- Animal Health

- Veterinary Therapeutic Diet Market

Veterinary Therapeutic Diet Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Veterinary Therapeutic Diet Market by Animal Type (Dogs, Cats, Others), Product Form (Dry Food, Wet/Canned Food, Semi-Moist Food, Treats and Supplements), Diet Type (Weight Management Diets, Renal / Kidney Support Diets, Gastrointestinal Health Diets, Diabetic Management Diets, Joint & Mobility Support Diets, Skin & Coat Health Diets, Dental Health Diets, Others), Distribution Channel (Veterinary Clinics & Hospitals, Pet Specialty Stores, Online Retail / E-commerce Platforms, Retail Pharmacies, Supermarkets & Hypermarkets, Others), and Regional Analysis from 2026 to 2033

Veterinary Therapeutic Diet Market Share and Trends Analysis

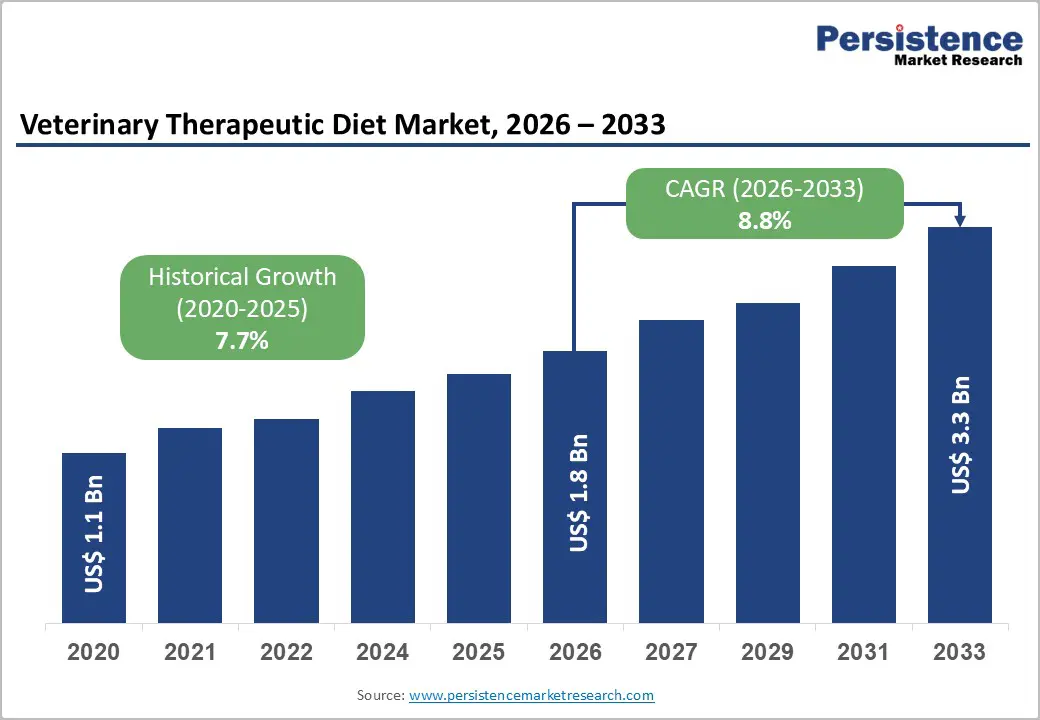

The global veterinary therapeutic diet market is estimated to grow from US$ 1.8 Bn in 2026 to US$ 3.3 Bn by 2033. The market is projected to record a CAGR of 8.8% during the forecast period from 2026 to 2033.

The global veterinary therapeutic diet market is experiencing steady growth, driven by rising pet humanization, increasing prevalence of chronic conditions such as obesity and renal disorders, and growing veterinarian recommendations for prescription nutrition. Expanding premium pet food adoption and e-commerce penetration further support demand. North America leads, while Asia-Pacific grows rapidly due to rising pet ownership.

Key Industry Highlights

- Dominant Segment: Renal & Kidney Support Diets account for 21.5% share of the veterinary therapeutic diet market in 2025, driven by the rising prevalence of chronic kidney disease in aging pets. Increasing veterinary prescriptions, clinically proven formulations, and growing awareness among pet owners regarding therapeutic nutrition contribute to sustained segment dominance globally.

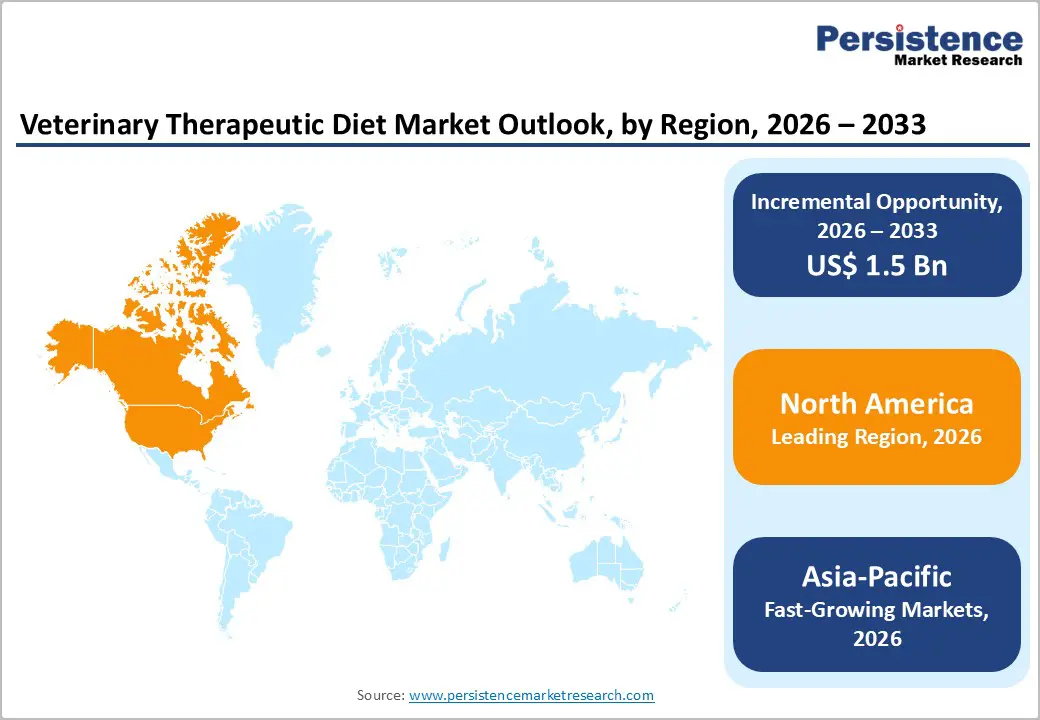

- Dominant Region: North America leads the veterinary therapeutic diet market in 2025 with 40.8% share, supported by high pet ownership rates, strong veterinary infrastructure, widespread adoption of prescription diets, and presence of major players. Meanwhile, Asia-Pacific remains the fastest-growing region, driven by rising disposable income, increasing pet humanization, and expanding veterinary services.

- Market Drivers: Rising pet humanization, increasing prevalence of chronic conditions such as obesity, diabetes, renal and gastrointestinal disorders, growing veterinarian recommendations for prescription diets, expanding pet insurance coverage, and premiumization trends in pet nutrition are key factors driving market growth.

- Market Opportunity: Opportunities include development of condition-specific and breed-specific therapeutic formulations, expansion through e-commerce and direct-to-consumer channels, increasing demand in emerging markets, innovation in functional ingredients and palatability enhancement, and strategic collaborations with veterinary clinics and pet care providers.

| Global Market Attributes | Key Insights |

|---|---|

| Global Veterinary Therapeutic Diet Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 3.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.7% |

Market Dynamics

Driver: Growing Pet Humanization and Owner Spending on Premium Nutrition

Pet humanization, where owners increasingly see pets as family members, is a significant driver for the Veterinary Therapeutic Diet Market. In the U.S., 70% of households own a pet, and pet-related spending continues to grow, with total industry expenditures projected at $157 billion in 2025. Pet food and treats alone accounted for about $67.8 billion, showing continued prioritization of nutrition. Moreover, 81% of U.S. pet owners who purchased premium pet food did so online, and 76% are willing to pay more for human-grade ingredients, reflecting deeper investment in higher-quality diets beyond basic food.

This driver directly translates into demand for therapeutic diets that address health conditions. Pet owners increasingly opt for specialized, nutrient-rich formulations that promise better health outcomes, particularly for chronic conditions common in aging pets. The trend toward premium nutrition is supported by data showing annual per-pet spending exceeding $1,500 in the U.S. and a notable rise in owners prioritizing pet health over other expenses. As owners perceive nutrition as preventative healthcare, veterinarians’ recommendations for therapeutic diets gain more traction, further boosting market adoption of condition-specific veterinary diets.

Restraints: High Cost of Veterinary Therapeutic Diets Limiting Affordability

The high cost of veterinary therapeutic diets presents a notable restraint on market growth. Specialized diets formulated for clinical conditions often come at a premium compared to standard pet food due to the additional research, specialized ingredients, and controlled manufacturing processes required. Estimates suggest that veterinary prescription diets can cost two to three times more than regular premium commercial foods, making them less affordable for many pet owners, especially those with limited disposable income.

As a result, cost sensitivity can reduce long-term compliance with veterinary diet recommendations. With inconsistent pet insurance coverage for nutritional therapy many plans exclude prescription diets owners may avoid or discontinue these diets due to expense. This is especially impactful in economically volatile periods or lower-income demographics, where the perceived benefit of therapeutic diets may not outweigh their higher cost. Overall, the cost barrier slows broader adoption, limiting the market’s penetration, particularly in price-sensitive regions and among first-time pet owners.

Opportunity: Development of Breed-Specific and Condition-Specific Therapeutic Formulations

Developing breed-specific and condition-specific therapeutic diets represents a key opportunity. As pets age and as chronic conditions such as obesity, renal disease, diabetes, and gastrointestinal disorders become more prevalent, owners seek nutrition tailored to individual health needs. For example, dog obesity rates have increased significantly over the last decade, driving demand for weight management formulas. Breed-specific therapeutic nutrition can also address differing metabolic needs between small and large breeds or predispositions to certain conditions, enhancing effectiveness and owner satisfaction.

Additionally, targeted diets for conditions like joint support, skin health, and urinary tract health enable differentiation in a competitive market. As awareness grows around the importance of nutrition in preventive healthcare, veterinarians increasingly support customized dietary interventions, and owners are willing to pay a premium for solutions that promise measurable health benefits. This opens avenues for product innovation, premium positioning, and strategic partnerships with veterinary clinics and specialists to educate owners about the value of tailored therapeutic nutrition.

Category-wise Analysis

By Animal Type, Dogs Dominates the Veterinary Therapeutic Diet Market

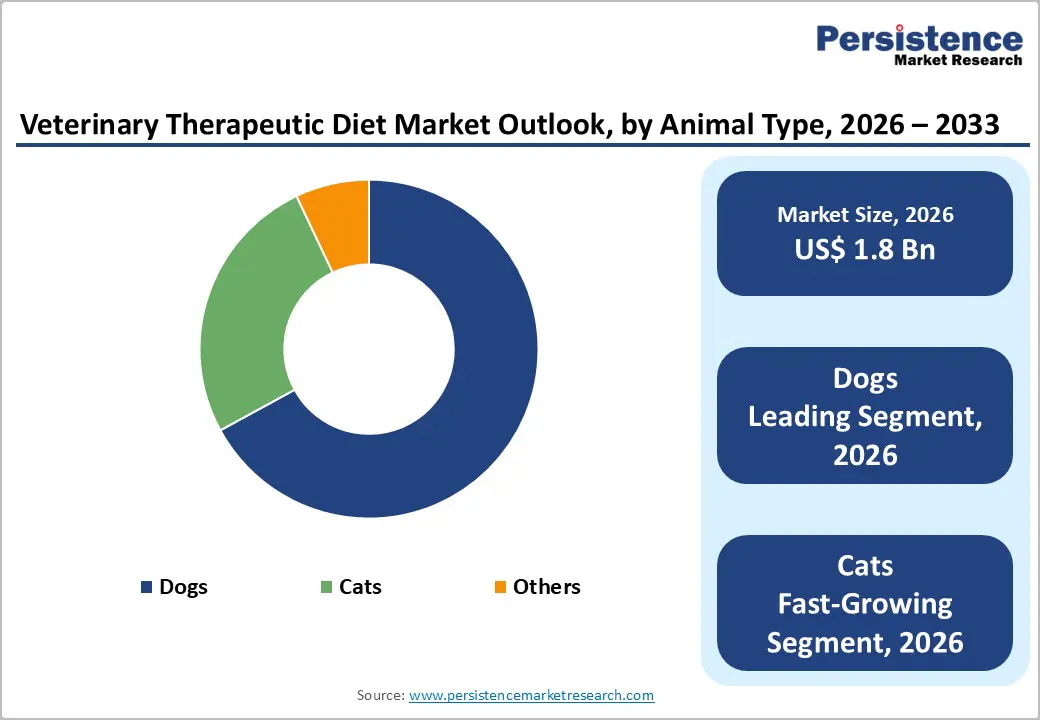

Dogs occupies 67.0% share of the global market in 2025, because they are the most commonly owned companion animal in major pet-care regions such as the U.S. According to U.S. household surveys, about 67% of households own a pet and dogs remain the most prevalent, with roughly 67% of U.S. households owning a dog, compared with lower percentages for other pets. Dogs also represent a larger share of pet food expenditure; dog food accounts for the largest segment of U.S. pet food sales, significantly outpacing other categories. These high ownership and expenditure patterns naturally translate into greater demand for condition-specific and clinical diets tailored to canine health needs, making dogs the dominant animal type for veterinary therapeutic nutrition.

Additionally, dogs typically have longer life spans and higher rates of chronic health conditions that benefit from therapeutic nutrition, such as obesity, joint disorders, and renal issues. With more frequent veterinary visits and preventive care regimens that often include diet modifications, therapeutic diets for dogs are prescribed more often than for other animals. This combination of ownership prevalence and higher clinical diet adoption underpins why dogs hold the largest share in the veterinary therapeutic diet market worldwide.

By Product Form, Dry Food dominates due to convenience and effectiveness

Dry food dominates the veterinary therapeutic diet market primarily due to its convenience, cost-effectiveness, and widespread acceptance among pet owners. In the U.S., surveys show that dry kibble is the most commonly fed food type, with around 61% of dogs eating dry food and a similarly strong preference among pet owners overall. Dry food’s longer shelf life, easier storage, lower production cost per calorie, and suitability for a broad range of clinical formulations make it the default choice for many therapeutic diets. These characteristics are especially valuable in therapeutic contexts, where controlled nutrient delivery and consistent dosing are essential.

Furthermore, industry feeding patterns indicate that dry food accounts for the largest share of overall pet food revenue globally - for example, dry pet food holds approximately 55-56% of total pet food sales, underscoring its broad market penetration. Veterinarians often recommend dry therapeutic diets for conditions such as weight management, renal support, and dental health, where kibble formats can be engineered for specific nutrient profiles, texture, and caloric content. These factors, supported by consumer habits favoring dry food for ease and economics, explain why dry therapeutic diets remain the dominant product form in the market.

Regional Insights

North America Veterinary Therapeutic Diet Market Trends

North America dominates the veterinary therapeutic diet market with 40.8% share because of very high pet ownership and spending on pet health. In the U.S., about 66-67% of households own a pet, with millions of dogs and cats, and annual pet food expenditure exceeding $65 billion. Pet spending overall reached over $150 billion in recent years, reflecting strong consumer investment in premium, health-oriented nutrition.

The region also has an advanced veterinary healthcare infrastructure that supports frequent diagnosis and management of chronic conditions, making veterinarians more likely to recommend therapeutic diets. With well-developed retail and e-commerce channels, specialized diets are widely accessible, reinforcing North America’s leadership in the global market.

Europe Veterinary Therapeutic Diet Market Trends

Europe stands as a key region for veterinary therapeutic diets due to its high pet population and mature nutritional awareness. Countries such as Germany, the U.K., and France together house millions of dogs and cats, creating a substantial consumer base for specialized diets. Pet food expenditures are significant, with Europe accounting for nearly 28-30% of the global pet food market, underpinned by strong interest in premium, natural, and functional pet nutrition.

The region benefits from well-established veterinary care systems and regulatory frameworks that emphasize safety and quality, encouraging adoption of diet-based management for chronic conditions. With growing owner awareness of preventive health and prescription nutrition, Europe remains a robust and influential market for therapeutic diets.

Asia-Pacific Veterinary Therapeutic Diet Market Trends

The Asia-Pacific region is the fastest-growing market for veterinary therapeutic diets because of rapid increases in pet ownership, urbanization, and disposable income, especially in countries like China, India, and South Korea. Urban pet populations are rising quickly, and a growing middle class is increasingly willing to spend on premium pet care, including specialized nutrition.

While starting from a smaller base than North America or Europe, commercial pet food adoption is expanding, and awareness of pet health and preventive care is increasing. The region’s expanding retail networks and veterinary services, coupled with strong online sales growth, translate into faster market growth rates for therapeutic diets than in more mature regions. This combination of economic and demographic trends fuels Asia-Pacific’s leading growth trajectory.

Market Competitive Landscape

The veterinary therapeutic diet market is highly competitive, dominated by key players such as Hill’s Pet Nutrition, Royal Canin, Purina Pro Plan, and Mars Veterinary Health. Companies compete through product innovation, breed- and condition-specific formulations, premium positioning, and strategic veterinary partnerships, driving global adoption and market expansion across regions.

Key Industry Developments:

- In May 2025, Nestlé announced that it had strengthened its pet nutrition innovation strategy by increasing its focus on biotechnology and therapeutic solutions. The company stated that it was expanding research capabilities to develop advanced nutritional products aimed at supporting pet health through science-based formulations and precision nutrition.

- In April 2025, Rayne Nutrition announced the relaunch of its Skin Relief Dry Dog Food, formulated to support dogs suffering from atopic dermatitis and food sensitivities. The updated product was designed to provide targeted nutritional support through carefully selected, limited ingredients that help manage adverse food reactions and chronic skin inflammation.

Companies Covered in Veterinary Therapeutic Diet Market

- Rayne Clinical Nutrition

- Nestlé Purina PetCare

- Iams Veterinary Formula

- Diamond Pet Foods

- Royal Canin

- Mars Veterinary Health

- Blue Buffalo Company

- Purina Pro Plan Veterinary Diets

- Hill's Pet Nutrition, Inc.

- Eukanuba Veterinary Diets

- Others

Frequently Asked Questions

The global veterinary therapeutic diet market is projected to be valued at US$ 1.8 Bn in 2026.

Rising pet humanization, chronic conditions, veterinary recommendations, premium nutrition adoption, and growing e-commerce accessibility drive growth.

The global veterinary therapeutic diet market is poised to witness a CAGR of 8.8% between 2026 and 2033.

Developing breed- and condition-specific diets, expanding emerging markets, functional ingredients, premium products, and veterinary collaborations.

Rayne Clinical Nutrition, Nestlé Purina PetCare, Iams Veterinary Formula, Diamond Pet Foods, Royal Canin, Mars Veterinary Health.