- Biotechnology

- Antibody Testing Market

Antibody Testing Market Size, Share, and Growth Forecast, 2025 - 2032

Antibody Testing Market By Assay Type (Immunoassays, Lateral Flow Assays, Rapid Tests, ELISA-based Tests, Multiplex Assays, Others), Application (Infectious Diseases, Autoimmune Diseases, Others), End-user (Hospitals, Diagnostic Laboratories, Others), and Regional Analysis for 2025 - 2032

Antibody Testing Market Share and Trends Analysis

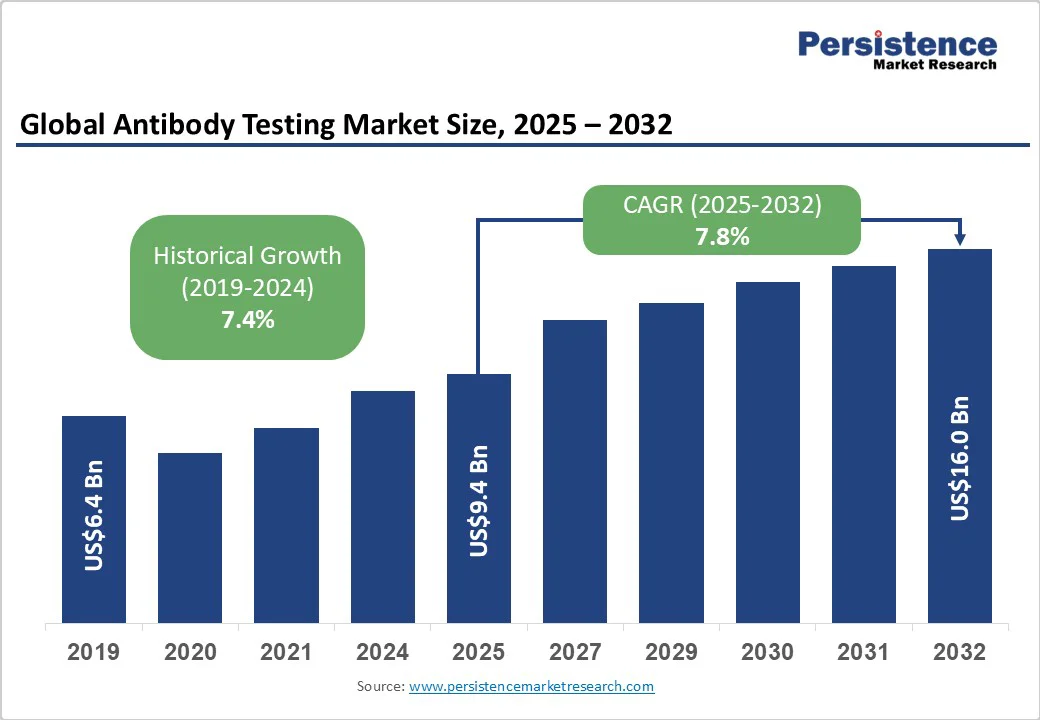

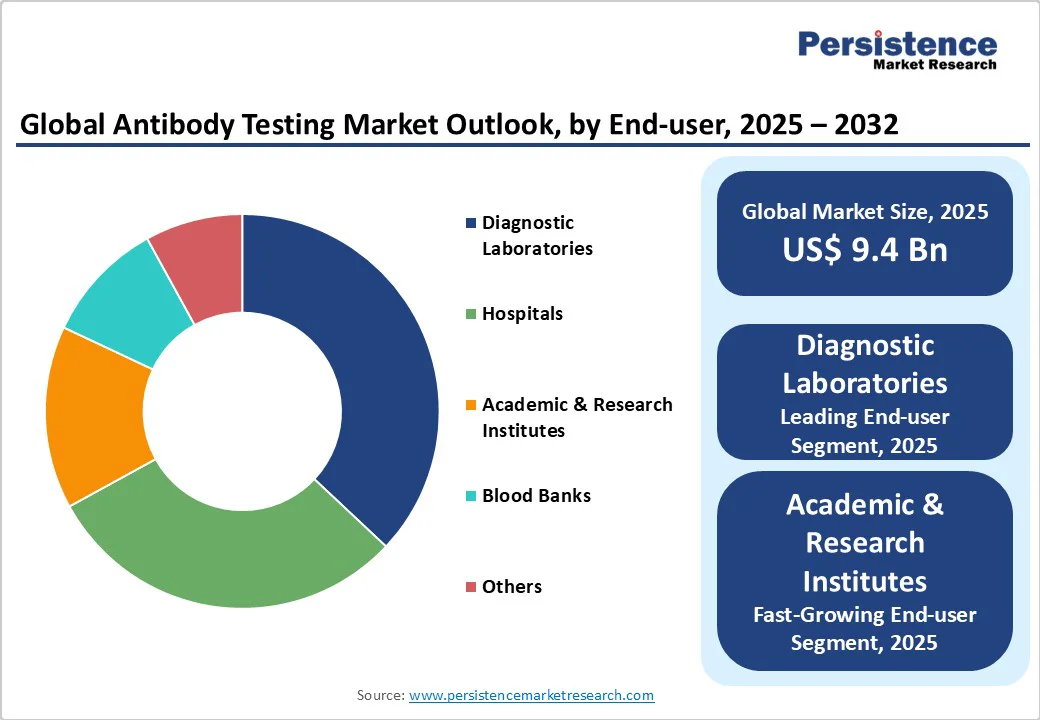

The global antibody testing market size is likely to be valued at US$9.4 billion in 2025. It is estimated to reach US$16 billion by 2032, growing at a CAGR of 7.8% during the forecast period 2025−2032, driven by the sustained prevalence of infectious diseases, the rapid adoption of advanced diagnostic technologies, and increasing investments in public health.

Major healthcare infrastructure upgrades and the expanding focus on precision diagnostics are supporting robust demand, while the rise in population health initiatives and the acceleration of point-of-care solutions are further amplifying market growth. Recurrent outbreaks of diseases and shifting regulatory priorities will also drive market growth.

Key Industry Highlights

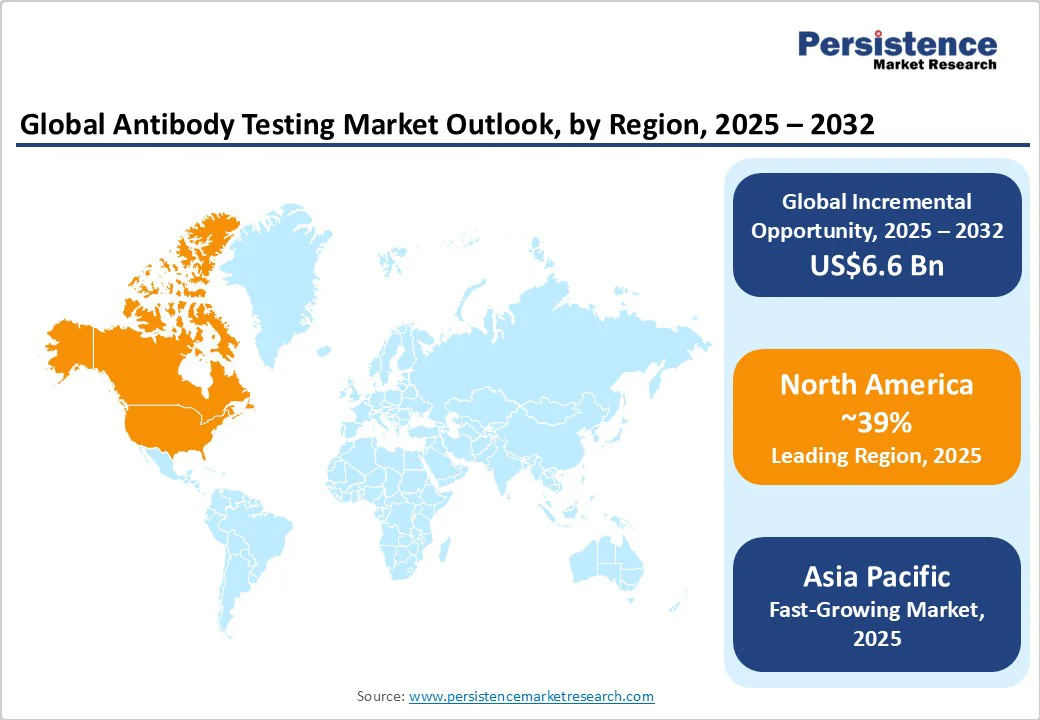

- Dominant Region & Fastest-growing Regional Market: North America is slated to lead with around 39% market share in 2025, whereas Asia Pacific is likely to post the highest growth rate during 2025-2032.

- Leading & Fastest-growing End-users: Diagnostic laboratories are projected to hold approximately 37% of the end-user share in 2025, while research institutes are expected to be the fastest-growing segment through 2032.

- Dominant & Fastest-growing Assays: ELISA-based assays are anticipated to lead with a 44% share in 2025; rapid lateral flow assays are projected to grow the fastest from 2025 to 2032.

- July 2025: Agilus Diagnostics and Sebia launched an Anti-MCV antibody test for the early detection of rheumatoid arthritis, particularly in seronegative patients.

- Strategic Initiatives: Next-generation technology investments, rapid diagnostics expansion in emerging economies, and partnerships with research and hospital networks.

| Key Insights | Details |

|---|---|

|

Antibody Testing Market Size (2025E) |

US$9.4 Bn |

|

Market Value Forecast (2032F) |

US$16 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Proliferation of Respiratory Infections and Chronic Diseases

In 2021, the World Health Organization (WHO) reported nearly 2.5 million deaths from lower respiratory infections and 8.8 million from COVID-19, while chronic non-communicable diseases caused around 43 million deaths globally. The COVID-19 pandemic accelerated investments in antibody-based diagnostics, driving demand for scalable, rapid-response testing systems.

According to CDC surveillance, diagnostic testing for diseases such as hepatitis and tuberculosis has increased over 12% annually since 2019, with serological testing surging in dengue- and HIV-endemic regions. This growing disease burden sustains high antibody test utilization, promoting organic market growth and fostering competitive innovation through technological advancements.

Emerging economies benefit significantly from point-of-care antibody testing, which is extensively used in community screenings and vaccination monitoring, creating long-term opportunities for manufacturers offering high-throughput, user-friendly platforms. Immunodiagnostic advances, including multiplex assays, digital ELISA, and automated chemiluminescence analyzers, are revolutionizing antibody testing, with patent filings for novel immunoassays rising 18% between 2020 and 2023.

Approximately 30% of new diagnostic product launches focus on improving antibody tests. Precision medicine further fuels growth, with the European Medicines Agency noting that over half of cancer therapies in clinical trials utilize antibody-based companion diagnostics. Manufacturers investing in next-generation technologies and data analytics are well-positioned to capture premium market segments in hospitals and research institutions.

Cross-Reactivity and Technical Accuracy Limitations

Cross-reactivity remains a significant challenge for antibody tests, affecting diagnostic accuracy across many applications. Studies show that 15%-20% of commercial antibody kits exhibit cross-reactivity with unrelated pathogens or human proteins, leading to false positives. This issue is especially problematic in autoimmune disease diagnostics, where overlapping antibody signatures are common.

For example, SARS-CoV-2 antibody tests have demonstrated cross-reactivity with other coronaviruses, and rheumatoid factors further complicate the interpretation. These limitations reduce physician confidence and increase the risk of misdiagnosis or inappropriate treatment. Achieving 100% specificity requires extensive epitope mapping and validation, which increases development costs and delays market entry.

The lack of universally accepted validation standards also hinders market growth and the approval process. The Global Biological Standards Institute reports that no clear minimum standards exist, with over 500 scientists citing inconsistent validation as a major cause of research irreproducibility. Regulatory requirements differ widely between the EMA, the FDA, and national bodies, extending approval timelines by 12-18 months and raising compliance costs above US$2 million per product in key markets.

Home-Based Testing and Telemedicine Integration Expansion

The integration of antibody testing with telemedicine and at-home diagnostics is transforming the market, projected to exceed US$1.2 billion by 2030. Rising consumer demand for convenient, privacy-focused healthcare has driven the widespread adoption of home testing kits, particularly following the COVID-19 pandemic.

Telemedicine platforms enable remote consultations, real-time result interpretation, and seamless integration of digital health records, all of which ensure clinical oversight and regulatory compliance. Companies offering user-friendly home collection kits with smartphone connectivity and cloud-based reporting are rapidly expanding, some experiencing 150% year-over-year growth in users. This trend extends beyond infectious disease management to chronic disease management, autoimmune monitoring, and routine health screenings, generating sustainable revenue through subscription-based services and repeat testing.

AI and machine learning are enhancing antibody testing workflows by improving result accuracy and reducing human error by up to 35% in labs. Automation enables high-throughput processing, multiplex testing, and real-time quality control, thereby increasing efficiency and reducing operational costs. Firms that invest in predictive analytics, automated reporting, and AI-driven cross-reactivity detection gain a competitive advantage. Emerging technologies such as CRISPR diagnostics, mass spectrometry validation, and single-cell proteomics further differentiate products, enabling precise, personalized medicine and therapeutic monitoring. Together, these advancements position the market for robust growth and innovation.

Category-wise Analysis

Assay Type Insights

ELISA-based assays are expected to maintain their dominant position, accounting for an estimated 44% of the revenue share in 2025, driven by their proven accuracy, regulatory acceptance, and broad clinical applications across hospitals and diagnostic laboratories. This dominance stems from decades of clinical validation, standardized protocols, and compatibility with existing laboratory infrastructure, making them the preferred choice for high-volume testing in infectious diseases, autoimmune disorders, and vaccine efficacy monitoring.

The leadership of this segment is further reinforced by the cost-effectiveness of bulk testing scenarios and the availability of automated ELISA platforms, which enable laboratories to process hundreds of samples daily with minimal manual intervention.

Rapid tests, particularly lateral flow assays, are forecast to be the fastest-growing segment, as demand is expected to accelerate for on-site diagnostics and decentralized healthcare delivery models. This rapid expansion is driven by increasing adoption in point-of-care settings, emergency departments, and community health programs, where immediate results are crucial for informed clinical decision-making.

The segment is also benefiting from technological advances in microfluidics, improved sensitivity through signal amplification, and the development of multiplex lateral flow devices that can detect multiple antibodies simultaneously. Manufacturers are leveraging innovations in biosensor technology, smartphone integration, and digital result interpretation to differentiate rapid assay solutions and capture market share in emerging economies where laboratory infrastructure remains limited.

Application Insights

Infectious diseases are projected to convincingly dominate as the leading application, capturing approximately 51% of total market revenue in 2025, driven by persistent regional outbreaks, pandemic preparedness initiatives, and heightened surveillance needs in emerging markets. Substantial government investment in community-based screening programs, WHO-mandated disease monitoring protocols, and the ongoing need for serological surveillance of endemic diseases such as hepatitis, tuberculosis, and HIV underpin the robust performance. The prospects of this segment are further strengthened by the increasing frequency of zoonotic disease outbreaks and the growing emphasis on monitoring vaccine effectiveness, particularly in regions with high population density and limited healthcare infrastructure.

Oncology applications are expected to be the fastest-growing segment from 2025 to 2032, driven by the increasing demand for personalized immunotherapy, the expansion of antibody-based companion diagnostics in advanced cancer care, and the growing adoption of immune checkpoint inhibitor therapies.

The segment is experiencing accelerated growth due to increased investments in precision oncology, the development of novel biomarker panels for cancer prognosis, and the integration of antibody testing in clinical trial protocols for new cancer therapeutics. Cancer centers and specialized oncology clinics are driving the adoption of personalized treatment selection and therapeutic monitoring, creating opportunities for premium-priced diagnostic solutions.

End-user Insights

Diagnostic laboratories are expected to sustain the highest share of the market, estimated at 37% in 2025, primarily benefiting from centralized procurement, enhanced capabilities, and the adoption of advanced tests across multiple disease areas. Their position is strengthened by established research partnerships, integration of automated high-throughput analyzers, and the ability to process large sample volumes cost-effectively.

Major laboratory networks are consolidating market share through strategic acquisitions and standardized testing protocols that enable consistent quality across multiple locations. The segment’s dominance is further reinforced by insurance reimbursement preferences for accredited laboratory testing and the increasing complexity of diagnostic assays that require specialized expertise and equipment.

Academic and research institutes form the fastest-growing end-user segment, driven by expanding research funding from government agencies, pharmaceutical companies, and international health organizations focused on developing next-generation diagnostic technologies. Universities and research centers are increasingly adopting cutting-edge antibody testing platforms for biomarker discovery, therapeutic development, and epidemiological studies, creating demand for specialized, high-sensitivity assays not typically used in routine clinical practice. The segment also benefits from collaborative research initiatives, public-private partnerships, and the growing emphasis on precision medicine research that requires sophisticated antibody characterization and validation.

Regional Market Insights

North America Antibody Testing Market Trends

North America is projected to lead in 2025 with a 39% market share, driven primarily by the U.S. The region benefits from advanced healthcare infrastructure, high per capita healthcare spending exceeding $ 12,000, and a robust regulatory framework overseen by the FDA. Continuous funding from the National Institutes of Health (NIH) supports diagnostic innovation, while widespread adoption of advanced testing technologies across major hospitals and health networks accelerates market growth. Key drivers include rapid diffusion of technology, health system consolidation, and strong private sector investment in diagnostic automation and AI-powered platforms.

Clinical adoption of multiplex assays, expansion of personalized medicine programs, and significant public investment in pandemic response and chronic disease surveillance further strengthen the market. The competitive landscape features established multinationals and agile startups engaging in cross-border mergers and acquisitions (M&A), backed by venture capital and expedited regulatory pathways. Investment is concentrated in high-throughput immunoassay systems, AI-enhanced diagnostics, and point-of-care testing, supported by state-level efforts to streamline reimbursement and regulatory processes for quicker adoption.

Europe Antibody Testing Market Trends

Europe is expected to account for 27% of the market share in 2025, led by Germany, France, and the U.K. Germany remains the region’s largest market, supported by strong manufacturing capabilities, advanced research infrastructure, and government-backed biotechnology programs. France benefits from its centralized healthcare system and focus on preventive diagnostics, while the U.K. leverages post-Brexit regulatory independence to fast-track innovative diagnostic approvals. The European Medicines Agency (EMA) is accelerating harmonized approval processes for antibody tests, complemented by national health ministries prioritizing disease surveillance, cancer detection, and infectious disease control.

Implementation of the In Vitro Diagnostic Regulation (IVDR) and Horizon Europe funding is enhancing cross-border collaboration and product standardization. EU priorities around sustainability are also spurring demand for eco-friendly diagnostic solutions and minimal packaging waste. Key investment areas include digital health platforms, telemedicine integration, and supply chain resilience. Competition intensifies through the development of pan-European laboratory networks, technology licensors, and growing public-private partnerships that support diagnostic innovation.

Asia Pacific Antibody Testing Market Trends

The Asia Pacific is the fastest-growing region, driven by large patient populations, rapid economic development, and substantial investments in healthcare infrastructure. China leads regional expansion with its Healthy China 2030 initiative, extensive public health screening programs, and the world’s largest diagnostic manufacturing base. Japan contributes through rising healthcare demands from an aging population, strong regulatory support, and the adoption of advanced technology. India’s momentum is fueled by growing middle-class healthcare access, national insurance programs, and a cost-focused biotechnology sector. ASEAN countries are scaling diagnostic infrastructure and biosensor production while launching subsidized screening programs targeting infectious and chronic diseases.

Markets such as South Korea, Singapore, and Australia drive premium segment growth via cutting-edge research facilities, robust IP protections, and medical tourism. Regional manufacturing strengths include low-cost production, integrated supply chains, and proximity to raw material sources, enabling competitive pricing in cost-sensitive markets. Regulatory bodies such as China’s NMPA and India’s CDSCO are accelerating approvals, reducing market entry barriers. The competitive landscape features both domestic leaders and global firms expanding through joint ventures, partnerships, and tech transfers. Key opportunities include localized manufacturing, AI-powered diagnostics, and digital health integration to support scalable, affordable testing across diverse economic tiers.

Competitive Landscape

The global antibody testing market structure is moderately concentrated, with approximately 65% of global revenues accruing to the top ten players. Leading companies command sizable shares on the strength of proprietary assay platforms, geographic coverage, and established hospital and lab relationships. Roche Holding AG, Abbott Laboratories, and Thermo Fisher Scientific Inc. each maintain 8%-13% market shares, while mid-tier firms such as Bio-Rad Laboratories and Siemens Healthineers AG capture notable niche segments.

Despite such consolidation at the top, robust competition persists from specialized rapid test manufacturers and regional technology integrators, contributing to a dynamic blend of innovation, price pressure, and licensing rivalry.

Key Industry Developments

- In October 2025, Boster Biological Technology launched a free antibody validation program and expanded IHC services, offering complete support from project design to microscopic analysis. With over 16,000 validated antibodies, Boster ensures reproducibility and specificity across key research areas, utilizing publicly accessible data.

- In June 2025, SIAT and the Chinese Academy of Sciences developed a compact diagnostic platform that enables rapid COVID-19 antibody testing using a fingertip blood sample. Designed for point-of-care and potential at-home use, the portable device delivers quick, minimally invasive results, enhancing accessibility and testing capacity during pandemic conditions.

- In March 2025, Revvity's EUROIMMUN division received CE marking for its Anti-Measles Virus ELISA 2.0 (IgG) assay, the first in its portfolio to be validated for use with dried blood spots. This minimally invasive method enables stable, accessible measles testing using fingertip blood samples, ideal for routine use and resource-limited settings.

Companies Covered in Antibody Testing Market

- Roche Holding AG

- Abbott Laboratories

- Thermo Fisher Scientific Inc.

- Siemens Healthineers AG

- Bio-Rad Laboratories Inc.

- Danaher Corporation

- Becton, Dickinson and Company

- Merck KGaA

- PerkinElmer Inc.

- Eurofins Scientific SE

- Agilent Technologies Inc.

- QuidelOrtho Corporation

- DiaSorin S.p.A.

- Luminex Corporation

- Hologic Inc.

Frequently Asked Questions

The antibody testing market is projected to reach US$9.4 Billion in 2025.

Consistent prevalence of infectious diseases, the rapid adoption of advanced diagnostic technologies, and increasing investments in public health are driving the market.

The antibody testing market is poised to grow at a CAGR of 7.8% from 2025 to 2032.

Expanding focus on precision diagnostics, rise in population health initiatives, and the acceleration of point-of-care solutions are key market opportunities.

Roche Holding AG, Abbott Laboratories, and Thermo Fisher Scientific Inc. are some of the key market players.