- Specialty & Fine Chemicals

- Transformer Oil Market

Transformer Oil Market Size, Share, and Growth Forecast 2026 – 2033

Transformer Oil Market by Oil Type (Mineral Oil [Naphthenic Oil, Paraffinic Oil], Silicone Oil, Bio-based Oil), Application (Transformers [Power Transformer, Distribution Transformer], Switchgear, Reactors), End-user (Transmission & Distribution, Power Generation, Railways & Metros, Others), and Regional Analysis for 2026–2033

Transformer Oil Market Size and Trend Analysis

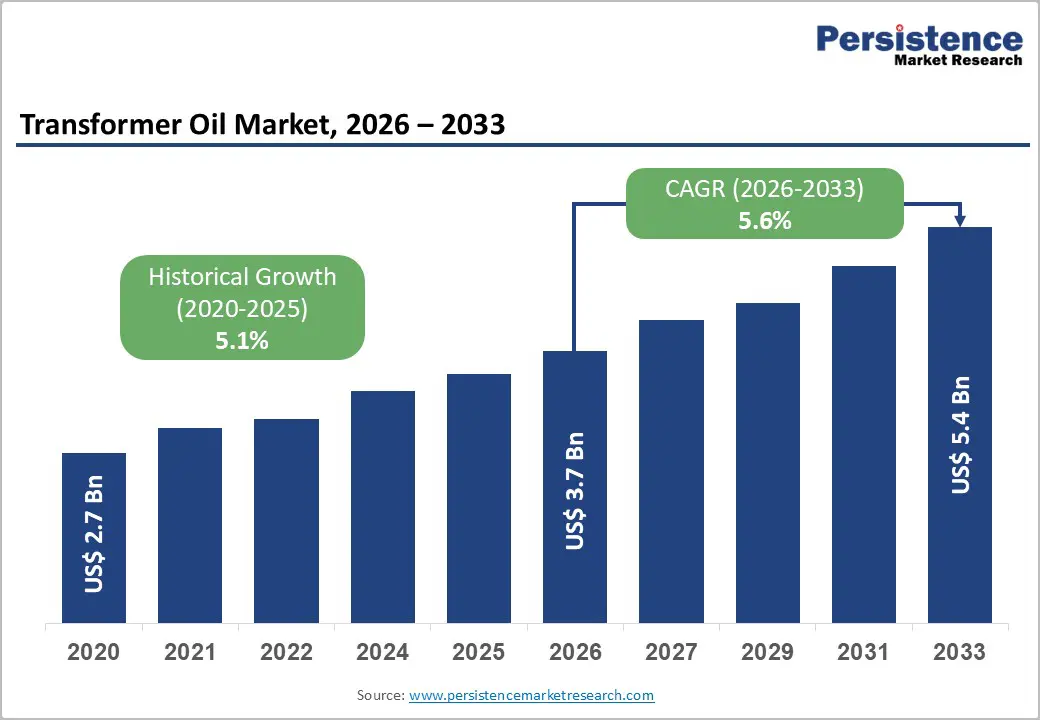

The global transformer oil market size is estimated to be valued at US$ 3.6 Bn in 2026 and is projected to reach US$ 5.4 Bn by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The sustained growth of the transformer oil market is primarily fueled by accelerating investments in power infrastructure modernization and grid expansion programs across both developed and emerging economies. Aging transformer fleets in North America and Europe, combined with large-scale electrification drives in the Asia Pacific and the Middle East, are generating robust replacement and new installation demand. Additionally, the rapid integration of renewable energy sources such as wind and solar into national grids requires additional transformer capacity, further expanding consumption of high-performance transformer oils.

Key Industry Highlights:

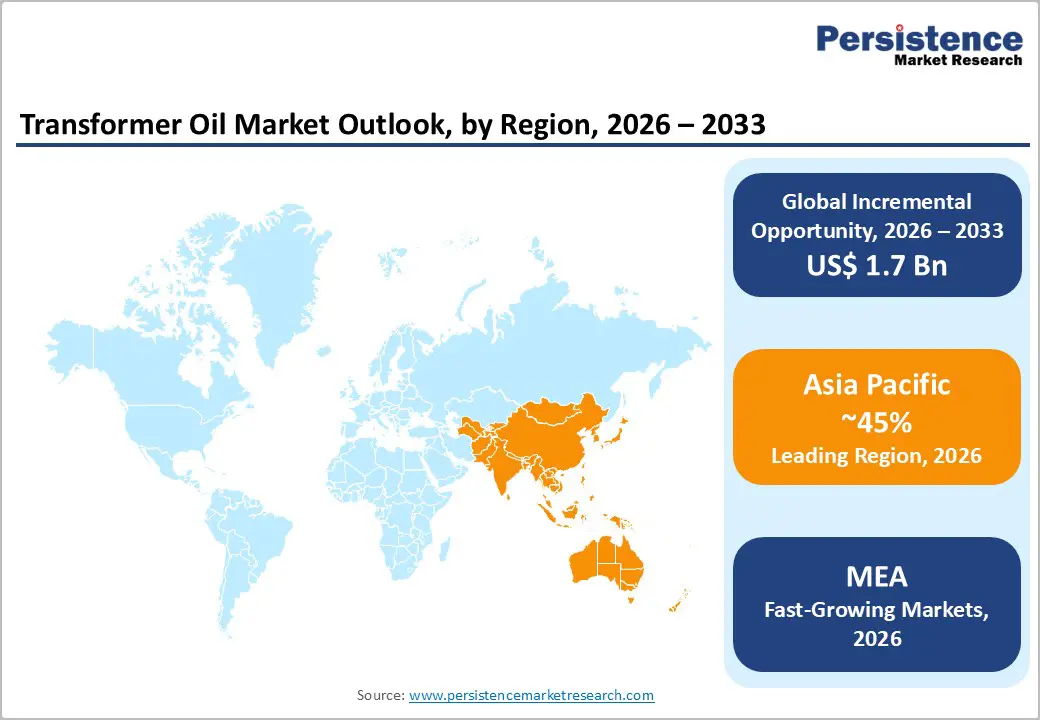

- Leading Region – Asia Pacific dominates the global transformer oil market, accounting for over 45% of consumption, driven by China's State Grid investments and India's large-scale electrification programs under the RDSS and National Electricity Plan.

- Fastest Growing Region – The Middle East & Africa region is projected to record the highest CAGR through 2033, fueled by massive grid infrastructure buildout in the GCC and electrification drives across Sub-Saharan Africa backed by World Bank and African Development Bank financing.

- Dominant Oil Type – Mineral oil commands approximately 72% of market share by oil type, anchored by naphthenic oil's superior low-temperature and oxidation performance, cost advantage, and entrenched adoption across power and distribution transformer applications globally.

- Fast-Growing Oil Type– Bio-based transformer oils are the fastest growing segment, benefiting from sustainability mandates, EU regulatory push, and utility environmental commitments. Natural ester oils such as Cargill's ENVIROTEMP FR3 are gaining rapid adoption across urban and high-risk installation environments.

- Key Opportunity – Global railway and metro electrification programs, including India's 100% rail electrification target and EU rail corridor upgrades, represent a growing demand channel for specialized transformer oils used in traction substations and metro power systems.

DRO Analysis

Drivers - Global Grid Expansion and Power Infrastructure Investments

One of the foremost drivers of the transformer oil market is the unprecedented surge in electricity grid investments worldwide. According to the International Energy Agency (IEA), global spending on electricity networks surpassed US$ 300 Bn in 2023, with grid infrastructure, including transformers, constituting a substantial share.

Governments in the Asia Pacific, particularly India and China, are channelling billions into transmission and distribution networks under flagship initiatives such as India's Revamped Distribution Sector Scheme (RDSS), which has a total outlay of over US$ 37 Bn. As transformers are central to power transmission infrastructure, this investment directly amplifies demand for transformer oil as both a dielectric insulator and a cooling medium, driving consistent volume growth across all transformer categories.

Rising Renewable Energy Integration Driving Transformer Deployments

The rapid global buildout of renewable energy capacity is structurally expanding transformer oil demand. The International Renewable Energy Agency (IRENA) reported that global renewable energy capacity additions reached a record 295 GW in 2022, with solar and wind dominating. Each new solar park, onshore wind farm, or offshore wind installation requires dedicated step-up and grid-connection transformers, each filled with several thousand litres of transformer oil.

Offshore wind installations in particular demand high-performance, fire-resistant transformer oils due to challenging environmental conditions. The European Union's target to install 600 GW of renewable capacity by 2030 under the Repower EU plan alone is expected to create sustained transformer procurement cycles, directly catalysing transformer oil consumption throughout the forecast period.

Restraints - Volatility in Crude Oil Prices Affecting Mineral Oil Margins

Mineral transformer oils, derived from naphthenic and paraffinic crude fractions, are highly susceptible to crude oil price fluctuations. The U.S. Energy Information Administration (EIA) recorded average crude oil prices swinging between US$ 40 and US$ 120 per barrel over 2020–2022.

Such volatility introduces significant margin pressure for transformer oil manufacturers, limiting their ability to offer stable long-term supply contracts to utilities and transformer OEMs. This unpredictability also complicates procurement planning for large infrastructure projects, potentially slowing order commitments and hampering steady market growth.

Environmental Regulations and PCB Disposal Challenges

Stringent environmental regulations governing the disposal of used transformer oils, particularly those historically contaminated with polychlorinated biphenyls (PCBs)pose a persistent restraint on market participants. Under the Stockholm Convention, over 180 countries are obligated to phase out and properly dispose of PCB-containing equipment by 2028.

Compliance with such regulations adds substantial remediation costs for utilities managing aging transformer fleets. Additionally, increasingly strict REACH and EPA guidelines for used oil disposal limit operational flexibility and increase lifecycle costs, indirectly constraining market expansion in regions with aging infrastructure.

Opportunities - Surge in Bio-based Transformer Oils Amid Sustainability Mandates

Bio-based transformer oils derived from natural esters such as soybean, rapeseed, and sunflower oils represent a compelling high-growth opportunity as utilities increasingly seek environmentally responsible alternatives to mineral oil. Bio-based fluids offer superior biodegradability, higher fire points (above 300°C), and improved moisture tolerance, making them particularly suited for urban and environmentally sensitive installations.

The U.S. Department of Agriculture (USDA) has been actively promoting bio-based product adoption through its BioPreferred Program. Major utilities in the United States and Europe are piloting natural ester-filled distribution transformers at scale.

Electrification of Railways and Urban Transit Systems

The electrification of railway networks and urban metro systems globally is emerging as a high-potential end-use opportunity for transformer oil suppliers. According to the International Union of Railways (UIC), rail transport accounts for only 2% of global transport energy consumption while delivering 8% of passenger and freight movement, underpinning strong government interest in further electrification.

India's National Rail Plan targets 100% railway electrification, while the European Commission is funding major rail corridor upgrades across member states. Each railway substation requires multiple traction transformers, which are typically oil-immersed and demand specialized transformer oils with high thermal stability.

Category-wise Analysis

Oil Type Insights

Mineral oil dominates the transformer oil market by oil type, commanding approximately 72% of the total market share. Within the mineral oil segment, naphthenic oil leads over paraffinic variants owing to its superior low-temperature performance, lower pour point, and better oxidation resistance characteristics critical for transformer insulation and cooling efficiency.

Naphthenic oils exhibit pours points as low as −40°C, making them the preferred choice for utilities in cold-climate regions of North America and Northern Europe. The well-established refining and supply chain infrastructure for mineral-based transformer oils, combined with significantly lower cost relative to bio-based and silicone alternatives, reinforces the dominance of this sub-segment.

Application Insights

Transformers constitute the leading application segment in the transformer oil market, accounting for approximately 78% of overall demand. Within this segment, power transformers lead consumption by virtue of their large oil volumes a single extra-high-voltage power transformer can require up to 100,000 litres of transformer oil.

Distribution transformers follow closely, driven by the massive expansion of distribution networks in high-growth markets. The U.S. Department of Energy (DOE) estimates that the United States alone has over 3 million distribution transformers in service, a significant proportion of which are approaching end-of-life.

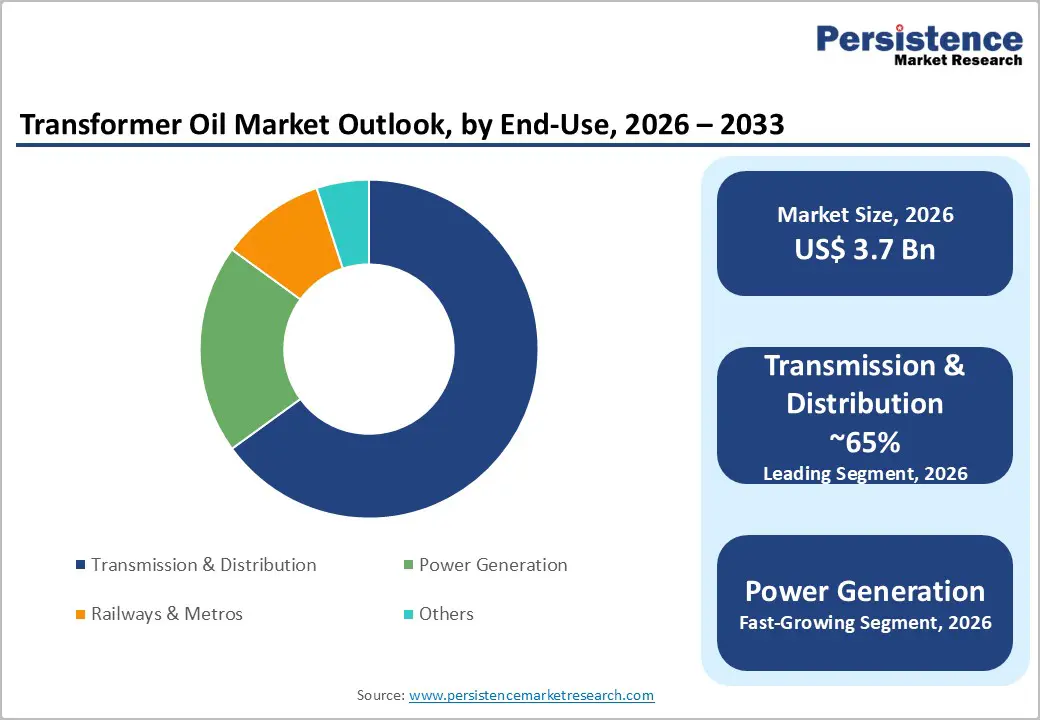

End-user Insights

Transmission & Distribution (T&D) is the dominant end-use segment for transformer oil, representing approximately 65% of global demand. T&D infrastructure constitutes the largest installed base of oil-filled transformers, both in terms of unit count and oil volume, making it the primary consumption channel.

Governments across the globe are investing heavily in T&D modernization; the World Bank has channelled over US$ 20 Bn into transmission and distribution projects in developing countries over the past five years alone. In the United States, the Bipartisan Infrastructure Law allocated US$ 65 Bn for power grid upgrades, including extensive T&D investment.

Regional Analysis

North America Transformer Oil Market Trends & Analysis

North America holds a significant share of the global transformer oil market, underpinned by substantial ongoing grid modernization investments and the aging of installed transformer infrastructure. The U.S. Department of Energy has identified that a large share of the American transmission grid is over 25 years old, necessitating extensive refurbishment and transformer replacement.

The Bipartisan Infrastructure Law and the Inflation Reduction Act together commit over US$ 100 Bn to grid enhancement, creating a strong multi-year demand pipeline for transformer oil. The region is also witnessing growing adoption of bio-based natural ester oils, driven by utility sustainability commitments and USDA Bio Preferred Program incentives.

U.S. Transformer Oil Market Size

The U.S. represents the largest individual country market in North America, accounting for an estimated ~80% of the regional share. Driven by the replacement of aging infrastructure and clean energy grid expansion, the U.S. market reflects consistent demand growth, with both mineral and bio-based oil segments experiencing volume increases through the forecast horizon.

Europe Transformer Oil Market Trends, Drivers, & Insights

Europe represents a mature yet dynamically evolving transformer oil market, characterized by a strong regulatory push toward eco-friendly insulating fluids and an ambitious renewable energy integration agenda. The European Green Deal and Repower EU programs mandate a fundamental restructuring of energy infrastructure, driving significant investment in offshore wind connections, smart grid deployments, and cross-border interconnectors.

European utilities such as Elia, National Grid, and TenneT are among the most active procurers of transformer oil globally. Regulatory frameworks under EU REACH are accelerating the transition from conventional mineral oils to biodegradable alternatives.

Germany Transformer Oil Market Size

Germany, as Europe's largest economy and a leader in the Energiewende (energy transition), accounts for the largest national share in the European transformer oil market, approximately 18% of regional demand. Grid operator investments under the Federal Network Agency framework continue to drive both replacement and expansion of transformer capacity.

U.K. Transformer Oil Market Size

The U.K. is a major contributor to Europe's transformer oil demand, particularly with its ambitious offshore wind expansion under the Contracts for Difference (CfD) scheme. The U.K. accounts for approximately 12% of European market volume, with bio-based oil adoption accelerating among National Grid ESO-affiliated utilities.

France Transformer Oil Market Size

France's transformer oil market is shaped by its extensive nuclear fleet modernization and renewable energy expansion initiatives. Réseau de Transport d'Électricité (RTE) is investing significantly in grid upgrades, maintaining France's share at approximately 10–12% of the European market.

Asia Pacific Transformer Oil Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing regional market for transformer oil, driven by massive electrification programs, infrastructure buildout, and rapid industrialization in China, India, and Southeast Asia. The region is characterized by high transformer installation rates for both new generation capacity and expanding T&D networks.

China's 14th Five-Year Plan and India's National Electricity Plan are landmark policy frameworks accelerating grid expansion at scale. Demand for transformer oil in Asia Pacific is also supported by rapidly growing metro rail and industrial electrification projects.

China Transformer Oil Market Size

China is the world's single largest transformer oil market, consuming an estimated 30–32% of global volume. State grid companies State Grid Corporation of China (SGCC) and China Southern Power Grid (CSG)are among the world's largest transformer oil purchasers, with annual procurement volumes running into hundreds of thousands of metric tons.

India Transformer Oil Market Size

India is the second-largest market in Asia Pacific and one of the fastest growing globally, with transformer oil demand strongly correlated to the government's Saubhagya and RDSS schemes. India accounts for approximately 8% of the regional market and is projected to exhibit above-average CAGR driven by new distribution transformer installations in rural electrification.

Japan Transformer Oil Market Size

Japan's transformer oil market is driven by grid resilience investments following the 2011 Fukushima Daiichi disaster and the ongoing diversification of the energy mix. Japan accounts for approximately 6% of Asia Pacific transformer oil demand, with strong adoption of silicone and bio-based insulating oils in urban distribution applications.

Competitive Landscape

The global transformer oil market exhibits a moderately consolidated structure, with a handful of large multinational oil and chemical companies commanding significant shares alongside numerous regional and national players. Leading companies compete on product quality, technical service capabilities, sustainability credentials, and supply chain reliability.

Key competitive strategies include capacity expansions in high-growth markets, development of bio-based and synthetic oil portfolios, and long-term supply agreements with major utilities and transformer OEMs. Emerging business trends include the provision of oil lifecycle management services, including on-site oil testing, regeneration, and reclamation, enabling manufacturers to build recurring revenue streams.

Key Developments:

- In January 2026, Nynas delivered nearly 700 metric tonnes of NYTRO Lyra X transformer oil for the first phase of Poland’s largest offshore wind project in collaboration with GE Vernova, supporting offshore renewable grid infrastructure.

- In November 2025, Nynas AB and KON?AR - Electrical Industry Inc. deployed NYTRO BIO 300X bio-based transformer oil in Croatia’s electricity distribution network, marking the country’s first transformer to operate with a fully renewable insulating fluid.

Global Transformer Oil Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.7 Bn |

|

Current Market Value (2026) |

US$ 3.7 Bn |

|

Projected Market Value (2033) |

US$ 5.4 Bn |

|

CAGR (2026-2033) |

6.5% |

|

Leading Region |

Asia Pacific, 45% share |

|

Dominant Application |

Transformers, 78% share |

|

Top-ranking Product |

Transmission & Distribution, 65% |

|

Incremental Opportunity |

US$ 1.7 Bn |

Companies Covered in Transformer Oil Market

- Nynas AB

- Shell plc

- Cargill, Incorporated

- ExxonMobil Corporation

- Ergon International

- Calumet Specialty Products

- Apar Industries Ltd.

- Gandhar Oil Refinery (India) Ltd.

- Savita Oil Technologies Ltd.

- PetroChina Company Limited

- Sinopec (China Petroleum & Chemical Corporation)

- Repsol S.A.

- Petronas Lubricants International

- Calfrac Well Services

- Engen Petroleum Ltd.

- Dow Corning (Dow Inc.)

- Behran Oil Company

- CEPSA

- Powerlink Oil

- Midwest Industrial Supply

Frequently Asked Questions

The global Transformer Oil market is estimated to be valued at US$ 3.6 Bn in 2026 and is projected to reach US$ 5.4 Bn by 2033, growing at a CAGR of 5.6% during the forecast period of 2026–2033.

The market is primarily driven by large-scale electricity grid modernization investments globally, growing integration of renewable energy sources such as solar and wind that require new transformer installations, and governmental initiatives in emerging economies particularly in Asia Pacific aimed at universal electrification and T&D network expansion.

Mineral oil, specifically naphthenic transformer oil, leads the market with approximately 72% share. Its superior low-temperature performance, cost-effectiveness, well-established supply infrastructure, and excellent dielectric and cooling properties make it the preferred insulating fluid for most power and distribution transformer applications worldwide.

Asia Pacific is the leading region, accounting for over 45% of global transformer oil consumption. China and India are the primary demand centres, driven by State Grid Corporation of China (SGCC) investments and India's Revamped Distribution Sector Scheme (RDSS), with the region expected to maintain its dominance through 2033.

Key players in the global Transformer Oil market include Nynas AB, Shell plc, Cargill Incorporated, ExxonMobil Corporation, Apar Industries Ltd., Ergon International, Savita Oil Technologies Ltd., Gandhar Oil Refinery (India) Ltd., PetroChina Company Limited, and Sinopec, among others.