- Specialty & Fine Chemicals

- Firearm Lubricants Market

Firearm Lubricants Market Size, Share, and Growth Forecast, 2026 – 2033

Firearm Lubricants Market by Product Type (Synthetic, Mineral Oil, Bio-Based, Blended), Form (Oils, Aerosol Spray, Grease, Liquid Lubricants, Dry Lubricants), and Regional Analysis for 2026 – 2033

Firearm Lubricants Market Size and Trends Analysis

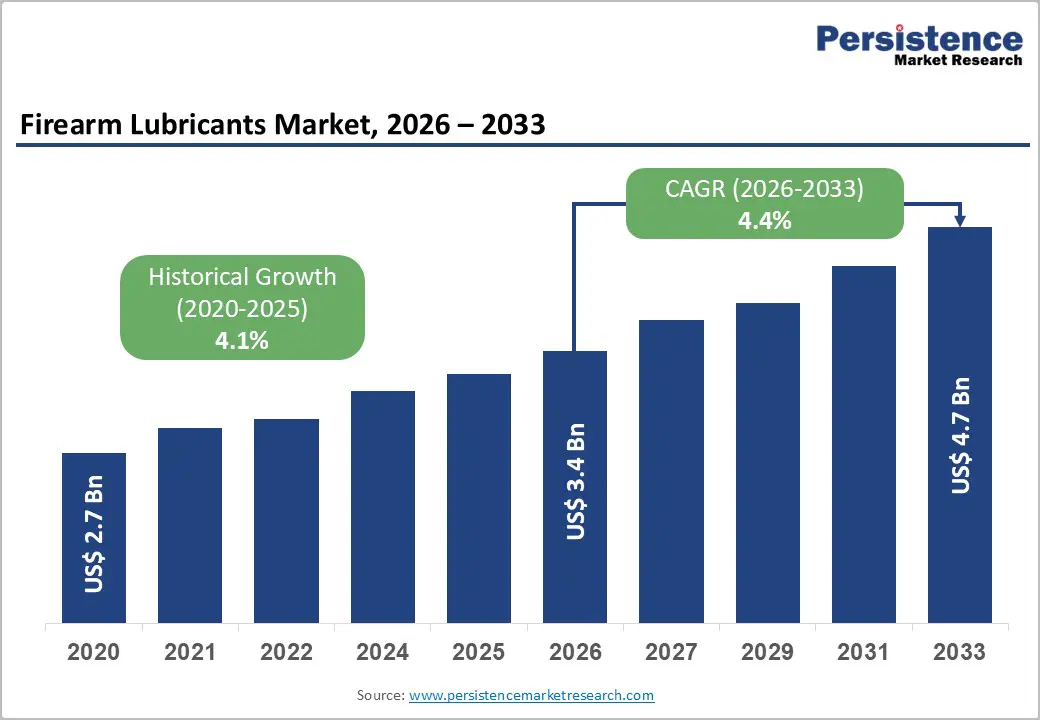

The global firearm lubricants market size is likely to be valued at US$3.4 billion in 2026 and is expected to reach US$4.7 billion by 2033, growing at a CAGR of 4.4% during the forecast period from 2026 to 2033, driven by consistent demand from military modernization programs, law enforcement maintenance protocols, and a steadily engaged civilian user base. The market’s expansion reflects sustained procurement cycles for small arms maintenance, increasing emphasis on weapon reliability, and the adoption of advanced lubrication technologies designed to perform under high-heat, high-friction, and extreme environmental conditions. Growing participation in shooting sports, recreational hunting, and private firearm ownership reinforces recurring demand for cleaning and lubrication solutions. Technological advancements are driving innovation in firearm lubricants, with manufacturers emphasizing synthetic and bio-based formulations, enhanced corrosion protection, and multi-function CLP (cleaner, lubricant, protectant) solutions to improve performance and extend firearm durability.

Key Industry Highlights:

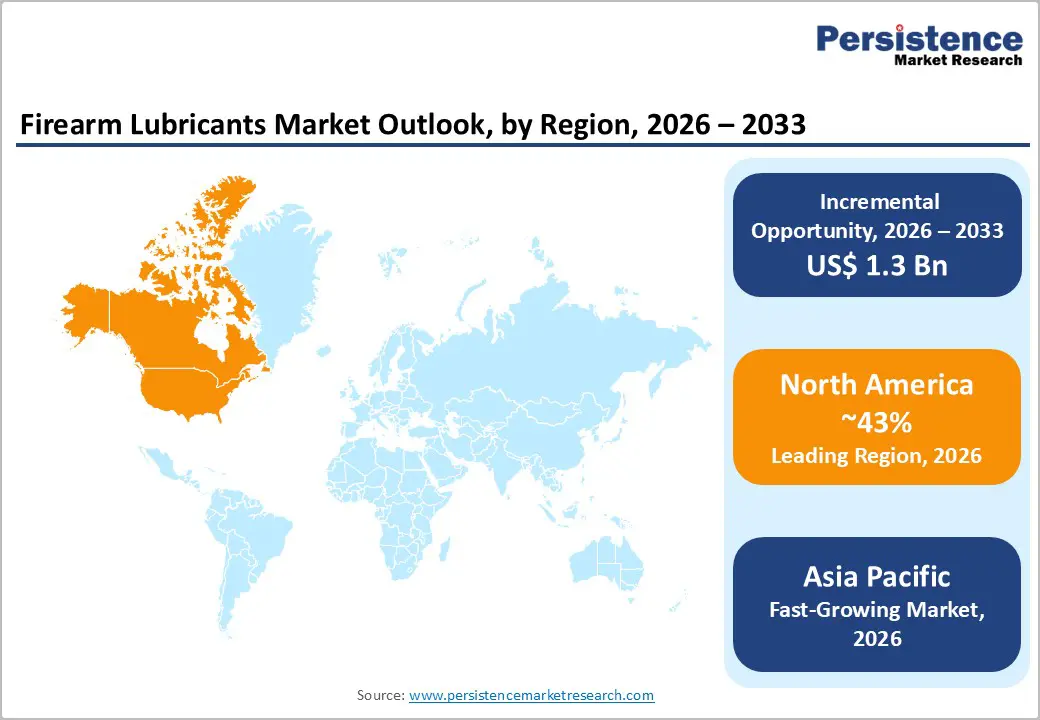

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 43% in 2026, driven by strong civilian ownership, defense procurement, and law enforcement demand.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rising defense expenditures, expanding domestic firearm manufacturing, and increasing demand from civilian and border-security segments.

- Leading Product Type: Synthetic lubricants are projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by their superior thermal stability, oxidation resistance, and high-performance reliability in military and high-volume civilian applications.

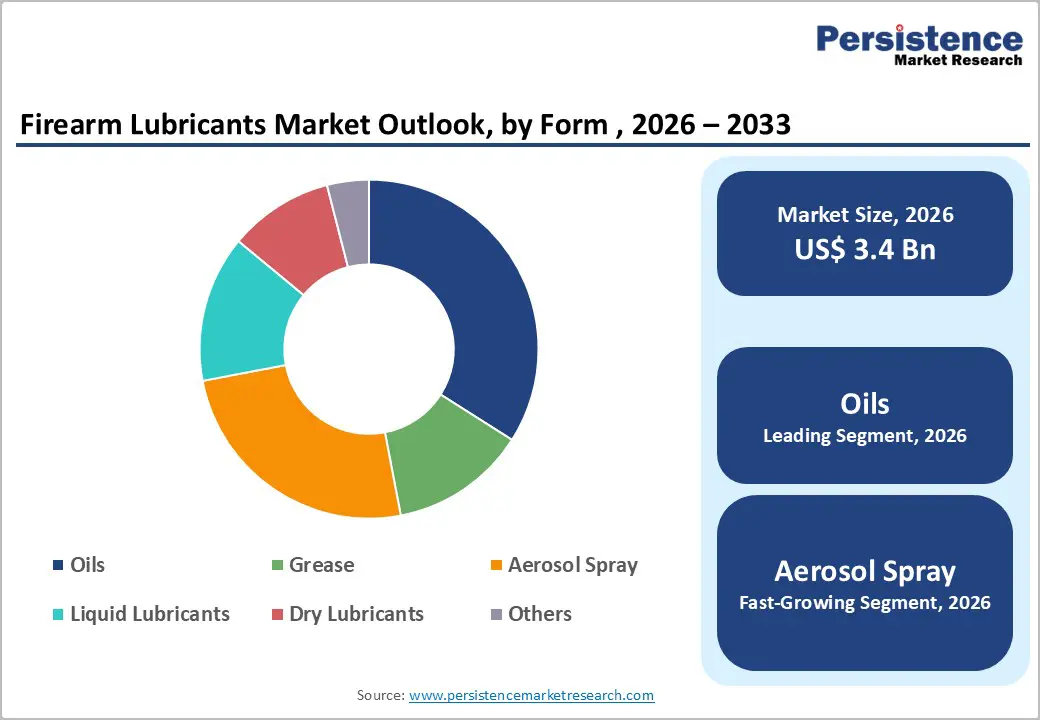

- Leading Form Type: Oils are anticipated to be the leading form type, accounting for over 45% of the revenue share in 2026, supported by their ease of application, deep penetration capability, and widespread use across military, law enforcement, and civilian firearm maintenance.

| Key Insights | Details |

|---|---|

| Firearm Lubricants Market Size (2026E) | US$3.4 Bn |

| Market Value Forecast (2033F) | US$4.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Military and Law Enforcement Procurement

Rising military and law enforcement procurement significantly drives demand in the firearm lubricants market, as operational readiness depends heavily on weapon reliability and durability. Defense agencies prioritize preventive maintenance protocols to ensure firearms perform consistently under extreme heat, humidity, sand, and cold conditions. Regular training exercises, border-security deployments, and modernization programs increase lubricant consumption volumes. Procurement contracts typically require high-performance formulations that meet military-grade specifications for corrosion resistance and thermal stability.

Law enforcement agencies also contribute substantially through standardized firearm maintenance schedules and fleet-wide servicing requirements. Patrol rifles, service pistols, and tactical weapons require routine cleaning and lubrication to prevent malfunctions and extend service life. Institutional purchasing ensures steady volume contracts rather than sporadic retail demand, creating predictable revenue streams for manufacturers. Specialized units operating in coastal, desert, or high-moisture regions require corrosion-resistant and low-temperature formulations. Increasing focus on reliability, officer safety, and reduced maintenance downtime accelerates the shift toward premium-grade lubricants.

Expansion of Shooting Sports, Hunting, and Civilian Ownership

Growing participation in competitive shooting events and range activities increases maintenance frequency, directly increasing lubricant consumption. Civilian firearm owners are increasingly educated about proper cleaning practices, encouraging routine use of oils, greases, and CLP formulations. Retail distribution through specialty stores and e-commerce platforms has improved accessibility, expanding market penetration. Seasonal hunting cycles and sport-shooting leagues create recurring purchasing patterns, strengthening demand stability within the civilian segment across developed and emerging markets.

Rising interest in personal defense and hobby shooting has supported growth in firearm accessory sales, including maintenance products. Consumers increasingly prefer premium synthetic lubricants that offer improved performance and reduced residue buildup. Social media communities, training programs, and firearm safety initiatives promote awareness of preventive maintenance benefits. Product differentiation through odorless, low-toxicity, and multi-function formulas appeals to home users seeking convenience. As civilian ownership expands in select regions, lubricant manufacturers benefit from repeat purchases, brand loyalty, and product bundling strategies, reinforcing sustained growth within the non-institutional segment.

Barrier Analysis - Negative Environmental Impact of Traditional Formulations

Traditional firearm lubricants often rely on petroleum-based ingredients and chemical additives that may pose environmental concerns. Improper disposal and runoff from cleaning activities can contribute to soil and water contamination. Volatile components may also release emissions during application, raising sustainability concerns among regulators and environmentally conscious users. Growing scrutiny over hazardous substances places pressure on manufacturers to reformulate products. As environmental standards evolve, companies face higher compliance costs associated with testing, labeling, and reformulation processes, which can limit flexibility and increase operational complexity within the market.

Environmental impact concerns also influence purchasing behavior among government and institutional buyers. Defense and law enforcement agencies increasingly incorporate sustainability benchmarks into procurement criteria. Traditional formulations that lack biodegradable properties lose competitiveness compared to eco-friendly alternatives. Environmental advocacy and consumer awareness campaigns have amplified scrutiny around chemical compositions. Smaller manufacturers with limited research budgets may struggle to transition toward greener formulations. These pressures collectively act as a restraint, particularly in regions with strict environmental policies, slowing the adoption of conventional petroleum-based lubricant products.

Stringent Regulatory Hurdles on VOCs and Chemical Composition

Stringent regulatory requirements regarding volatile organic compounds (VOCs) and chemical composition present a notable restraint in the firearm lubricants market. Many jurisdictions enforce strict emission standards that limit solvent content in aerosol sprays and liquid lubricants. Compliance demands extensive laboratory testing, certification, and reformulation, increasing production costs. Companies must adapt labeling and packaging to meet safety communication standards. Regulatory inconsistencies across regions complicate distribution strategies, requiring customized product variations for different markets. These barriers can delay product launches and reduce speed to market for innovative formulations.

Evolving chemical safety frameworks may restrict certain additives historically used for corrosion resistance and lubrication efficiency. Manufacturers must invest in research and alternative ingredient sourcing to maintain performance while complying with regulations. Smaller players face financial constraints in meeting documentation and certification requirements. Regulatory audits and import-export compliance checks add administrative burdens. Such constraints can discourage rapid expansion into new territories, especially where environmental laws are aggressively enforced, thereby moderating overall market growth potential.

Opportunity Analysis - Emergence of Bio-Based and Low-VOC Lubricants

The emergence of bio-based and low-VOC firearm lubricants presents significant growth opportunities for market participants. Increasing regulatory emphasis on sustainability and reduced emissions encourages the adoption of renewable-content formulations. Bio-based lubricants offer biodegradability and lower toxicity while maintaining competitive performance standards. Government procurement programs increasingly favor environmentally compliant products, expanding institutional opportunities. Civilian consumers also show a rising preference for eco-friendly alternatives that minimize odor and chemical exposure. These shifts create avenues for product innovation.

Manufacturers investing in green chemistry research can differentiate their portfolios and capture environmentally conscious segments. Advances in plant-derived base oils and additive technologies enable improved oxidation stability and corrosion resistance. Certification programs highlighting environmental compliance enhance brand credibility. Bio-based products also support export growth in regions with strict chemical regulations. As sustainability becomes a strategic priority across defense and civilian sectors, companies developing low-VOC, biodegradable solutions are well-positioned to gain a competitive advantage and long-term revenue expansion.

Technological Convergence with Smart Maintenance Solutions

Technological convergence with smart maintenance solutions offers emerging opportunities in the firearm lubricants market. Integration of advanced diagnostics, predictive maintenance systems, and digital tracking tools is gradually influencing firearm servicing practices. High-performance lubricants designed for compatibility with modern weapon systems enhance reliability and reduce maintenance frequency. As defense agencies adopt data-driven asset management systems, lubricant selection increasingly aligns with performance analytics and lifecycle optimization strategies. This transition encourages the development of specialized formulations tailored for specific weapon platforms.

Manufacturers can leverage innovation by offering value-added solutions such as condition-monitoring guidance, traceable batch formulations, and performance-certified products. Partnerships with firearm producers and defense contractors may facilitate co-developed maintenance solutions. Smart maintenance ecosystems emphasize durability, heat resistance, and corrosion control, favoring advanced synthetic blends. As weapon systems become more technologically sophisticated, the demand for precision-engineered lubricants increases to ensure consistent performance, reduced wear, and enhanced operational reliability. Companies aligning product development with digital maintenance trends can unlock new premium segments and strengthen long-term market positioning.

Category-wise Analysis

Product Type Insights

Synthetic lubricants are expected to lead the firearm lubricants market, accounting for approximately 40% of revenue in 2026, driven by their superior thermal stability, oxidation resistance, and long service intervals. These formulations are specifically engineered to withstand extreme firing temperatures, rapid cycling, and harsh environmental exposure, making them highly preferred across military and law enforcement applications. Their ability to reduce carbon buildup and minimize wear on moving components enhances firearm reliability and lifecycle performance. For example, Lucas Oil Products, Inc., which offers fully synthetic gun oils designed for heavy-duty tactical and sporting use, is reinforcing the segment’s dominant market position.

Bio-based lubricants are likely to represent the fastest-growing segment, supported by regulatory pressure and sustainability initiatives that reshape purchasing decisions. These lubricants are formulated from renewable resources and are designed to offer low toxicity, biodegradability, and reduced volatile emissions while maintaining comparable performance to synthetic alternatives. Increasing environmental scrutiny from defense procurement bodies and civilian consumers encourages the transition toward renewable-content formulations. For example, Renewable Lubricants Inc., which develops plant-based industrial and firearm-compatible lubricants that meet modern environmental standards.

Form Type Insights

Oils are projected to lead the market, capturing around 45% of the revenue share in 2026, supported by their versatility, penetration efficiency, and ease of controlled application. Liquid oils effectively reach internal firearm components such as bolts, trigger assemblies, and barrel mechanisms, ensuring smooth operation and corrosion protection. Military and law enforcement agencies rely on oil-based lubricants for routine servicing and preventive care because they allow accurate metering and uniform coating. For example, G96 Products Inc., known for its gun treatment oils widely used in professional and sporting environments, is reinforcing the segment’s dominant share.

Aerosol sprays are likely to be the fastest-growing form type, driven by convenience, portability, and rapid application benefits. Spray formulations enable quick coverage of firearm surfaces, making them ideal for tactical field conditions and on-site maintenance at shooting ranges. Their ability to distribute lubricant evenly without direct contact reduces contamination risks and application errors. Growing preference for multi-function spray-based CLP products supports rising adoption across both professional and civilian segments. For example, Clenzoil, which offers aerosol-based cleaner-lubricant-protectant solutions designed for quick field maintenance.

Regional Insights

North America Firearm Lubricants Market Trends

North America is anticipated to be the leading region, accounting for a market share of 43% in 2026, driven by high civilian firearm ownership, steady defense spending, and consistent law enforcement procurement cycles. A well-established shooting culture, encompassing competitive leagues, hunting, and recreational ranges, bolsters routine maintenance activity and recurring product demand. Retail penetration through specialty stores and online marketplaces enhances accessibility to advanced formulations, while institutional contracts provide predictable volume revenue for suppliers. Premium synthetic and multi-function CLP (cleaner-lubricant-protectant) solutions are especially prominent due to their performance advantages under varied operational conditions, including extreme temperatures and high-round count usage.

The region also reflects increasing interest in environmentally compliant and low-VOC formulations as procurement guidelines evolve to incorporate sustainability criteria. Civilian users are more informed about the benefits of biodegradable and eco-friendly products, influencing purchase patterns across retail and online channels. For example, Militec, Inc., has diversified its portfolio to include low-emission and high-performance lubricants preferred by both professional and recreational shooters. Militec’s formulations cater to corrosion resistance and thermal stability, aligning with the sophisticated maintenance requirements of North American firearm users and institutions.

Europe Firearm Lubricants Market Trends

Europe is likely to be a significant market for firearm lubricants in 2026, due to a diverse blend of military requirements, civilian shooting culture, and strict regulatory frameworks. Many European countries maintain robust defense forces that prioritize regular maintenance of small arms, contributing to sustained institutional demand for high-performance lubricants. Civilian participation in hunting, sport shooting, and range activities also supports steady consumption, with users increasingly seeking premium solutions that deliver reliability in varied climates from Nordic cold to Mediterranean humidity. A key regional trend is the harmonization of safety and environmental standards under EU directives, which influences formulation strategies and product approvals.

European consumers demonstrate growing interest in advanced and specialty lubricant formats that combine durability with easy application. Aerosol sprays and multi-function CLP products are gaining favor, especially among recreational shooters and professional armourers who require efficient field and workshop maintenance solutions. Environmental stewardship is also a strong influence, with demand for biodegradable and eco-friendly lubricants rising among conscious end users. For example, ROCOL, which offers high-quality synthetic and low-emission lubricant products tailored for firearm maintenance and industrial applications.

Asia Pacific Firearm Lubricants Market Trends

The Asia Pacific region is likely to be the fastest-growing region in 2026, driven by expanding defense budgets, increasing local firearm production, and heightened focus on internal security modernization. Countries across the region are investing in border protection and tactical readiness, prompting armed forces to adopt higher-performance maintenance products that enhance weapon reliability and longevity in diverse climates, including humid tropical, arid desert, and high-altitude environments. Civilian segments, particularly in India and Southeast Asia, show rising interest in recreational shooting and personal-protection ownership, contributing to growing aftermarket demand.

Alongside institutional adoption, there is an increased preference for multi-function aerosol and synthetic lubricants that combine cleaning, protection, and lubrication in a single application, aligning with the practical needs of users who require efficiency and ease of use. This trend is especially noticeable at shooting ranges and among enthusiast communities that prioritize convenience without compromising performance. For example, Taurus Petroleums Private Limited offers a portfolio of specialty lubricants designed for varied mechanical and environmental conditions. Taurus Petroleums’ product lines demonstrate adaptability to Asia Pacific’s diverse market requirements, combining durability with performance across civilian and professional applications.

Competitive Landscape

The global firearm lubricants market exhibits a moderately fragmented structure, driven by the presence of numerous regional specialists and international brands catering to diverse end users such as military, law enforcement, and civilian shooters. Market participants range from established chemical and specialty lubricant manufacturers to niche companies focused exclusively on firearm maintenance products. This fragmentation reflects variations in product portfolios, formulation technologies, distribution channels, and regional regulatory compliance. Collaborations with shooting associations and participation in trade events bolster brand visibility.

With key leaders including Lucas Oil Products, Inc., Ballistol, and Clenzoil, the competitive landscape encompasses companies with strong brand recognition and extensive reach. These players serve institutional contracts as well as aftermarket retail demand, balancing performance, environmental compliance, and price positioning to capture share. Strategic partnerships with firearm manufacturers, range operators, and defense procurement agencies enhance market access and credibility. Investment in research and development enables differentiated formulations, including synthetic, bio-based, and low-VOC alternatives that align with evolving regulatory and end-user expectations.

Key Industry Developments:

- In February 2026, CICO SLT GmbH unveiled its new CICO® GunCare firearm maintenance line, including the CICO® GUNCLEANER GC 55, CICO® GUNSPRAY GS 77, and CICO® GUNLUBE GL 99 at IWA OutdoorClassics 2026 in Nuremberg, Germany, highlighting precision cleaning, protection, and long-lasting reliability for both short and long guns. These products are engineered to meet the needs of professional users and enthusiasts by enhancing operational safety and protection against wear and corrosion.

- In February 2026, the Liqui Moly GUNTEC range of firearm care products, including GUNTEC Barrel and Gun Cleaner and accompanying lubrication solutions, was highlighted as part of an expanded lubrication portfolio aimed at safe and effective firearm maintenance for hunters, sport shooters, and security professionals. The range provides high-quality cleaning and lubrication that clings to common firearm materials such as steel, wood, and polymer, ensuring thorough residue removal and protection during routine servicing.

Companies Covered in Firearm Lubricants Market

- Lucas Oil Products, Inc.

- ROCOL

- L&R Manufacturing

- Amsoil Inc.

- MPT Industries

- G96 Products Inc.

- Radco Industries, Inc.

- Pacific Specialty Oils

- Ballistol

- Renewable Lubricants Inc.

- Militec, Inc.

- Pro-Shot Products Inc.

- Liberty Gun Lubricants

- Clenzoil

- Taurus Petroleums Private Limited

Frequently Asked Questions

The global firearm lubricants market is projected to reach US$3.4 billion in 2026.

Rising demand for reliable firearm maintenance in military, law enforcement, and recreational shooting activities drives the firearm lubricants market.

The firearm lubricants market is expected to grow at a CAGR of 4.4% from 2026 to 2033.

Growing demand for eco-friendly, bio-based firearm lubricants and the expansion of shooting sports and firearm accessories retail channels create key opportunities in the firearm lubricants market.

Lucas Oil Products, Inc., ROCOL, L&R Manufacturing, Amsoil Inc, MPT Industries, G96 Products Inc, and Radco Industries, Inc. are the leading players.