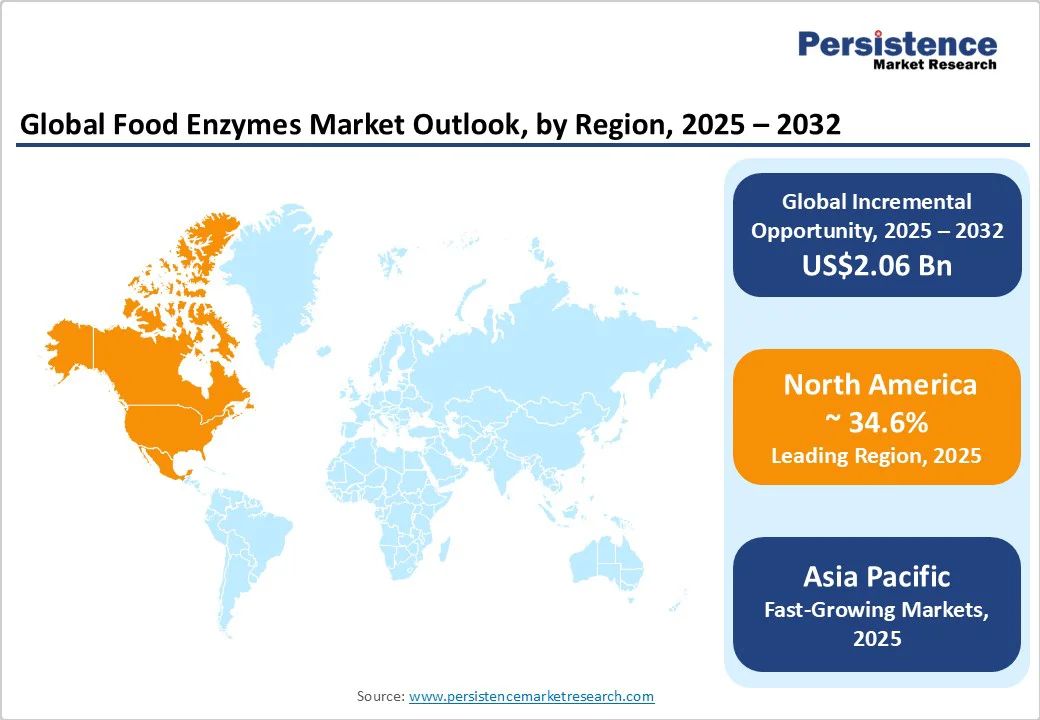

The global food enzymes market size is likely to be valued at US$3.62 Bn in 2025. It is expected to reach US$5.71 billion by 2032, growing at a CAGR of 6.7% during the forecast period from 2025 to 2032, driven by food manufacturers’ increasing adoption of enzymes for clean-label reformulations, cost efficiency, and enhanced functionality in the bakery, dairy, and beverage sectors.

The rising consumption of processed food, stricter regulatory approvals to ensure safety, and technological innovation in fermentation are also key growth drivers.

Key Industry Highlights

- Leading Region: North America, holding 34.6% of the global market share in 2025, supported by advanced fermentation capacity, strong bakery and dairy industries, and a predictable GRAS-based regulatory framework.

- Fastest-growing Region: Asia Pacific, projected to grow at a CAGR of 8.2% between 2025 and 2032, driven by urbanization, rising packaged food consumption, and manufacturing scale-up in China, India, and ASEAN.

- Investment Plans: Significant expansions in fermentation infrastructure in North America and Europe, alongside rising precision fermentation investments in Europe and joint ventures in Asia Pacific.

- Dominant Enzyme Type: Carbohydrases, contributing over 40% of total revenues in 2025, led by applications in bakery, beverages, and sweeteners.

- Leading Application: Bakery segment, holding over 36% of global revenues in 2025, supported by high bread and confectionery production.

| Key Insights | Details |

|---|---|

|

Food Enzymes Market Size (2025E) |

US$3.62 Bn |

|

Market Value Forecast (2032F) |

US$5.71 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Clean-Label, Health-Led Reformulation and Process Efficiency

Consumer demand for natural, transparent ingredient lists and minimally processed foods has structurally shifted formulation choices. Clean-label claims now drive higher enzyme substitution, replacing synthetic additives in bakery, dairy, and beverages. Regulators such as EFSA have introduced strict evaluation frameworks that support enzymes as safe alternatives. The impact is a measurable increase in enzyme penetration across large food categories, raising both per-unit consumption of enzymes and the value of reformulation projects.

Enzymes deliver strong process benefits, including higher yields, lower energy use, and faster cycle times. Case studies demonstrate single-digit to low-double-digit improvements in production efficiency, helping manufacturers reduce costs and achieve sustainability targets. Enzymes also cut waste in bakery and dairy production, directly lowering the cost of goods. As global manufacturers prioritize sustainability reporting and operational efficiency, enzyme adoption has become a procurement-driven necessity with significant long-term impact.

Advancements in precision fermentation and enzyme engineering have expanded the functionality, stability, and cost-efficiency of food enzymes. Engineered enzymes with improved thermostability and shelf-life are enabling applications in emerging segments such as plant-based protein modification and novel texturants. Continuous R&D investments and new fermentation capacity are accelerating the availability of cost-effective, specialty enzymes. This strengthens the innovation pipeline and supports steady revenue growth across both mature and emerging applications.

Barrier Analysis - Regulatory Complexity, Approval Timelines, and Production Scale-Up Economics

Food enzymes face region-specific approval processes. In Europe, EFSA assessments can take several years, requiring extensive safety dossiers. In the U.S., FDA notifications add regulatory layers before commercialization. These lengthy and expensive approval cycles slow product launches, limit the agility of smaller firms, and increase compliance costs for new entrants.

Large-scale enzyme production requires significant investment in fermentation capacity, downstream processing, and cold-chain logistics. Small- and mid-sized firms often lack access to pilot-scale facilities, creating supply constraints. Production economics are highly sensitive to yield and titre performance, which can increase unit costs during demand surges. This creates a barrier to entry and reinforces market concentration.

Opportunity Analysis - Packaged Food and Clean-Label Specialty Enzyme Opportunities in the Asia Pacific

Asia Pacific is experiencing the fastest growth in packaged food consumption, supported by rising disposable incomes and rapid industrialization. The local adaptation of enzyme formulations for rice- and soy-based applications presents a significant opportunity. Capturing even a small share of additive replacement in these high-volume categories could generate several hundred million USD in incremental enzyme sales.

Non-GMO and plant-derived enzyme portfolios offer premium pricing opportunities. These products support clean-label claims, which are expanding rapidly in developed markets. Targeting just 1–2% of reformulation projects in North America and Europe could translate into significant revenue opportunities for companies with validated, regulatory-ready enzyme solutions.

An emerging model bundles enzymes with process optimization, engineering support, and service-level agreements. This shift enables sales from commodity transactions to value-based partnerships, resulting in increased revenue per customer and reduced churn. Companies adopting this model differentiate themselves and build long-term customer relationships, capturing higher margins in the process.

Category-wise Analysis

Source Insights

Microbial enzymes remain the dominant source in the global food enzymes market, accounting for the largest share of approximately 64% in 2025. Their prominence stems from cost-effectiveness, scalability, and consistent production yields through controlled fermentation processes. Microbial enzymes are widely accepted under regulatory frameworks such as the U.S. FDA’s GRAS and the EU’s EFSA approvals, which enhances their adoption across food applications. Their ability to be engineered for temperature stability, pH tolerance, and specific substrate targeting ensures their versatility in the bakery, dairy, and beverage industries.

Plant-derived and precision-fermentation enzymes are recording the fastest growth, expanding at a CAGR above the overall market average. Rising demand for animal-free, vegan, and sustainable ingredients in North America and Europe is a critical driver. Clean-label trends, coupled with regulatory encouragement for sustainable sourcing, are pushing food manufacturers to shift toward plant-based and recombinant alternatives. Precision fermentation, in particular, enables the production of enzymes identical to those derived from animals with a lower environmental footprint. This growth is amplified by the surge in plant-based dairy and meat substitutes, where such enzymes play a crucial role in texture and flavor optimization.

Enzyme Type Insights

Carbohydrases hold the largest share of 40% market in 2025, supported by extensive utilization in bakery, beverages, and sweeteners. Amylases and glucoamylases are widely used to improve dough performance, extend bread shelf life, and enhance syrup conversion efficiency. In the beverage sector, carbohydrases improve fermentation consistency and sugar breakdown, while in sweeteners, they are central to high-fructose corn syrup production. The steady demand for processed and convenience foods worldwide ensures carbohydrases maintain their leadership, accounting for over 40% of the market share in 2025. Their broad applications and proven reliability make them the cornerstone of enzyme usage.

The proteases segment represents the fastest-growing enzyme category between 2025 and 2032, with a CAGR exceeding 7%. Proteases facilitate protein hydrolysis, a process essential for plant-based meat alternatives, dairy modification, and sports nutrition products. With consumers seeking high-protein diets, lactose-free dairy, and reduced-fat formulations, proteases are experiencing accelerated demand. Advances in enzyme engineering are enhancing stability and diversifying applications, thereby expanding their commercial use in global markets and enabling entry into premium and functional food categories.

Application Insights

Bakery applications dominate the food enzymes market in 2025, with a market share of 36% supported by the high global consumption of bread, cakes, and pastries. Enzymes such as amylases and xylanases improve dough handling, texture, and volume, while lipases contribute to better crumb structure and extended shelf life. With bread remaining a staple in Western diets and growing demand for packaged bakery products in emerging markets, the bakery maintains the largest share of global enzyme consumption. Multinational bakery chains and industrial-scale production further reinforce reliance on enzymes, ensuring that this application retains its dominant market position throughout the forecast period.

Dairy applications are expanding rapidly, projected to record the highest CAGR from 2025 to 2032. Growth is driven by demand for lactose-free milk, functional yogurts, and plant-based dairy alternatives. Lactase enzymes are central to removing lactose, meeting consumer needs in regions where lactose intolerance is widespread, particularly in Asia Pacific. Proteases improve cheese yield and flavor, while lipases support low-fat dairy reformulations. The rapid expansion of the plant-based dairy industry, especially in Europe and North America, further accelerates demand.

Regional Insights

North America Food Enzymes Market Trends - Strong Bakery-Dairy Industries and GRAS-Backed Innovation

North America represents the largest regional market, accounting for a 34.6% share of global revenues in 2025. The U.S. leads due to its robust bakery and dairy industries, which generate billions in annual sales and drive consistent enzyme demand. Regulatory approvals under the Generally Recognized as Safe (GRAS) framework provide clarity and predictability for manufacturers, encouraging innovation and commercialization. Growth in the region is supported by clean-label trends, with over 60% of U.S. consumers preferring minimally processed foods, according to USDA reports.

The rise of lactose-free dairy, projected to exceed US$10 Bn by 2030, further supports enzyme adoption. The region also benefits from advanced fermentation capacity, strong R&D infrastructure, and the presence of global leaders such as DuPont and Novozymes. Investment trends include fermentation plant expansions in the Midwest and mergers targeting specialty enzyme portfolios. With its mature market and emphasis on sustainability, North America remains a hub for technological innovation and commercial scaling in the food enzyme sector.

Asia Pacific Food Enzymes Market Trends - Rapid urbanization and rising demand for processed food enzymes

Asia Pacific is the fastest-growing regional market, forecast to record a CAGR of 8.2% through 2032. Rapid urbanization and rising disposable incomes are reshaping dietary habits, driving demand for packaged and processed foods. China, the largest contributor, is investing heavily in industrial modernization and advanced fermentation technologies, while India presents high potential for cost-effective enzyme applications in bakery and dairy. Japan’s market is more specialized, with strong demand for premium and functional enzymes in high-value food segments.

ASEAN countries are becoming attractive manufacturing hubs due to their cost advantages and supportive government incentives for food processing industries. The regulatory landscape is fragmented, requiring country-specific approvals that can slow market entry. Despite this, opportunities are abundant in tailored enzyme formulations for regional staples such as noodles, rice-based products, and soy-based dairy substitutes. Strategic investments include joint ventures with local producers and expansions of fermentation capacity. Asia Pacific’s combination of consumer-driven demand and production advantages positions it as the most dynamic growth frontier in the food enzymes market.

Europe Food Enzymes Market Trends - Strict regulatory oversight and advanced enzyme production hubs

Europe holds a high-value share in the global market, underpinned by strict regulatory oversight and advanced food-tech clusters. The European Food Safety Authority (EFSA) plays a central role, ensuring consumer trust through rigorous approval processes. Germany and the U.K. serve as production hubs, hosting both multinational corporations and SMEs focused on niche enzyme solutions. France and Spain, with strong bakery and dairy industries, drive regional consumption. Sustainability initiatives such as the European Green Deal are fueling demand for precision fermentation and clean-label enzymes, aligning with consumer preferences for natural and transparent food products.

European consumers are also highly receptive to plant-based and lactose-free innovations, reinforcing enzyme adoption. Competitive dynamics reveal ongoing consolidation among market leaders, with recent acquisitions aimed at strengthening capabilities in microbial fermentation. At the same time, smaller companies are targeting functional and specialty enzyme segments. Investment momentum is strong in R&D collaborations, precision fermentation facilities, and cross-border partnerships, positioning Europe as a key innovator in the global food enzymes market.

Competitive Landscape

The global food enzymes market is moderately concentrated. Global leaders such as Novonesis (Novozymes + Chr. Hansen), DSM-Firmenich, DuPont/IFF, Kerry, AB Enzymes, and BASF control premium segments, while regional players in India, China, and Southeast Asia supply lower-cost alternatives. The market structure is evolving through mergers, acquisitions, and service-oriented business models.

These deals highlight strategic consolidation, portfolio diversification, and entry into fast-growing dairy enzyme applications. Market leaders emphasize innovation through biotechnology, cost leadership via manufacturing scale, and expansion into Asia Pacific. Emerging trends include integrated service models and customized formulations for plant-based and clean-label applications.

Key Industry Developments

- In July 2024, Novozymes A/S launched its next-generation baking enzyme portfolio to improve dough stability and shelf life, targeting large-scale bakery manufacturers in Europe and North America.

- In May 2024, DSM-Firmenich introduced a new lactase enzyme solution designed for lactose-free and reduced-sugar dairy products, enhancing its position in the dairy enzyme segment.

Companies Covered in Food Enzymes Market

- Novozymes A/S

- DuPont Nutrition & Biosciences (IFF)

- DSM-Firmenich

- AB Enzymes GmbH

- Chr. Hansen Holding A/S

- BASF SE

- Kerry Group plc

- Amano Enzyme Inc.

- Dyadic International Inc.

- Biocatalysts Ltd.

- Advanced Enzyme Technologies Ltd.

- Specialty Enzymes & Probiotics

- Enzyme Development Corporation

- Aumgene Biosciences

- Nagase & Co., Ltd.

- Roquette Frères

- Jiangsu Boli Bioproducts Co., Ltd.

- Puratos Group

- Clerici-Sacco Group

- Creative Enzymes

Frequently Asked Questions

The food enzymes market size was valued at US$3.62 Bn in 2025.

By 2032, the global food enzymes market is projected to reach US$5.71 Bn.

Key trends include the rise of plant-derived and precision-fermentation enzymes, strong demand for lactose-free and plant-based dairy, growing emphasis on sustainability and clean-label formulations, and expansion of fermentation capacity across North America, Europe, and Asia Pacific.

By enzyme type, carbohydrases lead the market with over 40% share in 2025, driven by bakery, beverages, and sweeteners. By application, the bakery segment holds more than 36% share, supported by high global bread and confectionery production.

The food enzymes market is projected to grow at a CAGR of 6.7% between 2025 and 2032.