- Automotive Components & Materials

- Automotive Glass Market

Automotive Glass Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Glass Market By Product Type (Tempered Glass, Others), Application (Windscreen, Backlite, Sidelite, Others), Vehicle (Passenger Cars, Others), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2025 - 2032

Automotive Glass Market Size and Trends Analysis

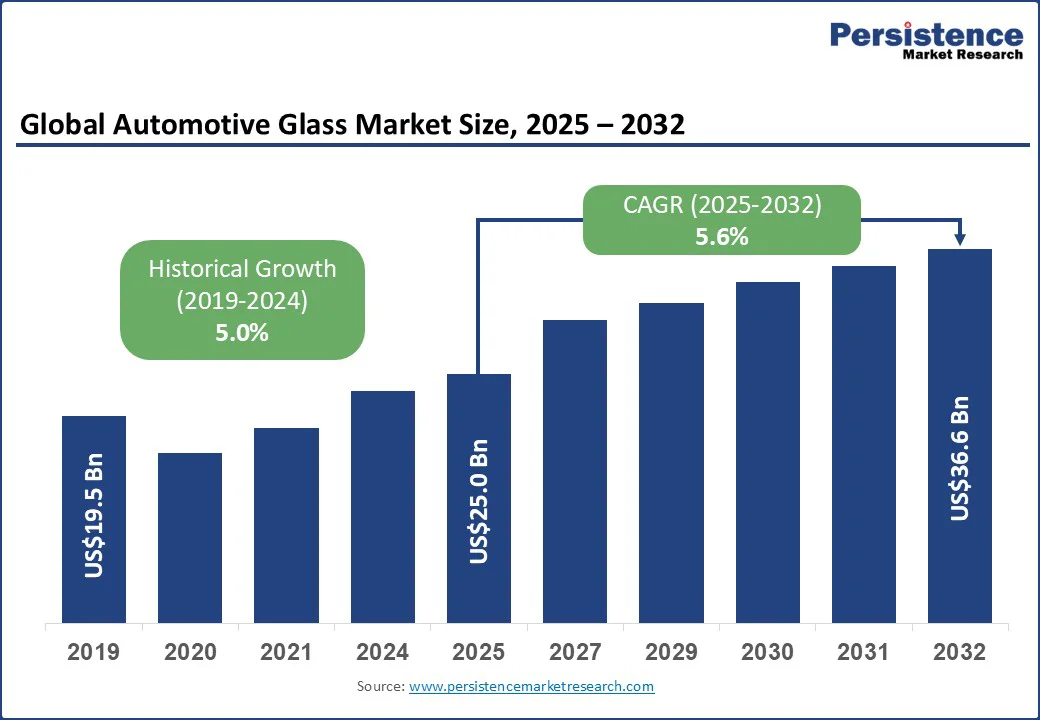

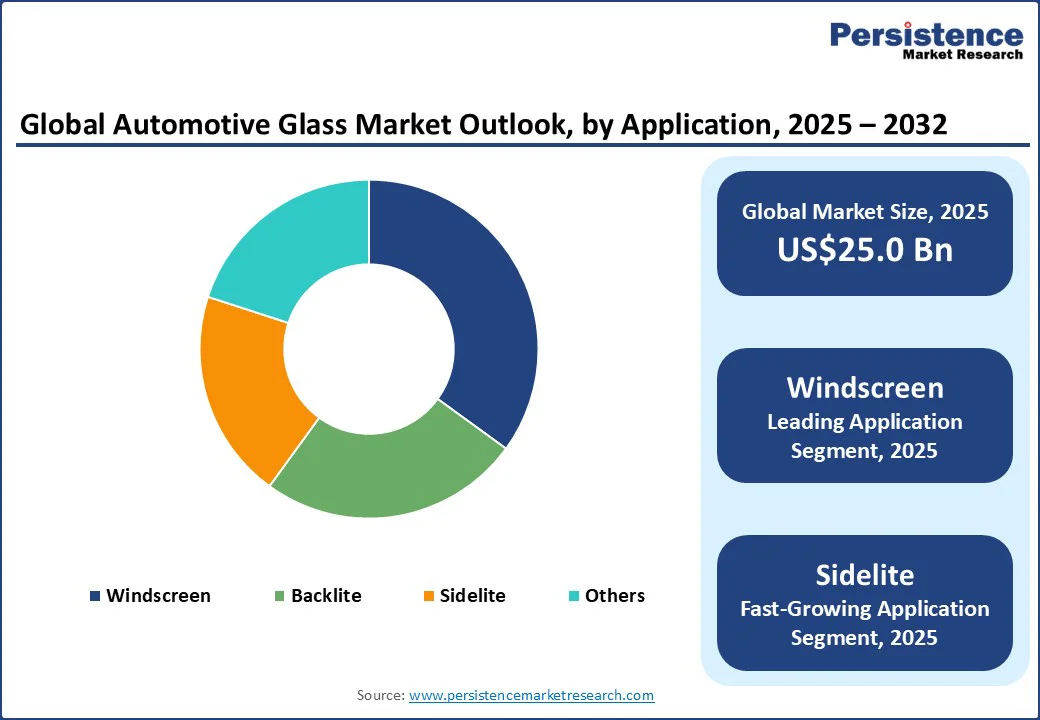

The global automotive glass market size is likely to be valued at US$25.0 Bn in 2025 and is expected to reach US$36.6 Bn by 2032, growing at a CAGR of 5.6% during the forecast period from 2025 to 2032.

The automotive glass industry is witnessing rapid innovation, with technologies such as smart glass and Gorilla glass transforming vehicle safety, efficiency, and comfort. Gauzy is at the forefront of this shift with its advanced smart glass solutions that integrate dynamic light and vision control into modern vehicle design.

Gauzy’s glass enables instant opacity adjustment while blocking UV and infrared light and minimizing glare by using suspended particle device (SPD) and polymer-dispersed liquid crystal (PDLC) technologies. These features enhance passenger comfort, reduce heat buildup, improve energy efficiency, and boost the overall safety. The adoption of Gauzy’s smart glass by leading automakers, including Mercedes-Benz, Ferrari, and BMW, highlights its growing influence and critical role in shaping the future of automotive glass technology.

Key Industry Highlights

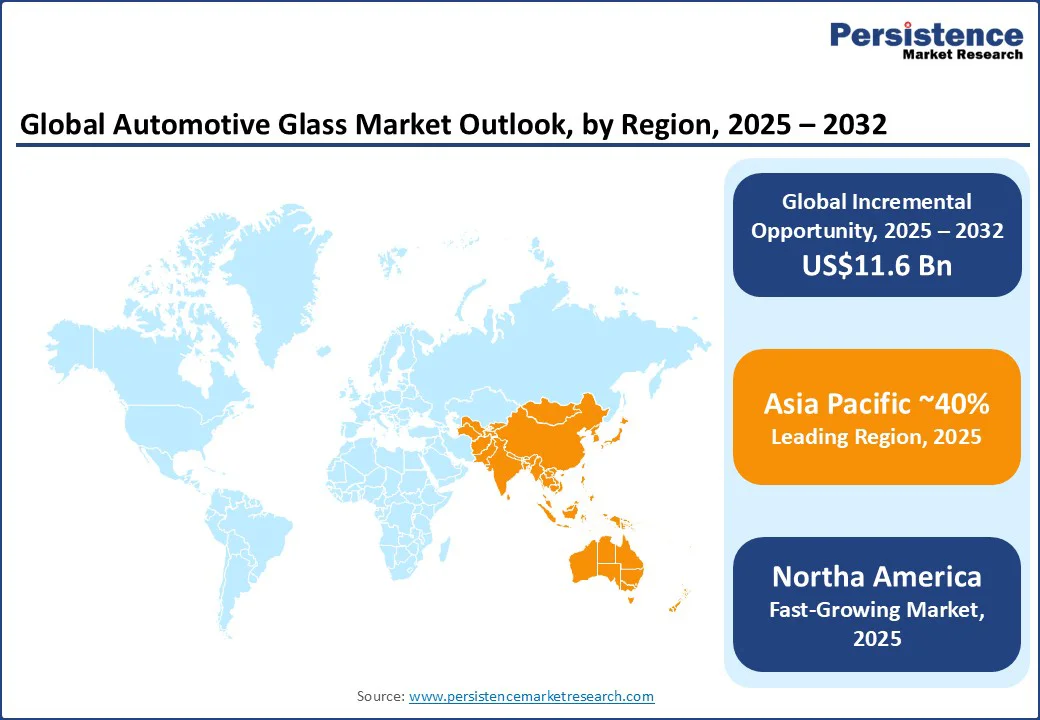

- Leading Region: Asia Pacific, accounting for over 40% market revenue share in 2025, driven by robust automotive production in China, India, and Japan, coupled with strong OEM and Tier-1 supplier networks.

- Fastest-growing Region: North America, projected CAGR of 6.5% from 2025 to 2032, fueled by increasing vehicle production, expansion of electric and hybrid vehicle manufacturing, and localization of glass supply chains.

- Dominant Vehicle Type: The passenger cars segment led the market with the largest revenue share of 62.3% in 2025, due to rising vehicle ownership, growing demand for comfort and safety features, and increasing adoption of advanced automotive glass technologies.

- Leading Product Type: The tempered glass segment led the market with the largest revenue share of 60.1% in 2025, owing to its high strength, cost-effectiveness, safety benefits, and widespread use in side and rear windows across passenger and commercial vehicles.

- Country Dominance: China dominates the market, driven by its vast automotive manufacturing base, cost-effective production, and strong export capacity. The country is home to leading players such as Fuyao Glass and Xinyi Glass, supplying both domestic and international automakers, making it the global hub for automotive glass production and exports.

- Import-Export Scenario: Asia Pacific, particularly China and India, is emerging as a major exporter due to large-scale production. Europe and North America import high volumes to meet demand for advanced glass technologies, while regulatory standards and logistics significantly influence trade flows.

|

Global Market Attribute |

Key Insights |

|

Automotive Glass Market Size (2025E) |

US$25.0 Bn |

|

Market Value Forecast (2032F) |

US$36.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.0% |

Market Dynamics

Driver - Increasing Demand for Electric and Hybrid Vehicles

The rise in the production of electric vehicles and the incorporation of various new technologies in terms of display and battery are expected to positively influence the demand for automotive glass over the forecast period. For instance, in December 2024, Hyundai introduced a Metal-Coated Heated Glass system in its luxury Genesis EV models. This 48-volt system rapidly clears ice from the windshield in just five minutes, significantly faster than traditional defrosting systems, enhancing safety and convenience for drivers.

Between 2023 and 2024, the global EV sales grew by 25% Y-o-Y, with monthly sales approaching the mark of 2 million units. The lightweight glass, which is a key component in reducing the overall weight of the vehicle has witnessed a surge in demand from the sector. These vehicles require specialized glass components, such as sunroofs and wide-angle windshields, which drive the market demand.

Restraint - Rising Raw Material Costs to Restrain Market Growth

One of the key restraints in the automotive glass market is the rising cost and limited availability of essential raw materials. Glass production heavily depends on raw materials and energy, which together form a major portion of its cost structure. Soda ash, a crucial input for glass manufacturing, has experienced continuous price increases in recent months due to supply shortages. Such fluctuations directly impact production costs and, in turn, glass prices, creating uncertainty for manufacturers.

Although soda ash producers are working to expand capacities to meet the growing demand from industries such as automotive glass, chemicals, and industrial products, the imbalance between demand and supply remains a challenge. These rising input costs are expected to restrain profitability and hinder smooth expansion in the market.

Opportunity - Shift Toward Sustainable and Smart Glass Solutions

The growing focus on sustainability and environmental consciousness opens doors for the automotive glass market to explore energy-efficient and sustainable glass solutions. Manufacturers can develop glass products that are lightweight, energy-efficient, and recyclable, incorporating advanced coatings and materials that enhance thermal insulation and reduce energy consumption.

The integration of smart glass technologies, such as electrochromic and photovoltaic glass, improves vehicle efficiency and contributes to sustainable mobility. This shift toward sustainable glass solutions aligns with global efforts to reduce carbon emissions, promote a greener future, and meet stringent environmental regulations.

SPD technology allows for rapid switching between light and dark states, offering instant control over the amount of light passing through the glass. This rapid response time is highly advantageous for enhancing visual comfort for passengers and drivers in various lighting conditions.

Category-wise Analysis

Product Type Insights

Based on product, tempered glass is projected to dominate with a 60% revenue share in 2025, due to its affordability, strength, and durability. It is four to five times stronger than float glass and more cost-effective than laminated glass, making it the preferred choice for side windows and backlights.

Its ability to shatter into small, blunt fragments upon impact enhances passenger safety, reducing the risk of severe injuries. Additionally, tempered glass is widely used due to its ease of manufacturing and installation, further contributing to its market dominance.

The laminated glass segment is projected to grow at a rapid CAGR. Laminated glass is also popular for sunroofs, driving segment growth. Prominent car manufacturers, including Volvo, Ferrari, and Tesla, incorporate laminated glass in vehicles featuring panoramic sunroofs.

Vehicle Insights

The passenger cars segment is expected to dominate in 2025, accounting for the largest revenue share of 62.3%. This growth is driven by shifting consumer preferences, a steadily expanding middle-class population, and rising environmental concerns, which are boosting the demand for lightweight and low-emission vehicles. In contrast, the light commercial vehicles (LCVs) segment is projected to record the fastest CAGR during the forecast period. The surge in transportation and construction activities is fueling the demand for commercial vehicles globally.

Notably, Vietnamese EV manufacturer VinFast has begun construction of its first integrated EV manufacturing facility in Thoothukudi, Tamil Nadu. Covering 400 acres, the facility represents a planned investment of up to US$2 Bn, with an initial US$500 Mn over five years. Operations are set to start by June 2025 with a capacity of 50,000 units, expandable to 150,000 units annually.

Regional Insights

Asia Pacific Automotive Glass Market Trends - Leading Region

Asia Pacific is anticipated to dominate, capturing a significant 44.2% revenue share in 2025. This can be attributed to the region's robust economic growth, increasing disposable incomes, and the rising demand for commercial vehicles. The automotive industry in Asia Pacific is witnessing substantial investments, further driving market growth.

China’s automotive output, surpassing 26.8 million units in 2024, is driving significant demand for advanced automotive glass solutions, with leading manufacturers such as Fuyao Glass and Xinyi Glass at the forefront of innovation. In China, the adoption of LiDAR technology in ADAS is gaining momentum, as manufacturers increasingly integrate it to enhance autonomous driving capabilities. This trend indicates a growing opportunity for specialized automotive glass that supports the sensors and systems needed for autonomous driving.

Government initiatives such as India’s “Make in India” program are strengthening domestic automotive component and glass production, while the rapid rise in EV manufacturing by companies including BYD and Tata Motors is increasing the demand for lightweight, energy-efficient glass, including panoramic sunroofs and wide-angle windshields.

North America Automotive Glass Market Trends - Strengthened by Commercial Vehicle Sales and Technological Advancements

North America’s automotive glass market is projected to expand at a CAGR of 4.4%, fueled by increasing sales of commercial vehicles that drive demand for high-performance glass solutions. Manufacturers are focused on integrating value-added features such as solar control, de-icing, rain/light sensors, and embedded antennas to differentiate their products and boost profitability.

The U.S. is one of the largest automotive markets in the world. Owing to continuous technological advancements, the applications of automotive glass in the U.S. are highly technical. The presence of numerous glass and car manufacturers is expected to play a key role in fueling the automotive glass demand in the U.S.

The U.S. alone has approximately 289 million vehicles, representing 18% of the global total and one of the highest ownership rates globally, with about 860 vehicles per 1,000 people. This substantial vehicle base drives consistent demand for automotive glass, both for new vehicles and aftermarket replacements.

Competitive Landscape

The global automotive glass market depends strongly on raw material manufacturers, suppliers, distributors, and end-users. Despite the presence of many participants, the market remains consolidated, with major players such as AGC Ltd., Saint-Gobain, Fuyao Glass Industry Group Co., Ltd., and NSG Group holding dominant positions.

Leading manufacturers are adopting strategies such as capacity expansions, mergers, acquisitions, and product innovations to strengthen their market share. Vertical integration across the value chain has also emerged as a key approach to gaining a competitive edge.

Additionally, startups introducing innovative solutions are intensifying competition. To remain ahead, companies are investing in expanding production capacity and advancing technological features. The focus is on creating innovative functionalities and integrating new technologies to ensure successful market entry, long-term growth, and broader adoption in this dynamic industry.

Key Industry Developments

- In March 2024, PGW Auto Glass acquired AutoglassCRM, a provider of VIN decoding and point-of-sale software, to equip automotive glass installers with advanced tools for a competitive market. The acquisition supported PGW's strategic mission to provide customers with the best technologies to compete in the complex industry. "Everything Autoglass" offered a low-cost, advanced technology solution covering all aspects of shop management, aiming to help customers succeed.

- In December 2023, Corning, a global leader in automotive glass solutions, advanced its innovation efforts with the launch of ColdForm™ Technology and Fusion5™ Glass under its Automotive Glass Solutions division. These technologies marked a significant industry shift by enabling manufacturers to form glass at room temperature.

Companies Covered in Automotive Glass Market

- AGC Inc.

- Fuyao Glass Industry Group Co., Ltd.

- Nippon Sheet Glass Co., Ltd.

- Saint-Gobain

- Corning Incorporated

- PGW Auto Glass

- Xinyi Glass Holdings Limited

- Central Glass Co., Ltd.

- Guardian Industries

- TAIWAN GLASS IND. CORP.

Frequently Asked Questions

The automotive glass market is estimated to be valued at US$25.0 Bn in 2025.

The key demand driver is the growing emphasis on vehicle safety, comfort, and energy efficiency, supported by advancements in glass technologies.

In 2025, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the automotive glass market.

Passenger vehicles hold the highest preference, capturing beyond 60% of the market revenue share in 2025, surpassing other vehicles.

The key players include AGC Inc., Fuyao Glass Industry Group Co., Ltd., Nippon Sheet Glass Co., Ltd., Saint-Gobain, and Corning Incorporated.