- Automation & Robotics

- Fire Protection System Market

Fire Protection System Market Size, Share, and Growth Forecast for 2025 - 2032

Fire Protection System Market By Product Type (Fire Detection Systems, Fire Extinguishers, Others), Service Outlook (Managed Service, Installation and Design Service, Others), End-user (Residential, Commercial, and Industrial, and Regional Analysis for 2025 - 2032

Fire Protection System Market Size and Trends Analysis

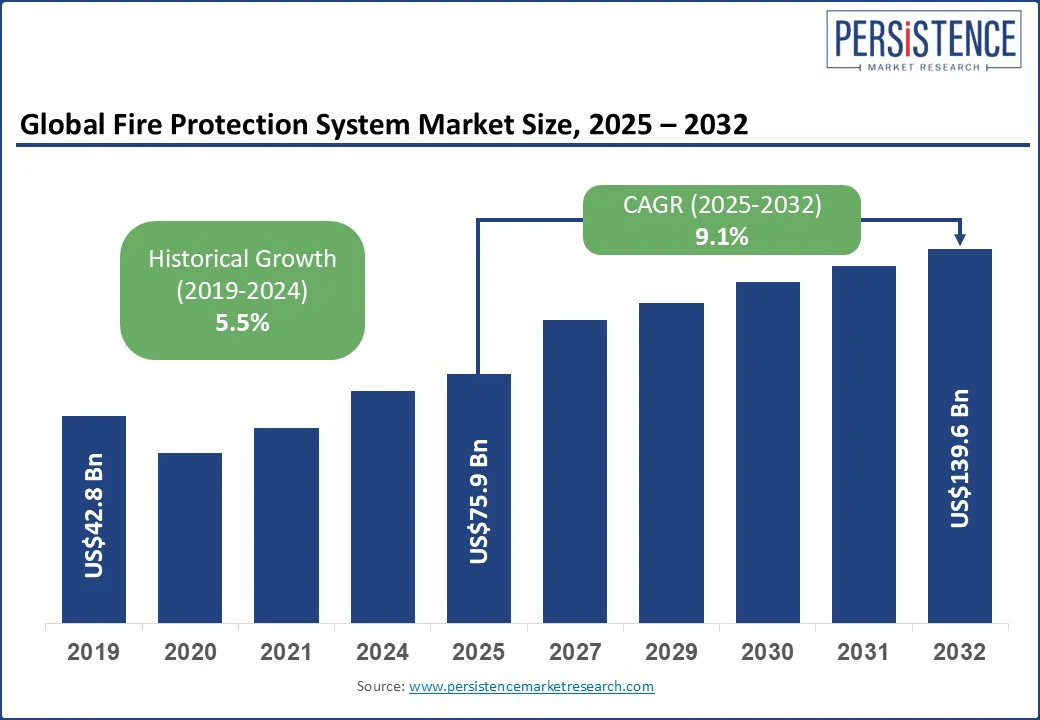

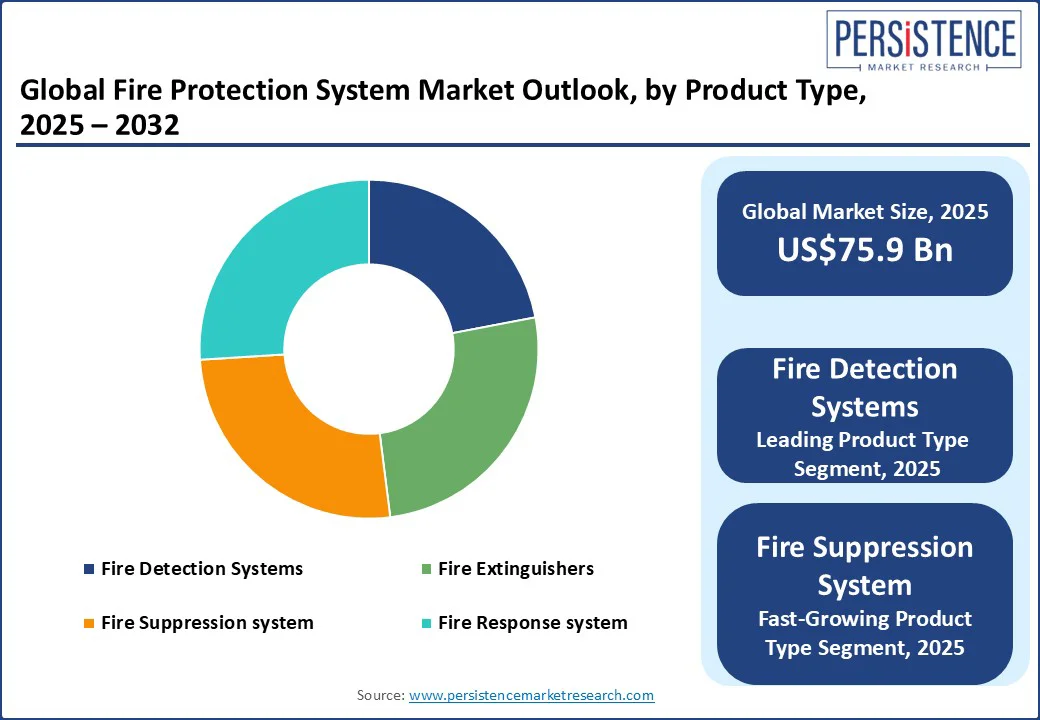

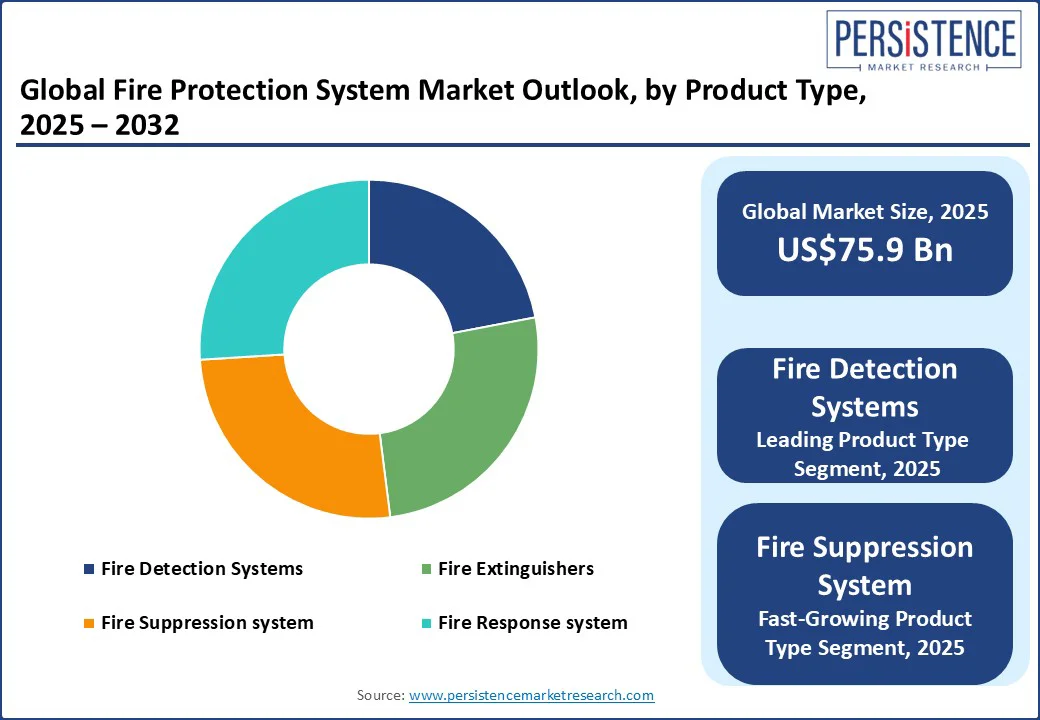

The global fire protection system market size is projected to rise from US$75.9 Bn in 2025 to US$139.6 Bn by 2032. It is anticipated to witness a CAGR of 9.1% during the forecast period from 2025 to 2032.

Fire Protection Systems (FPS) refer to emergency response equipment designed to be deployed in the event of fires, including fire detection systems, fire extinguishers, fire suppression systems, fire response systems, and related sub-segments. Fire protection system market dynamics are shaped by the rapid development and growing adoption of wireless fire detection systems, which seamlessly integrate with smart building control platforms, enhancing flexibility and real-time responsiveness.

From a regulatory standpoint, governments are enforcing stricter fire safety standards, thereby driving consistent demand for system upgrades, retrofits, and ongoing maintenance services.

Additionally, the enforcement of stringent cybersecurity regulations, particularly for Industrial Control Systems (ICS), is accelerating the adoption of advanced measures, especially in highly regulated sectors such as oil & gas, energy, and manufacturing.

Key Industry Highlights:

- Leading Region: North America is anticipated to dominate, accounting for a share of 30% in 2025, driven by a surge in non-residential fire accidents and robust construction sector investments across the U.S., Mexico, and Canada.

- Fastest-growing Region: The Asia Pacific fire protection system market is set to register the fastest CAGR, driven by rapid urbanization and extensive commercial construction.

- Product Type: In 2025, fire detection systems are projected to account for over 57% of market revenue, comprising devices that work together to detect and alert occupants through audio-visual signals during fire, smoke events, carbon monoxide release, or other emergencies.

- Leading End-user: The commercial segment is expected to lead the market in 2025, with over 47% revenue, driven by strict global fire prevention regulations across sectors such as retail, BFSI, government, healthcare, and education.

|

Global Market Attribute |

Key Insights |

|

Fire Protection System Market Size (2025E) |

US$75.9 Bn |

|

Market Value Forecast (2032F) |

US$139.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

9.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Dynamics

Driver - Increasing Adoption of Smart and Integrated Fire Protection Systems

FPS are increasingly deployed across buildings to detect, control, and alert occupants in the event of a fire, thereby reducing casualties and minimizing property loss. This critical functionality is a key factor driving market growth. The system comprises components such as fire detectors, extinguishers, hydrant systems, hose reels, and automatic sprinklers.

Technological advancements, particularly in wireless integration, are enhancing system efficiency and responsiveness. For instance, in September 2021, Johnson Controls introduced body-worn cameras and autonomous robots integrated with RaySecur-powered screening technology, extending building safety far beyond traditional fire and access control solutions.

Furthermore, stringent fire safety regulations enforced by global authorities are compelling building owners to adopt certified FPS, further accelerating market expansion.

Restraint - High Initial Capital Investments May Restrain Market Growth

Advanced FPS comprising intelligent detection devices, automated suppression equipment, and integrated monitoring solutions requires substantial upfront capital for procurement, installation, and integration. This high initial investment can be a major deterrent, particularly for small and medium-sized enterprises, budget-constrained organizations, and businesses in price-sensitive markets.

In many cases, stakeholders may opt for basic or low-cost systems to reduce expenditure, potentially compromising the effectiveness and compliance of fire safety measures. The challenge is more pronounced in emerging economies, where limited financial resources and competing infrastructure priorities can slow down adoption. As a result, despite the long-term safety and operational benefits, high capital requirements continue to hinder the widespread deployment of technologically advanced FPS.

Opportunity - Rising Popularity of Foam-based Fire Detectors

Foam-based FPS, made of air-filled bubbles generated from aqueous solutions, is highly effective in combating flammable liquid fires. By forming a floating blanket over the fuel surface, these systems exclude oxygen, cool the fuel, and prevent re-ignition by suppressing the release of flammable vapors. Their ability to provide rapid and comprehensive fire suppression makes them ideal for high-risk industrial applications such as refineries, petrochemical plants, and oil & gas facilities, as well as commercial storage areas.

With increasing industrialization and expansion of hazardous material handling equipment facilities worldwide, demand for reliable and efficient foam-based systems is set to rise. Additionally, the push for improved safety standards and compliance in industries handling volatile fuels offers manufacturers a strong opportunity to expand foam-based offerings, particularly in emerging markets where industrial safety infrastructure is rapidly evolving.

Category-wise Analysis

Product Type Insights

By product type, fire detection systems accounted for over 57% of market revenue in 2025, comprising devices that work together to detect and alert occupants through audio-visual signals during fire, smoke, carbon monoxide, or other emergencies. Regulatory mandates, such as those from the National Fire Protection Association (USA) and the Building Code of Australia, are driving demand for these systems.

Fire suppression systems reduce heat release and prevent re-ignition by applying water, dry chemical powder, or other agents directly to the fuel source. Rising adoption of eco-friendly suppression agents, rapid industrialization, and commercial construction growth are creating lucrative opportunities. Renovations and new infrastructure projects must meet strict fire safety codes, prompting market players to invest to comply with government regulations and safety obligations.

End-user Insights

The commercial application segment dominated the market and accounted for the highest share, exceeding 47.0% revenue in 2025. The commercial application segment comprises applications for retail, BFSI, government, healthcare, telecom, and IT educational institutions.

The demand for FPS in commercial applications is increasing due to the formulation of stringent government rules for fire prevention and control across the globe. Furthermore, increasing investments by companies to reduce loss of property and life and safeguard the infrastructure are expected to fuel the demand for FPS.

The industrial application segment is projected to record the highest CAGR during the forecast period. Key sectors include oil and gas, mining, energy and power, and manufacturing. The need to protect automated systems from fire hazards is a major growth driver. In high-risk industries, emphasis is placed on installing comprehensive fire protection and prevention systems, with strict government safety regulations further boosting adoption in the industrial sector.

Regional Insights

North America Fire Protection System Market Trends - Fire Incidents and Emphasis on Strengthening Safety Policies

North America is projected to lead the global market in 2025, accounting for 30% of the total market share. This dominance is driven by a surge in non-residential fire incidents and sustained investment in construction across the U.S., Mexico, and Canada. In 2024, construction accounted for 4.5% of U.S. GDP, with total gross output exceeding US$ 2.2 Tn, including US$ 2 Tn in industry spending and a record-setting workforce of 8.3 million.

The American Institute of Architects projects that spending on non-residential buildings, such as commercial, industrial, and institutional facilities, will grow by 2.9% by mid-2026. This follows strong gains of nearly 20% in 2023 and 6% in 2024, reflecting a continued, albeit slower, upward trend in construction investment.

In 2024, the U.S. reported 64,897 wildfires, burning 8,924,884 acres, a marked increase over 2023's 56,580 fires and 2.7 million acres burned. The U.S. experienced approximately 1,389,000 fires in 2023, down from 1,504,500 in 2022.

These incidents resulted in 3,670 deaths, 13,350 injuries, and an estimated US$ 23.2 Bn in property damage. From 2022 to 2023, NFPA data shows a 7.7% reduction in total fires, a 3.2% decrease in deaths, but one percent rise in civilian injuries. These trends highlight a nuanced shift in fire-related risks, reinforcing the importance of advanced detection, suppression, and prevention technologies in high-risk environments.

Asia Pacific Fire Protection System Market Trends - Rapid Urbanization and Extensive Commercial Construction

Asia Pacific is set to register the fastest CAGR, driven by rapid urbanization and extensive commercial construction. Countries such as China and India are leading this growth, supported by stricter enforcement of fire codes and significant infrastructure investments. Expanding high-density residential, commercial, and industrial zones is boosting system installation rates.

In India, the market is projected to grow at a robust CAGR, fueled by urban expansion, new high-rise and commercial developments, and stronger compliance with fire safety regulations. In China, rapid urbanization, massive real estate projects, industrialization, and government-backed infrastructure developments are spurring demand. Stricter national fire safety standards are driving adoption across residential, commercial, and industrial sectors, solidifying the country’s position as a key growth engine in the regional market.

Europe Fire Protection System Market Trends - Stringent Standards and Retrofit Demand

Europe is driven by strict fire safety standards, comprehensive insurance mandates, and a mature enforcement landscape. Efforts to renovate and retrofit aging building stock, including historic and cultural sites, boost demand for both traditional and clean-agent solutions. Eco-friendly and digitally integrated systems are gaining traction as sustainability and performance become key priorities.

The U.K. is projected to grow at a significant CAGR over the forecast period. Growth is driven by strict fire safety standards, a robust regulatory framework, and insurance-led compliance in commercial and institutional sectors. Trends include rapid adoption of clean-agent and environmentally friendly suppression systems in data centers, offices, and public buildings.

France’s market represented a considerable portion of Europe’s regional revenue. The country’s strict fire codes and insurance mandates drive consistent adoption, especially in commercial, cultural, and residential buildings.

Competitive Landscape

The global fire protection system market is becoming increasingly competitive as key players take strategic steps to tap into growth opportunities, especially in emerging regions. Companies are prioritizing the launch of advanced and intelligent fire safety products to meet evolving customer demands. One notable trend is the development of compact, high-performance fire alarm control panels that offer powerful capabilities while being easy to install, commission, and maintain.

To strengthen their market position, firms are actively pursuing mergers, acquisitions, and strategic partnerships, particularly with local distributors to expand their reach and enhance product offerings. With the rising demand for efficient, reliable, and technology-driven FPS across industries, competition is fueling continuous innovation. This dynamic landscape is shaping a market focused on smarter, more connected, and cost-effective fire safety solutions.

Key Industry Developments

- In October 2024, Siemens Smart Infrastructure announced its acquisition of Danfoss Fire Safety, a Denmark-based subsidiary specializing in sustainable fire suppression technologies, particularly high-pressure water mist systems. This acquisition strengthens Siemens's fire safety portfolio by integrating environmentally friendly and rapidly growing fire suppression solutions.

- In April 2024, Honeywell International Inc. launched the Fire Lite alarm system for small and medium enterprises across residential, commercial, and industrial sectors, featuring cloud support, remote operation, and enhanced compliance.

Companies Covered in Fire Protection System Market

- Consilium AB

- DESAUTEL SAS

- HALMA PLC

- Hochiki Corporation

- Johnson Controls International Plc

- United Technologies Corporation

- Yamato Protec Corporation

- Robert Bosch GmbH

- Siemens AG

- Honeywell International, Inc.

- Swastik Synergy Engineering Private Limited

- Gentex Corporation

Frequently Asked Questions

The fire protection system market is set to reach US$ 75.9 Bn in 2025.

Major growth drivers include stringent government regulations and safety standards, along with rapid urbanization and infrastructure development.

The fire protection system market is estimated to grow at a CAGR of 9.1% through 2032.

Key market opportunities include the integration of IoT and smart technologies, along with rising demand from emerging economies.

Consilium AB, DESAUTEL SAS, HALMA PLC, Hochiki Corporation, and Johnson Controls International Plc are a few leading players.