- Automotive Components & Materials

- Europe Automotive Aluminum Extruded Parts Market

Europe Automotive Aluminum Extruded Parts Market Size, Share, Trends, Growth, Regional Forecasts 2026 to 2033

Europe Automotive Aluminum Extruded Parts Market by Product(Sub-structures, Front Side Rails, Sub-frames), Material(6000 series, 7000 series, 5000 series), Vehicle (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles), and Regional Analysis 2026 - 2033

Europe Automotive Aluminum Extruded Parts Market Share and Trends Analysis

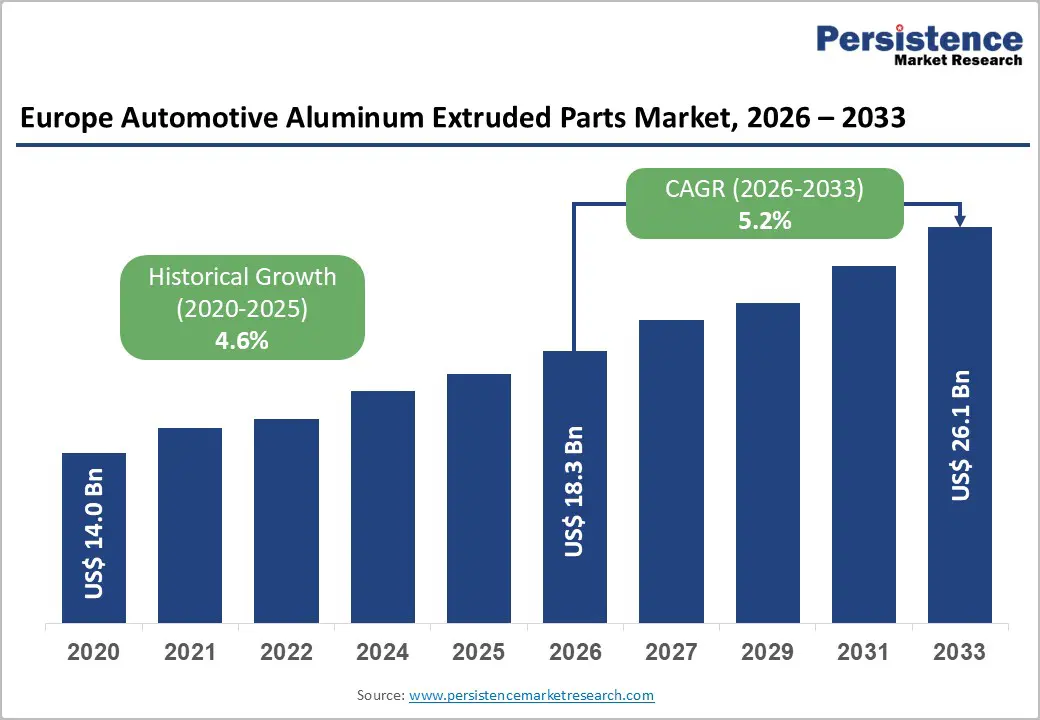

Europe automotive aluminum extruded parts market size is likely to be valued at US$18.3 Billion in 2026 and is projected to reach US$26.2 Billion by 2033, growing at a CAGR of 5.23% between 2026 and 2033. The global automotive aluminum extruded parts market holds US$68.5 Billion in 2026 and is expanding at a 6.1% CAGR, reflecting robust demand across passenger vehicles, commercial vehicles, and EV platforms.

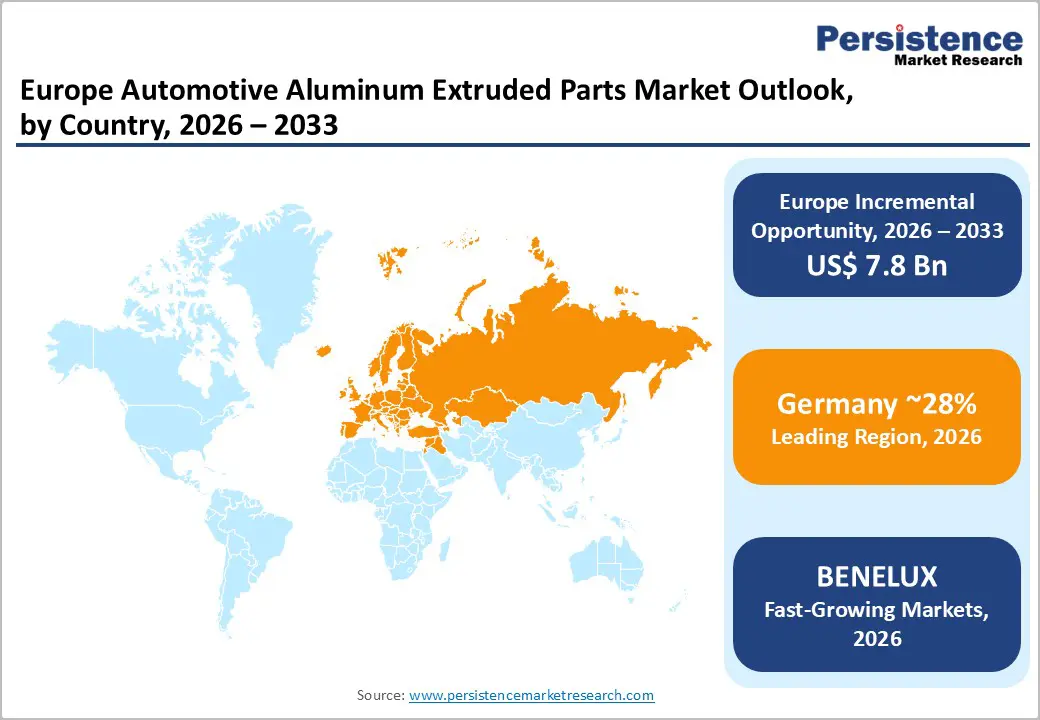

Europe’s growth is driven by stringent EU emissions reduction targets mandating a 55% CO2 reduction by 2030, accelerating vehicle electrification, with EV adoption reaching 40% year-on-year, and lightweight architecture optimization, where aluminum extrusions enable 20-30% weight reduction versus steel. Germany leads with 28% regional share, while France, UK, and Benelux present substantial growth opportunities through regulatory harmonization and sustainable manufacturing initiatives.

Key Industry Highlights:

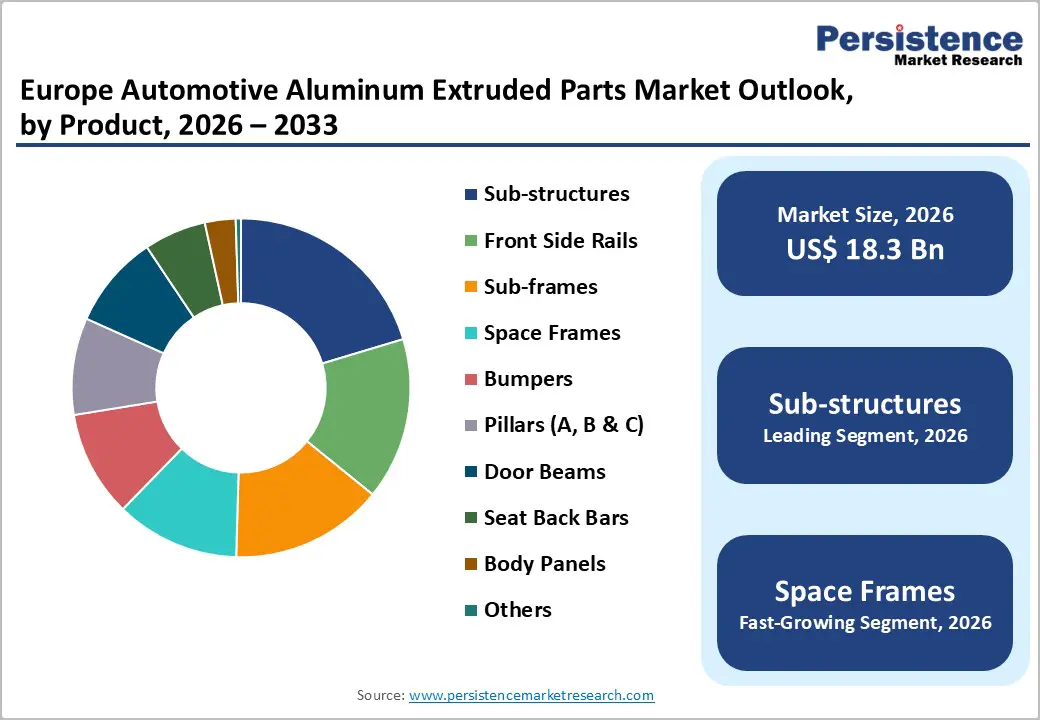

- Sub-Structures Lead: Sub-structures dominate with 21% market share, while space frames grow fastest at 6.6% CAGR, driven by EV platform development and modular architectures enabling rapid variant production.

- Material Trends: 6000 series alloys hold 46% share, while 7000 series expand at 6.8% CAGR, meeting premium EV and advanced structural performance demands for maximum weight optimization.

- Vehicle Segment Dynamics: Passenger cars account for 75% share, with EVs growing fastest at 10.6% CAGR, supported by 40% annual EV adoption and UK battery enclosure opportunities worth £870 million.

- Regional Insights: Germany leads with 28% share; France and UK gain from aerospace and EV infrastructure, while Benelux expands at 5.4% CAGR.

- Competitive Landscape: Constellium, Hydro, and Novelis leverage hydrogen-powered production, advanced alloys, and battery enclosure innovations to demonstrate technological leadership for next-generation EV platforms.

| Key Insights | Details |

|---|---|

| Europe Automotive Aluminum Extruded Parts Market Size (2026E) | US$ 18.3 billion |

| Market Value Forecast (2033F) | US$ 26.2 billion |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics Analysis

Drivers - European Union Emissions Regulation Compliance and CO2 Reduction Mandates

European Union environmental regulations are the strongest growth catalyst for automotive aluminum extrusion, with binding targets mandating a 55% reduction in CO2 emissions by 2030 versus 1990 levels, forcing OEMs to prioritize vehicle lightweighting. The EU’s 2050 climate neutrality goal requires nearly 80% of the vehicle fleet to be fossil fuel free, accelerating electrification and lightweighting investments across all platforms. Regulations quantify benefits, indicating that replacing one kilogram of steel with aluminum reduces lifecycle emissions by about 18 kilograms, justifying cost premiums. European OEMs, including Volkswagen Group, BMW Group, Daimler, and Stellantis are embedding aluminum extrusions into next generation architectures to meet compliance without sacrificing safety. Interim targets for 2025, 2028, and 2030 compress development cycles, accelerating adoption. EV subsidies exceeding €10,000 further boost aluminum-intensive battery enclosures and structures across European markets and value chains, supporting long term decarbonization.

Accelerating Electric Vehicle Production and Battery Management Requirements

Vehicle electrification is transforming automotive aluminum extrusion demand patterns, with European EV production exceeding four million units in 2024 and projected to expand toward eight to ten million units by 2030, creating sustained structural demand growth across battery enclosures, thermal management systems, and lightweight structural components. Electric vehicles require highly optimized lightweight architectures, with engineering analysis indicating that reducing vehicle mass by 100 kilograms improves driving range by approximately seven to ten percent, strengthening the economic case for aluminum extrusion adoption. Battery enclosures represent the most significant EV application, with the UK market alone estimated at £870 million, driven by crash protection, thermal conductivity, and structural integrity requirements.

Advanced aluminum alloys, including specialized 6061 and 7075 grades, deliver superior thermal performance compared to steel, enabling effective battery cooling. Premium EVs such as Mercedes-Benz EQE, BMW i7, and Porsche Taycan increasingly rely on extrusion-intensive architectures. Public procurement programs accelerating commercial vehicle electrification further reinforce long-term aluminum extrusion demand across European platforms.

Restraints - Raw Material Cost Volatility and Recycled Aluminum Supply Chain Complexity

European automotive aluminum extrusion manufacturing faces vulnerabilities from disruptions to primary and recycled feedstocks, energy cost volatility, and logistics constraints that limit flexibility during demand surges and complicate cost optimization. European aluminum output is concentrated among a few smelters, with Nordic hydropower-based producers supplying low-carbon metal at premium prices for sustainability-driven applications. Recycled aluminum sourcing depends on mature scrap collection, sorting, and reprocessing infrastructure, creating regional cost disparities. Carbon intensity differences between European primary aluminum at 9.1 tonnes CO2e per tonne and Asian coal-based production at 22.4 tonnes CO2e per tonne pressure competitiveness despite sustainability benefits, overall margins.

Regulatory Compliance Complexity and Automotive Industry Qualification Requirements

European automotive aluminum extrusion development requires compliance with multiple regulatory frameworks, including IATF 16949 quality standards, EU automotive material specifications under ECE regulations, crash safety testing, and environmental compliance, creating high entry barriers and limiting flexibility. EU conflict mineral regulations mandate responsible sourcing documentation, adding administrative and verification costs across supply chains. Product carbon footprint declarations and mandatory lifecycle assessments intensify competition, favoring suppliers with proven sustainability credentials. Qualification of crash-critical components requires extensive impact simulations, energy-absorption analysis, and deformation validation beyond standard testing, which can extend development timelines by 12 to 24 months compared to typical design-to-production cycles.

Opportunity - Premium EV Platform Development and Modular Architecture Standardization

European automotive OEMs are establishing proprietary EV platforms featuring modular aluminum extrusion-based architectures that support rapid variant development across vehicle segments and market categories, creating opportunities for specialized extrusion suppliers to develop customized component solutions aligned with platform standardization initiatives. Cell-to-pack battery architecture development is eliminating traditional module housings, requiring sophisticated aluminum enclosure designs optimizing thermal management, crash protection, and manufacturing efficiency simultaneously.

Multi-material integration strategies combining aluminum extrusions with complementary materials (steel, composites, magnesium) are enabling engineers to achieve unprecedented weight reduction while maintaining structural integrity, creating demand for extrusion suppliers capable of supporting integrated solutions provision. German automotive manufacturers, including Audi, BMW, and Mercedes-Benz, are leading premium EV platform development, with an estimated battery enclosure market opportunity for the United Kingdom alone projected at £870 million through 2035, suggesting comparable or larger opportunities across broader European markets.

Low-Carbon Aluminum Production and Sustainability-Focused Supply Chain Development

European government initiatives supporting the adoption of green hydrogen in aluminum production and the development of closed-loop recycling infrastructure are creating opportunities for extrusion suppliers developing low-carbon production capabilities aligned with corporate sustainability commitments and regulatory decarbonization mandates. Constellium's successful industrial-scale hydrogen casting milestone in December 2024 demonstrates the viability of hydrogen-powered aluminum production at a commercial scale, with an ambitious roadmap toward decarbonized manufacturing operations. European automakers' willingness to pay a premium for low-carbon aluminum (EUR 10-25 per tonne) indicates sustained market segments where sustainability positioning justifies material cost premiums. Government subsidies for hydrogen infrastructure development, renewable-powered smelter expansion, and recycling facility establishment are creating a favorable policy environment for domestic production capacity development. Industry collaboration initiatives, including the HyInHeat project partnerships exploring hydrogen substitution in aluminum transformation processes, are accelerating technology commercialization and cost reduction pathways supporting scaled implementation.

Category-wise Analysis

Product Type Insights

Sub-structures and chassis components represent the dominant automotive aluminum extrusion application in Europe, commanding 21% of regional market share, driven by critical structural importance, significant weight reduction opportunities, and an established supplier ecosystem supporting high-volume production across diverse vehicle architectures. European automotive manufacturers, including Audi, BMW, and Mercedes-Benz, have systematically integrated aluminum sub-structure components into premium vehicle platforms, with engineering optimization enabling 20-30% weight reduction compared to conventional steel chassis. Longitudinal beams, cross-members, and sub-frame structures leverage aluminum extrusions' superior strength-to-weight characteristics, enabling comprehensive platform lightweighting while maintaining crashworthiness standards mandated by European New Car Assessment Programme (Euro NCAP) protocols.

Space frame applications represent a growing aluminum extrusion category in Europe, expanding at a 6.6% CAGR, driven by EV platform development, autonomous readiness, and premium vehicle growth that emphasizes design flexibility and scalable manufacturing. EV architectures increasingly adopt modular space frames optimizing battery integration, weight distribution, and structural efficiency. Joining methods including friction stir welding enable seamless extrusion integration within complex structures.

Material Type Insights

6000-series aluminum alloys (aluminum-magnesium-silicon) account for 46% of the European automotive extrusion market share, the preferred specification for the majority of automotive applications due to excellent machinability, superior weldability, and a well-established supplier ecosystem supporting consistent high-volume production. 6061 and 6063 alloys dominate European automotive extrusion applications, delivering an optimal balance of mechanical properties, cost-effectiveness, and manufacturing reliability, enabling consistent quality across distributed supplier operations. European quality standards and automotive industry qualification protocols have established 6000-series alloys as the default specifications for non-critical structural applications, supporting supply chain maturity and competitive pricing.

The 7000-series aluminum alloys are the fastest-growing material category in Europe, expanding at a 6.8% CAGR, driven by lightweight architectures, autonomous platform requirements, and premium vehicle demand for maximum structural performance at minimal weight. European OEMs partner with aluminum suppliers on tailored 7000-series alloys, where a 35-40% weight reduction versus steel justifies premium costs in EV and performance platform applications.

Vehicle Type Insights

Passenger cars represent the dominant automotive aluminum extrusion application in Europe, commanding 75% of regional market volume, driven by the installed base, established OEM-supplier relationships, and sophisticated lightweighting requirements across the compact, midsize, luxury, and SUV segments. Premium vehicle manufacturers, including Mercedes-Benz, BMW, and Audi, have made fundamental commitments to aluminum-intensive lightweight architectures, with multi-material design strategies combining aluminum extrusions with complementary materials optimized for specific functional requirements.

Electric vehicles are the fastest-growing vehicle category in Europe, expanding at 10.6% CAGR, supported by strong incentives, consumer shifts toward zero-emission mobility, and stringent regulations. European EV platforms increasingly integrate aluminum extrusions for battery enclosures, thermal management, and structural optimization. Aluminum’s high thermal conductivity is critical for managing heat during fast-charging cycles in modern electric vehicle architectures.

Regional Market Insights

Germany Automotive Aluminum Extruded Parts Market Trends

Germany holds market dominance within Europe, commanding a 28% share of regional automotive aluminum extrusion consumption, driven by premium automotive manufacturing concentration, a robust supply chain ecosystem, and strategic EV production supporting next-generation vehicle development. German OEMs, including Volkswagen, BMW, Daimler, and Porsche, systematically integrate aluminum extrusions across vehicle platforms, leveraging engineering expertise for advanced lightweight architectures.

Government support for EV manufacturing, domestic battery gigafactories, and automotive semiconductor initiatives attracts capital investment, strengthening the regional ecosystem. German suppliers, including Constellium, Hydro Extrusions, and regional specialists, maintain leadership through strong customer relationships, comprehensive portfolios, and advanced manufacturing capabilities. EU emissions standards, German sustainability programs, and OEM lightweighting mandates accelerate adoption. Investment in lightweight materials and advanced extrusion technologies by multinational and regional suppliers sustains innovation leadership across Germany and the broader European market.

U.K. Automotive Aluminum Extruded Parts Market Share

The U.K. holds a considerable market share of 13% within Europe’s automotive aluminum extrusion market, expanding at a CAGR of 5.3%, supported by its aerospace industry presence, Airbus operations, and automotive manufacturing clusters across regional centers. The U.K. automotive sector, while undergoing restructuring, maintains a strong aerospace footprint, producing over 1,000 commercial aircraft annually and sustaining aluminum extrusion demand. The U.K. EV battery housing market represents a £870 million opportunity through 2035, positioning the country as a significant growth engine driving the adoption of comprehensive aluminum extrusion across vehicle development cycles. Government commitments to renewable energy infrastructure and EV adoption provide a favorable policy environment, supporting automotive aluminum extrusion demand. Established aerospace manufacturing further underpins advanced extrusion technology development and specialized supplier capabilities throughout the U.K.

Benelux Automotive Aluminum Extruded Parts Market Share

The Benelux countries, Belgium, the Netherlands, and Luxembourg, exhibit strong growth momentum in the automotive aluminum extrusion market, expanding at a CAGR of 5.4%, driven by a concentration of advanced automotive supplier infrastructure, strategic logistics hub positioning, and proximity to major European automotive manufacturing centers.

Belgium and the Netherlands host significant automotive component manufacturing and aluminum processing operations, supporting both regional and broader European supply chains. Luxembourg contributes through specialized materials and financial services supporting automotive investments. Government sustainability initiatives, including low-carbon manufacturing programs, alongside EU regulatory harmonization, create an aligned policy framework that fosters consistent adoption of aluminum extrusion across the region. The combination of robust supplier networks, strategic location, and supportive regulatory environments positions the Benelux countries as key growth drivers within Europe’s automotive aluminum extrusion market.

Competitive Landscape

Europe automotive aluminum extrusion market is moderately consolidated, with multinationals such as Constellium, Hydro, and Novelis dominating alongside regional specialists serving specific markets, alloys, and vehicle segments. High entry barriers, including qualification protocols, long development cycles, capital intensity, and regulatory compliance, limit competition. Regional specialists compete through market expertise, customer service, and manufacturing flexibility for German, French, and UK OEMs.

Strategic Developments:

- In December 2024, Constellium completed industrial-scale hydrogen casting at its C-TEC facility, producing a 12-tonne aluminum slab using hydrogen fuel at Neuf-Brisach, demonstrating commercial-scale decarbonized production without quality loss and strengthening sustainability-focused supply chain positioning.

- In June 2023, Hydro Extrusions successfully tested green hydrogen for aluminum recycling at its Navarra, Spain facility, advancing renewable energy-powered manufacturing, supporting EU sustainability goals, and positioning the supplier for low-carbon automotive supply chain integration.

Companies Covered in Europe Automotive Aluminum Extruded Parts Market

- Constellium

- Hydro Extrusions

- Novelis (Aleris operations)

- Aluswiss

- Pechiney

- Aleona

- Hydro Extrusions Europe

- Grangemouth Extrusions

- Trimet

- Constellium Neuf-Brisach

- Comalco

- Hydro Tasman

- Alcan (Rio Tinto subsidiary)

- SWM (Stahl- und Walzwerk)

Frequently Asked Questions

Europe Automotive Aluminum Extruded Parts Market was valued at US$18.3 billion in 2026 and is projected to reach US$26.2 billion by 2033.

Market growth is driven by EU CO2 reduction targets, vehicle electrification with EV production reaching 4 million units in 2024 and projected to 8-10 million by 2030, and advanced manufacturing enabling complex extrusion geometries, precision tolerances, and integrated designs for innovative EV platforms.

The market is projected to grow at a 5.2% CAGR between 2026 and 2033.

Key opportunities include premium EV platform and battery enclosure optimization, low-carbon aluminum production with willingness to pay EUR 10-25 per tonne premiums, and emerging autonomous and connected vehicle applications requiring specialized aluminum extrusions for thermal management and electrical integration.

Key players include Constellium, Hydro Extrusions, Novelis (Aleris operations), and Aluswiss, supported by regional specialists such as Pechiney, Aleona, Grangemouth Extrusions, and Trimet, with strategic initiatives focused on hydrogen-powered production, battery enclosure innovation, and sustainability positioning for European OEM decarbonization and EV platform development.