- Semiconductor Materials & Components

- Quad Flat No-Lead (QFN) Packaging Market

Quad Flat No-Lead (QFN) Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Quad Flat No-Lead (QFN) Packaging Market by Package Type (Plastic QFN (PQFN), AC QFN, Misc.), Manufacturing Method (Punched QFN, Sawn QFN), End-use (Consumer Electronics, Automotive, Telecommunications & Networking, IoT & Wearables, Medical Devices, Other Industrial), and Regional Analysis for 2025 - 2032

Quad Flat No-Lead (QFN) Packaging Market Share and Trends Analysis

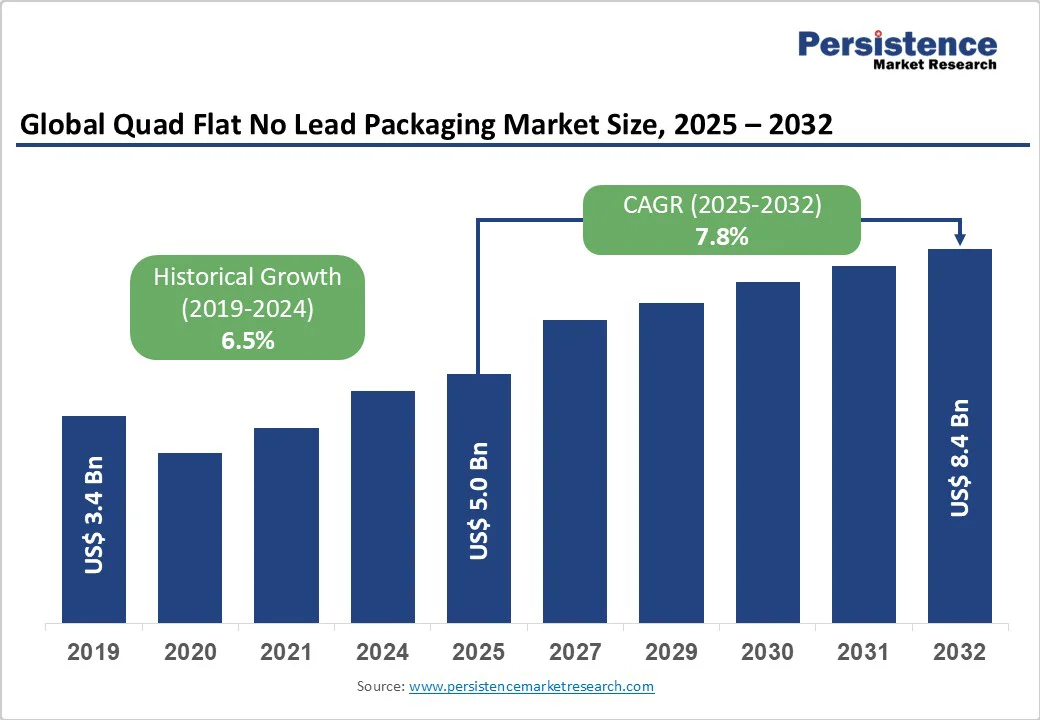

The global quad flat no-lead (QFN) packaging market size is likely to be valued at US$ 5.0 billion in 2025, and is projected to reach US$ 8.4 billion by 2032, growing at a CAGR of 7.8% during the forecast period 2025 - 2032.

This robust growth trajectory reflects the sector's critical role in supporting the miniaturization of electronics around the world, with QFN packages becoming increasingly essential for space-constrained applications where thermal management and electrical performance are paramount.

The market demonstrates strong momentum driven by the proliferation of consumer electronics, automotive electrification, and the rapid deployment of 5G infrastructure, which collectively demand compact, high-performance packaging solutions.

Key Industry Highlights:

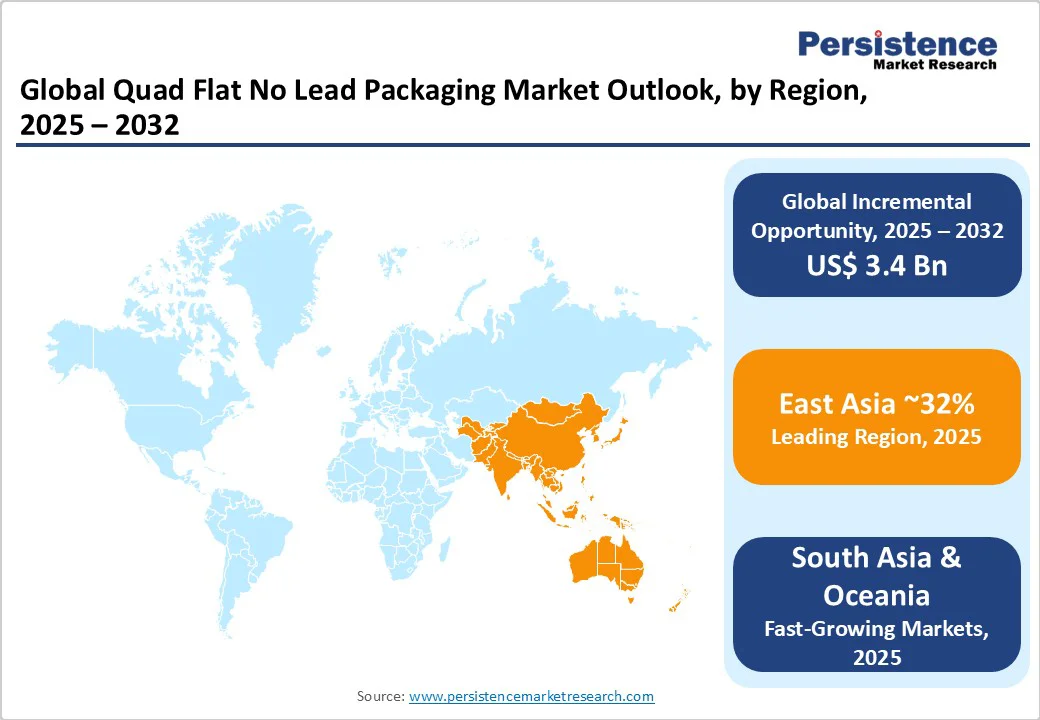

- Dominant Region: Asia Pacific dominates the QFN packaging market with over 45% share in 2025, driven by China’s large-scale electronics manufacturing ecosystem and Japan’s robust automotive electronics production.

- Regional Dynamics: North America holds around 25% of the market share, with strong demand from 5G infrastructure, automotive electronics, and industrial applications, while Europe accounts for approximately 20% market share, led by Germany’s automotive dominance.

- Leading Country: China remains the largest producer and consumer of quad flat no-lead packaging, supported by strong domestic semiconductor policies and integrated supply chains.

- Investment Focus: Massive investments such as Texas Instruments’ US$ 60 billion semiconductor expansion and Amkor Technology’s US$ 7 billion Arizona facility reinforce QFN demand in advanced semiconductor packaging.

| Key Insights | Details |

|---|---|

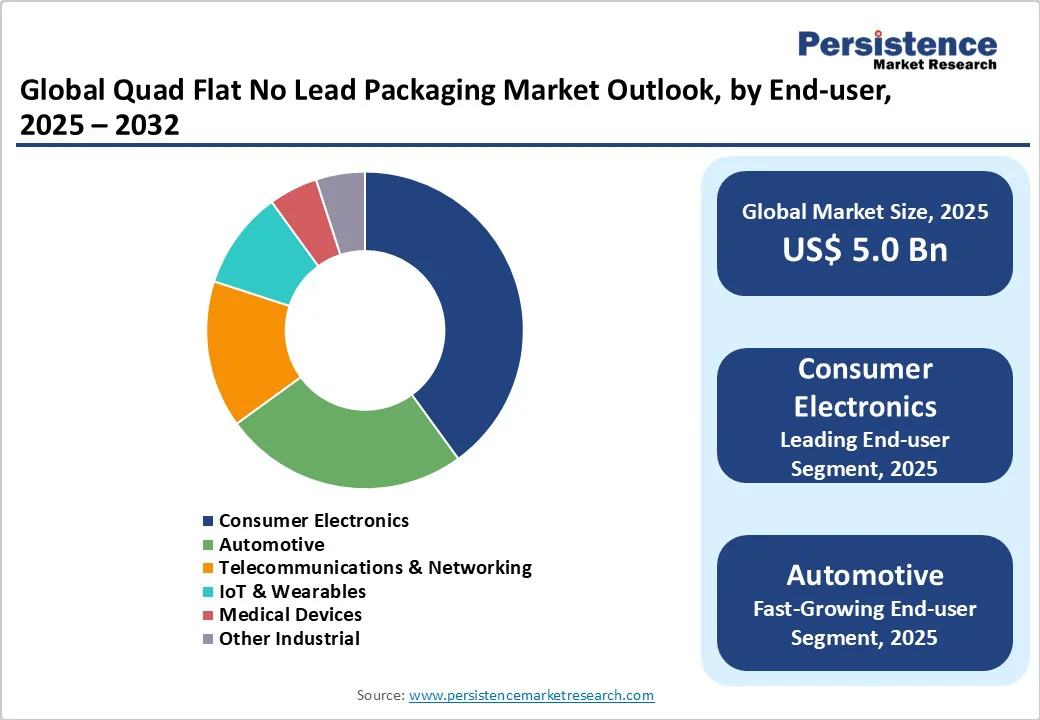

| Quad Flat No-Lead (QFN) Packaging Market Size (2025E) | US$ 5.0 Bn |

| Market Value Forecast (2032F) | US$ 8.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Accelerating Electronics Miniaturization and Device Integration

The relentless pursuit of smaller, more powerful electronic devices represents the primary catalyst propelling QFN market expansion. Modern consumer electronics, particularly smartphones and wearables, require packaging solutions that maximize functionality within increasingly constrained spaces.

According to industry data, IoT devices are expected to surpass 30 billion units by 2025. This miniaturization imperative extends beyond consumer electronics into automotive, industrial automation, and medical devices, where compact form factors enable new product categories and enhanced integration of functionality.

The global 5G network rollout necessitates advanced packaging solutions capable of handling high-frequency operations with minimal signal degradation. QFN packages demonstrate superior RF performance characteristics, featuring reduced parasitic inductance and enhanced signal integrity compared to traditional leaded packages.

The exposed thermal pad design facilitates efficient heat dissipation, crucial for 5G base stations and wireless communication equipment. Industry projections indicate global 5G connections will exceed 1.5 billion by 2025, driving substantial demand for RF-capable QFN packages in telecommunications infrastructure.

Supply Chain Complexity and Leadframe Availability

The QFN packaging market faces significant supply chain constraints, particularly in leadframe procurement from specialized suppliers. Market consolidation has reduced the number of leadframe manufacturers, creating supply bottlenecks during demand surges.

The leadframe business operates on low margins, causing some suppliers to exist in the market and creating periodic shortages that impact QFN production capacity. These supply chain vulnerabilities can lead to extended lead times and increased costs, particularly affecting smaller packaging houses with limited supplier relationships.

The manufacturing process of quad flat no-lead packages requires precise control over multiple variables, including void formation, solder paste volume, and thermal via design to ensure reliable performance. The large coverage area and numerous thermal vias in QFN packages create challenges for achieving consistent solder joint quality, with void control being particularly critical for thermal performance. Manufacturing complexities increase with higher pin counts and advanced features, requiring specialized equipment and processes that represent significant capital investments for packaging houses.

Emerging Market Penetration and Geographic Expansion

Developing economies, particularly in Asia Pacific, present substantial growth opportunities as electronics manufacturing capacity expands globally. Government initiatives in India, such as the Production Linked Incentive (PLI) schemes that have allocated massive financial resources for electronics manufacturing, have created favorable investment environments for QFN adoption.

On the other hand, China's semiconductor packaging market expansion, supported by domestic policy initiatives, offers significant potential for QFN technology deployment. These emerging markets combine cost advantages with growing technical capabilities, creating attractive opportunities for QFN package manufacturers to establish local production and serve regional demand.

Furthermore, continuous advancement in leadframe materials, including enhanced copper alloys with improved thermal conductivity and reduced oxidation properties, creates opportunities for superior QFN package performance.

Innovations in surface treatments such as Palladium-Nickel coatings and Pre-Plated Frame technologies improve solderability and corrosion resistance, expanding QFN applications into high-reliability sectors. The development of thinner, multi-layer leadframes and embedded passive component integration enables more complex circuit designs within compact form factors, opening new application possibilities in advanced electronic systems.

Category-wise Analysis

Package Type Insights

Plastic QFN (PQFN) is expected to dominate the market with an estimated 60% share in 2025, primarily due to its cost-effectiveness and versatility across mass-market applications. PQFN packages excel in consumer electronics applications, with over 50% of smartphones globally utilizing plastic-molded QFNs in 2023.

The manufacturing efficiency and scalability of plastic molding processes make PQFN ideal for high-volume production scenarios, particularly in portable devices, IoT sensors, and smart home applications. Plastic encapsulation provides adequate environmental protection while maintaining competitive pricing for consumer-focused applications.

Air-cavity QFN (AC QFN) is set to be the fastest-growing segment in 2025, driven by its superior thermal management capabilities and enhanced electrical performance for specialized applications. AC QFN packages feature reduced parasitic capacitance and inductance compared to plastic variants, making them particularly suitable for high-frequency RF applications and wireless communication systems.

The air gap design facilitates improved heat dissipation, essential for high-power applications in automotive electronics and 5G infrastructure equipment.

End-use Insights

Consumer electronics is poised to lead demand with around 40% of the quad flat no-lead packaging market revenue share in 2025, reflecting the sector's massive scale and continuous innovation cycles. The segment encompasses smartphones, tablets, wearables, and smart home devices that collectively drive high-volume QFN consumption.

Consumer electronics applications particularly value QFN's compact footprint and thermal efficiency, enabling thinner device profiles and longer battery life. The rapid adoption of advanced features in consumer devices, including AI processing capabilities and 5G connectivity, sustains strong demand for high-performance QFN packages.

Automotive emerges as the fastest-growing segment in 2025, driven by vehicle electrification and advanced driver assistance systems (ADAS) integration. Electric vehicle (EV) adoption and autonomous driving technologies require numerous electronic control units utilizing QFN packages for space efficiency and reliability.

Automotive applications demand QFN packages capable of withstanding extreme temperature variations and vibration conditions while maintaining consistent performance. Interestingly, the transition of the automotive industry toward smart, connected vehicles creates substantial growth opportunities for QFN suppliers.

Regional Insights

Asia Pacific Quad Flat No-Lead (QFN) Packaging Market Trends

Asia Pacific is predicted to dominate the quad flat no-lead packaging market share in 2025 in terms of production and consumption, with China representing the largest manufacturing base for consumer electronics and automotive components. Japan's automotive industry, generating 63 trillion yen in shipments while supporting over 5.58 million jobs, creates substantial demand for QFN packages in automotive electronics.

The regional market also benefits from integrated supply chains combining semiconductor fabrication, packaging, and assembly capabilities, enabling cost-effective QFN production for global markets. China's semiconductor policy initiatives and domestic market expansion support continued QFN market growth in the region.

North America Quad Flat No-Lead (QFN) Packaging Market Trends

North America is anticipated to maintain a strong position in advanced QFN applications, particularly in automotive electronics and 5G infrastructure deployment. The regional market makes substantial gains from major semiconductor companies such as Texas Instruments, which are investing billions in semiconductor fabs, creating an enormous demand for advanced packaging solutions.

Government initiatives, including the CHIPS and Science Act, provide robust support for domestic semiconductor manufacturing, with companies such as Amkor Technology expanding its facilities within the U.S. Moreover, the domestic automotive sector's rapid electrification, with U.S. new car sales incorporating increasing EV content, drives QFN adoption in power management and control systems.

Europe Quad Flat No-Lead (QFN) Packaging Market Trends

Europe focuses on automotive and industrial applications, with Germany's automotive industry representing over 30% of European passenger car production and maintaining strong export capabilities.

The region's emphasis on premium automotive segments, where German original equipment manufacturers (OEMs) control nearly 60% of global premium vehicle production, has generated a massive demand for high-reliability quad flat no-lead packages in advanced electronic systems.

European regulatory initiatives supporting 5G infrastructure development and automotive electrification offer growth catalysts for QFN adoption in telecommunications and automotive applications.

Competitive Landscape

The global quad flat no-lead packaging market exhibits a consolidated structure dominated by major semiconductor packaging service providers. Leading players include ASE Technology, Amkor Technology, JCET Group, Powertech Technology, and Tongfu Microelectronics, representing the top-tier companies with comprehensive QFN manufacturing capabilities.

Market concentration reflects the capital-intensive nature of advanced packaging operations and the technical expertise required for high-volume QFN production. Competitive positioning emphasizes technological capability, manufacturing scale, and customer relationship strength across diverse end-market applications.

Key Industry Developments:

- In August 2025, Amkor Technology signed a multi-year patent license agreement with GEM Services Inc., granting GEM access to Amkor’s MicroLeadFrame® (MLF®) QFN patents. This agreement strengthens the adoption of Amkor’s QFN packages, which offer excellent thermal and electrical performance, and supports the growing demand for power management products in portable and battery-powered systems.

- In August 2025, Japanese electronic component manufacturer Murata opened its first manufacturing facility in India at OneHub Chennai Industrial Park. The 3,500-square-meter plant will focus on packaging and shipping multilayer ceramic capacitors (MLCC), essential components used by global brands such as Apple, Samsung, and Sony. Murata’s entry aims to capitalize on India’s expanding electronics ecosystem and diversify its manufacturing base internationally.

- In June 2025, Nordson Electronics Solutions developed a high-precision panel-level packaging solution for Powertech Technology Inc. that achieves yields exceeding 99% for underfilling during semiconductor manufacturing. This advanced system enhances the accuracy and consistency of epoxy dispensing, crucial for maintaining package reliability in semiconductor assembly. The solution integrates seamlessly with Powertech’s versatile manufacturing processes, supporting various substrate sizes and package types while minimizing material waste and improving production efficiency.

Companies Covered in Quad Flat No-Lead (QFN) Packaging Market

- Amkor Technology

- Texas Instruments

- STATS ChipPAC Pte. Ltd.

- Microchip Technology Inc.

- ASE Group

- NXP Semiconductor

- Toshiba Corporation

- UTAC Group

Frequently Asked Questions

The global quad flat no-lead (QFN) packaging market is projected to reach US$ 5.0 billion in 2025.

The widespread miniaturization of electronics around the world and the intensifying need for advanced packaging solutions for space-constrained applications where thermal management and electrical performance are driving the market.

The market is poised to witness a CAGR of 7.8% from 2025 to 2032.

Key market opportunities include expanding electronics manufacturing in emerging economies supported by government incentives and advancements in QFN materials and thermal management technologies for high-reliability applications.

ASE Technology, Amkor Technology, JCET Group, Powertech Technology, and Tongfu Microelectronics are some major players.