- Semiconductor Materials & Components

- Solid State Transformer Market

Solid State Transformer Market Size, Share, and Growth Forecast 2026 - 2033

Solid State Transformer Market by Product Type (Distribution Solid State Transformer, Power Solid State Transformer, Traction Solid State Transformer), Component (Converters, High-Frequency Transformers, Switches, Others), Application, End-user, and Regional Analysis, 2026 - 2033

Solid State Transformer Market Size and Trend Analysis

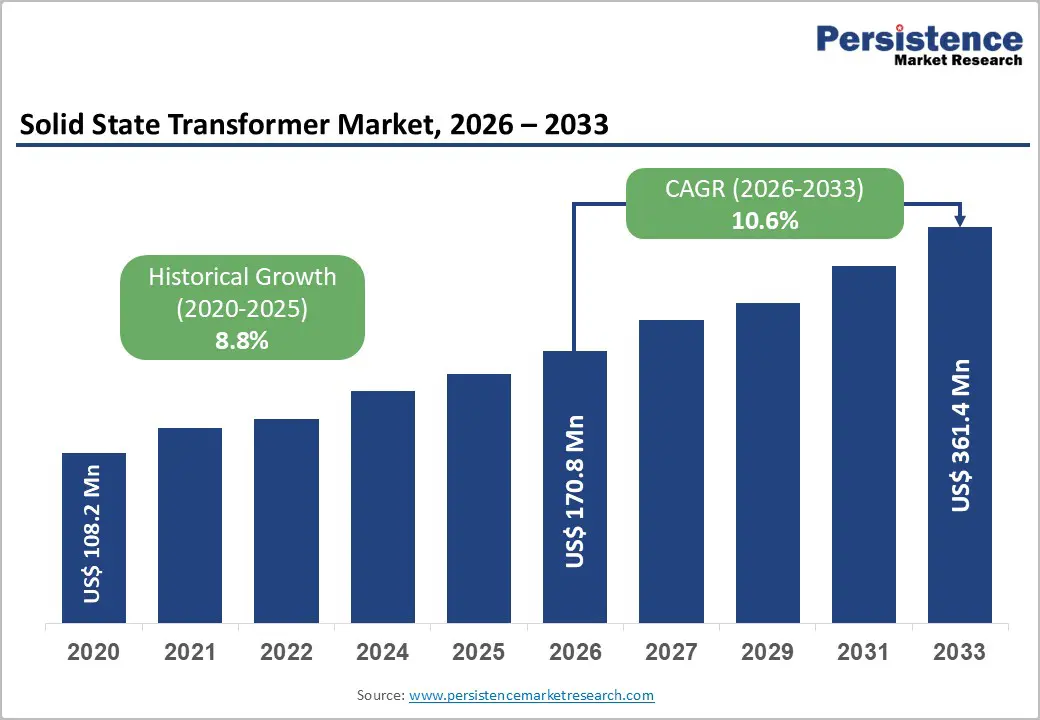

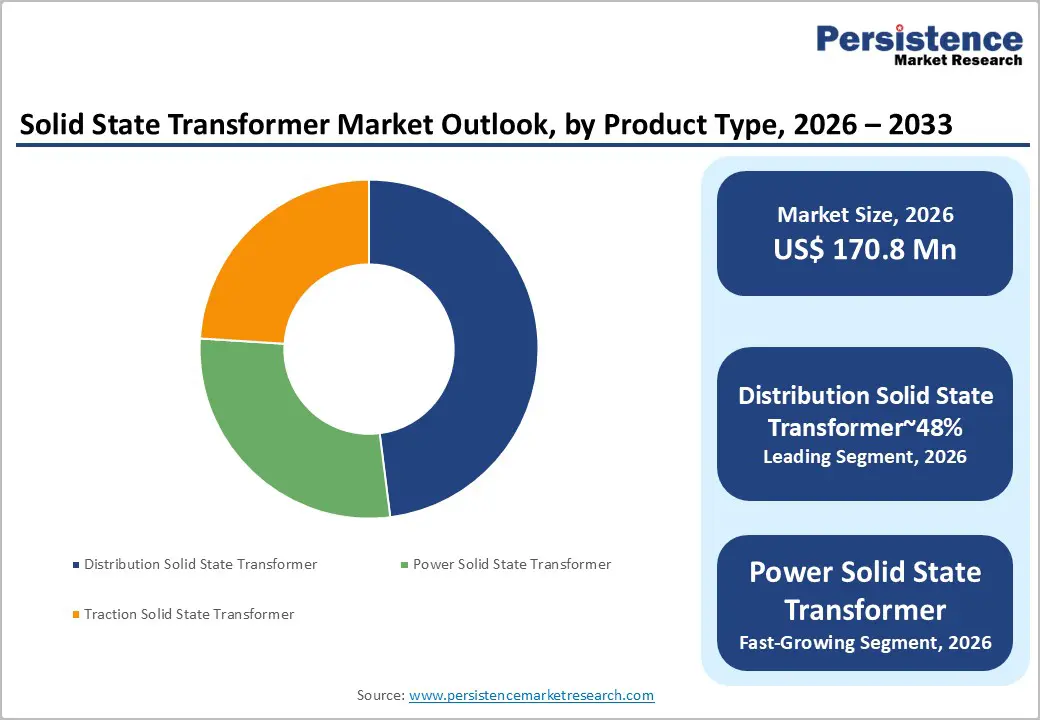

The global solid state transformer market size is likely to be valued at US$ 170.8 Million in 2026 and is expected to reach US$ 361.4 Million by 2033, growing at a CAGR of 11.3% during the forecast period from 2026 to 2033.

This exceptional growth trajectory is driven by the convergence of three structural forces: accelerating global grid modernization investment, explosive renewable energy integration requirements, and the rapid scale-up of electric vehicle charging and railway electrification infrastructure worldwide.

Key Market Highlights

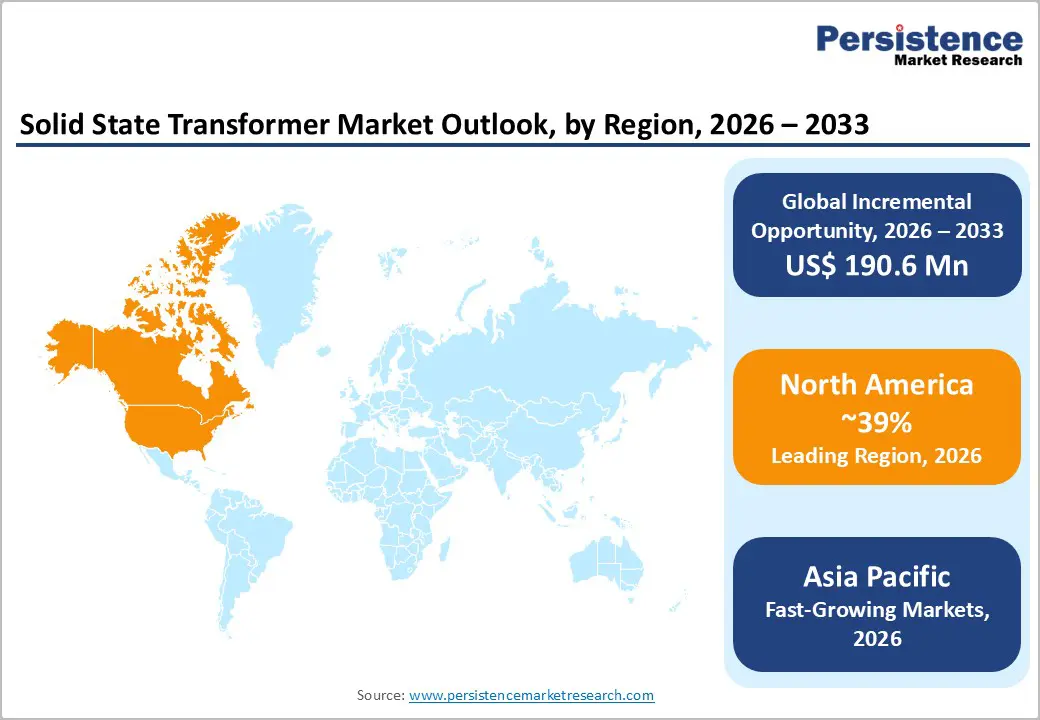

- Leading Region: North America leads the global Solid State Transformer Market with 39% share, anchored by the U.S. DOE's US$ 20+ million SST-specific investment program, US$ 3.7 billion in 2024 grid modernization commitments, and a strong innovation ecosystem featuring Hitachi Energy, GE Vernova, and GridBridge advancing SST commercialization.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market with rising CAGR of 13.4%, powered by China's unrivaled renewable energy deployment, Japan's railway electrification programs, India's national grid expansion under PGCIL, and ASEAN's rapidly industrializing manufacturing economies driving escalating power conversion technology demand.

- Leading Segment: The Distribution Solid State Transformer (DSST) segment dominates product type with approximately 48% market share, driven by global smart grid modernization programs, the IEA's documented need to increase annual grid investment by 50% above US$ 400 billion, and pilot validations by ABB and Siemens at utility scale.

- Fastest-Growing Segment: EV Charging Infrastructure is the fastest-growing application segment, fueled by the IEA's reporting of 17+ million EV sales in 2024, the US$ 5 billion NEVI federal funding program, and SSTs' unique V2G bidirectional capability that conventional transformer architectures fundamentally cannot replicate.

- Key Opportunity: The greatest market opportunity lies in data center power infrastructure modernization, where AI-driven hyperscale expansion, projected by the IEA to drive 50% of U.S. electricity demand growth through 2030, is compelling operators to adopt SST-enabled DC bus power distribution architectures for superior efficiency and density.

| Key Insights | Details |

|---|---|

| Solid State Transformer Market Size (2026E) | US$ 170.8 Million |

| Market Value Forecast (2033F) | US$ 361.4 Million |

| Projected Growth CAGR (2026 - 2033) | 11.3% |

| Historical Market Growth (2020 - 2025) | 7.9% |

Market Dynamics

Drivers - Accelerating Global Grid Modernization Investment and Smart Grid Deployment

The urgent need to upgrade aging electrical infrastructure is one of the strongest and most unavoidable demand drivers for solid state transformers worldwide. According to the World Energy Investment 2024 report by the International Energy Agency (IEA), global grid investment reached US$ 400 billion in 2024, the highest level in the past decade. However, the agency also highlighted that this investment must increase by nearly 50% annually through 2030 to support the rising electricity demand driven by renewable energy integration, expanding data centers, and electric vehicle adoption.

In the United States, the Department of Energy (DOE) invested US$ 1.5 billion in four major transmission modernization projects during 2024 and also committed over US$ 20 million specifically to advance solid-state transformer technologies. SSTs offer advanced features such as active power factor correction, real-time fault detection, reactive power compensation, and seamless integration with DC microgrids. These capabilities make them significantly more suitable than conventional transformers for modern smart grid infrastructure, encouraging utilities worldwide to adopt them as part of their grid modernization strategies.

Renewable Energy Integration and Power Quality Management Requirements

The ongoing global transition toward clean energy is creating a structural and rapidly growing demand for solid state transformers, which serve as an important power-electronics interface between intermittent renewable energy sources and stable grid infrastructure. Research published in Nature Scientific Reports (2024) confirmed that SSTs used in photovoltaic systems can provide essential grid support functions such as reactive power compensation, voltage regulation, and fault detection. These functions are critical for maintaining grid stability as the share of solar and wind power continues to increase.

The International Energy Agency (IEA) projects that solar PV and wind energy will contribute the majority of new electricity generation capacity additions globally through 2030. Each gigawatt of renewable energy capacity requires reliable power conversion and conditioning equipment to maintain consistent power flow. SSTs operate at high switching frequencies using advanced wide-bandgap semiconductors such as Silicon Carbide (SiC) and Gallium Nitride (GaN). This technology enables compact and lightweight transformer designs with energy conversion efficiencies ranging from 91.5% to 94.1%, outperforming conventional transformers under variable renewable energy load conditions.

Restraints - High Manufacturing Cost and Technology Maturity Constraints

Despite their performance advantages, solid state transformers remain considerably more expensive to manufacture than traditional line-frequency transformers. The primary reason is the high cost of advanced components such as wide-bandgap power semiconductors including Silicon Carbide (SiC) and Gallium Nitride (GaN), high-frequency magnetic cores, and complex multilevel converter topologies. In an SST architecture, power electronics components such as IGBT or MOSFET switches, gate drivers, and digital control systems contribute significantly to the total system cost.

These advanced components create a noticeable price premium compared to conventional copper-wound transformer systems. As a result, large-scale procurement by utilities is often restricted, particularly in emerging and cost-sensitive markets where minimizing capital expenditure remains a key priority. While SSTs provide long-term operational efficiency and advanced grid functionality, many utilities still prioritize lower upfront investment. This cost barrier slows down widespread commercial adoption and limits deployment speed despite the strong technological advantages of solid state transformers.

Thermal Management Challenges and Reliability Validation Gap

Solid state transformers generate significantly higher internal heat compared to conventional passive transformers because they rely on active semiconductor switching components. This increased heat generation requires advanced thermal management systems to maintain safe operating temperatures and ensure long-term performance reliability. Such cooling systems often add extra weight, size, and design complexity to SST installations while also increasing maintenance requirements.

In demanding applications such as railway traction systems, SST equipment must meet strict environmental and operational standards including IEC 60077 and EN 50124, which regulate vibration tolerance, temperature cycling, and electromagnetic compatibility. Meeting these standards requires long and expensive testing and qualification programs before commercial deployment can occur. Another challenge is the limited availability of long-term operational data for large-scale SST installations. Utilities and grid operators typically prefer equipment with decades of proven field reliability before integrating new technologies into critical infrastructure. This lack of extensive historical performance data creates hesitation among conservative infrastructure operators when considering SST deployment.

Opportunities - Ultra-Fast EV Charging Infrastructure as a High-Growth SST Application

The rapid expansion of electric vehicle charging infrastructure represents one of the most promising commercial opportunities for solid state transformer manufacturers. SSTs offer bidirectional power flow capability and a compact design, making them highly suitable for the technical requirements of ultra-fast EV charging stations. According to the International Energy Agency (IEA), global electric vehicle sales exceeded 17 million units in 2024, and the agency expects tens of millions of public charging points to be installed worldwide by 2030 to support growing EV adoption. SST technology allows vehicle-to-grid (V2G) bidirectional power exchange, enabling EV charging stations to act not only as energy consumers but also as distributed energy storage systems that can support the power grid during peak demand.

Government initiatives are also accelerating infrastructure deployment. In the United States, the National Electric Vehicle Infrastructure (NEVI) Formula Program, supported by US$ 5 billion under the Bipartisan Infrastructure Law, is funding the installation of high-power charging corridors along major highways, creating a significant procurement opportunity for SST-enabled charging technologies.

Data Center Power Infrastructure Modernization Driving Demand for High-Efficiency SSTs

The rapid growth of artificial intelligence computing, cloud platforms, and hyperscale data centers is creating strong demand for advanced power conversion technologies capable of delivering higher efficiency and greater power density. Solid state transformers are well positioned to meet these requirements because they can support direct DC power distribution and reduce energy losses compared with traditional transformer-rectifier systems.

According to the International Energy Agency (IEA), electricity consumption by data centers in the United States is expected to grow by nearly 2% annually through 2030, with AI-driven workloads responsible for almost half of this growth. Major hyperscale operators such as Microsoft, Google, and Amazon Web Services are actively exploring next-generation power distribution systems based on DC bus architectures. SSTs can directly support these systems by eliminating multiple AC-to-DC conversion stages, thereby improving overall energy efficiency. At the same time, advanced computing platforms, such as high-performance GPUs operating above 700 watts per unit, are increasing rack-level power density requirements, making SST-based power infrastructure a highly attractive solution.

Category-wise Analysis

Product Type Insights

Distribution Solid State Transformers (DSSTs) dominate the product type segment, accounting for approximately 48% of total market revenues. These transformers act as a critical interface between medium-voltage distribution networks and low-voltage end-user systems. DSSTs enable advanced functions such as active power flow control, reactive power compensation, and seamless integration of distributed energy resources including rooftop solar systems, battery storage, and electric vehicle chargers at the distribution level.

Their ability to support real-time grid management makes them highly suitable for modern smart grid infrastructure. The U.S. Department of Energy’s 2024 commitment of more than US$ 20 million to develop solid-state transformer architectures specifically highlighted distribution-level voltage and power rating applications as a key deployment focus. In addition, ABB Ltd. integrated 1,500 DSST units into EV charging infrastructure during a pilot project in Japan in early 2024, demonstrating the commercial readiness of the technology for large-scale distribution networks. As countries accelerate smart grid modernization initiatives, DSSTs are expected to remain the most commercially viable and widely adopted product segment within the solid state transformer portfolio.

Component Insights

Converters represent the largest component segment within the Solid State Transformer Market, accounting for around 42% of total component-level revenue. These converters include AC-DC, DC-DC, and DC-AC power conversion stages that form the technological backbone of SST systems. They are the most complex, high-value, and technologically intensive parts of the transformer architecture. The overall performance of a solid state transformer depends heavily on converter efficiency, switching frequency, and thermal management capabilities.

The converter design and manufacturing remain the primary value-creating activities in the SST supply chain. Research showed that wide-bandgap semiconductor-based converters can achieve overall SST efficiency levels ranging from 91.5% to 94.1% across varying output power conditions. This finding confirms the strong performance and commercial potential of advanced converter technologies. Companies such as Infineon Technologies AG, ROHM Co., Ltd., and STMicroelectronics are increasingly adopting Silicon Carbide (SiC) MOSFET converters, which improve power density while reducing heat generation and cooling requirements, further strengthening converters’ leadership in the component segment.

Application Insights

The smart grid and power distribution segment holds the largest share in the Solid State Transformer Market by application, contributing approximately 35% of total application-segment revenues. Governments worldwide are investing heavily in smart grid systems to enhance grid reliability, integrate renewable energy sources, and enable real-time demand management. Solid state transformers are well suited to these requirements because they offer advanced capabilities such as bidirectional power flow control, voltage regulation, and improved energy management.

According to the International Energy Agency, global grid investments must increase by about 50% above the current US$ 400 billion annual spending level to meet electricity demand by 2030. This significant increase in infrastructure spending creates a strong policy-supported environment for the deployment of advanced power electronics technologies such as SSTs. Major national grid modernization programs in the United States, the European Union, China, and India are allocating multibillion-dollar budgets to upgrade grid infrastructure, with solid state transformers emerging as a premium technology for efficient power management and distribution applications.

End-user Insights

The Energy and Utilities segment leads the Solid State Transformer Market by end-use, accounting for roughly 44% of total market demand. Utilities, grid operators, renewable energy developers, and electricity generation companies form the primary customer base for SST technology. These organizations operate large-scale power infrastructure and require advanced solutions to maintain grid stability, integrate renewable energy, and meet regulatory standards related to efficiency and decarbonization. In 2024, Hitachi Energy Ltd. announced investments exceeding US$ 6 billion to strengthen its global transformer production capacity, including about US$ 1.5 billion dedicated specifically to scaling transformer manufacturing facilities.

This significant investment highlights the growing importance of advanced power transformation technologies. Additionally, the European Union’s Electricity Regulation (EU) 2019/943 and the Clean Energy for All Europeans Package require active management of distribution systems, which increases the need for advanced power electronics at grid interfaces. Because utilities and grid operators control major infrastructure investments, the Energy and Utilities segment remains the primary driver of SST technology adoption worldwide.

Regional Insights

North America Solid State Transformer Market Trends

The United States is the leading market for solid state transformers in North America, supported by the world’s largest grid modernization investment programs and a strong power electronics innovation ecosystem. In December 2024, the U.S. Department of Energy announced more than US$ 20 million in funding for critical power equipment development, including projects focused on improving solid-state transformer architectures for enhanced performance across different voltage levels. This initiative is part of a broader national effort to upgrade electricity transmission and distribution infrastructure.

In the same year, the DOE committed US$ 1.5 billion to four major transmission modernization projects and allocated an additional US$ 2.2 billion for eight transmission projects spanning 18 states. These investments collectively create a large near-term procurement environment for advanced power conversion technologies such as SSTs. Canada is also contributing to regional market growth through its clean electricity transition strategy. Hitachi Energy announced a CAD 270 million investment in September 2025 to expand transformer manufacturing capacity at its Varennes, Quebec facility, strengthening North America’s advanced transformer supply chain.

Europe Solid State Transformer Market Trends

Europe represents a highly advanced and policy-driven market for solid state transformers, supported by ambitious decarbonization and energy transition initiatives. Programs such as the European Green Deal and the EU Clean Energy Package are driving major upgrades to power distribution infrastructure across the region. Germany, Europe’s largest electricity market, is implementing the Energiewende energy transition strategy, which requires extensive grid modernization to support rapidly expanding wind and solar power capacity.

This transformation is creating strong demand for advanced power management technologies, including solid state transformers, particularly at distribution grid interfaces. Major technology companies such as Siemens AG and ABB Ltd. are leading SST research and pilot deployments in European smart grid projects, demonstrating the technology’s performance in real-world conditions. The United Kingdom’s Clean Power 2030 Action Plan aims to fully decarbonize the electricity system by 2035, prompting National Grid ESO to invest in advanced grid management technologies. In addition, utilities such as EDF in France and grid operators in Spain are expanding renewable integration projects, further increasing demand for SST-enabled infrastructure.

Asia Pacific Solid State Transformer Market Trends

Asia Pacific is the fastest-growing regional market for solid state transformers, driven by rapid renewable energy deployment, large-scale infrastructure development, and increasing electricity demand. China plays a leading role due to its massive investments in renewable power and ultra-high-voltage grid expansion. The National Development and Reform Commission and the State Grid Corporation of China are actively funding research and pilot projects focused on advanced solid-state transformer technologies as part of the country’s grid modernization strategy.

Academic institutions such as Tsinghua University and the Chinese Academy of Sciences are conducting advanced research on multi-port SST architectures designed for DC microgrid applications. Japan also represents a major SST opportunity because of its highly developed railway electrification and industrial automation sectors. Companies such as Mitsubishi Electric Corporation and Toshiba Corporation are actively developing SST technologies supported by research grants from Japan’s Ministry of Economy, Trade and Industry. Meanwhile, India is expanding its national power grid through major projects led by Power Grid Corporation of India Limited, while industrial automation growth across ASEAN countries is creating additional demand for advanced power conversion technologies.

Competitive Landscape

The global Solid State Transformer Market has a moderately consolidated competitive structure, particularly among companies that lead in technology development and system integration capabilities. Major players such as Hitachi Energy Ltd., ABB Ltd., Siemens AG, GE Vernova, and Mitsubishi Electric Corporation dominate the market through strong vertical integration across semiconductor technology, power converters, magnetic components, and system-level engineering. Their competitive advantage comes from proprietary wide-bandgap semiconductor technologies, certified high-frequency transformer designs, and real-world pilot deployment data that demonstrates system reliability and performance.

Leading companies are focusing on securing large-scale contracts with national grid operators and utility providers while also expanding manufacturing capacity for Silicon Carbide-based converter systems. In addition, companies are strengthening research collaborations with universities and research institutions to accelerate innovation in multi-port solid state transformer architectures designed for future DC microgrid applications. New business models are also emerging, including power-electronics-as-a-service offerings, performance-based infrastructure contracts, and long-term joint development partnerships with national energy agencies and utility companies.

Key Developments:

- In March 2025: Hitachi Energy Ltd. announced an additional US$250 million investment to expand transformer manufacturing capacity in U.S. facilities located in Virginia, Missouri, and Mississippi. The investment supports rising grid modernization demand and builds on the company’s broader US$6 billion global infrastructure expansion program.

- In May 2025: Hitachi Energy Ltd. successfully tested the world’s first 765 kV / 400 kV single-phase, 250 MVA natural ester-filled transformer, marking a major technological milestone. The breakthrough supports next-generation ultra-high-voltage AC transmission networks and strengthens grid reliability for large-scale power infrastructure projects.

- In February 2024: ABB Ltd. demonstrated a pilot deployment in Japan integrating 1,500 Distribution Solid State Transformers for EV charging infrastructure. The project validated bidirectional power flow, grid load balancing, and advanced power management capabilities, highlighting SST potential for large-scale utility and e-mobility infrastructure integration.

Companies Covered in Solid State Transformer Market

- Hitachi Energy Ltd.

- ABB Ltd.

- Siemens AG

- Mitsubishi Electric Corp.

- GE Vernova

- Ermco

- Semiconductor Components Industries, LLC (onsemi)

- GridBridge

- Infineon Technologies AG

- Vollspark

- ROHM Co., Ltd.

- STMicroelectronics

- Renesas Electronics Corporation

- Alstom SA

- Toshiba Corporation

- Eaton Corporation plc

- Schneider Electric SE

- Power Electronics S.A.

- Amantys Limited

Frequently Asked Questions

The global Solid State Transformer Market is valued at US$ 170.8 Million in 2026 and is projected to reach US$ 361.4 Million by 2033, growing at a CAGR of 11.3% over the forecast period. The market recorded a historical CAGR of 7.9% between 2020 and 2025, reflecting consistent growth driven by grid modernization and renewable energy integration imperatives.

The foremost drivers are accelerating global grid modernization investment, with the IEA documenting the need for a 50% increase above the current US$ 400 billion annual grid investment baseline, combined with surging renewable energy integration requirements and the rapid EV charging and railway electrification infrastructure build-out globally. The U.S. DOE's targeted SST investment programs further validate institutional commitment to the technology's commercial deployment.

Distribution Solid State Transformers (DSSTs) lead the product type segment with approximately 48% market share. Their central role in enabling active power flow management, renewable energy integration, and bidirectional EV charging at the distribution grid level, validated by ABB's pilot integration of 1,500 DSST units for EV infrastructure in Japan in 2024, positions them as the highest near-term commercial volume product type.

North America leads the global market, driven by the U.S. DOE's multi-billion-dollar grid modernization investment program, targeted SST architecture development funding exceeding US$ 20 million in 2024, and a world-class innovation ecosystem comprising Hitachi Energy, GE Vernova, GridBridge, and national laboratory research centers advancing SST commercialization.

Data center power infrastructure modernization represents the highest-impact near-term opportunity, as AI-driven hyperscale expansion is projected by the IEA to drive approximately 50% of U.S. electricity demand growth through 2030. SSTs' ability to enable direct DC bus power distribution for high-density computing loads, eliminating multiple conversion stages, positions them as a premium, high-margin technology solution for hyperscale operators committed to operational efficiency improvement.

Key market participants include Hitachi Energy Ltd., ABB Ltd., Siemens AG, GE Vernova, Mitsubishi Electric Corp., Infineon Technologies AG, STMicroelectronics, ROHM Co., Ltd., Toshiba Corporation, Alstom SA, Renesas Electronics Corporation, GridBridge, Cree (Wolfspeed), Eaton Corporation plc, and Schneider Electric SE, among other specialist power electronics and transformer manufacturers globally.