- Hardware & Software IT Services

- Industrial Control Systems (ICS) Security Market

Industrial Control Systems (ICS) Security Market Size, Share, and Growth Forecast, 2025 - 2032

Industrial Control Systems (ICS) Security Market By Component (Solutions, Services), Security Type (Network Security, Endpoint Security), Control System Type (Supervisory Control and Data Acquisition (SCADA), Distributed Control System (DCS), Others), End-use, and Regional Analysis for 2025 – 2032

Industrial Control Systems (ICS) Security Market Size and Trends Analysis

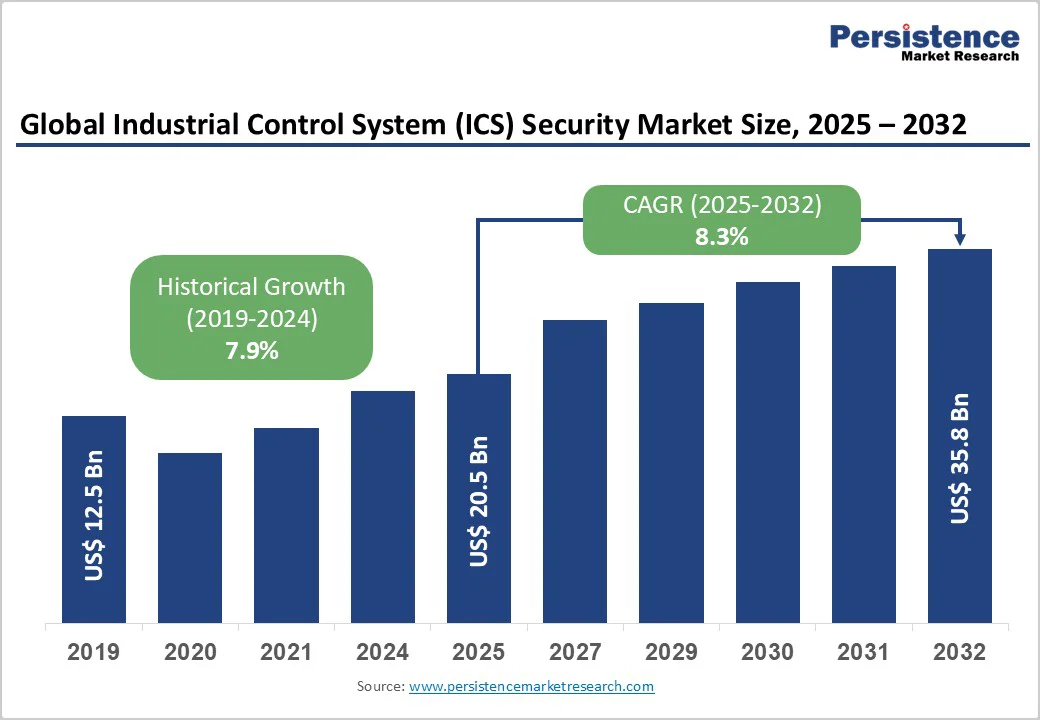

The global industrial control systems (ICS) security market size is likely to be valued US$20.5 Billion in 2025, projected to US$35.8 Billion by 2032, growing at a CAGR of 8.3% during the forecast period from 2025 to 2032, driven by the increasing prevalence of cyber threats to critical infrastructure, rising demand for OT/IT convergence, and advancements in AI-based threat detection. The need for zero-trust architecture and compliance, particularly in power utilities, has significantly boosted the adoption of industrial control systems (ICS) security across various industries. The market is further propelled by innovations in network security and SCADA solutions, catering to preferences for proactive and integrated options. The growing acceptance of industrial control systems (ICS) security as essential for operational resilience, particularly in oil and gas, is a key growth factor.

Key Industry Highlights

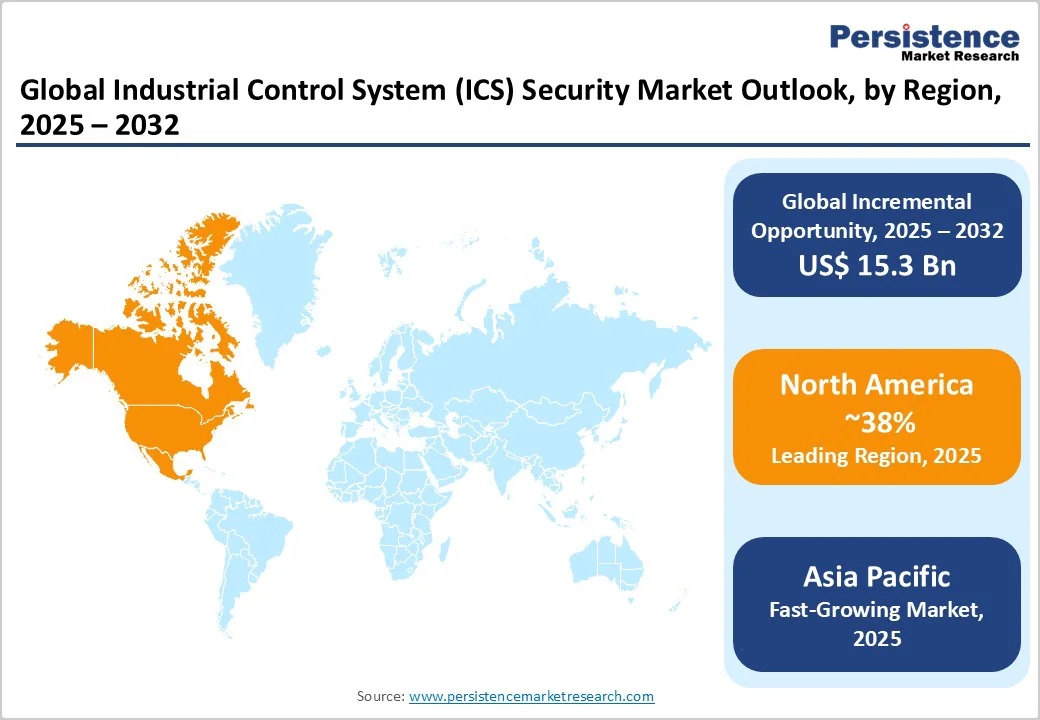

- Leading Region: North America, commanding a 38% market share in 2025, driven by stringent CISA regulations, high prevalence of critical infrastructure, and strong R&D activities in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rapid industrialization, rising awareness of OT security, and growing investments in smart grids in China and India.

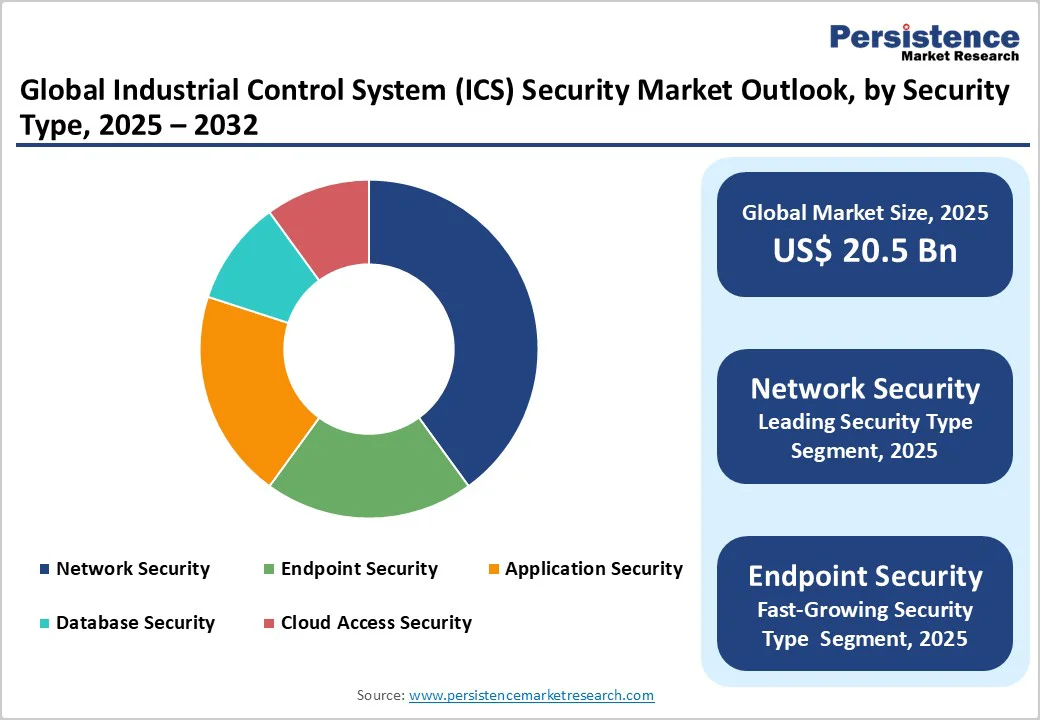

- Dominant Component: Solutions, holding approximately 60% of the market share, due to core threat detection tools.

- Leading Security Type: Network Security, accounting for over 40% of market revenue, driven by perimeter defense needs.

- Leading Control System Type: SCADA, contributing nearly 45% of market revenue, due to widespread deployment.

- Leading End-use: Power and Utilities, with approximately 30% share, driven by grid protection.

- Key Market Driver: Rapid automation and cloud-based SCADA deployments expand the attack surface, creating demand for modern security solutions.

- Market Opportunity: Growing use of AI-driven threat detection and predictive analytics offers opportunities for smarter, automated security solutions.

| Key Insights | Details |

|---|---|

| Industrial Control Systems (ICS) Security Market Size (2025E) | US$20.5 Bn |

| Market Value Forecast (2032F) | US$35.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Cyber Threats to Critical Infrastructure and Demand For OT/IT Convergence

The increasing prevalence of cyber threats to critical infrastructure globally is driving the demand for stronger convergence between Operational Technology (OT) and Information Technology (IT). As industries adopt digital transformation and automation, interconnected systems create vulnerabilities that cybercriminals increasingly exploit. Attacks targeting industrial control systems (ICS) and SCADA networks can disrupt operations, cause financial losses, and pose safety risks.

Enterprises are prioritizing the integration of OT and IT to enhance real-time visibility, threat detection, and coordinated response mechanisms. OT/IT convergence enables seamless data exchange between operational assets and enterprise networks, allowing predictive maintenance, automated security updates, and unified monitoring. The adoption of advanced technologies such as AI-driven analytics, zero-trust architectures, and edge computing further strengthens cyber resilience. Governments and industry bodies are also implementing stricter cybersecurity standards and frameworks to safeguard critical infrastructure.

High Implementation and Skill Gap Costs

The high costs associated with implementation and the skill gap in industrial control systems (ICS) security pose a significant restraint on market growth. Integrating complex systems such as industrial automation, cybersecurity frameworks, or digital twin solutions requires substantial capital investment in hardware, software, and network infrastructure. Small and medium-sized enterprises often struggle to justify these expenses due to limited budgets and uncertain return on investment.

Beyond infrastructure, the shortage of skilled professionals with expertise in both IT and OT domains exacerbates the issue. Bridging this talent gap demands extensive training, upskilling programs, and recruitment of specialized personnel, further increasing operational costs. Improper implementation or lack of skilled oversight can lead to system inefficiencies, downtime, and security vulnerabilities, amplifying financial risks. The need for continuous updates, maintenance, and compliance with evolving standards also adds to long-term expenses.

Advancements in AI-Based Threat Hunting and Zero-Trust Frameworks

Advancements in AI-based threat hunting and zero-trust frameworks present significant growth opportunities for the Industrial Control Systems (ICS) Security Market. AI-driven threat hunting leverages machine learning algorithms to detect anomalies, identify hidden threats, and predict potential breaches before they occur. Unlike traditional security systems that rely on predefined rules, AI continuously learns from data patterns, improving accuracy and response speed.

This proactive approach enables organizations to neutralize sophisticated cyberattacks, such as ransomware and insider threats, with minimal manual intervention. Complementing this, the zero-trust framework operates on the principle of “never trust, always verify,” ensuring continuous authentication and strict access control for every user, device, and application. AI-based analytics and zero-trust architectures create a multilayered defense mechanism that enhances visibility, reduces attack surfaces, and mitigates risks associated with remote access and cloud environments.

Category-wise Analysis

Component Insights

Solutions dominate the market, accounting for 60% of the share in 2025. Its dominance is driven by core tools such as firewalls, ensuring protection. Solutions, such as those from Palo Alto, provide intrusion prevention, ensuring compliance. Its integration and updates make it preferred for manufacturers.

Services is the fastest-growing segment, due to rising demand for managed security and the expanding role of Managed Security Service Providers (MSSPs). These services offer specialized expertise essential for securing complex OT environments. Growing emphasis on consulting and customized solutions further accelerates adoption, particularly across Asia Pacific and Europe’s rapidly digitalizing industries.

Security Type Insights

Network Security leads the market, holding 40% of the share in 2025, driven by the need for strong perimeter defense and widespread use of firewalls. Its role in securing communication channels and enabling network segmentation makes it vital for protecting connected systems. Rising cyber threats and compliance requirements continue to fuel demand across industries.

Endpoint Security is the fastest-growing segment, fueled by the rising need for device hardening and increased IoT adoption. Its agent-based approach offers convenience, continuous monitoring, and enhanced visibility across connected endpoints. As remote work and smart device usage expand, organizations increasingly invest in endpoint protection to prevent breaches and ensure network integrity.

Control System Type Insights

Supervisory Control and Data Acquisition (SCADA) dominate the market, contributing 45% share in 2025. Their widespread adoption in utilities and critical infrastructure stems from strong remote monitoring and control capabilities. SCADA’s ability to provide real-time visibility and operational efficiency makes it the preferred choice for large-scale industrial operations

Distributed Control System (DCS) is the fastest-growing segment, driven by its expanding use in process industries and heightened focus on operational safety. Its flexible architecture and built-in redundancy enhance reliability and control efficiency. Industries such as oil & gas, chemicals, and power generation increasingly adopt DCS for stable, continuous, and secure operations.

End-use Insights

Power and Utilities dominate the market, with 30% share in 2025, driven by the critical nature of power grids and compliance with NERC CIP standards. Their extensive use in substations for monitoring and control ensures operational reliability. Rising energy demand and grid modernization further strengthen the sector’s dominance in cybersecurity adoption.

Oil and Gas is the fastest-growing, driven by increasing cyber threats targeting pipelines and upstream operations. The sector’s high-stakes environment and reliance on remote monitoring systems amplify the need for advanced security solutions. Growing digitalization, coupled with stringent safety and compliance requirements, further accelerates cybersecurity adoption across exploration and production facilities.

Regional Insights

North America Industrial Control Systems (ICS) Security Market Trends

North America is accounting for 38% share in 2025, driven by CISA directives and critical infrastructure in the U.S. his dominance is driven by stringent cybersecurity regulations such as NERC CIP and initiatives from the Cybersecurity and Infrastructure Security Agency (CISA), which mandate robust protection for critical infrastructure. The increasing convergence of Operational Technology (OT) and Information Technology (IT), alongside the adoption of IIoT sensors, remote access solutions, and cloud-based SCADA platforms, has expanded the region’s attack surface.

Organizations are investing heavily in advanced ICS-specific security solutions. AI- and ML-powered anomaly detection, zero-trust architectures, and network segmentation are becoming integral to industrial networks. The demand for managed and consulting services is also surging, as industries rely on external expertise to handle complex OT environments. Challenges persist, including outdated legacy systems and a shortage of skilled ICS security professionals.

Europe Industrial Control Systems (ICS) Security Market Trends

Europe hold 26% share in 2025, driven by stringent regulatory frameworks and the rising frequency of cyberattacks targeting critical infrastructure. The enforcement of the EU’s NIS2 Directive, along with GDPR and industry-specific standards, is pushing organizations to strengthen their cybersecurity posture. The region’s strong industrial base in manufacturing, energy, and utilities further amplifies the need for secure and resilient control systems.

As digitalization and Industry 4.0 initiatives accelerate, the integration of IT and OT networks has expanded the threat landscape, increasing demand for advanced ICS protection. Companies are adopting AI-based analytics, zero-trust frameworks, and network segmentation to enhance visibility and mitigate risks. The managed security services segment is also growing rapidly, as firms seek specialized expertise to secure complex OT environments. Key economies such as Germany, the UK, and France lead adoption due to their advanced industrial infrastructure.

Asia Pacific Industrial Control Systems (ICS) Security Market Trends

Asia Pacific is the fastest-growing market for industrial control systems (ICS) security, driven by rapid industrialization, digital transformation, and the expansion of smart infrastructure. Countries such as China, India, Japan, and South Korea are heavily investing in automation, IIoT integration, and connected manufacturing, which has significantly widened the region’s cyberattack surface. The rising frequency of targeted attacks on utilities, energy networks, and production facilities has heightened awareness of OT security risks, prompting organizations to adopt advanced ICS security solutions.

Governments across the region are also implementing stricter cybersecurity frameworks and national regulations for critical infrastructure protection, further accelerating market adoption. While hardware and software solutions dominate, the demand for managed and consulting services is increasing due to the shortage of skilled OT security professionals. AI-driven threat detection, zero-trust models, and network segmentation are being rapidly implemented to strengthen resilience.

Competitive Landscape

The global Industrial Control Systems (ICS) Security Market is highly competitive, featuring a diverse mix of cybersecurity giants, automation vendors, and OT-focused specialists. In developed regions such as North America and Europe, major players such as Cisco Systems, ABB Group, and Honeywell dominate through extensive R&D investments, strong distribution networks, and comprehensive product portfolios covering both IT and OT security. In Asia Pacific, companies such as Kaspersky Labs and Trend Micro are gaining traction by offering localized and cost-effective solutions tailored to regional industrial environments.

competitive landscape is further shaped by the rapid adoption of AI-driven analytics, real-time monitoring, and zero-trust security architectures, which enhance predictive threat detection and response capabilities. Strategic collaborations, partnerships, and acquisitions are common as vendors seek to expand their technology ecosystems and address the growing complexity of industrial cybersecurity. Increasing demand for managed and cloud-based security services has prompted players to innovate beyond traditional firewalls and antivirus solutions.

Key Industry Developments

- In June 2025, Cisco unveiled a new network architecture to power the campus, branch, and industrial networks of the future. The new architecture delivers unmatched operational simplicity through unified management, next-generation networking devices purpose-built for AI workloads, and advanced security capabilities embedded into the network.

- In November 2025, Kaspersky has announced an enhanced version of its flagship industrial security platform, Kaspersky Industrial CyberSecurity (KICS), which now supports Linux nodes and includes an investigation graph for root-cause analysis across ICS endpoints and networks.

Companies Covered in Industrial Control Systems (ICS) Security Market

- ABB Group

- BAE Systems

- Cisco Systems

- Check Point

- DarkTrace

- Fortinet

- Honeywell International Inc.

- IBM Corporation

- Kaspersky Labs

- Microsoft Corporation

- Nozomi Networks

- Palo Alto

- Siemens AG

- Trend Micro Incorporated

Yokogawa Electric Corporation

Frequently Asked Questions

The global industrial control systems (ICS) security market is projected to reach US$20.5 Billion in 2025.

The rising prevalence of cyber threats to critical infrastructure and demand for OT/IT convergence are key drivers.

The market is poised to witness a CAGR of 8.3% from 2025 to 2032.

Advancements in AI-based threat hunting and zero-trust frameworks are key opportunities.

ABB Group, Cisco Systems, Honeywell International Inc., Siemens AG, and Nozomi Networks are key players.