- Automotive

- Wheel Loaders Market

Wheel Loaders Market Size, Share, and Growth Forecast, 2025 - 2032

Wheel Loaders Market by Type of Loader (Small Wheel Loaders, Medium Wheel Loaders, Large Wheel Loaders), Engine Power (Less than 100 HP, 100-200 HP, 201-300 HP, above 300 HP), Application (Construction, Agriculture, Mining, Forestry, Waste Management), End-use, and Regional Analysis for 2025 - 2032

Wheel Loaders Market Size and Trends Analysis

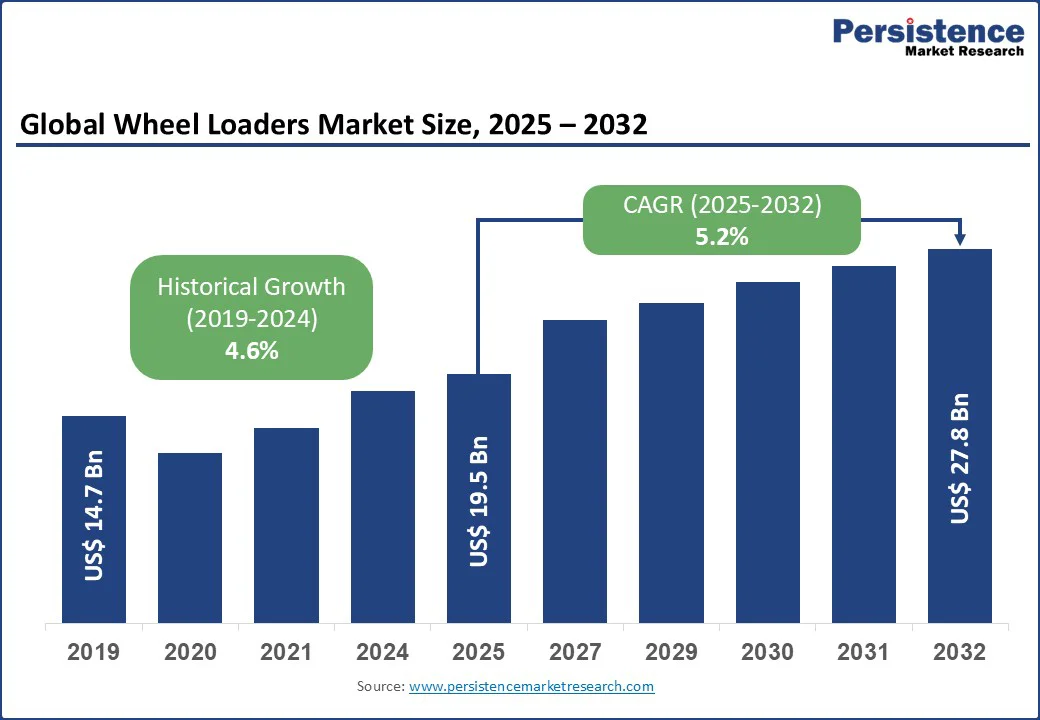

The global wheel loaders market size is projected to be valued at US$ 19.5 Bn in 2025 and is forecasted to reach US$ 27.8 Bn by 2032, growing at a CAGR of 5.2% during the forecast period from 2025 to 2032, driven by rising demand for efficient material handling in construction and mining, and advancements in loader technologies.

Key Industry Highlights:

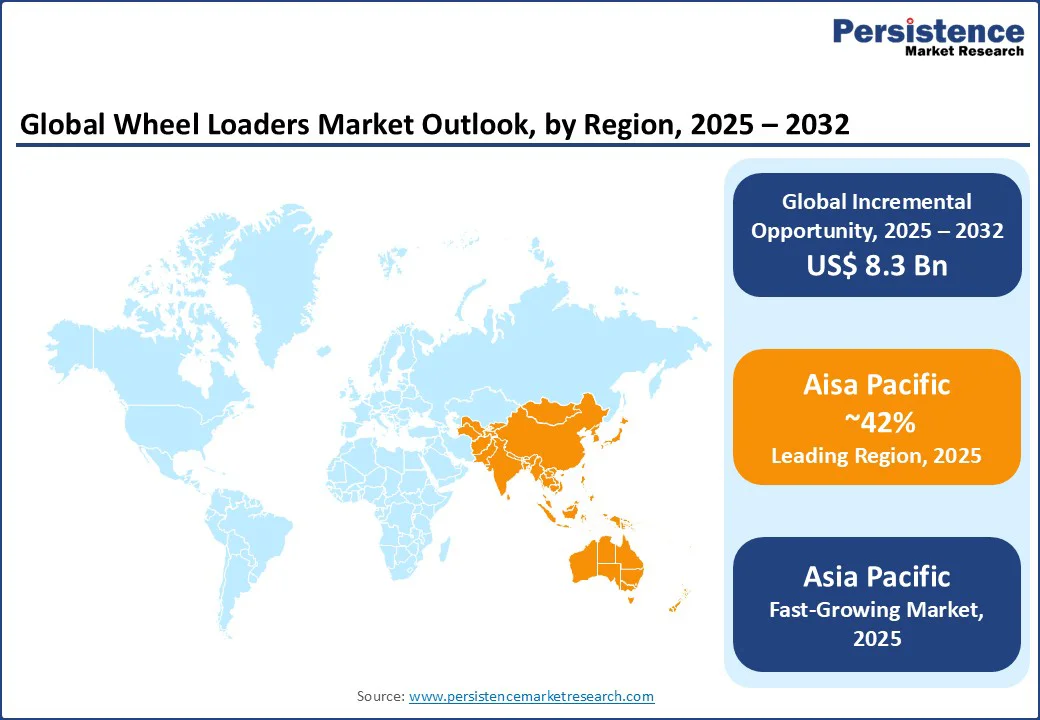

- Leading Region: Asia Pacific, holding a 42% share in 2025, driven by large-scale infrastructure projects and urbanization in China and India.

- Fastest-growing Region: Europe, propelled by increasing mining activities and infrastructure development in Germany and France.

- Dominant Type of Loader: Medium Wheel Loaders, commanding a 45% market share, due to their versatility and widespread use in construction and mining.

- Leading Application: Construction, accounting for 48% of market revenue, driven by global infrastructure investments.

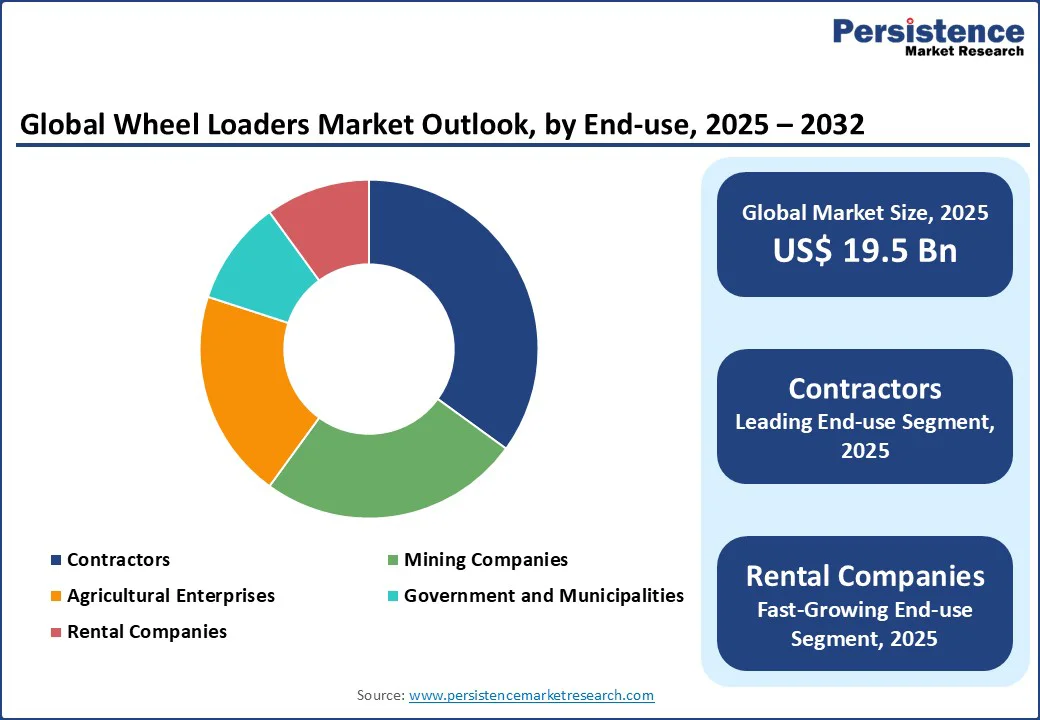

- Dominant End-use: Contractors, holding a 40% share, due to their extensive use in construction projects worldwide.

| Key Insights | Details |

|---|---|

|

Wheel Loaders Market Size (2025E) |

US$ 19.5 Bn |

|

Market Value Forecast (2032F) |

US$ 27.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.6% |

Market Dynamics

Drivers - Global Infrastructure Development and Technological Advancements

The wheel loaders market is propelled by several key drivers, supported by robust industry trends and statistics. Global infrastructure development is a primary catalyst, with governments worldwide investing heavily in transportation, urban development, and energy projects.

For instance, China’s Belt and Road Initiative and India’s Smart Cities Mission are driving demand for wheel loaders, with construction equipment sales in Asia Pacific expected to achieve 6% growth annually through 2032.

Technological advancements, such as hybrid and electric models, are enhancing fuel efficiency and reducing operational costs. Companies such as Caterpillar and Volvo have introduced loaders with telematics and automation, improving productivity by up to 15% in construction and mining applications.

Restraints - High Initial Costs Challenges Growth

Despite its growth, the wheel loaders market faces challenges. High initial costs of advanced bucket loaders, particularly those with hybrid or electric systems, can deter small and medium-sized enterprises, with prices ranging from US$ 50,000 to US$ 500,000 depending on size and features. Additionally, stringent environmental regulations in regions such as Europe and North America require manufacturers to invest in low-emission technologies, increasing production costs. The shortage of skilled operators also poses a restraint, as advanced loaders require specialized training, particularly in automated systems, which can limit adoption in developing regions.

Opportunities - Adoption of Electric and Hybrid Wheel Loaders

The wheel loaders market presents significant opportunities. The adoption of electric and hybrid bucket loaders offer growth potential, driven by global sustainability goals and incentives for green equipment. Integration with IoT and telematics provides opportunities for predictive maintenance and real-time monitoring, reducing downtime by up to 20%. Additionally, the expansion of rental services in emerging markets such as Latin America and the Asia Pacific offers cost-effective access to pay loaders with the equipment. Finally, growth in renewable energy projects, such as wind and solar farms, is increasing demand for shovel loaders in material handling and site preparation.

Category-wise Analysis

Type of Loader Insights

Medium Wheel Loaders dominate the market, expected to account for approximately 45% share in 2025. Their versatility, balancing power and manoeuvrability, makes them ideal for construction, mining, and waste management. These loaders, typically with bucket capacities of 2-4 cubic meters, are widely used in urban construction projects due to their efficiency in confined spaces.

Small Wheel Loaders are the fastest-growing segment, driven by their affordability and suitability for small-scale projects in agriculture and landscaping. Their compact size and lower operational costs are accelerating adoption in emerging markets like India and Brazil.

Engine Power Insights

The 100-200 HP segment leads the market, commanding a 38% share in 2025, due to its widespread use in medium-sized construction and mining projects. This power range offers a balance of fuel efficiency and performance, making it suitable for diverse applications.

The Above 300 HP segment is the fastest-growing, driven by increasing demand in large-scale mining and infrastructure projects. High-power loaders, used for heavy-duty tasks such as quarry operations, are seeing rapid adoption in regions such as Latin America and Africa.

Application Insights

Construction dominates the application segment, holding a 48% share in 2025, driven by global infrastructure investments and urbanization. Shovel loaders are critical for tasks such as earthmoving and material handling in residential, commercial, and industrial projects.

The mining segment is the fastest-growing, fueled by rising global demand for minerals and metals. The expansion of mining activities in countries like Brazil and Australia is driving demand for large wheel loaders.

End-use Insights

Contractors leading the end-use segment, accounting for 40% of the market in 2025, due to their extensive use of wheel loaders in construction projects worldwide. The rise in public-private partnerships for infrastructure development supports this segment’s dominance.

Rental Companies are the fastest-growing end-use segment, driven by the increasing popularity of equipment rental services in emerging markets. The cost-effectiveness of renting over purchasing is boosting demand.

Regional Insights

North America Wheel Loaders Market Trends

North America holds a significant share of the wheel loaders market, driven by robust construction and mining activities in the U.S. and Canada. The U.S. infrastructure bill, allocating US$ 1.2 Tn for transportation and urban development through 2030, is a key driver. In the U.K., the market is propelled by government investments in sustainable infrastructure and renewable energy projects, such as offshore wind farms. The U.K.’s Construction Equipment Association reports a 5% annual increase in wheel loader sales, driven by demand for compact and hybrid models in urban redevelopment projects such as HS2. Manufacturers such as JCB are responding with new electric wheel loader models, aligning with both regulatory targets and customer demand for cleaner, more efficient machinery.

Europe Wheel Loaders Market Trends

Europe is the fastest-growing region, led by Germany, France, and the U.K., supported by strong regulatory frameworks and infrastructure investments. Germany’s focus on Industry 4.0 and smart construction technologies drives demand for advanced shovel loaders with telematics.

France’s Grand Paris Express project, one of Europe’s largest infrastructure initiatives, boosts the need for medium and large front loaders. The European Union’s Green Deal, aiming for carbon neutrality by 2050, is a major driver reshaping the market. Regulatory pressure to reduce emissions is compelling both buyers and manufacturers to shift toward low-emission, hybrid, and fully electric loaders. Companies such as Volvo Construction Equipment and Liebherr are actively developing and commercializing hybrid and electric wheel loader models, positioning themselves as leaders in sustainable machinery solutions.

Asia Pacific Wheel Loaders Market Trends

Asia Pacific dominates the global market, holding a 42% share in 2025, driven by rapid urbanization and infrastructure development in China and India. China’s ongoing Belt and Road Initiative and India’s US$ 1.4 Tn National Infrastructure Pipeline are key drivers, with construction equipment demand expected to grow by 6.5% annually. The mining sector in Australia also contributes significantly, with large shovel loaders in high demand for iron ore and coal extraction.

The region’s shift toward smart city development and sustainable construction practices. Governments across China, Japan, South Korea, and India are actively promoting the adoption of electric and hybrid bucket loaders to reduce emissions, comply with tightening environmental regulations, and improve operational efficiency. This trend is further supported by technological advancements in battery systems, telematics, and automation, which are rapidly being integrated into next-generation loaders.

Competitive Landscape

The global wheel loaders market is highly competitive, with key players including Caterpillar, Deere & Company, Doosan Bobcat, Hitachi Construction Machinery, Komatsu, J C Bamford Excavators (JCB), Volvo, Yanmar, Kubota, and Terex Corporation. These companies focus on innovation, sustainability, and global expansion to maintain market leadership. Leading players are investing in R&D to develop fuel-efficient and electric tractor loaders, aligning with global sustainability goals. Strategic partnerships, such as JCB’s collaboration with rental companies in Latin America, are expanding market reach. Companies are also leveraging telematics and automation to offer advanced features, enhancing competitiveness in construction and mining applications.

Key Developments:

- In 2024, Caterpillar launched an all-electric version of its Cat 906 Wheel Loader, the Cat 906, at the beginning of 2024, which is designed for sustainability by producing zero exhaust emissions. This new electric model is essentially the same machine as the diesel-powered Cat 906K, but with a battery-electric power source, resulting in significantly reduced emissions and operational costs.

- In 2025, Volvo CE is introducing the first wave of a new generation of wheel loaders, starting with five models ranging in size from the L150 to the L260. Designed for optimal productivity, operator comfort and safety, these new wheel loaders are enhanced by innovative new technologies and service solutions. Customers will benefit from these new machines when they are introduced across select markets globally during 2025.

Companies Covered in Wheel Loaders Market

- Caterpillar

- Deere & Company

- Doosan Bobcat

- Hitachi Construction Machinery

- Komatsu

- J C Bamford Excavators

- Volvo

- Yanmar

- Kubota

- Terex Corporation

- Others

Frequently Asked Questions

The global wheel loaders market is projected to reach US$ 19.5 Bn in 2025.

Infrastructure development, technological advancements, and rising mining activities drive the market.

The market is expected to grow at a CAGR of 5.2% from 2025 to 2032.

Adoption of electric loaders and IoT integration offer significant growth opportunities.

Caterpillar, Komatsu, Volvo, JCB, and Hitachi Construction Machinery are key players.