- Automotive Components & Materials

- Automotive Airbag Inflator Market

Automotive Airbag Inflator Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Airbag Inflator Market by Product Type (Pyrotechnic Inflator, Stored Gas Inflator and Hybrid Inflator), Component Type (Airbag Inflator Filter, Airbag Tubes, and Others), Vehicle Type (Passenger Vehicle and Light Commercial Vehicle) and Regional Analysis for 2026 - 2033

Automotive Airbag Inflator Market Size and Trends Analysis

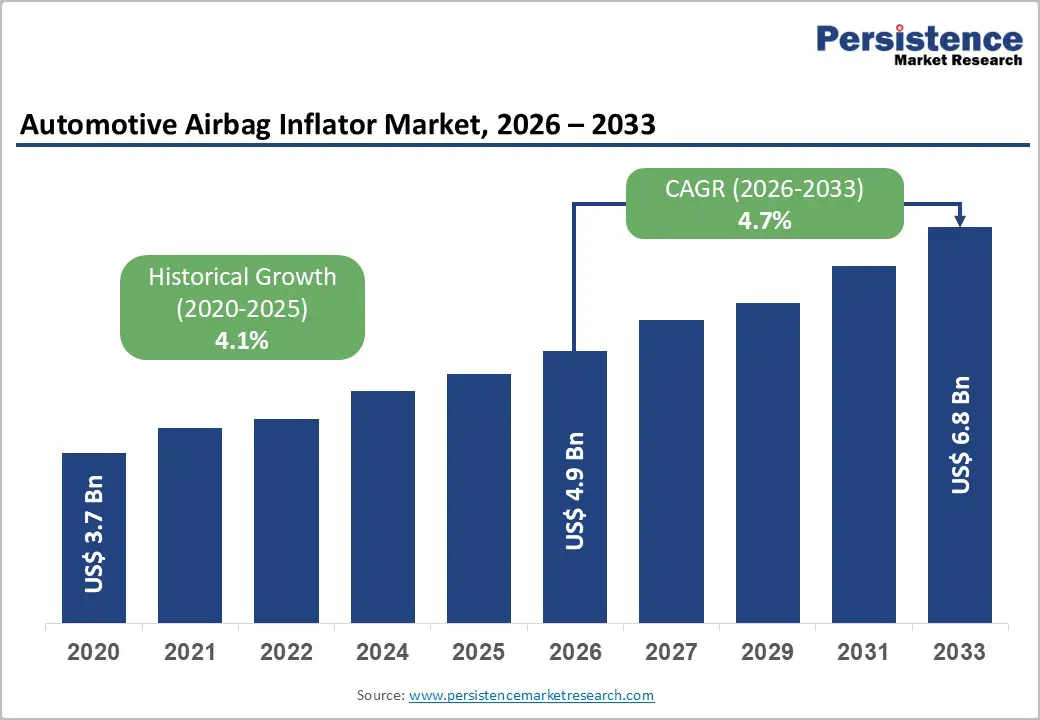

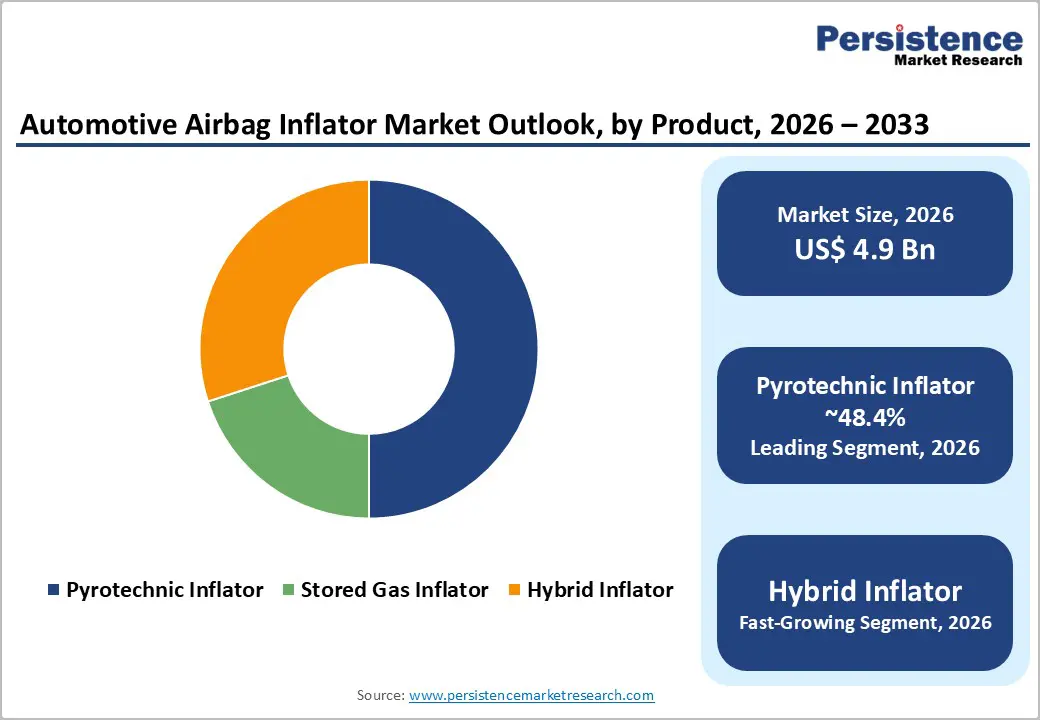

The global automotive airbag inflator market size is likely to be valued at US$ 4.9 billion in 2026 and is projected to reach US$ 6.8 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

This expansion reflects advances in vehicle safety standards, progressive electrification that has created more sophisticated occupant protection requirements, and regulatory mandates that establish comprehensive airbag deployment across vehicle segments. The market is driven by pyrotechnic inflator dominance through proven reliability and rapid deployment, and by hybrid inflator emergence as the fastest-growing technology, achieving enhanced safety performance and sensor integration.

Key Industry Highlights:

- Leading Product Type: Pyrotechnic inflators dominate with 48.4% market share, driven by proven deployment reliability; Hybrid inflators are the fastest-growing at a 6% CAGR, driven by multi-stage deployment capability and sensor integration.

- Dominant Component Type: Airbag inflator filters command 53.2% component market share through critical filtration functionality; Airbag tubes represent fthe astest growing at 5.6% CAGR, driven by advanced deployment system design innovation.

- Leading Vehicle Type: Passenger vehicles maintain 67.4% market share through comprehensive airbag system requirements; Light commercial vehicles represent the fastest growing at 4.9% CAGR, driven by emerging market safety regulation adoption and fleet modernization.

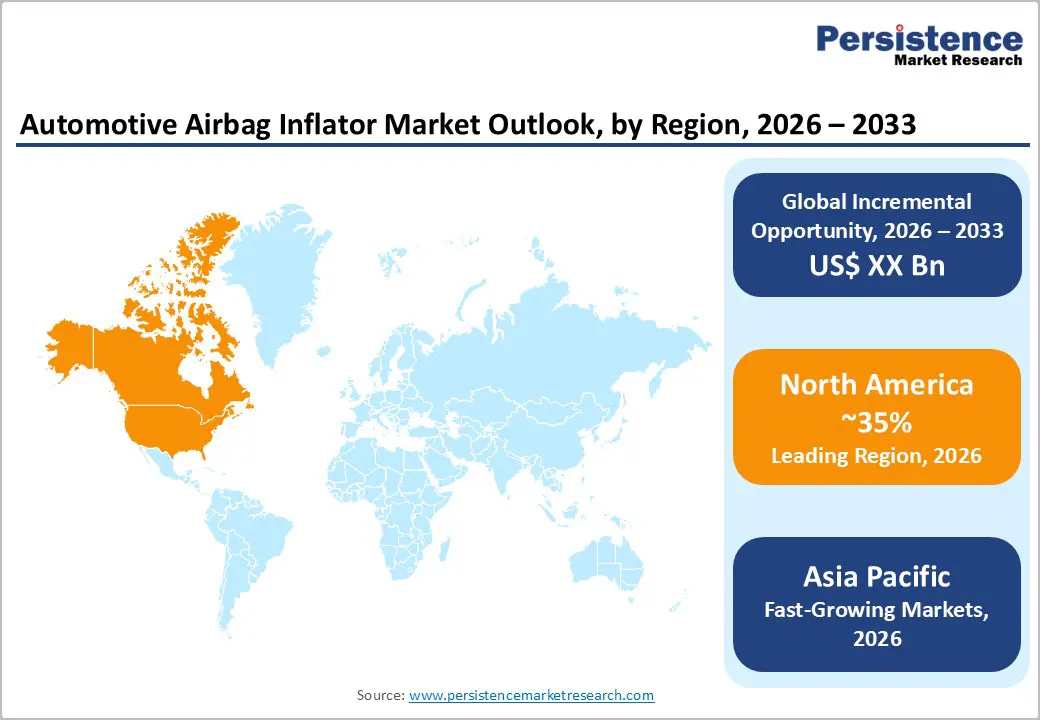

- Regional Market Dominance and Growth: North America maintains 35% global market share, driven by comprehensive safety regulations and a concentration of premium vehicles; Asia Pacific demonstrates the fastest regional growth at a 7% CAGR, expanding from its current 25% share to 35% by 2033.

- Technology and Market Innovation Momentum: Top 10 suppliers control 60% market share (Autoliv, ZF, Toyoda Gosei, Joyson leading); Hybrid inflator systems achieving multi-stage deployment and sensor integration; Electronic control advancement enabling predictive deployment; EV-specialized systems optimized for electric powertrain architecture.

| Key Insights | Details |

|---|---|

|

Automotive Airbag Inflator Market Size (2026E) |

US$ 4.9 Bn |

|

Market Value Forecast (2033F) |

US$ 6.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.7% |

|

Historical Market Growth (CAGR 2020 to 2024) |

4.1% |

Market Dynamics

Drivers - Strict Government Norms Supporting Public Safety to Bolster Demand

A key driver of the growing demand for automotive airbag inflators is the tightening of global safety regulations. Government agencies are stepping up enforcement of strict vehicle safety standards to reduce road accidents and injuries. Various countries now require that all new cars be equipped with airbags, a clear response to data showing that airbags significantly reduce the risk of severe injuries in accidents. For example,

- Government initiatives, such as the National Traffic and Motor Vehicle Safety Act, mandate that automobile manufacturers implement safety standards. These are intended to protect the public from unreasonable risks associated with vehicle design and operation.

- Federal Motor Vehicle Safety Standards (FMVSS) require the inclusion of safety features, such as seat belts and airbags, that have significantly reduced fatalities in traffic accidents.

Due to safety requirements, car manufacturers are being pushed to adopt advanced airbag systems, driving the market for airbag inflators.

Media Coverage of Vehicle Safety Tests to Augment Demand

As people become more aware of road safety, they are paying close attention to the safety features in their vehicles. Social media campaigns, consumer reviews, and increased media coverage of vehicle safety tests have helped educate buyers about the key role of airbags.

In emerging countries where prices are a key consideration when buying a car, consumers are willing to spend a bit more on vehicles that come with advanced safety features like effective airbag inflators. This rising demand is set to have a direct positive effect on the growth of the new energy vehicle airbag inflator market. Various companies in the industry are focusing on developing effective and safe airbags for enhanced safety. For example,

- ZF LIFETEC, a German-based company, introduced a Pre-crash Dual Stage Side Airbag (Dual Stage SAB) system to enhance safety in side impact collisions. The system works in two phases, providing essential distance before the impact. It predicts crashes and sets off the airbag at the ideal location, combining hybrid and pyrotechnic inflators.

Restraint - Rising Safety Concerns and Product Recalls May Hamper Demand

A key challenge facing the global automotive airbag inflator market is safety concerns and product recalls. High-profile cases involving defective airbag inflators have led to rising scrutiny from consumers, regulatory bodies, and the auto industry. These safety recalls can severely damage a manufacturer’s reputation and come with high costs for fixing and replacing faulty parts. For example,

- In 2024, the U.S. National Highway Traffic Safety Administration announced that BMW is recalling over 390,000 vehicles in the U.S. due to defective airbag inflators that could potentially explode.

- In September 2024, Mazda recalled 77,670 units of its MX-5 roadster and retractable fastback due to a software issue with the airbag sensor control module. Mazda North American Operations tested the airbag deployment force compliance with Federal Motor Vehicle Safety Standard 208 for occupant crash protection.

Limited Public Awareness about Airbag Technology to Hinder Growth

Addressing changing consumer preferences and educating consumers about airbag technology are key challenges in the automotive airbag inflator market. While awareness of vehicle safety is on the rise, consumers often have varying levels of understanding of airbag systems and their components, such as inflators. This lack of knowledge or misconceptions can affect consumer confidence and influence their buying choices.

Manufacturers need to effectively communicate the safety benefits, reliability, and advancements in airbag inflator technology to consumers. Government bodies in several countries are prioritizing public awareness and education for airbag inflators. For example,

- The U.S. National Highway Traffic Safety Administration (NHTSA) established programs to facilitate the removal of recalled airbags, particularly those associated with the Takata airbag crisis. This includes initiatives to expedite the recall process and ensure that consumers are informed about open recalls when registering their vehicles.

Opportunity - Emergence of Smart Airbag Systems to Open the Door to Success

Technological innovations in the automotive industry, especially in airbag systems, are significantly boosting the global automotive airbag inflator market. Introduction of smart airbag systems marks a key step forward, as these inflators are equipped with sensors and algorithms that adjust deployment based on various factors. These factors can include the severity of a collision, the position of occupants, and other dynamic aspects, allowing for more accurate and effective airbag deployment.

Smart airbag systems improve safety and help reduce the risk of injuries related to airbags by optimizing how they deploy. As technology advances, manufacturers are investing in research to make airbag inflators even smarter and more responsive. This push for innovation creates a vibrant market environment, with ongoing developments aimed at enhancing the effectiveness of airbag systems in protecting vehicle occupants. For instance,

- The Dainese Smart Air, an innovative smart jacket by Dainese, based in Italy, offers improved usability and certified protection. The product features a user-replaceable inflator and wireless firmware updates via the D-Air app for Android and iOS.

Launch of Lightweight and Unique Materials to Create Fresh Prospects

The automotive industry's ongoing emphasis on reducing weight and using specialized materials is shaping the global automotive airbag inflation market. The push for better fuel efficiency and lighter vehicles has prompted manufacturers to explore new materials for inflator production. While traditional inflators typically used steel, innovations in materials science have led to the development of lightweight yet strong alternatives like composites and advanced alloys.

By adopting lightweight materials, manufacturers can reduce vehicle weight without sacrificing safety. This trend supports the automotive industry's objectives of enhancing fuel efficiency and minimizing environmental impact. As a result, makers of airbag inflators are incorporating innovative materials into their designs. They are creating new products that not only perform well in crash situations but also align with the goals of sustainable automotive engineering.

Category-wise Analysis

Product Type Insights

The pyrotechnic inflator segment holds 48.4% market share due to proven reliability, rapid deployment, and manufacturing maturity. Pyrotechnic inflators achieve full airbag inflation within 20–50 milliseconds, ensuring effective occupant protection during high-impact collisions. Their consistent performance across extreme temperatures (-40°C to +70°C) and cost-efficient, well-established production processes make them the preferred choice for mass-market vehicles. Decades of manufacturing optimization, standardized OEM specifications, and well-defined regulatory approval frameworks further reinforce their dominance.

The hybrid inflator segment is the fastest-growing, expanding at a 5.6% CAGR through 2033. Hybrid systems combine pyrotechnic and stored-gas technologies to enable multi-stage inflation, enhanced crash adaptability, and occupant-specific deployment. Weight reduction, advanced sensor integration, and improved safety performance are driving adoption, particularly in premium and next-generation vehicle platforms.

Component Type Insights

Airbag inflator filter components hold 53.2% market share due to their critical role in ensuring safe airbag deployment. During pyrotechnic combustion, inflators generate gases at 300–500°C, which contain particulates that must be filtered to prevent airbag fabric damage and occupant injury. Filters require advanced materials such as ceramics, fiberglass, and specialty composites, driving high material and manufacturing costs that account for 40–50% of the total value of the inflator system. Stringent performance validation and regulatory certification further reinforce their dominance, while specialized manufacturing limits supplier concentration.

Airbag tubes are the fastest-growing component, expanding at 7% CAGR through 2033. Growth is driven by multi-stage airbag deployment, innovative tube geometries for optimized inflation, compact vehicle interior integration, and advanced materials enabling thermal resistance and sensor-enabled diagnostics in next-generation restraint systems.

Vehicle Type Insights

The passenger vehicle segment holds 67.4% market share due to comprehensive airbag requirements and dominant global production volumes. Over 60 million passenger vehicles are produced annually, making them the primary source of demand for airbag inflators. Regulatory mandates require multiple airbags—front, side, curtain, and increasingly center airbag resulting in 8–12 inflators per vehicle in modern models. Rising consumer emphasis on safety ratings and willingness to pay for advanced protection support widespread OEM adoption. Platform-level standardization by major automakers further enables high-volume inflator sourcing, while a large installed base of over 300 million passenger vehicles sustains aftermarket replacement demand.

The light commercial vehicle segment is the fastest-growing, expanding at a 6% CAGR through 2033. Growth is driven by expanding safety regulations, fleet modernization, rising commercial vehicle production in emerging markets, and higher vehicle utilization rates, increasing replacement demand.

Component Insights

Landing gear steering systems account for 41.3% of component market share, driven by high cost, system complexity, and growing technology content. Advanced steering assemblies account for 35% of total landing gear cost and integrate actuators, sensors, and control electronics. Enhanced control precision reduces ground handling incidents by 20%, justifying premium OEM specifications. Increasing adoption of electronically controlled steering enables automated taxiing and tighter integration with fly-by-wire systems, while retrofit programs for narrow-body fleets prioritize steering electrification. Steering systems dominate nose landing gear value, reinforcing revenue concentration and market leadership.

Actuation systems are the fastest-growing component segment (17% CAGR through 2033), driven by the shift from hydraulic to electro-mechanical systems. Electric actuation delivers 16% weight reduction, 25% lower maintenance costs, smart diagnostics for predictive maintenance, and standardization across next-generation aircraft platforms, accelerating adoption.

Regional Insights

North America Automotive Airbag Inflator Market Analysis

Market Scale and Performance: North America commands approximately 35% of global Automotive Airbag Inflator market share, valued at approximately US$ 1.82 billion in 2026 with projections approaching US$ 2.5 billion by 2033. The United States represents dominant regional market contributor, accounting for 80% of North American market value, driven by comprehensive vehicle safety regulation and high-volume automotive manufacturing.

Vehicle production dominance, with Detroit automakers (Ford, GM, Stellantis) and international OEMs maintaining North American manufacturing facilities establishing significant inflator demand. Safety regulation leadership, with NHTSA advancing vehicle safety standards and mandating comprehensive airbag system deployment establishing specification requirements. Premium vehicle market concentration, with North American consumers prioritizing vehicle safety features and accepting technology premium supporting advanced inflator system adoption.

Europe Automotive Airbag Inflator Market Analysis

Europe represents approximately 25% of global Automotive Airbag Inflator market share, valued at approximately US$ 1.25 billion in 2026. Germany, France, and Italy collectively represent 70% of European market value, reflecting automotive manufacturing concentration and advanced safety technology emphasis.

Automotive manufacturing concentration, with German automakers (Volkswagen, BMW, Mercedes-Benz, Audi) maintaining significant European manufacturing and establishing inflator specification leadership. Euro NCAP standard advancement, with consumer safety organization testing driving manufacturer competitive differentiation through advanced airbag system adoption. Sustainability focus, with European environmental emphasis driving lightweight material development and energy-efficient inflator system advancement.

Asia Pacific Automotive Airbag Inflator Market Analysis

Asia Pacific demonstrates robust growth dynamics, commanding approximately 25% market share with projections increasing to 35% by 2033. The region valued at approximately US$ 1.23 billion in 2026 is anticipated to reach US$ 2.0 billion by 2033, representing fastest-growing regional market with an estimated CAGR of 7%.

Vehicle production acceleration, with China, India, Japan, and ASEAN nations achieving 40+ million vehicle production annually, establishing proportionate inflator demand. Safety regulation implementation, with China, India, and ASEAN countries implementing comprehensive vehicle safety standards, and establishing compliance requirements for all manufacturers. Emerging market motorization, with 300-500 million emerging market consumers entering vehicle purchasing establishing rapid fleet growth.

Competitive Landscape

The global automotive airbag inflator market demonstrates moderate consolidation, with established automotive suppliers and specialized manufacturers maintaining competitive positions.

The top 10 suppliers, including Autoliv Inc., ZF Friedrichshafen, Toyoda Gosei, Joyson Electronics, KSS, Daicel Corporation, Semtech, Advanced Airbag Systems, Ashimori Industry, and Fenghua Advanced Technology, collectively control approximately 60% of global market share, reflecting technology leadership, manufacturing scale, and OEM relationships.

Market structure reflects bifurcation between multinational automotive suppliers offering comprehensive safety system solutions and specialized manufacturers focusing exclusively on inflator technology development.

Key Industry Developments:

- In September 2024, Chennai-based ZF Rane Automotive India Pvt Ltd. opened a new inflator plant and sled test facility in Tiruchirappalli, Tamil Nadu, to boost local manufacturing capabilities and meet market demands. The joint venture, which invested around US$ 12 Mn, will produce about 3 million inflators per annum for driver and passenger versions. The facility also enhances testing capabilities and reduces the company's lead time.

- In June 2024, Autoliv China and XPENG AEROHT, Asia's leading flying car innovators, signed a strategic cooperation agreement to develop safety solutions for future mobility. These companies aim to combine their unique technology and safety solutions expertise to create safe electric flying cars for individual users.

Companies Covered in Automotive Airbag Inflator Market

- Autoliv Inc.

- Joyson Safety System

- Robert Bosch GmbH

- Toyoda Gosei Co. Ltd

- Nippon Kayaku

- TRW Automotive

- Aptiv PLC

- Daicel Corporation

- ARC Automotive, Inc.

- Others Key Players

Frequently Asked Questions

The Automotive Airbag Inflator market is estimated to be valued at US$ 4.9 Bn in 2026.

The key demand driver for the Automotive Airbag Inflator market is the global tightening of vehicle safety regulations and mandatory airbag installation requirements.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Automotive Airbag Inflator market.

Among the Product Type, Narrow-Body holds the highest preference, capturing beyond 48.4% of the market revenue share in 2026, surpassing other Product Type.

The key players in Automotive Airbag Inflator are Autoliv Inc., Joyson Safety System, Robert Bosch GmbH, Toyoda Gosei Co. Ltd, and Nippon Kayaku.