- Advanced Materials

- Flat Glass Market

Flat Glass Market Size, Share, Trends, and Growth Forecast 2025 - 2032

Flat Glass Market by Technology (Float, Rolled, Sheet), Product Type (Float Glass, Coated, Extra Clear, Toughened, Laminated), Industry (Construction, Automotive, Solar Panels, Other), and Regional Analysis for 2025 - 2032

Flat Glass Market Size and Trends Analysis

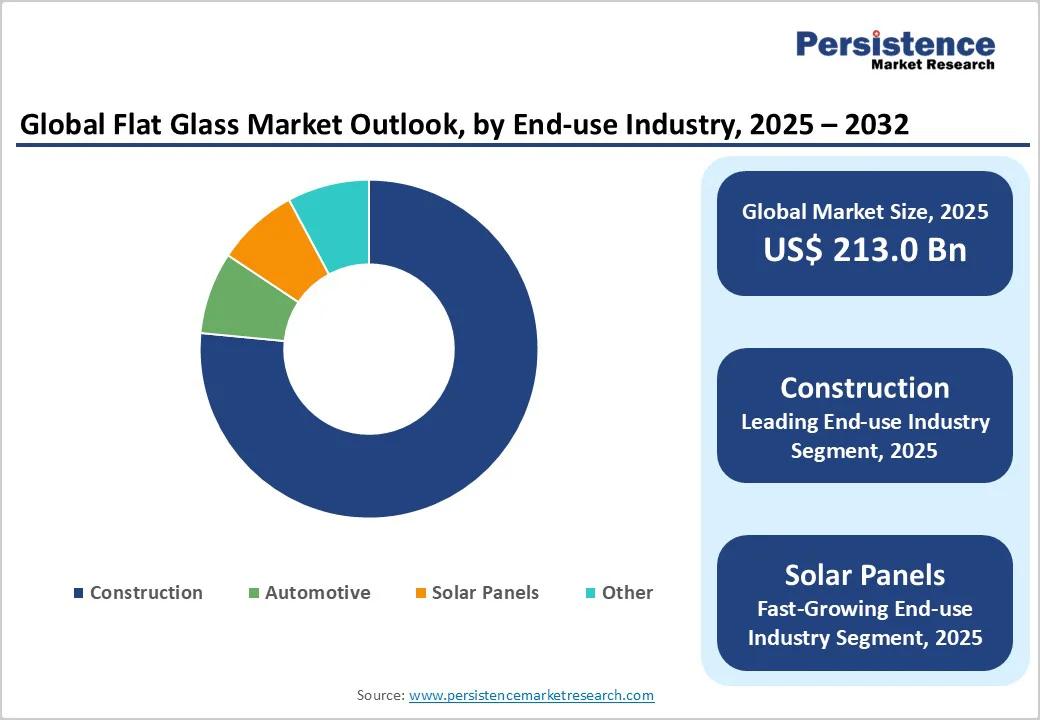

The global flat glass market size was valued at US$ 213.0 Bn in 2025 and is projected to reach US$ 326.7 Bn by 2032, growing at a CAGR of 6.3% between 2025 and 2032.

Infrastructure development boosts demand for energy-efficient building materials such as low-emissivity glass in construction projects worldwide.

In addition, the construction sector's expansion, fueled by government investments in sustainable housing, has led to a surge in flat glass applications for facades and windows, while the automotive industry's shift toward electric vehicles propels lightweight, durable glazing solutions.

Key Market Highlights:

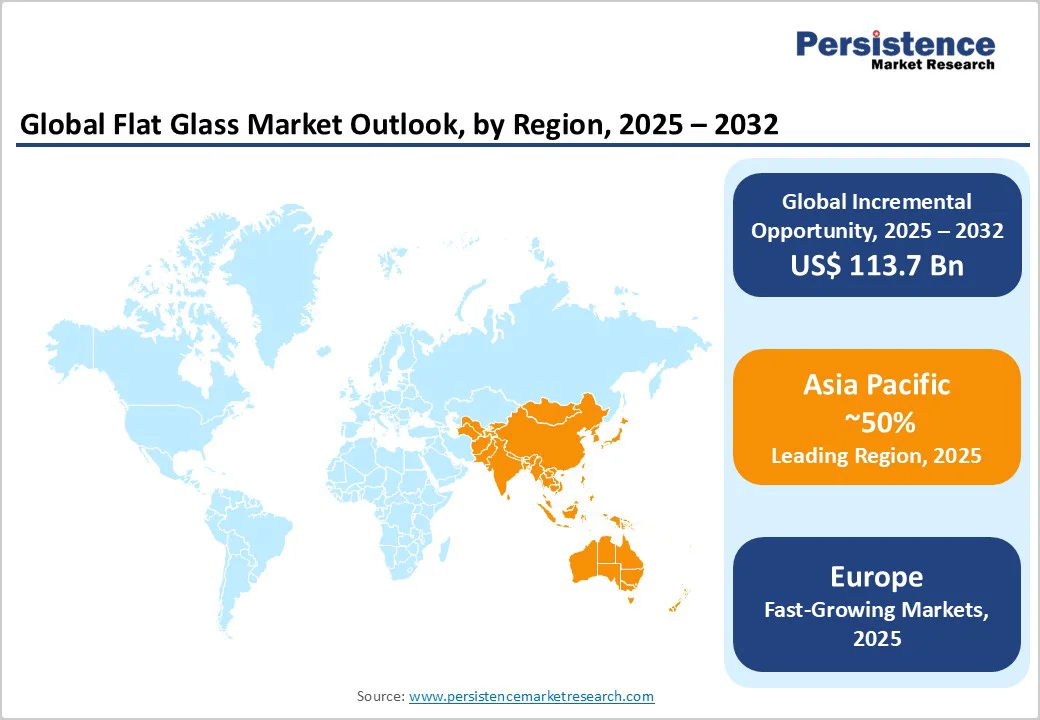

- Regional Leader: Asia Pacific leads the flat glass market with 50% market share, due to rapid urbanization in China and India, driving construction demand for energy-efficient glazing solutions.

- Fastest Growing Region: Europe is the fastest-growing region, fueled by manufacturing hubs and solar investments.

- Leading Segment: Construction dominates as the key segment, accounting for 80% share with applications in sustainable buildings worldwide.

- Fastest Growing Segment: Solar Panels emerge as the fastest-growing end-use, boosted by renewable targets adding 500 GW capacity annually.

- Growth Opportunities: Key opportunities lie in smart glass adoption, enabling 20% energy savings in buildings per EU Green Deal initiatives.

| Key Insights | Details |

|---|---|

| Flat Glass Market Size (2025E) | US$ 213.0 Bn |

| Market Value Forecast (2032F) | US$ 326.7 Bn |

| Projected Growth CAGR (2025-2032) | 6.3% |

| Historical Market Growth (2019-2024) | 5.7% |

Market Dynamics

Driver - Urbanization and Infrastructure Expansion

Rapid urbanization in emerging economies is a major driver for the flat glass market, as cities expand and require modern building materials for residential and commercial structures. According to the United Nations, the global urban population reached 56% in 2024, projected to rise to 68% by 2050, spurring infrastructure projects that utilize flat glass for energy-efficient windows and facades.

This demand is evident in the Asia Pacific, where construction spending has increased by 7% annually, driven by government initiatives like China's Belt and Road Initiative, which emphasizes sustainable urban development. The integration of flat glass enhances building aesthetics and thermal performance, reducing energy consumption by up to 30% in new constructions, thereby supporting market growth through compliance with green building standards.

Automotive Sector Advancements

The automotive industry's evolution, particularly the rise of electric vehicles (EVs), is propelling flat glass demand for windshields, sunroofs, and side windows that prioritize safety and weight reduction. Global EV sales surged to 14 million units in 2024, a 35% increase from the previous year, as reported by the International Energy Agency, necessitating advanced laminated and toughened glass to meet crash safety regulations like those from the European New Car Assessment Programme.

In Europe, automakers are incorporating acoustic glass to reduce noise by 10 decibels, improving passenger comfort in premium models. This trend not only boosts volume but also encourages innovation in lightweight glazing, which can cut vehicle weight by 5-10%, enhancing fuel efficiency and aligning with emissions targets under the Paris Agreement. Subsequently, the Automotive Glass Market interconnection drives a sustained positive impact on flat glass consumption.

Restraint - High Production Energy Costs

Energy-intensive manufacturing processes pose a significant restraint for the flat glass market, as production relies heavily on natural gas and electricity, leading to volatility in cost. Flat glass melting requires temperatures exceeding 1,500°C, consuming about 4-6 GJ per ton, and with global energy prices rising 15% in 2024 due to geopolitical tensions, as noted by the International Energy Agency, manufacturers face margin pressures.

In Europe, the EU Emissions Trading System adds compliance costs estimated at €50 per ton of CO2, exacerbating expenses for carbon-heavy operations. This restraint hampers profitability, particularly for smaller producers, and could slow investment in capacity expansion amid fluctuating raw material prices like silica sand.

Supply Chain and Raw Material Volatility

Volatility in raw material supply disrupts flat glass production, negatively impacting market stability due to reliance on soda ash and limestone. Disruptions from events like the 2024 Red Sea shipping issues increased logistics costs by 20%, according to the World Shipping Council, delaying deliveries and raising prices.

Furthermore, environmental regulations on mining in regions like the US have reduced supply by 10%, forcing imports and adding tariffs. These factors create uncertainty, potentially stalling projects in the construction and automotive sectors, where timely material availability is critical, thus constraining overall market growth.

Opportunity - Expansion in Solar Energy Applications

The solar energy sector presents a key opportunity for flat glass manufacturers, as demand for anti-reflective and tempered glass in photovoltaic panels surges with global renewable targets. The International Renewable Energy Agency reports that solar capacity additions reached 510 GW in 2024, a 25% year-over-year increase, requiring specialized flat glass to cover 90% of panel surfaces for efficiency gains of up to 5%.

In the Solar Energy Market, innovations such as thinner substrates reduce material use by 15% while enhancing light transmission, supported by policies such as the US Inflation Reduction Act, which allocated $370 billion for clean energy. Companies can capitalize by partnering with panel producers, as seen in Europe's European Solar Rooftop Initiative, adding 2 GW in 2024, promising significant revenue from high-volume, low-carbon glass production in the coming decade.

Adoption of Smart and Sustainable Glass Technologies

Advancements in smart glass technologies offer substantial opportunities, enabling flat glass firms to tap into energy-efficient building retrofits and IoT-integrated applications. The European Commission estimates that smart glazing could cut building energy use by 20-30%, aligning with the European Green Deal's net-zero goals by 2050, where over 40% of energy consumption stems from structures.

Developments like electrochromic glass, which adjusts tint via voltage, have seen adoption rise 40% in commercial buildings since 2023, per industry associations.

With governments subsidizing green retrofits such as the UK's Green Homes Grant funding £1.5 billion, manufacturers can target the fastest-growing segment of coated glass, integrating with the Portable Solar Panels Market for hybrid solutions. This positions companies for future potential through R&D in recyclable, low-emission variants, driving demand in construction and beyond.

Category-wise Insights

Technology Analysis

The Float technology segment leads the flat glass market with approximately 90% market share, owing to its superior surface quality and scalability for large-scale production. Developed by Pilkington Brothers in the 1950s, the float process involves pouring molten glass over molten tin, yielding distortion-free sheets ideal for high-precision applications like automotive windshields and architectural facades.

According to the Glass for Europe association, float glass accounts for most of the output due to its efficiency, producing over 80 million tons annually worldwide, compared to rolled or sheet methods, which are limited to textured or patterned uses.

This dominance is justified by its versatility in meeting stringent standards from bodies such as the American Society for Testing and Materials, ensuring uniform thickness and optical clarity that rolled glass, at 5-10% share, cannot match for modern demands.

Product Type Analysis

Float Glass holds the leading position in the product type category with around 70% market share, driven by its foundational role as the base material for further processing into specialized variants. Its production via the float method ensures smooth, parallel surfaces suitable for diverse uses, from basic windows to advanced coatings, as highlighted by the International Glass Association.

In 2024, float glass production exceeded 100 million tons globally, supported by its cost-effectiveness, 20% lower than laminated alternatives, and compliance with safety norms like ISO 12543 for building applications. This segment's lead is further validated by its adaptability in the Automotive Glass Market, where it forms the core of 95% of vehicle glazing, outperforming coated or toughened types in volume due to economies of scale in manufacturing hubs like Asia.

Industry Analysis

The Construction segment dominates the Industry with about 80% market share, fueled by its essential role in windows, facades, and interior partitions for energy-efficient buildings. As per Glass for Europe, construction consumes the bulk of flat glass output, with demand rising 5% annually due to urbanization and regulations such as the EU's Energy Performance of Buildings Directive, mandating low-emissivity glazing.

In 2024, global building projects incorporated over 60 billion square meters of flat glass, justified by its thermal insulation properties that reduce heating costs by 25%, surpassing automotive (15%) and solar (5%) uses. This leadership is reinforced by trends in green architecture, where flat glass enables daylight optimization while meeting certifications from the U.S. Green Building Council.

Regional Insights

North America Flat Glass Trends

North America, led by the U.S., exhibits strong flat glass market trends centered on regulatory frameworks promoting sustainability and an innovation ecosystem fostering advanced materials. The U.S. Department of Energy invested $200 million in 2024 for energy-efficient construction, driving the adoption of insulated glass units that cut energy use by 30% in buildings.

Innovations like self-cleaning coatings from companies such as AGC Inc. align with the region's focus on smart buildings, where retrofitting older structures, comprising 40% of the stock, boosts demand.

The automotive sector further supports growth, with 25 GW of new solar capacity installed in 2024, enhancing photovoltaic glass needs, per the Solar Energy Industries Association. This ecosystem, bolstered by R&D hubs in California, positions North America as a leader in high-value applications.

Europe Flat Glass Trends

Europe's flat glass trends emphasize performance in key countries such as Germany, the U.K., France, and Spain, underpinned by regulatory harmonization under the European Green Deal.

In 2024, the directive on building energy performance mandated Low-E glass in new constructions, reducing emissions by 20% and spurring a 10% rise in coated glass use, as reported by the European Commission. Germany's automotive integration, with Mercedes-Benz adopting laminated glass for EVs, highlights harmonized safety standards like UN ECE R43.

France and Spain focus on solar applications, with the European Solar Rooftop program adding 2 GW capacity in 2024, driving tempered glass demand. This regulatory push ensures consistent growth across the region, balancing innovation with environmental compliance.

Asia Pacific Flat Glass Trends

Asia Pacific's flat glass trends are propelled by growth dynamics in China, Japan, India, and ASEAN, leveraging manufacturing advantages and rapid urbanization.

China's dominance, producing 50% of global flat glass via efficient float lines, supports infrastructure like the High-Speed Rail Network, where glass facades cover millions of square meters, per the China Glass Association. In 2024, investments in EV manufacturing boosted automotive glass by 15%, with BYD incorporating advanced laminates.

India and ASEAN exhibit explosive growth, with India's construction boom under Pradhan Mantri Awas Yojana adding 20 million homes by 2025, favoring affordable float glass. Japan's precision tech, like NSG's solar innovations, enhances Solar Energy Market ties, with ASEAN's 5% annual capacity growth underscoring cost-competitive production.

Competitive Landscape

The global flat glass market is moderately consolidated, with top players like Saint-Gobain, AGC Inc., and NSG Group controlling around 60% of global production through strategic expansions and R&D investments. Companies pursue mergers, such as joint ventures for sustainable tech, and focus on vertical integration to secure raw materials amid volatility.

Key differentiators include eco-friendly processes, like low-carbon melting, enabling premium pricing in green segments. Emerging models emphasize circular economy practices, recycling 30% of glass waste, while digital twins optimize manufacturing for 10% efficiency gains. This structure favors leaders with global footprints, fostering innovation in smart glass for competitive edges.

Key Market Developments:

- January 2024: AGC Inc. and Saint-Gobain partnered on a pilot flat glass line in the Czech Republic, aiming for 50% electrification to cut CO2 emissions by 50%, advancing decarbonization.

- September 2024: Saint-Gobain introduced ORAÉ®, the world's first low-carbon flat glass, produced with 70% less emissions, targeting the construction and automotive sectors.

- March 2025: NSG Group invested $100 million in a new float glass plant in India, boosting capacity by 20% for solar and building applications.

Top Companies in the Flat Glass Market

- Saint-Gobain (France) is a global leader with a diverse portfolio in sustainable flat glass, emphasizing R&D in energy-efficient coatings that serve construction and automotive markets.

- AGC Inc. (Japan), headquartered in Tokyo, excels in advanced technologies like antimicrobial glass, holding 15% market share via innovations for EVs and solar panels. With operations in 30 countries, it drives growth through partnerships, reducing emissions.

- NSG Group (Japan) dominates automotive glazing, leveraging the Pilkington trademark for laminated products. Its maturity in float processes supports 10% annual expansion in Asia.

Companies Covered in Flat Glass Market

- AGC Inc.

- Saint-Gobain

- NSG Group

- Guardian Industries

- Sisecam

- Taiwan Glass Ind. Corp.

- Central Glass Ltd.

- Euroglass

- Xinyi Glass Holding Ltd.

- Fuyao Group

- Vitro

- SCHOTT AG

- Pittsburgh Glass Works

Frequently Asked Questions

The global Flat Glass Market is valued at US$ 213.0 Bn in 2025 and expected to reach US$ 326.7 Bn by 2032, growing at a CAGR of 6.3%.

Key drivers include urbanization, boosting construction needs, and automotive EV growth requiring advanced glazing, alongside solar energy expansions.

Construction leads with 80% share, driven by energy-efficient building demands and global infrastructure projects.

Asia Pacific dominates, holding over 50% share due to manufacturing strengths in China and rapid urbanization in India.

Solar energy applications offer significant potential, with glass demand rising from 510 GW capacity additions in 2024.