- Clothing, Footwear, & Accessories

- Firefighter Turnout Gear Market

Firefighter Turnout Gear Market Size, Share, and Growth Forecast, 2026 – 2033

Firefighter Turnout Gear Market by Product Type (Helmets, Jackets, Pants, Gloves, Boots, Hoods), Material (Nomex, Kevlar, PBI, Carbon Fiber, Leather), End-User (Municipal Fire Departments, Industrial Fire Departments, Military Fire Departments, Wildland Firefighters), and Regional Analysis for 2026-2033

Firefighter Turnout Gear Market Share and Trends Analysis

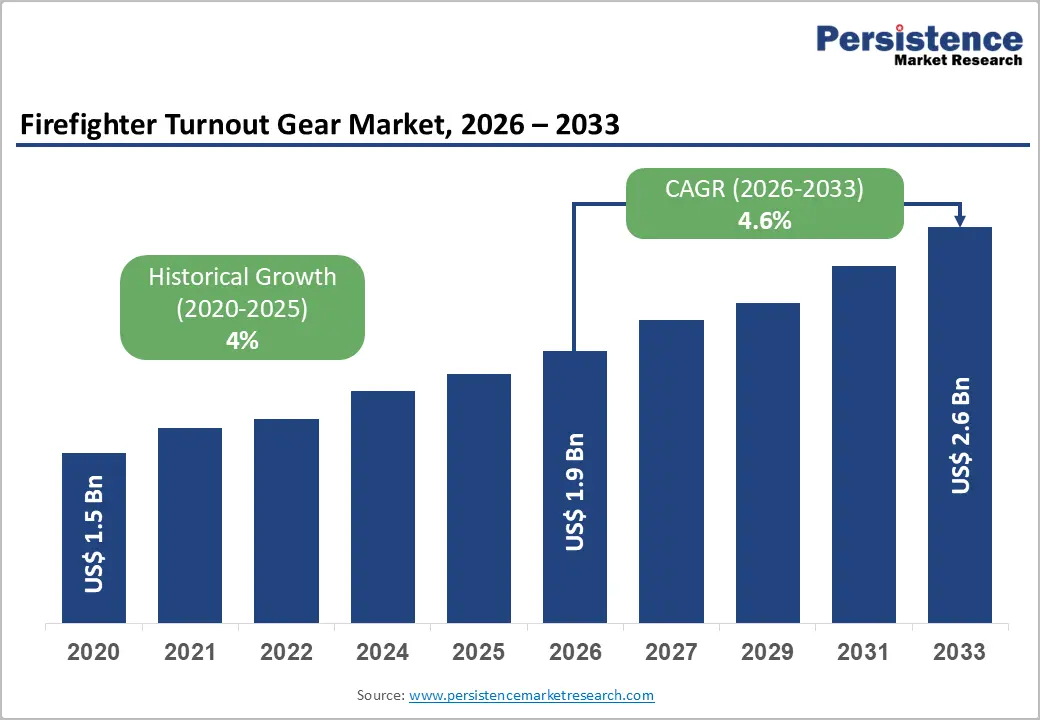

The global firefighter turnout gear market size is likely to be valued at US$ 1.9 billion in 2026, and is projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 4.6% during the forecast period 2026−2033. Market expansion in densely populated and industrial regions is fueling demand for protective equipment as fire incidents rise. Advanced heat-resistant fabrics and integrated wearable systems enhance operational efficiency and safety, driving procurement across fire departments.

Regulatory mandates and occupational safety standards enforce compliance, prompting upgrades or replacements of aging gear. Growing awareness of firefighter health risks motivates the adoption of preventive measures through improved protective ensembles. Expansion of municipal and industrial fire services in emerging economies supports scalable market penetration. Integration of digital tracking and monitoring systems adds operational value, influencing purchasing strategies and long-term investment decisions.

Key Industry Highlights

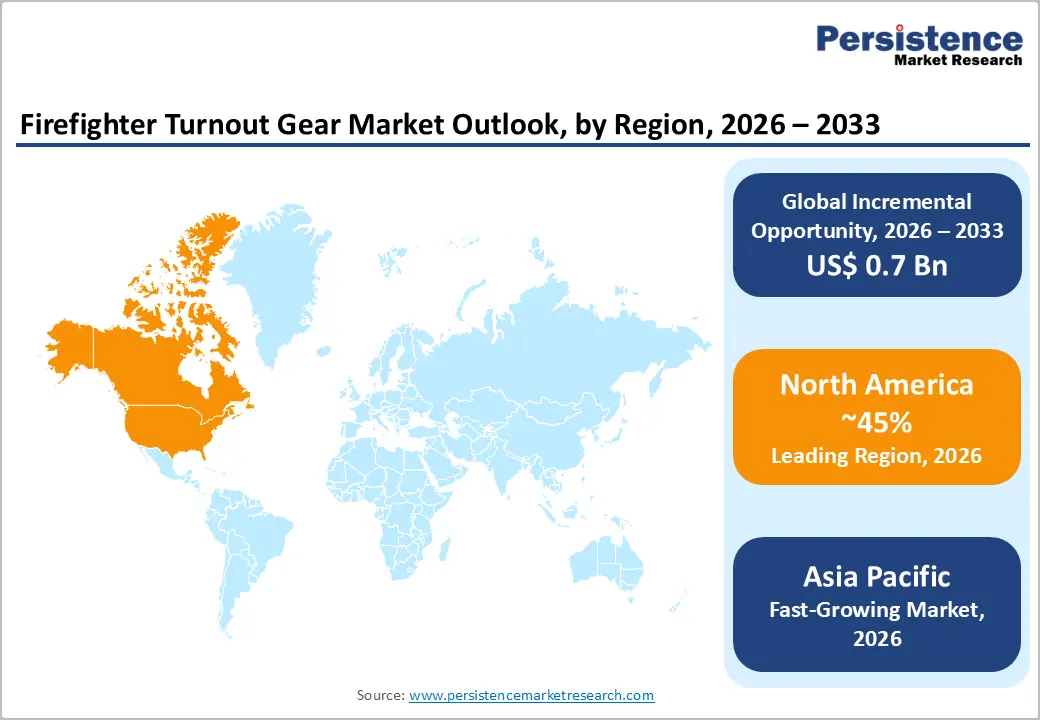

- Dominant Region: North America is projected to secure 45% of the market in 2026, supported by advanced safety regulations, high industrial activity, and mature municipal infrastructure.

- Fastest-growing Market: The Asia Pacific market is expected to grow the fastest from 2026 to 2033, driven by rapid industrial expansion and modernization of fire services.

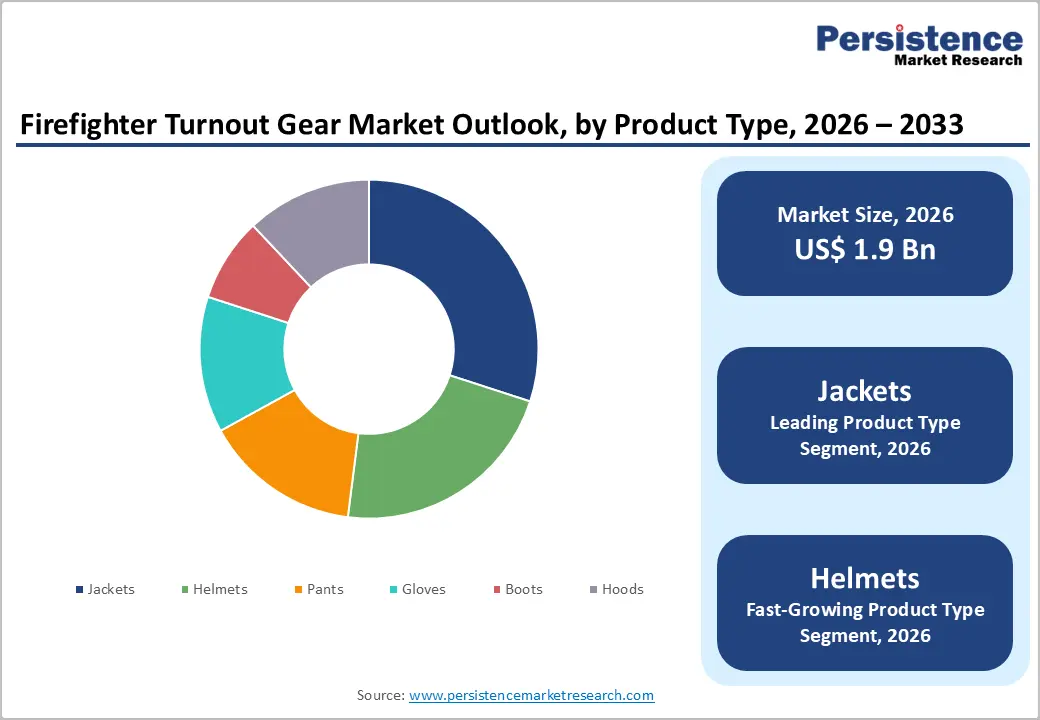

- Leading Product Type: Jackets are expected to account for about 30% of revenue in 2026, driven by their superior heat resistance, ergonomic design, and compliance with safety standards.

- Fastest-growing Product Type: Helmets are projected to grow the fastest from 2026 to 2033, owing to lightweight composites, integrated sensors and communication systems, and safety mandates.

- October 2025: TwiceMe Technology partnered with SCHUBERTH to integrate digital safety features into F300, F220, and F130 firefighting helmets launched in Germany.

| Key Insights | Details |

|---|---|

| Firefighter Turnout Gear Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Protective Gear

Innovation in protective gear is transforming firefighter operations, driving demand for modern turnout equipment. Advanced materials such as high-performance heat-resistant fabrics improve thermal insulation and reduce exposure to extreme temperatures, lowering injury risks and extending the service life of gear. Integration of wearable sensors and real-time monitoring systems allows fire departments to track vital signs, environmental hazards, and exposure levels during operations, enhancing situational awareness and decision-making. These enhancements increase confidence in workforce safety, prompting fire departments to prioritize procurement of upgraded turnout gear.

The rising complexity of fire scenarios and urban infrastructure challenges requires equipment that supports agility and resilience. Lightweight, ergonomic designs reduce physical strain on firefighters, improving mobility during prolonged operations. Modular and multifunctional gear systems allow customization for specific mission requirements, improving operational efficiency. Integration with communication and data platforms enables coordinated response in high-risk environments. Municipal and industrial fire services are increasingly investing in these solutions to meet regulatory compliance and occupational safety standards, ensuring teams are prepared for evolving hazards.

High Procurement and Maintenance Costs

High acquisition and maintenance expenditures exert downward pressure on departmental budgets, as outfitting each firefighter with certified protective gear represents a substantial capital commitment. A complete turnout gear ensemble, including coat, pants, helmet, gloves and boots, typically costs US$3,000–US$ 5,000 per firefighter, illustrating the significant initial investment required for compliant protective equipment. Specialized materials such as aramid and moisture barriers, multi-layer thermal liners and integrated safety features increase manufacturing complexity and unit price. As departments need to equip multiple personnel, total procurement costs scale rapidly, often competing with other operational expenditures such as apparatus, training, and emergency medical equipment, placing strain on constrained budgets and limiting the speed at which modern, technologically advanced ensembles can be adopted.

Recurring maintenance and replacement expenses further intensify financial pressure as protective gear must be routinely inspected, cleaned and repaired to meet safety standards and ensure performance longevity. Regular decontamination and professional servicing are necessary to prevent degradation from heat, chemicals and contaminants encountered during operations, and these processes contribute to predictable but non-discretionary costs over the service life of the gear. Wear-related component replacements and end-of-service-life retirements require periodic reinvestment in new sets, reducing flexibility in capital planning and extending the time to return on investment.

Integration of Smart Wearable Systems

Smart wearable systems represent a transformative opportunity in the firefighter turnout gear market as agencies seek real-time insights that reshape operational decision-making and risk management. Fire departments operate in environments where situational awareness and rapid response determine life and asset preservation outcomes. Wearable sensors embedded in turnout gear deliver continuous monitoring of vital signs, core temperature, movement patterns and exposure to hazardous elements. These capabilities elevate incident command visibility and support preemptive interventions that reduce injury and fatality rates. Data streams generated from wearables feed into centralized platforms that enable trend analysis, predictive alerts and resource allocation adjustments. Market report data highlights that procurement strategies now prioritize solutions that deliver quantifiable performance metrics and align with broader digital transformation initiatives within emergency services. Investment in smart wearables strengthens accountability frameworks and supports compliance reporting against evolving safety standards.

Enterprises responsible for fire protection services are allocating capital towards technologies that extend beyond baseline protective performance. Smart wearable systems drive value by optimizing operational workflows and enhancing interoperability with dispatch, asset management and health surveillance systems. Firefighter wellness programs benefit from longitudinal health data collected in the field, which informs return-to-duty decisions and long-term care planning. Procurement committees evaluate wearable-enabled gear as a mechanism to improve training outcomes, reduce downtime and lower total cost of ownership through extended service life and reduced incident related liabilities. Insights from a recent market report indicate that adoption rates correlate with organizational emphasis on resilience and workforce sustainability.

Category-wise Analysis

Product Type Insights

Jackets are poised to lead with a forecasted 30% of the firefighter turnout gear market revenue share in 2026, owing to comprehensive thermal protection, ergonomic design, and adaptability across fire scenarios. Core attributes include high heat resistance, moisture barriers, and integrated reflective elements that improve visibility. Municipal and industrial departments prioritize jackets for multi-hazard operations, establishing consistent procurement cycles. Regulatory frameworks require compliance with thermal protection standards, positioning jackets as essential equipment in standard firefighter ensembles. Manufacturer innovation in modular designs and wearable technology integration enhances functional utility and adoption rates. Departments favor jackets for lifecycle durability and maintenance predictability, influencing capital allocation.

Helmets are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by advancements in lightweight composites, sensor integration, and communication systems. Adoption is driven by safety mandates for head protection and the growing need for situational awareness tools. Technological enhancements include thermal imaging mounts, communication headsets, and biometric sensors. Industrial and military fire departments prioritize helmets to mitigate high-risk exposures, expanding procurement. Market penetration is supported by replacement cycles and retrofitting programs, ensuring consistent demand growth.

Material Insights

Nomex are likely to be the leading segment with a projected 35% market share in 2026, due to its high thermal stability, flame resistance, and proven durability. Departments prioritize Nomex for certified compliance with international standards, ensuring uniform adoption. The material supports integration with wearable technology without compromising protective properties. Retail and institutional penetration is widespread, facilitating predictable procurement and lifecycle management. Acceptance is reinforced by historical performance data and operational reliability, creating sustained demand. Cross-departmental adoption in municipal, industrial, and military units reinforces market dominance.

Polybenzimidazole (PBI) is expected to grow the fastest between 2026 and 2033, driven by its superior heat resistance, mechanical strength, and compatibility with sensor integration. Adoption is expanding across high-risk industrial fire departments and military applications. Technological acceptance is supported by pilot programs validating operational performance. Evolving regulations promoting advanced protective standards drive procurement. Increased digital commerce access for specialized materials enhances availability, reducing adoption barriers. PBI offers long-term value through lifecycle durability, safety performance, and modular design flexibility, ensuring continued growth acceleration.

End-User Insights

The municipal fire departments are slated to hold a dominant position, with an anticipated 40% of the firefighter turnout gear market share in 2026, driven by structured regulatory compliance, budget allocation, and high-volume deployment requirements. Municipal units prioritize standardized gear, ensuring consistency across operations and districts. Adoption is influenced by procurement guidelines established by local and national fire safety authorities. Training programs reinforce gear usage, supporting compliance and operational efficiency. Predictable procurement cycles facilitate strategic partnerships with manufacturers and long-term supply agreements.

Industrial fire departments are forecast to be the fastest-growing end-user segment between 2026 and 2033, driven by rapid industrial expansion, heightened risk protection requirements, and regulatory pressure. Industrial entities prioritize customized ensembles for chemical, electrical, and high-heat exposure scenarios. Investments in workforce safety programs and technology-enabled monitoring enhance adoption. Collaborative frameworks with manufacturers ensure tailored solutions that support scalable deployment. Digital tracking and compliance reporting reinforce operational efficiency, accelerating penetration into industrial departments.

Regional Insights

North America Firefighter Turnout Gear Market Trends

North America is expected to dominate with an estimated 45% of the firefighter turnout gear market share in 2026, reflecting advanced safety regulations, high industrial activity, and mature municipal infrastructure. Government agencies mandate compliance with National Fire Protection Association (NFPA) standards, ensuring high adoption of technologically advanced gear. Fire departments implement protocols for routine inspection and maintenance, which extend equipment lifecycle and improve safety outcomes. Federal and state funding programs support modernization and replacement initiatives, reinforcing predictable procurement cycles. The competitive landscape is defined by established manufacturers offering integrated services, including training, maintenance, and digital solutions. Collaborative programs between departments and manufacturers accelerate the adoption of innovative materials and designs.

Investment flows target research & development (R&D), manufacturing facilities, and integration of advanced technology into turnout gear. Urbanization in the United States and Canadian cities increases demand for high-capacity fire response units capable of handling complex emergencies. Regulatory oversight ensures that fire departments maintain lifecycle compliance and adhere to occupational safety standards, fostering consistent replacement and upgrade cycles. Strategic alliances with digital technology providers enable deployment of smart wearable systems that monitor firefighter health and environmental exposure in real time. These investments improve operational efficiency, reduce risk, and support long-term sustainability in emergency response services.

Europe Firefighter Turnout Gear Market Trends

Europe is foreseen to occupy a prominent position in the market for firefighter turnout gear through 2033, on the back of harmonized safety directives and focus on sustainable materials. Germany and the United Kingdom lead demand through robust industrial operations and well-developed municipal fire services. Enhanced preparedness for wildfires and industrial incidents drives adoption of advanced turnout gear with superior thermal protection, chemical resistance, and integration with monitoring systems. Funding programs supported by the European Union encourage modernization of fire response equipment, while procurement processes prioritize compliance with unified safety standards. Collaboration among fire departments, research institutions, and equipment providers accelerates innovation in protective ensembles. Emphasis on eco-friendly materials and performance certifications ensures high-quality solutions that align with environmental initiatives and occupational safety requirements, reinforcing continued market relevance.

Investment opportunities focus on cross-border partnerships and development of advanced fabrics and wearable technologies that enhance operational safety and efficiency. Research and development initiatives target next-generation heat- and chemical-resistant materials, lightweight composites, and ergonomic designs that reduce fatigue during extended operations. Integration of smart wearable systems enables real-time monitoring of firefighter vital signs, core temperature, location tracking, and exposure to hazardous environments, supporting rapid decision-making and incident management. Firefighter training programs incorporate simulation-based learning and familiarization with advanced gear, ensuring effective adoption and optimized field performance. Departments increasingly prioritize modular and upgradeable ensembles that allow incremental integration of new technologies, reducing total lifecycle costs.

Asia Pacific Firefighter Turnout Gear Market Trends

Asia Pacific is forecast to be the fastest-growing market for firefighter turnout gear between 2026 and 2033, driven by rapid urbanization, industrial expansion, and the modernization of emergency response infrastructure. Government initiatives across the regional market emphasize compliance with international safety standards, fostering structured procurement frameworks for fire departments. High-risk industrial zones in China, India, and Southeast Asia drive elevated operational demand, requiring gear with advanced heat resistance, chemical protection, and integration with digital monitoring systems. Expanding municipal and industrial fire services requires prioritizing equipment capable of sustaining intensive operational cycles to support long-term adoption. Urban population growth intensifies the need for high-capacity fire response units, while industrial diversification introduces varied hazard profiles, further motivating investment in technologically advanced turnout gear.

Investment in local manufacturing facilities, material development, and technology adaptation reduces cost barriers for regional departments, enabling broader access to premium protective solutions. Collaborative partnerships between local authorities and global manufacturers facilitate knowledge transfer, ensuring timely introduction of cutting-edge materials and smart wearable systems. Workforce training programs strengthen operational proficiency, familiarizing personnel with integrated monitoring and safety technologies, and promoting the adoption of advanced protective ensembles. Combined with digital supply chains and growing awareness of firefighter health risks, these factors drive a sustained growth trajectory, positioning Asia Pacific as a high-potential market with both short-term demand and long-term strategic opportunities.

Competitive Landscape

The global firefighter turnout gear market structure exhibits moderate concentration, with leading players holding substantial share through established brands, technological innovation, and proven operational performance. Key participants include Honeywell, Rosenbauer, DuPont, MSA (Mine Safety Appliances), Dräger, TEXPORT, and ITURRI Group. These companies leverage expertise in advanced heat- and chemical-resistant materials, ergonomic designs, and integration of smart wearable systems to maintain competitive advantage. While global players dominate large-scale industrial and municipal procurement, regional suppliers cater to niche requirements, providing tailored solutions and specialized protective ensembles. Investment in R&D and pilot programs ensures continual enhancement of gear performance, while adherence to international standards and certifications reinforces reliability, safety, and customer confidence across diverse operational environments.

Competitive positioning emphasizes compliance with NFPA standards, material quality, and comprehensive service networks that support deployment, maintenance, and training initiatives. Manufacturers focus on modular gear design, lifecycle durability, and technology-enabled monitoring systems that improve situational awareness and operational efficiency. Strategic alliances with technology providers and local distributors enable effective market penetration in emerging industrial and urban areas. Customization capabilities, rapid innovation cycles, and strong brand reputation allow top players to retain leadership while smaller regional manufacturers contribute to market diversity, fostering incremental innovation and addressing specific operational requirements.

Key Industry Developments

- In January 2026, LION announced its reentry into the EN-469 compliant technical garments market with a new lineup of high-performance turnout gear models tailored to international safety standards and global firefighter needs.

- In December 2025, San Francisco Fire Department became the largest U.S. department to fully transition to PFAS-free turnout gear for all 1,100 frontline firefighters, funded by a US$ 2.35 million FEMA grant and city matching, using Fire-Dex AeroFlex with Milliken's Assure moisture barrier (UL-certified, NFPA-compliant).

- In November 2025, Jotun introduced its Jotachar 1709 XT fire-protection coating, expanding its passive fire protection range with a product engineered for extreme environments and optimized for rigorous UL-1709 fire safety standards in energy and industrial applications.

Companies Covered in Firefighter Turnout Gear Market

- Honeywell

- Rosenbauer

- DuPont

- MSA (Mine Safety Appliances)

- Dräger

- TEXPORT

- ITURRI Group

- Taiwan KK Corporation

- Lakeland Fire

- Sioen NV

- 3M

Frequently Asked Questions

The global firefighter turnout gear market is projected to reach US$ 1.9 billion in 2026.

Market growth is driven by rising industrialization, urbanization, stringent safety regulations, and increasing investment in advanced protective and smart gear.

The market is poised to witness a CAGR of 4.6% from 2026 to 2033.

Key market opportunities include adoption of smart wearable systems, advanced heat‑ and chemical‑resistant materials, and expansion in emerging urban and industrial fire services.

Some of the key market players include Honeywell, Rosenbauer, DuPont, MSA, Dräger, TEXPORT, and ITURRI Group