- Semiconductor Materials & Components

- Step Up and Step Down Transformer Market

Step Up and Step Down Transformer Market Size, Share, and Growth Forecast 2026 - 2033

Step Up and Step Down Transformer Market by Material (Aluminum-wound, Copper-wound), by Cooling Type (Oil-cooled, Air-cooled/Dry-type), by Phase (Single-phase, Three-phase), by Application (Electric Utility, Power Plants, Industrial), and Regional Analysis 2026 - 2033

Step Up and Step Down Transformer Market Size and Trends Analysis

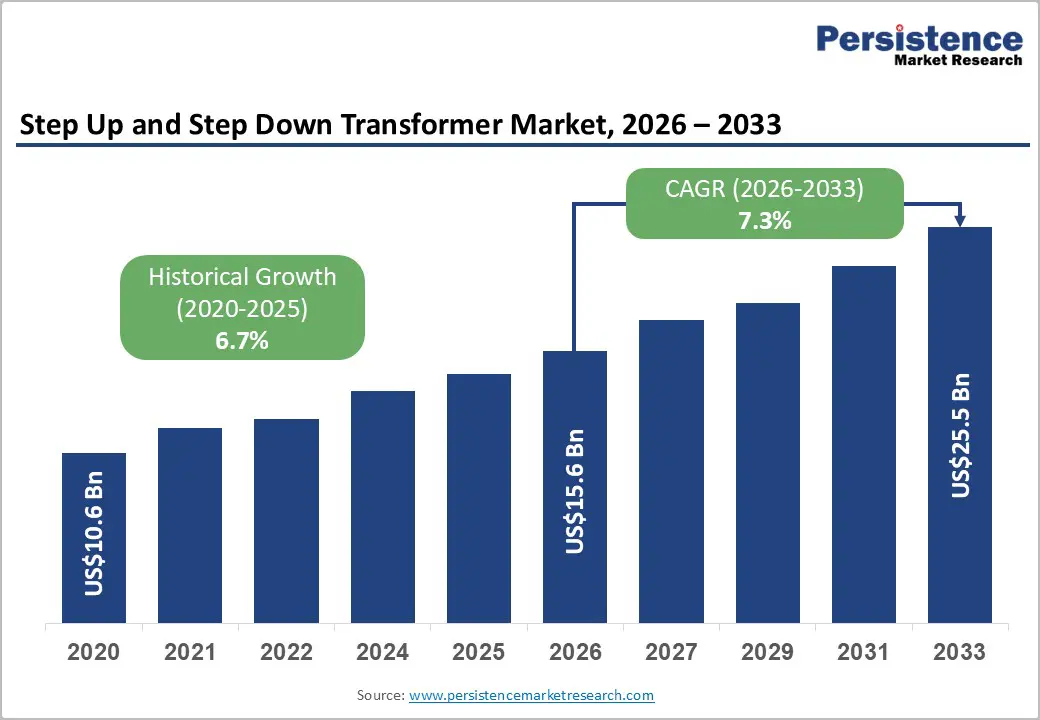

The global step up and step down transformer market size is likely to be valued at US$15.6 billion in 2026 and is projected to reach US$ 25.5 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by global transition toward renewable energy integration, the modernization of aging electrical grids in developed economies, and the exponential rise in industrial electricity demand within emerging markets. Simultaneously, the modernization of aging transmission infrastructure is necessitating the replacement of legacy units with high-efficiency, digitally enabled transformers.

Key Industry Highlights:

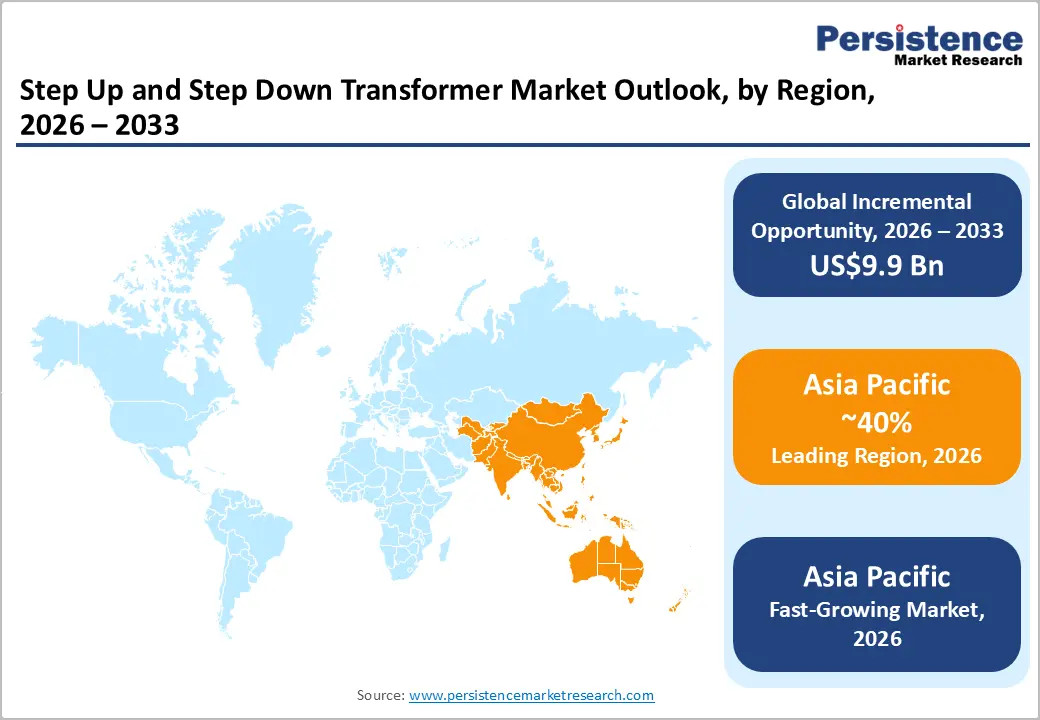

- Leading Region: Asia Pacific is projected to lead the market due to large-scale industrialization, urbanization, and infrastructure expansion, accounting for approximately 40% of the market share in 2026, supported by rapid utility-scale transmission, renewable integration, and high-capacity industrial deployment, along with technology adoption and ecosystem advantages.

- Fastest Growing Region: Asia Pacific is anticipated to grow fastest due to steady industrial modernization, regulatory support, and adoption across transmission, distribution, and EV infrastructure sectors.

- Leading Material: Copper-wound transformers are expected to dominate the material segment, accounting for approximately 70% of the market share through industrial adoption, driven by high throughput, superior electrical and mechanical performance, and deployment in high-value applications such as offshore wind, data centers, and UHV transmission projects.

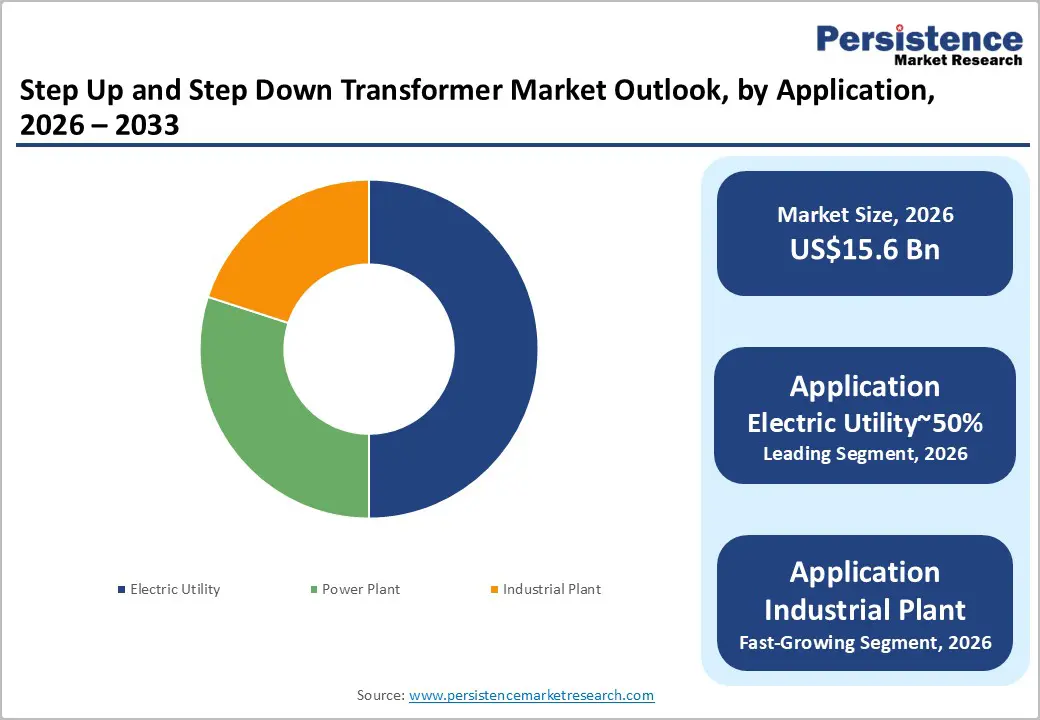

- Leading Application: Electric utility applications are projected to dominate for simplicity, cost-efficiency, and operational adoption across key sectors, holding approximately 50% share in 2026, reinforced by large-scale grid modernization, renewable integration, and high-capacity throughput in mature and emerging energy networks.

- Key Industry Developments: Leading players such as Siemens, ABB, and Schneider Electric are expanding localized manufacturing and consolidating supply chains to improve resilience and regulatory compliance.

| Key Insights | Details |

|---|---|

|

Step Up and Step Down Transformer Market Size (2026E) |

US$15.6 Bn |

|

Market Value Forecast (2033F) |

US$25.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Acceleration of Renewable Energy Integration

The accelerating integration of renewable energy is structurally reshaping transformer demand, anchored in decarbonization mandates and grid modernization objectives. Utility-scale solar and wind projects, often located far from consumption centers, intensify reliance on step-up transformers for high-voltage transmission and step-down units for localized distribution. Annual renewable capacity additions exceeding 500 GW reinforce a direct demand linkage. The growing penetration of intermittent generation further elevates requirements for transformers capable of bidirectional power flows, voltage stability, and dynamic load management, raising baseline technical thresholds across transmission and distribution networks.

Renewable-led grid expansion is also tightening technology cycles and capital allocation discipline across the transformer value chain. Offshore wind and large-scale renewable installations, defined by high-capacity and reliability requirements, are driving adoption of advanced insulation systems, enhanced thermal performance, and digital condition monitoring. Regulatory pressure to accelerate grid interconnection timelines is intensifying procurement activity, positioning compliant and scale-efficient manufacturers to capture outsized value as renewable integration deepens across global power systems.

High Initial Capital Expenditure and Raw Material Volatility

High initial capital investment remains a structural restraint across the transformer market, particularly for high-capacity step-up and step-down installations. Asset costs are compounded by civil works, installation complexity, grid integration, and auxiliary protection systems, raising total project expenditure. In emerging economies, this capital intensity constrains utilities and smaller industrial buyers, encouraging the life extension of legacy assets instead of fleet replacement. This behavior suppresses near-term sales volumes and slows penetration of high-efficiency technologies in cost-sensitive regions.

Manufacturing economics further intensify this restraint by exposing it to raw material volatility. High-capacity transformers rely heavily on copper and cold-rolled grain-oriented steel, both of which are subject to pronounced price fluctuations. Year-on-year copper price volatility approaching 20% directly compresses margins and disrupts procurement planning. In developing markets, the high cost of advanced transformers delays grid modernization initiatives, extending project timelines by several years and reinforcing uneven adoption across regional power systems.

Growth in Microgrids and Decentralized Energy Systems

The rising emphasis on energy security and grid resilience is accelerating microgrid deployment across hospitals, data centers, and defense infrastructure. These decentralized systems require specialized step-up and step-down transformers to manage localized generation, storage, and load balancing. Microgrid architectures place technical emphasis on bidirectional power flow, high-frequency operation, and compact form factors, elevating demand for advanced transformer designs. Market expansion toward a projected US$60 billion scale by 2030 reinforces a structurally attractive demand pocket within the broader power infrastructure ecosystem.

This shift is creating a clear opportunity for manufacturers to align with compact, high-efficiency, and safety-compliant transformer solutions. Dry-type transformers are gaining traction in microgrid environments due to fire safety, indoor suitability, and reduced maintenance requirements. An addressable opportunity approaching US$1.2 billion is emerging for suppliers capable of delivering standardized yet application-flexible products, particularly as regulatory and resilience mandates strengthen adoption across critical infrastructure segments.

Category–wise Analysis

Material Insights

Copper-wound transformers are expected to lead the global transformer market, accounting for approximately 70% of revenue in 2026, underpinned by their superior electrical conductivity, mechanical strength, and thermal stability compared to aluminum alternatives. This dominance is reinforced across high-efficiency utilities, offshore wind projects, and data centers, where reliability, compact footprint, and lower lifecycle costs are critical. Recent innovations, including continuously transposed conductors, hybrid winding designs, and 3D-printed copper coils, enhance performance while addressing supply challenges by integrating secondary copper. Industry leaders such as Hitachi Energy, Siemens Energy, ABB, and Hammond Power Solutions leverage advanced copper technologies and high-purity materials from suppliers such as Luvata and Wieland to maintain premium positioning. These capabilities, coupled with evolving DOE efficiency standards and circular-economy mandates, ensure that copper-wound units remain the preferred choice for demanding industrial and utility applications.

Aluminum-wound transformers are expected to be the fastest-growing segment in the global transformer market, driven by cost-sensitive distribution, residential, and rural electrification projects. Growth is being catalyzed by improved connection technologies, such as cold-friction welding and bimetallic connectors, which overcome historical reliability limitations, as well as lighter weight, easier transport, and lower upfront capital expenditure compared to copper. Adoption is further accelerated by cast-resin dry-type units, amorphous-core integration, and regulatory compliance updates (UL/IEC certifications, DOE 2027 standards) that enable aluminum to meet efficiency and safety requirements. Leading brands such as Hammond Power Solutions, Schneider Electric, Eaton, and Voltamp Transformers are expanding aluminum-based platforms to capture high-volume demand, while renewable energy standardization, rapid EV charger rollout, and residential infrastructure development reinforce the segment’s growth trajectory through the forecast period.

Application Insights

Electric utility applications are expected to lead the global transformer market, accounting for approximately 50% of the market share, driven by extensive investments in grid modernization and the transition to renewable energy. The segment’s dominance is underpinned by large-scale deployment across utilities, with adoption anchored in high-capacity throughput, reliability, and long-term operational efficiency. Massive capacity expansions, including India’s addition of 86,433 MVA in 2024–25, and industrial investments by Hitachi Energy, Siemens Energy, and Eaton, reinforce the entrenched infrastructure. Technological advancements such as AI-enabled predictive maintenance, IoT integration, solid-state transformers, and eco-friendly materials further enhance system resilience and efficiency. Leading brands, including Hitachi Energy, Siemens Energy, GE Vernova, Schneider Electric, CG Power, and TBEA, continue to lock in enterprise workflows, sustaining the segment’s dominance across mature and evolving energy networks.

Industrial applications are expected to be the fastest-growing segment of the global transformer market, driven by surging automation, decentralized power generation, and stringent energy-efficiency mandates across manufacturing, data centers, and EV infrastructure. Growth is being catalyzed by innovations such as amorphous metal cores, ester-based biodegradable insulating oils, dry-type and modular transformer designs, and digital twin-enabled predictive maintenance, which materially improve operational reliability, safety, and cost efficiency. Accelerating adoption is supported by Industry 4.0 integration, AI-driven optimization, and pre-fabricated solutions that reduce lead times for first-time industrial users. Companies such as Siemens Energy and Hitachi Energy are scaling new platforms to capture early-cycle demand, while regulatory compliance, environmental standards, and workforce familiarity further embed switching costs, positioning the industrial segment to outpace overall market growth.

Regional Insights

Asia Pacific Step Up and Step Down Transformer Market Trends

Asia Pacific is projected to remain the leading regional market, accounting for approximately 40% of global transformer demand, driven by large-scale industrialization, urbanization, and infrastructure expansion in China and India. The region’s demand is structurally anchored in utility-scale transmission, industrial electrification, and rapid urban power distribution. Government initiatives, including India’s Revamped Distribution Sector Scheme (RDSS), are modernizing distribution networks, generating substantial procurement volumes for domestic manufacturers. China continues to expand its Ultra-High Voltage (UHV) transmission capacity, reinforcing both consumption and production dominance, while regional cost efficiencies and integrated supply chains enhance competitiveness and export potential. These structural factors consolidate Asia Pacific’s position as the largest global market in both volume and strategic relevance.

The Asia Pacific region is also the fastest-growing market, driven by ongoing investment in grid modernization, renewable integration, and industrial capacity expansion. Step-down transformers for industrial applications and localized distribution are experiencing accelerated adoption, driven by high-volume deployments in smart factories, EV charging hubs, and urban substations. Combined with favorable policy frameworks, cost advantages, and a resilient manufacturing ecosystem, the Asia Pacific presents both immediate revenue scale and long-term growth potential, reinforcing its dual status as the largest and most dynamically expanding regional market globally.

North America Step Up and Step Down Transformer Market Trends

North America is expected to maintain a significant but non-dominant position in the global transformer market. The region is characterized by mature grid infrastructure, with modernization and reliability initiatives driving steady replacement of aging assets. Regulatory frameworks, including DOE efficiency standards, promote the adoption of high-grade electrical steel and amorphous-core transformers. Investment in smart and solid-state transformer technologies supports operational efficiency and integration of digital monitoring systems, maintaining the region’s relevance in high-value infrastructure segments without positioning it as a growth leader.

Market expansion is further influenced by the integration of renewable energy and the electrification of transport networks, which require robust step-down infrastructure to accommodate EV charging and distributed generation. Utilities prioritize compliance and lifecycle optimization to sustain steady demand across the transmission and distribution layers. While growth rates remain moderate compared with those of emerging regions, North America’s regulatory rigor, technological sophistication, and grid modernization programs ensure stable volume and revenue, reinforcing its status as a mature, high-value regional market in the global transformer landscape.

Europe Step Up and Step Down Transformer Market Trends

Europe is expected to maintain a significant regional position, underpinned by stringent environmental regulations and coordinated energy policy frameworks. Demand is concentrated in Germany, France, and the U.K., where the EU Green Deal and national renewable energy strategies are driving the deployment of specialized step-up transformers, particularly for offshore wind farms. Regulatory mandates, including eco-design directives and low-loss efficiency requirements, are phasing out legacy units and compelling widespread adoption of environmentally compliant transformers. Cross-border grid interconnections further reinforce demand for high-voltage equipment, ensuring harmonized power sharing and operational reliability across the region.

While growth is moderate relative to emerging markets, Europe’s market is shaped by sustainability priorities and advanced technical specifications, creating structural incentives for dry-type and ester-oil-filled transformers with reduced environmental risk. The convergence of regulatory oversight, grid modernization, and renewable integration sustains a predictable and high-quality demand profile. Manufacturers operating in the region must align with compliance standards and technological benchmarks to secure market access, positioning Europe as a stable, regulation-driven market with measured growth potential and strategic relevance within the global transformer landscape.

Competitive Landscape

The global step up and step down transformer market is moderately consolidated, with the top five players ABB, Siemens Energy, GE, Schneider Electric, and Eaton controlling approximately 45–50% of total market revenue. High-voltage transmission (step-up) remains concentrated due to technical complexity and capital intensity, where leading firms leverage turnkey solutions and expertise in green and digital features to maintain strategic positioning.

The low-voltage distribution (step-down) segment is more fragmented, with numerous regional manufacturers competing on standardized units and price. Competitive advantage increasingly depends on value-added capabilities, including energy efficiency, smart monitoring, and sustainability integration, while incumbents consolidate high-voltage operations to secure market influence and long-term contracts with utilities and industrial clients.

Key Industry Developments:

- In May 2025, GE Vernova secured a major Power Grid order for over 70 EHV transformers. The order strengthened demand for large step-up transformers in one of the fastest-growing transmission markets and supported long-term capex visibility for 400–765 kV equipment used in India’s renewable power evacuation corridors.

- In September 2025, GE Vernova invested an additional CAD 270 million in its Varennes, Canada transformer facility. The investment strengthened regional manufacturing capacity for grid transformers, supporting North American utilities’ grid-hardening and replacement programs while reducing lead-time risks for step-down and step-up units.

- In November 2025, GE Vernova expanded its Mysuru manufacturing facility to increase transformer and component output. Perks: The expansion reinforced India’s role as a cost-competitive production hub and improved supply and export capacity for oil-cooled step-up and step-down transformers across Asia and the Middle East.

Step Up and Step Down Transformer Market Scope

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2020 - 2025 |

|

Forecast Period |

2026 - 2033 |

|

Market Analysis |

Value: US$ Bn |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

Companies Covered in Step Up and Step Down Transformer Market

- ABB Ltd.

- Siemens Energy AG

- Schneider Electric SE

- Eaton Corporation PLC

- Bharat Heavy Electrics Limited (BHEL)

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Hyosung Heavy Industries

- GE Vernova

- Hyundai Electric & Energy Systems

- TBEA Co., Ltd.

- Hammond Power Solutions

- Wilson Transformer Company

- Crompton Greaves (CG) Power

- Hitachi Energy

Frequently Asked Questions

The global step up and step down transformer market is projected to be valued at US$15.6 billion in 2026 and is expected to reach US$25.5 billion by 2033, supported by grid modernization and renewable energy integration.

Demand is accelerating due to rapid renewable energy deployment, modernization of aging transmission infrastructure, rising industrial electricity consumption, and expansion of EV charging and microgrid systems across developed and emerging economies.

The global step up and step down transformer market is expected to grow at a CAGR of 7.3% between 2026 and 2033, reflecting sustained utility-sector investments and renewable-led grid expansion.

The fastest growth opportunities are emerging in Asia Pacific, driven by large-scale transmission projects, renewable evacuation corridors in China and India, and aggressive grid upgrade programs.

Key players in the step up and step down transformer market include ABB Ltd., Siemens Energy, Schneider Electric, GE Vernova, Hitachi Energy, Eaton Corporation, Mitsubishi Electric, Toshiba Corporation, Hyundai Electric, Hyosung Heavy Industries, BHEL, TBEA Co., Ltd., and Crompton Greaves Power.