- Automotive Components & Materials

- High-Performance Wheels Market

High-Performance Wheels Market Size, Share, and Growth Forecast, 2026 - 2033

High-Performance Wheels Market by Material Type (Aluminum, Steel, Magnesium, and Carbon Fiber), Sales Channel Type (OEM and Aftermarket), Vehicle Type (Top End Luxury, Mid-Level Luxury, and Others), and Regional Analysis for 2026 - 2033

High-Performance Wheels Market Size and Trends Analysis

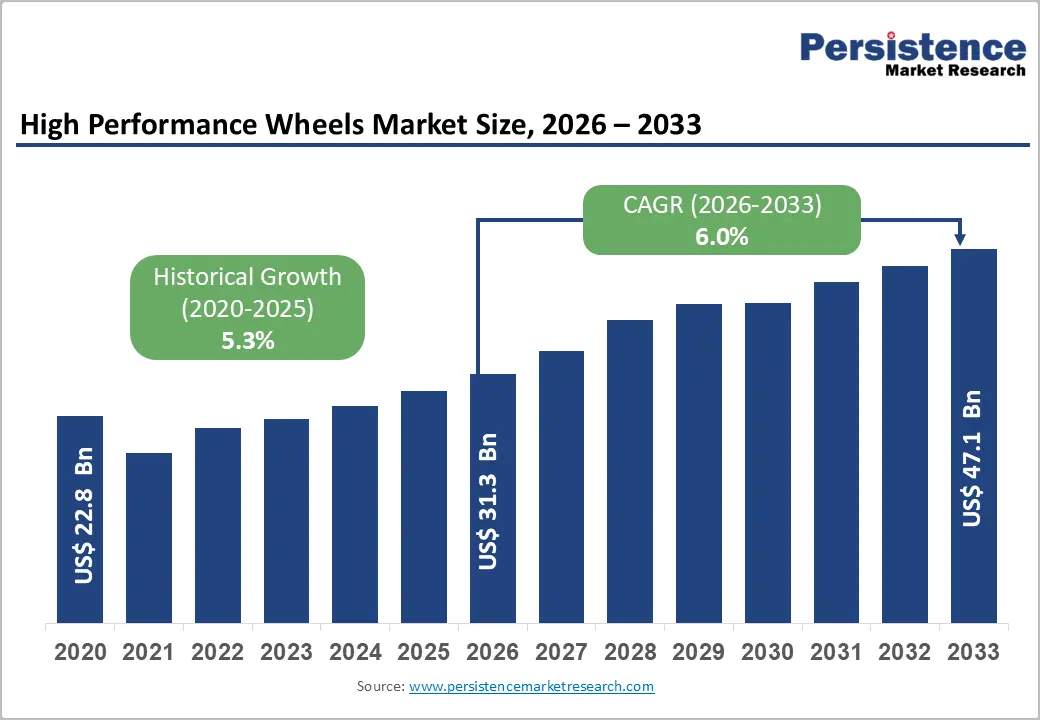

The global high-performance wheels market size is likely to be valued at US$ 31.3 billion in 2026 and is projected to reach US$ 47.1 billion by 2033, growing at a CAGR of 6.0% between 2026 and 2033. This growth builds on an already solid expansion from US$22.8 Bn in 2020. Demand is underpinned by rising sales of premium and performance vehicles, stringent fuel-economy and emissions regulations that favor lightweight wheel materials, and increasing consumer preference for aesthetics and customization in the aftermarket segment. The market is further shaped by advances in aluminum and magnesium alloy technologies and by the expanding adoption of mid- and top-end luxury vehicles.

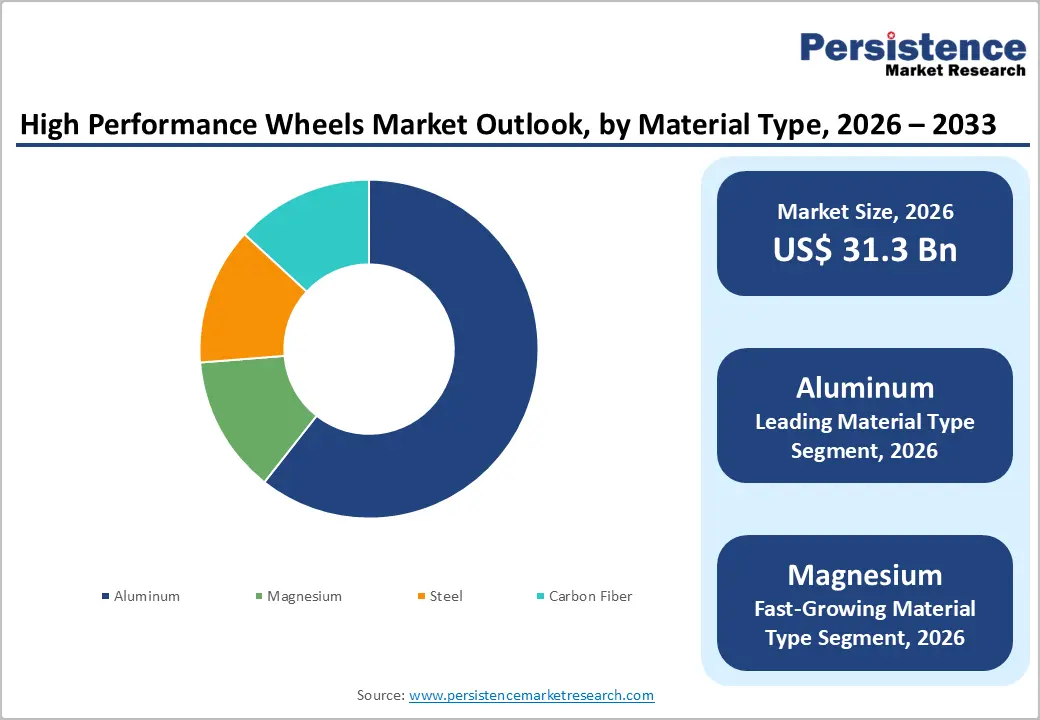

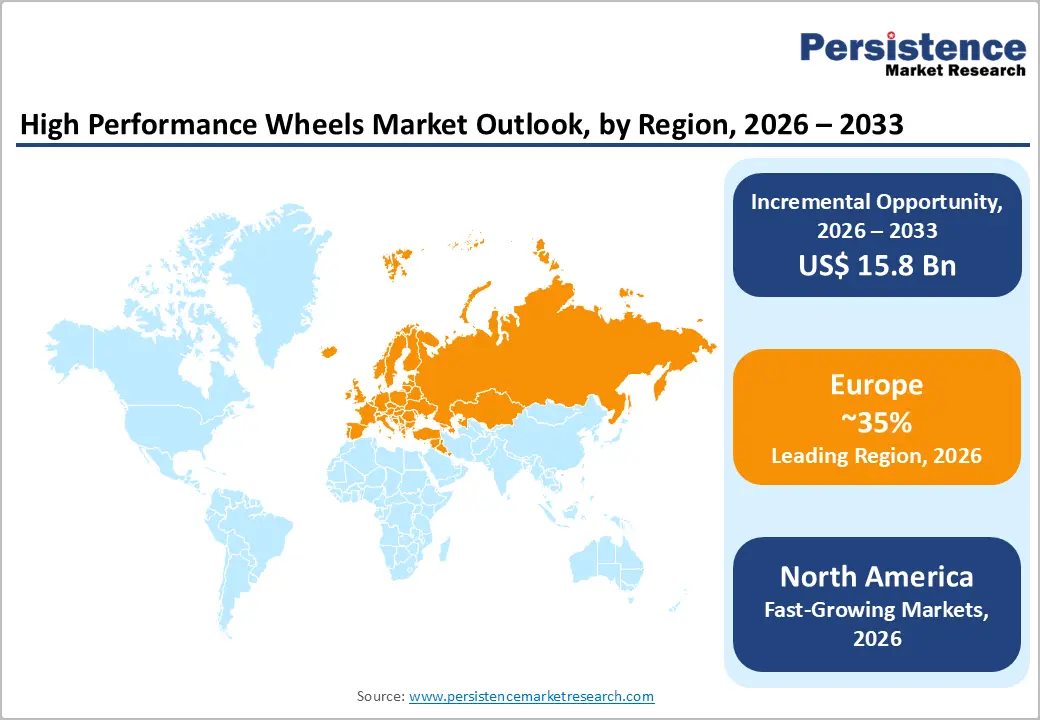

Between 2020 and 2026, the High-Performance Wheels market expanded at a robust pace, with a historical CAGR of 5.3%, reflecting steady upgrades from steel to alloy and composite wheels in both OEM and aftermarket applications. From 2026 to 2033, growth is projected to accelerate modestly to a 6.0% CAGR, driven by the adoption of lightweight materials, performance-focused consumer segments, and premiumization trends in passenger vehicles. Aluminum wheels account for over 60% of revenue, whereas aftermarket channels account for more than 65% of sales, indicating strong demand for replacement and customization. Regionally, Europe leads with a revenue share above 35%, while North America is the fastest-growing region at a 6.6% CAGR, reflecting a dynamic mix of regulatory pressures and consumer preferences.

Key Industr-Highlights:

- Material Type Analysis: Aluminum wheels account for over 60% of revenue, whereas magnesium is the fastest-growing material segment, with a CAGR of approximately 6.5%.

- Sales Channel Analysis: The aftermarket channel accounts for more than 65% of revenue, whereas OEM sales are expanding at a CAGR of approximately 6.7%.

- Vehicle Type Analysis: Mid-level luxury vehicles contribute more than 45% of revenue, whereas top-end luxury vehicles represent the fastest-growing vehicle type segment at roughly 6.9% CAGR.

- Regional Analysis: Europe leads regionally with above 35% global revenue share, while North America is the fastest-growing region at about 6.6% CAGR.

- Historically, the market grew at a 5.3% CAGR from 2020, supported by the shift from steel to alloy wheels and increasing penetration of premium vehicles.

- Post-2023 strategic developments focus on expanded capacity for lightweight alloys, composite- and hybrid-wheel R&D partnerships, and EV-optimized wheel launches, thereby reinforcing long-term growth prospects.

| Key Insights | Details |

|---|---|

|

High Performance Wheels Market Size (2026E) |

US$ 31.3 Bn |

|

Market Value Forecast (2033F) |

US$ 47.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

Market Dynamics

Drivers - Lightweighting and Emissions/Fuel Economy Regulations

Governmental and supranational regulations are a fundamental growth engine for high-performance wheels. The European Union’s CO fleet targets (e.g., 95 g CO/km and subsequent tightening under the Fit for 55 package) and the U.S. EPA/NHTSA Corporate Average Fuel Economy (CAFE) standards push OEMs to reduce vehicle curb weight to meet emissions and efficiency benchmarks. Lightweight, high-performance wheels made from aluminum and magnesium alloys can reduce unsprung mass and rotational inertia, thereby improving fuel economy and electric vehicle (EV) range. Industry analyses of automotive wheels show global wheel markets growing in the mid-single digits, with lightweight materials gaining share as OEMs optimize total cost of compliance with emissions rules while preserving driving dynamics and safety. As a result, high-performance wheel adoption continues to expand across mid-level and premium segments.

Restraint - Regulatory and Quality Assurance Challenges

While regulations encourage lightweighting, they also impose stringent safety, durability, and homologation standards. High-performance wheels must comply with regional standards such as UNECE regulations in Europe, Federal Motor Vehicle Safety Standards (FMVSS) in the U.S., and equivalent national regulations in the Asia-Pacific region, which require extensive testing for impact resistance, fatigue, corrosion, and environmental exposure. Certification and testing raise time-to-market and increase development costs, particularly for smaller manufacturers and new entrants. Failure to meet standards can lead to recalls, liability risks, and reputational damage, creating a structural barrier to innovation and competition.

Opportunity - Technological Convergence in Materials and Manufacturing

Advances in aluminum alloys, magnesium forming, and emerging carbon fiber wheel technologies open new performance–cost trade-off spaces. Innovations in heat treatment, surface coating, and hybrid wheel architectures (e.g., aluminum rims with composite inserts) help improve durability while lowering weight. Industry research indicates that carbon fiber wheels in the broader automotive wheel market are growing at double-digit CAGRs from a small base, as early adopters in performance and luxury segments validate their benefits. At the manufacturing scale, costs are expected to decline, enabling broader adoption of mid-level luxury and premium SUVs. Suppliers that invest in R&D and strategic technology partnerships can capture an early mover advantage in these high-value subsegments.

Category-wise Analysis

Material Type Insights

Aluminum currently represents the dominant material type in the global high-performance wheels market, accounting for more than 60% of total revenue. Its leadership is driven by an optimal balance of lightweight performance, cost efficiency, and large-scale manufacturability. Aluminum alloys are compatible with multiple production technologies, including casting, flow forming, and forging, enabling manufacturers to meet a wide range of OEM and aftermarket requirements. Beyond performance benefits, aluminum wheels are widely favored for their design flexibility and aesthetic appeal, making them a preferred choice across passenger cars, performance vehicles, and premium segments. Additionally, tightening fuel-efficiency and emission regulations in regions such as Europe and North America continue to accelerate OEM substitution of traditional steel wheels with lighter aluminum alternatives.

Magnesium, while currently holding a smaller market share, represents the fastest-growing material segment, projected to expand at a CAGR of approximately 6.5% from 2026 to 2033. Magnesium wheels offer greater weight reduction than aluminum, thereby improving handling and performance in high-end applications. Although higher costs and durability concerns have constrained adoption, ongoing advancements in manufacturing processes and protective coatings are improving corrosion resistance and fatigue life. These developments are expected to drive increased penetration in luxury vehicles, high-performance SUVs, and specialized aftermarket segments. Steel and carbon fiber remain niche materials, serving cost-sensitive and ultra-premium markets, respectively.

Sales Channel Insights

By sales channel, the aftermarket clearly dominates the high-performance wheels market, accounting for more than 65% of total revenue. This leadership is driven by frequent replacement cycles, upgrades from OEM-fitted wheels, and strong vehicle customization trends. Car owners increasingly prioritize visual appeal and performance enhancements, opting for larger wheel diameters, lightweight alloys, and performance-oriented wheel–tire packages. Specialist retailers, performance garages, and rapidly expanding e-commerce platforms have made aftermarket options more accessible, while the wide availability of brands, finishes, and price tiers enables differentiation across vehicle segments, from mass-market cars to premium and performance models.

In contrast, the OEM channel is the fastest-growing channel, projected to grow at a CAGR of approximately 6.7% from 2026 to 2033. Growth is supported by OEMs' increasing provision of high-performance wheels as standard or optional equipment on mid-range vehicles, luxury models, sports trims, and electric vehicles. By bundling performance wheels into appearance, handling, and efficiency packages, manufacturers are shifting incremental value from aftermarket upgrades to factory fitments, particularly in Europe and North America. Additionally, the OEM channel serves as a critical validation platform for advanced materials and designs, such as magnesium and composite wheels, which subsequently gain wider acceptance in the aftermarket.

Vehicle Type Insights

The vehicle type segmentation highlights the dominance of mid-level luxury vehicles, which account for more than 45% of total revenue. This segment includes premium sedans, crossovers, and SUVs that balance performance and affordability, making them attractive to a wide consumer base. Alloy wheels are increasingly offered as standard equipment in these vehicles, reinforcing consistent OEM demand. In addition, a rising middle class and a growing preference for feature-rich vehicles support aftermarket replacement and customization activities, further strengthening revenue from this category.

Top-end luxury vehicles represent the fastest-growing vehicle type segment, expanding at an estimated CAGR of 6.9% during 2026–2033. This segment comprises high-end sedans, luxury SUVs, and sports cars, where buyers place strong emphasis on performance, aesthetics, and brand differentiation. Consequently, advanced wheel materials such as forged aluminum, magnesium, and selective carbon fiber solutions are gaining rapid adoption. Higher vehicle transaction values in this segment enable OEMs and aftermarket suppliers to introduce technologically sophisticated, premium-priced wheel offerings with attractive margins.

Regional Insights

Europe Dominates High-Performance Wheel Demand Through Premium OEM Strength And Regulation

Europe represents the largest regional market for high-performance wheels, accounting for over 35% of global revenue. The region’s leadership is anchored in its strong premium OEM ecosystem, led by Germany, with manufacturers including BMW, Mercedes-Benz, Audi, and Porsche. The U.K., supported by Jaguar Land Rover and several niche sports-car brands, along with France, Italy, and Spain, further strengthens regional demand. Across Europe, alloy and high-performance wheels are widely adopted across mid-range premium and top-end luxury vehicles, reflecting consumer preferences for superior handling, driving dynamics, and distinctive design.

Market growth is reinforced by stringent EU fleet CO targets, Euro 6 and upcoming Euro 7 emission norms, and broader decarbonization objectives that emphasize lightweighting and vehicle efficiency. Harmonized regulatory frameworks under UNECE standards simplify cross-border vehicle and component approvals, supporting scale and innovation. Germany serves as the central hub for performance wheel engineering and premium OEM procurement, while the U.K., France, Italy, and Spain contribute through localized OEM production and active aftermarket channels. Competition remains intense, with multinational suppliers and specialized premium brands focusing on advanced forging technologies, weight reduction, sustainable materials such as high-recycled-content aluminum, and deeper integration with OEM design cycles and emerging EV platforms.

North America Drives Rapid Growth Through Performance Vehicles, Regulations, And Innovation Ecosystem

North America represents the fastest-growing regional market, projected to expand at a CAGR of approximately 6.6% between 2026 and 2033. Growth is supported by a large, affluent consumer base with strong preferences for performance and luxury vehicles, as well as a deeply rooted automotive enthusiast culture. The United States dominates regional revenue, driven by high ownership of pickup trucks, performance-oriented SUVs, and sports cars, many of which are equipped with premium alloy and forged wheels. Canada and Mexico further strengthen regional demand through established OEM manufacturing hubs and expanding vehicle customization and aftermarket communities.

Regulatory pressure is a major catalyst for market expansion. Stringent Corporate Average Fuel Economy (CAFE) and greenhouse gas emission standards enforced by U.S. authorities are compelling OEMs to adopt lightweight components, including high-performance wheels, to improve fuel efficiency without compromising performance. This has accelerated innovation in advanced aluminum alloys, magnesium wheels, and forged wheel technologies.

North America also benefits from a robust innovation ecosystem comprising wheel manufacturers, specialty forgers, and materials suppliers, enabling rapid product development and customization. Safety and durability regulations, including FMVSS compliance, heavily influence design, testing, and certification processes. Competitive intensity remains high, with global brands and regional specialists actively competing in the aftermarket. Investment activity increasingly focuses on expanding distribution networks, strengthening digital sales platforms, and forming partnerships with tuning shops and performance vehicle programs.

Competitive Landscape

The global High Performance Wheels market is moderately consolidated, characterized by the presence of large multinational wheel manufacturers alongside specialized premium and performance-focused brands. In the broader automotive wheel industry, established players such as Borbet, CITIC Dicastal, Enkei, Iochpe-Maxion, and TOPY collectively account for roughly one-quarter of total global wheel demand. However, within the high performance wheels segment, value capture is disproportionately higher for premium manufacturers that specialize in forged, lightweight, and motorsport-inspired wheel solutions. These companies benefit from higher margins driven by advanced engineering, material innovation, and strong brand recognition in both OEM-supplied and aftermarket performance applications.

Competitive positioning in this segment is primarily influenced by technological expertise in materials such as aluminum alloys, magnesium, and advanced composites, as well as long-standing OEM relationships and diversified regional manufacturing footprints. Brand equity within the enthusiast and performance aftermarket further strengthens market differentiation.

Post-2023, strategic investments have intensified. In 2024, several leading aluminum wheel manufacturers announced capacity expansions across Europe and Asia to support rising demand from premium internal combustion and electric vehicle programs. These expansions include new casting facilities, flow-forming technologies, and advanced surface treatment lines, improving supply reliability, shortening lead times, and reinforcing a strategic shift toward lightweight, high-value wheel offerings.

Key Developments:

- IndyCar is evaluating a shift from traditional magnesium wheels to aluminium alternatives by 2026 or 2027. The move is aimed at reducing costs and mitigating supply-chain constraints, as magnesium wheel sourcing has become increasingly limited despite its long-standing use in high-performance motorsport.

- Maxion Wheels has confirmed readiness to commence series production of forged aluminium truck wheels in January 2026. Announced at the SOLUTRANS 2025 exhibition in Lyon, production will take place at a newly built 24,500-square-metre facility in Manisa, Türkiye, developed through a joint venture with nci Holding. The fully operational plant has an initial annual capacity of approximately 350,000 wheels, with scalability to meet future demand.

- In December 2025, Steel Strips Wheels Limited announced a 420 crore investment to expand operations in Gujarat. The company plans to lease nearly 288,800 square meters to establish new manufacturing units for alloy wheels and aluminium steering knuckles, with completion targeted for Q4 FY2026–27.

- MAK expanded its 2025 alloy wheel lineup with seven new designs, including Monza, Stark, Chelsea, Asphalt, and Qvarz, tailored for Alfa Romeo, Audi, Mini, and Volkswagen vehicles. Additional launches include APX for sports models and NOMAD for heavy-duty and off-road applications.

Companies Covered in High-Performance Wheels Market

- CITIC Dicastal Co., Ltd.

- BORBET GmbH

- Enkei Corporation

- Iochpe-Maxion S.A.

- TOPY Industries, Ltd.

- RAYS Co., Ltd.

- BBS Kraftfahrzeugtechnik AG

- Accuride Corporation

- Maxion Wheels

- Vossen Wheels

- HRE Performance Wheels

- OZ Group

- Forgeline Motorsports

- Alcoa Wheels

- Other Market Players

Frequently Asked Questions

The High-Performance Wheels market is estimated to be valued at US$ 31.3 Bn in 2026.

The key demand driver for the High Performance Wheels market is the automotive industry’s structural shift toward vehicle lightweighting and performance optimization, particularly in premium, sports, and electric vehicles (EVs).

In 2026, the Asia Pacific region will dominate the market with an exceeding 75% revenue share in the global High Performance Wheels market.

Among vehicle types, Mid-Level Luxury has the highest preference, capturing beyond 35% of the market revenue share in 2026, surpassing other vehicle types.

CITIC Dicastal Co., Ltd., BORBET GmbH, Enkei Corporation, Iochpe-Maxion S.A., TOPY Industries, Ltd.,and RAYS Co., Ltd. There are a few leading players in the High Performance Wheels market.