- Rail

- Rail Wheel and Axle Market

Rail Wheel and Axle Market Size, Share, and Growth Forecast 2026 - 2033

Rail Wheel and Axle Market by Wheel Type (Monoblock Wheels, Resilient Wheels, Rubber Tired Wheels, Steel Tired Wheels, Other Special Wheels), Axle Type (Hollow Axles, Solid Axles), Product Type (Less Than 600mm, 600-1000 mm, 1000-1100 mm, Above 1100 mm), End Use (High Speed Railway, Fast Speed Railway, Subway, Other), Sales Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Rail Wheel and Axle Market Size and Trend Analysis

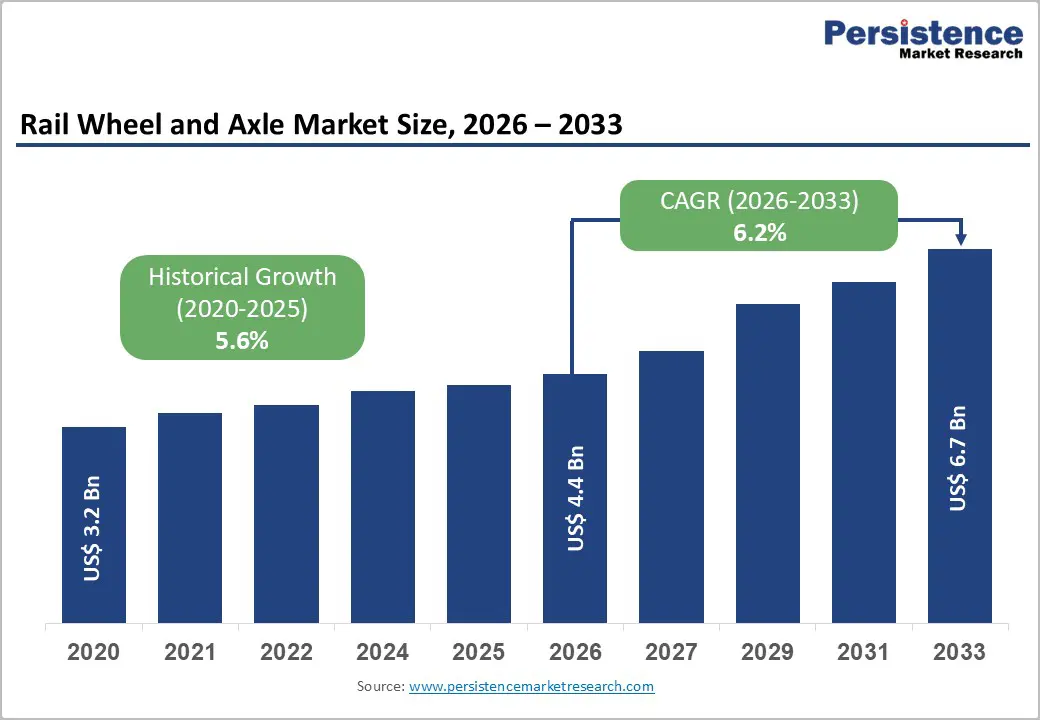

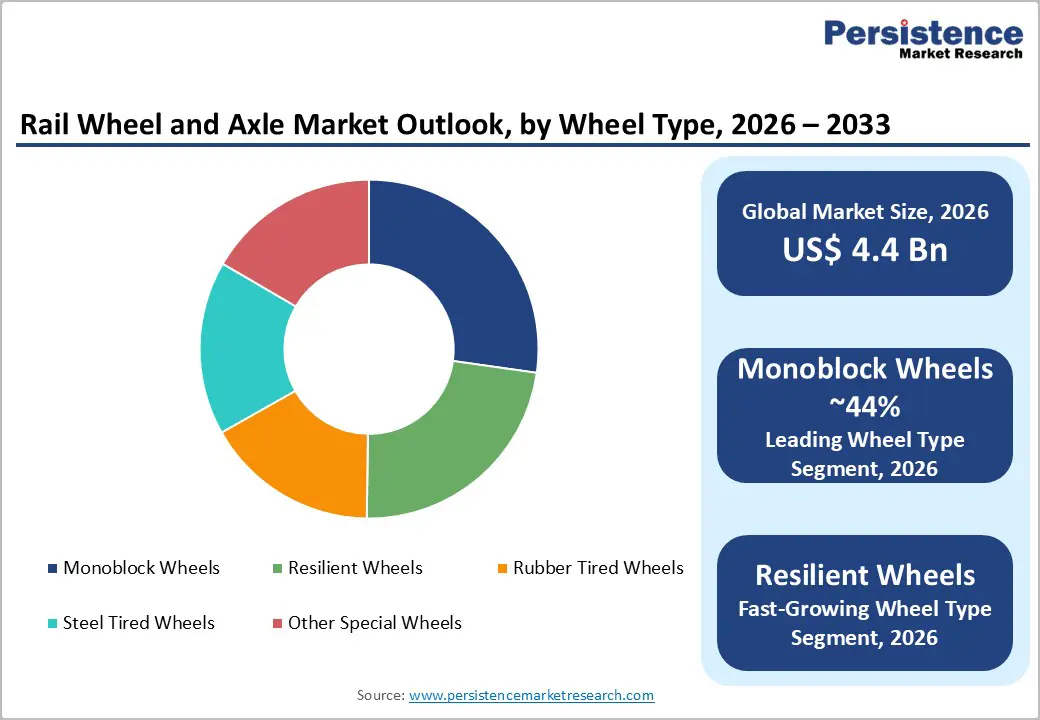

The global rail wheel and axle market size is expected to be valued at US$ 4.4 billion in 2026 and projected to reach US$ 6.7 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The market expansion is primarily driven by large-scale railway infrastructure modernization and capacity enhancement projects worldwide. Increasing investments in high-speed rail corridors and heavy-haul freight networks are strengthening demand for advanced wheelsets. Rapid urbanization and metro rail development further support market growth. Additionally, government initiatives promoting low-carbon transportation and technological advancements in high-strength, wear-resistant materials are accelerating product innovation and long-term adoption.

Key Industry Highlights:

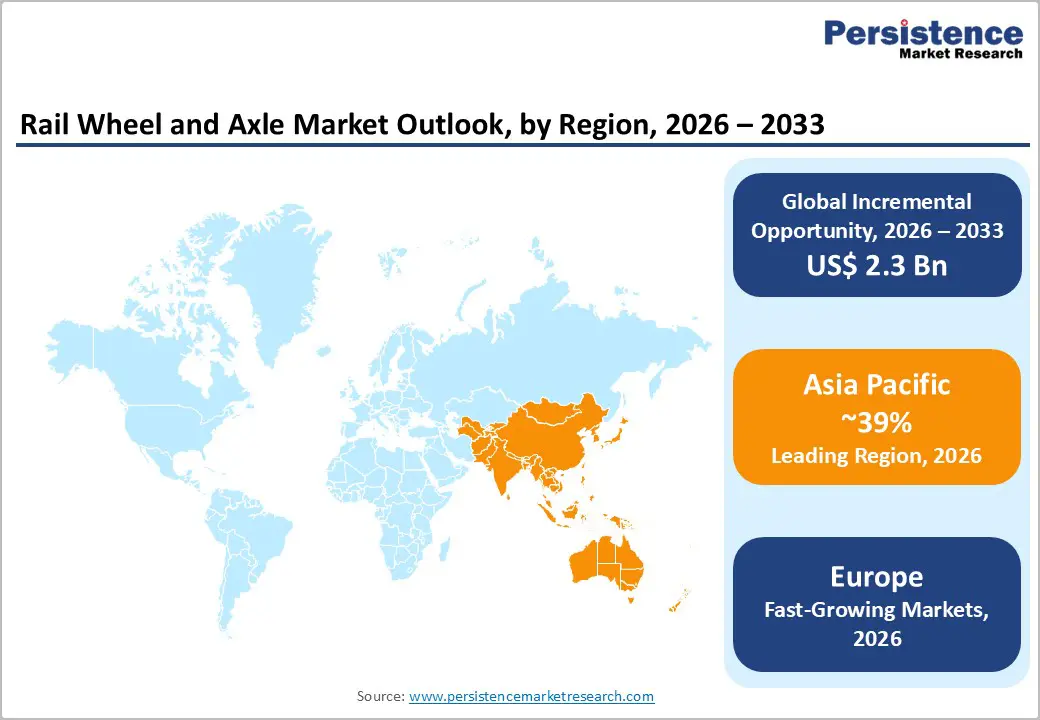

- Leading Region: Asia Pacific leads the market with approximately 39% share in 2025, driven by extensive railway infrastructure and strong domestic manufacturing capabilities.

- Fastest-Growing Region: Europe is the fastest-growing region with about 27% share in 2025, supported by modernization projects and EU infrastructure funding.

- Dominant Wheel Category: Monoblock Wheels dominate the market with roughly 44% share in 2025, favored for durability and reliability in freight and passenger applications.

- Fastest-Growing Axle Category: Hollow Axles are the fastest-growing segment, improving efficiency and reducing weight in high-speed rail systems.

- Key Opportunity: Urban Subway Systems present major growth potential, with expansion projects driving increasing replacement volumes.

| Key Insights | Details |

|---|---|

|

Rail Wheel and Axle Size (2026E) |

US$ 4.4 billion |

|

Market Value Forecast (2033F) |

US$ 6.7 billion |

|

Projected Growth CAGR(2026-2033) |

6.2% |

|

Historical Market Growth (2020-2025) |

5.6% |

Market Dynamics

Drivers - Accelerating Investments in High-Speed Rail Infrastructure and Network Modernization

Governments across major economies are significantly expanding high-speed rail networks to improve intercity connectivity and reduce carbon-intensive air travel. Countries such as China, Japan, and India continue investing in corridors designed for speeds above 300 km/h, requiring technologically advanced, fatigue-resistant wheels and axles.

These high-speed systems demand precision-engineered components capable of handling extreme rotational forces, thermal stress, and long operating cycles. Continuous infrastructure funding and network extensions create consistent demand for premium wheelsets, driving sustained production volumes and long-term replacement cycles within the market.

Growing Global Freight Rail Volumes and Heavy-Haul Capacity Expansion

Freight rail transport is witnessing steady growth due to its cost efficiency and lower environmental footprint compared to road transport. Rail networks are increasingly preferred for transporting bulk commodities, containers, and industrial goods over long distances, strengthening demand for heavy-duty wheel and axle assemblies.

Heavy-haul operations require solid forged axles and wear-resistant wheels designed to withstand high load stress and repetitive usage. Expanding trade flows, particularly across the Asia-Pacific and industrial corridors, are encouraging rail capacity upgrades, directly supporting replacement demand and aftermarket growth for wheelsets.

Restraints - Fluctuating Steel Prices and Supply Chain Instability Impacting Production Economics

Steel remains the primary raw material used in manufacturing rail wheels and axles, making the industry highly sensitive to price volatility. In recent years, global supply chain disruptions, energy cost increases, and geopolitical tensions have significantly affected steel availability and pricing structures.

Rising input costs increase overall production expenses, compress profit margins, and create pricing uncertainties for manufacturers. Smaller players are particularly vulnerable, as limited financial flexibility restricts their ability to absorb cost shocks. This volatility can delay procurement decisions, slow infrastructure projects, and affect overall market stability.

Stringent Safety Certifications and Compliance Requirements Limiting Market Entry

Rail wheel and axle components operate under critical safety conditions, requiring strict adherence to standards set by regulatory bodies such as the American Association of Railroads (AAR) and other international authorities. Extensive testing, certification procedures, and quality audits significantly increase compliance costs and production timelines.

Manufacturers must invest heavily in inspection systems, material testing, and traceability processes to meet regulatory approvals. Any product failure can result in costly recalls and reputational damage. These stringent requirements raise barriers to entry, limit rapid innovation, and slow the commercialization of new wheel and axle designs.

Opportunity - Technological Advancements in Lightweight Wheelsets and High-Performance Materials

Ongoing innovation in hollow axles, micro-alloyed steels, and composite-based wheel technologies is creating new growth avenues within the rail wheel and axle industry. Lightweight designs help reduce overall train mass, improving fuel efficiency, lowering energy consumption, and enhancing operational performance, particularly in high-speed passenger segments.

Advanced engineering now enables significant weight reduction without compromising structural strength, fatigue resistance, or safety standards. As high-speed rail corridors expand across Asia-Pacific and Europe, demand for lighter, durable components is increasing. Companies investing early in these technologies can secure competitive advantages and premium contracts.

Expansion of Urban Metro and Subway Networks in Rapidly Urbanizing Economies

Rapid urbanization is driving large-scale investments in metro and subway systems across developing and developed economies. Countries such as India and China continue expanding urban rail networks to manage congestion and support sustainable public transportation initiatives.

Urban transit systems require specialized wheel designs capable of handling frequent acceleration, braking cycles, and tight curves. Some networks also adopt rubber-tired or resilient wheel configurations to reduce noise and vibration. Continuous metro expansion and strong public infrastructure funding create recurring demand for both original equipment and replacement wheelsets.

Category-wise Analysis

Wheel Type Insights

Monoblock wheels account for approximately 44% of the market share in 2025, making them the leading wheel type globally. Manufactured from a single forged steel piece, these wheels provide superior structural strength, fatigue resistance, and durability under heavy loads. Their widespread adoption across freight wagons and passenger coaches is driven by low maintenance requirements, long service life, and compliance with stringent UIC and international safety standards.

Resilient wheels are emerging as the fastest-growing segment, particularly within urban transit systems. Designed with elastic elements to absorb vibration and reduce noise, they are increasingly preferred for metro and light rail applications. Rising urban rail expansion and stricter noise regulations are accelerating their adoption.

Axle Type Insights

Solid axles dominate with about 54% share in 2025, primarily due to their proven reliability and high load-bearing capacity. Widely approved under AAR and other regulatory standards, they are extensively used in freight operations where durability and operational simplicity are critical. Their cost-effectiveness and long lifecycle make them ideal for high-volume, heavy-haul rail applications.

Hollow axles represent the fastest-growing category, gaining traction in high-speed rail systems. Their lighter weight contributes to improved energy efficiency and reduced track stress. As high-speed passenger networks expand globally, demand for lightweight yet strong axle solutions continues to rise.

Product Type Insights

Wheels in the 1000–1100 mm diameter range hold the leading market share in 2025, widely utilized in high-speed passenger trains and freight rolling stock. These wheels offer an optimal balance between speed capability and load-bearing performance. Precision-engineered alloys and advanced heat treatments enhance durability, making them suitable for modern rail networks with demanding operational conditions.

Wheels above 1100 mm are the fastest-growing segment, largely driven by increasing deployment in heavy locomotives and long-haul freight trains. Growing freight volumes and higher axle load requirements are encouraging the adoption of larger-diameter wheels for enhanced traction and stability.

End-user Insights

High-speed railway applications dominate the market with a roughly 44% share in 2025. Trains operating at speeds exceeding 300 km/h require high-performance wheels and axles capable of withstanding thermal stress, rotational forces, and dynamic loading. Large-scale high-speed rail expansions, particularly in Asia, continue to reinforce demand within this segment.

Subway systems are the fastest-growing end-use category, supported by rapid urbanization and expanding metro rail projects. Frequent acceleration and braking cycles increase replacement demand, while public investments in sustainable urban transport further strengthen long-term growth prospects.

Sales Channel Insights

OEM sales account for over 55% of the market share in 2025, driven by new rolling stock production and infrastructure expansion projects. Manufacturers collaborate closely with train builders to integrate wheel and axle systems during the design phase, ensuring compliance with technical and safety specifications.

The aftermarket segment is the fastest-growing sales channel, supported by rising fleet modernization programs and periodic wheelset replacements. Aging rail assets, safety inspections, and performance upgrades are generating consistent demand for replacement components worldwide.

Regional Insights

North America Rail Wheel and Axle Market Trends

North America represents a mature yet steadily expanding market, supported by freight rail dominance and ongoing passenger rail modernization. The region is projected to grow at a CAGR of approximately 6.8% between 2025 and 2032. The United States leads demand, driven by infrastructure initiatives such as the California High-Speed Rail project and freight capacity upgrades.

Strict Federal Railroad Administration (FRA) safety regulations ensure consistent replacement cycles and high-quality standards. Innovation remains strong, with companies investing in advanced metallurgy, composite materials research, and durability improvements to enhance lifecycle performance across freight and passenger applications.

Europe Rail Wheel and Axle Market Trends

Europe accounted for approximately 27% of the global market share in 2025 and represents the fastest-growing regional market through 2032. Growth is supported by cross-border railway harmonization under European Union Railway Agency (ERA) standards and substantial funding through Trans-European Transport Network (TEN-T) initiatives aimed at infrastructure modernization.

Countries such as Germany, France, the U.K., and Spain are upgrading high-speed and regional rail systems to improve efficiency and sustainability. Leading manufacturers continue investing in advanced wheel materials and lightweight technologies, strengthening Europe’s innovation-driven market expansion.

Asia Pacific Rail Wheel and Axle Market Trends

Asia Pacific holds the largest market share at approximately 39% in 2025, driven by extensive railway network expansion and strong domestic manufacturing capabilities. China dominates regional demand with its vast high-speed and freight rail infrastructure, while India strengthens supply through large-scale production facilities such as the Rail Wheel Factory. Japan continues to lead in high-speed rail precision engineering.

Ongoing metro rail expansion, freight corridor development, and government-backed infrastructure programs support sustained demand across the region. Emerging ASEAN economies are also investing in rail connectivity, benefiting from cost-competitive manufacturing and localization strategies that reinforce the Asia Pacific’s leadership position.

Competitive Landscape

The rail wheel and axle market exhibits moderate consolidation, with leading players leveraging vertical integration to strengthen their positions. Companies focus on expanding production capacities and optimizing supply chains to meet growing global demand while ensuring timely delivery and operational efficiency.

Innovation and differentiation are key competitive strategies, with investments in advanced materials, custom alloys, and lightweight designs enhancing product performance and durability. Emerging technologies, such as sensor-based predictive maintenance and condition monitoring, are being adopted to reduce lifecycle costs and improve safety. These initiatives help manufacturers stay ahead in an increasingly technology-driven and quality-conscious market.

Key Market Developments

- In March 2024, NSSMC announced a major investment in research and development for composite rail wheels, focusing on lightweight designs that enhance fuel efficiency, reduce track wear, and improve overall performance in high-speed and urban rail applications.

- In February 2024, OMK inaugurated a new production line for high-strength axles, increasing manufacturing capacity by 15%. The expansion aims to meet growing demand from freight and passenger rail networks, while ensuring compliance with stringent safety and durability standards.

- In January 2024, Bochumer Verein introduced an eco-friendly production process for rail wheels and axles, cutting energy consumption by 20%. The initiative emphasizes sustainability, cost efficiency, and lower environmental impact across manufacturing operations.

Companies Covered in Rail Wheel and Axle Market

- CAF USA, Inc.

- Bharat Forge Ltd. (Kalyani Group)

- Amsted Rail Company, Inc.

- ArcelorMittal A.S.

- Bonatrans Group A.S.

- Comsteel

- CRRC Sifang Co., Ltd.

- Kolowag AD

- Lucchini RS S.p.A.

- Nippon Steel & Sumitomo Metal Corporation

- Rail Wheel Factory – Indian Railways

- Maanshan Iron and Steel Company

- Semco India (P) Ltd.

- United Metallurgical Company, OMK CJSC

- Simmons Machine Tool Corporation (NSH Group)

Frequently Asked Questions

The rail wheel and axle market is expected to reach US$ 4.4 billion in 2026.

Expansion of high-speed railway networks, requiring high-performance wheels and axles, drives market growth.

Asia Pacific leads with approximately 39% share in 2025, supported by extensive railway infrastructure and domestic production.

Urban subway expansions present significant growth potential through increasing replacement and fleet modernization.

Leading players include CAF USA, Inc., Bharat Forge Ltd. (Kalyani Group), Amsted Rail Company, Inc., ArcelorMittal A.S., and Bonatrans Group A.S.