- Semiconductor Materials & Components

- Traction Transformers Market

Traction Transformers Market Size, Share, and Growth Forecast 2026 - 2033

Traction Transformers Market by Rolling Stock (Electric Locomotives, High-Speed Trains, Metros), by Mounting Position (Underframe, Machine Room, Over The Roof), Overhead Line Voltage (AC, DC), and Regional Analysis, 2026 - 2033

Traction Transformers Market Size and Trend Analysis

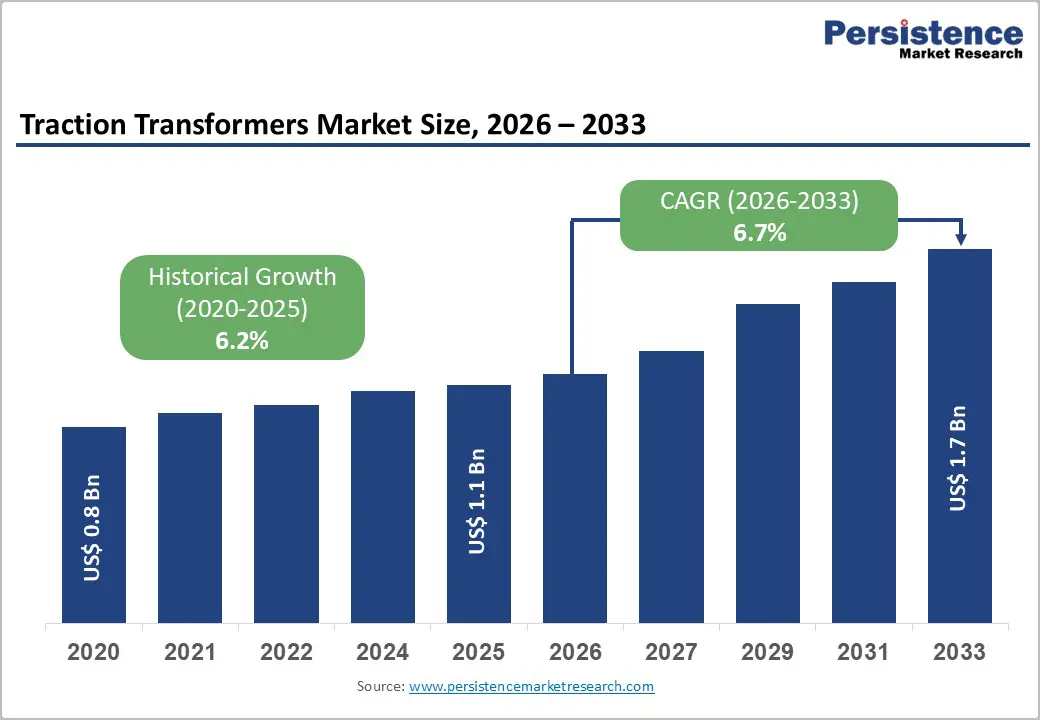

The global traction transformers market is likely to be valued at US$ 1.1 billion in 2026 and projected to reach US$ 1.7 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033.

The global market is experiencing robust expansion driven by three primary catalysts: escalating government commitments to rail electrification across developing and developed economies, the structural shift toward sustainable transportation modes in response to climate change imperatives, and technological breakthroughs enabling more efficient, compact, and intelligent transformer systems. Supporting this trajectory is the Infrastructure Investment and Jobs Act allocation of US$ 66 billion for rail improvements in North America, the European Union’s Green Deal targeting carbon neutrality by 2050 through electrified rail expansion, and India’s achievement of 94% railway network electrification as of early 2024 with ongoing expansion toward 100%.

Key Industry Highlights:

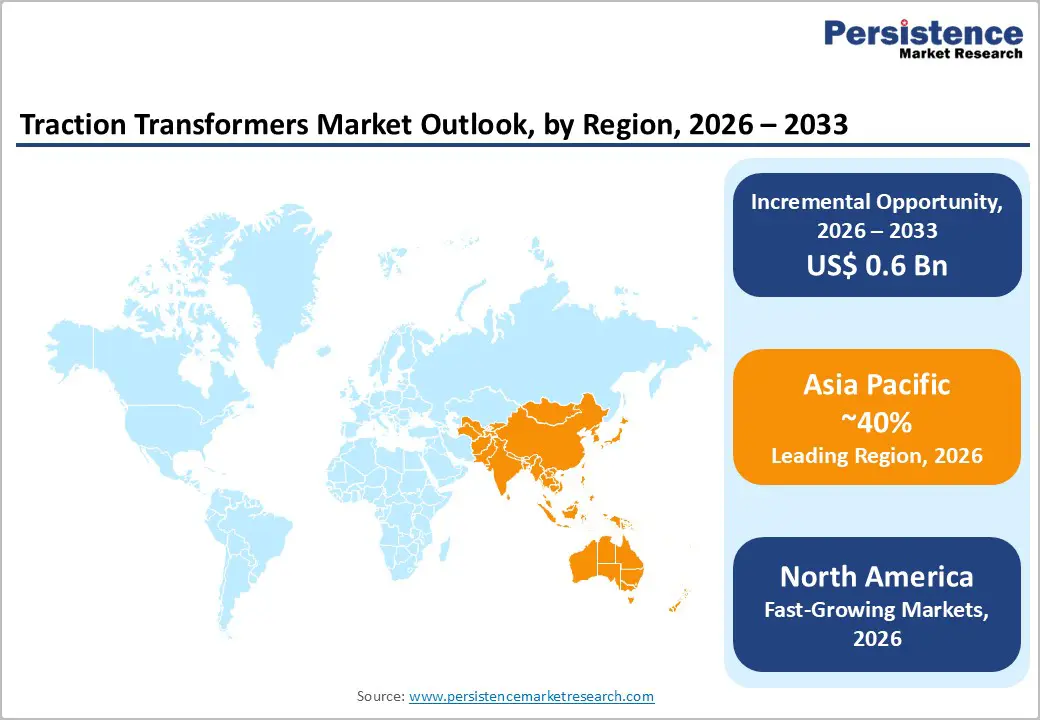

- Leading Region: Asia-Pacific holds a dominant 40% traction transformer market share, supported by China’s 40,000+ km HSR network, India’s 94% electrification, and rapid metro expansion, making it the strongest growth engine through 2033.

- Fastest-Growing Regional: North America shows the fastest growth, driven by US$ 66 billion federal rail modernization funding, early freight electrification efforts, and state-led high-speed rail programs such as California’s 500-mile corridor.

- Dominant Segment: Electric locomotives lead with roughly 58% share in 2025, supported by global electrification of freight and passenger systems, offering 30% higher energy efficiency and lower lifetime operating costs than diesel.

- Fastest-Growing Segment: Machine-room-mounted transformers are set for 7.5% CAGR through 2032, driven by demand for high reliability, easier maintenance, and suitability for premium long-distance and high-speed train operations.

- Key Opportunity: IoT-enabled predictive maintenance offers major value, enabling over 93% fault-detection accuracy, cutting maintenance costs by 30%, and generating US$ 150-200 million in annual software and service revenues by 2033.

| Key Insights | Details |

|---|---|

| Traction Transformers Market Size (2026E) | US$ 1.1 billion |

| Market Value Forecast (2033F) | US$ 1.7 billion |

| Projected Growth CAGR (2026 - 2033) | 6.7% |

| Historical Market Growth (2020 - 2025) | 6.2% |

Market Dynamics

Market Growth Drivers

Accelerating Rail Electrification Projects and Infrastructure Investment

Global governments are channeling unprecedented capital toward rail electrification initiatives, fundamentally transforming the demand landscape for traction transformers. India exemplifies this trend, having invested US$ 5.5 billion in railway electrification since 2014, achieving an electrification rate of 94% and targeting complete network electrification by 2024-2025. The Federal Railroad Administration in the United States committed US$ 66 billion specifically for rail infrastructure improvements, substantially elevating traction transformer procurement requirements. Similarly, the European Union’s Connecting Europe Facility allocates multi-billion euro investments annually toward cross-border rail electrification corridors, creating sustained procurement opportunities for AC traction transformers serving mainline applications. China’s railway sector expansion includes 6,000 kilometers of new high-speed rail requiring advanced transformer systems, with ABB Ltd securing major contracts to supply traction transformers for 1,120 rail cars across multiple high-speed platforms.

Rising Demand for Energy-Efficient and Sustainable Rail Solutions

The global transition toward decarbonized transportation systems creates structural demand for efficient traction transformer solutions that minimize energy losses and enable environmental compliance. Electric locomotives consume approximately 30% less energy than diesel equivalents while eliminating direct carbon emissions, aligning with international net-zero commitments and increasingly stringent emissions regulations. Modern traction transformers achieve efficiency improvements of 1-2 percentage points compared to legacy systems, translating to multi-million dollar operational cost savings over 30-year asset lifecycles on high-density routes. The European Union’s net-zero target by 2050 and India’s commitment to become a net-zero carbon emitter by 2030 in railway operations create regulatory frameworks accelerating electrification timelines. Additionally, electricity costs demonstrate lower volatility compared to diesel fuel subject to geopolitical fluctuations, enhancing operational predictability for rail operators.

Market Restraints

High Capital Costs and Electrification Barriers in Remote Regions

Traction transformer market expansion faces structural challenges from prohibitive infrastructure costs associated with rail electrification in geographically challenging or low-density regions. Electrifying railway networks requires substantial capital investments in overhead catenary systems, substations, signal infrastructure, and track modifications, often exceeding US$ 1-2 million per kilometer in developed markets and 30-50% higher in emerging economies requiring parallel infrastructure upgrades. Rural and remote areas present particularly acute challenges, where sparse population densities render per-kilometer electrification costs economically unjustifiable, limiting transformer deployment to densely populated corridors and major intercity routes. Countries including the United Kingdom, Brazil, Mexico, and Taiwan maintain significant diesel-powered fleets partly attributable to electrification cost barriers, with diesel locomotives representing 25-40% of operational stock despite superior long-term cost profiles favoring electric alternatives. The absence of electrified infrastructure in these regions creates persistent demand for traditional diesel locomotives, fragmenting market opportunities and preventing consolidated technology transitions.

Complex Design Standards and Multi-System Voltage Requirements

The traction transformer market confronts technical complexity arising from fragmented international railway standards and diverse voltage specifications across geographic regions, creating substantial engineering and manufacturing constraints. Railway networks operate under incompatible voltage systems including 15 kV 50 Hz AC (Europe), 25 kV 50 Hz AC (mainline European and Asian routes), 16.7 Hz AC systems (Germanic region), and 1.5-3 kV DC systems (metro and urban transit applications), necessitating manufacturer investment in multiple transformer variants lacking production economies of scale. Cross-border rail corridors require multi-system transformers accommodating voltage switching and frequency conversion, elevating design complexity and production costs by 15-25% versus single-system variants. Heterogeneous safety standards, vibration specifications, thermal performance requirements, and mechanical load parameters across national railway authorities fragment component specifications, preventing standardized production and limiting aftermarket component compatibility.

Market Opportunities

Rapid Urban Metro Expansion and Mass Transit Electrification

Urban metro systems represent the fastest-growing transformer application segment, driven by metropolitan population concentration and municipal investments in congestion mitigation and air quality improvement. The global urban population is projected to reach 68% by 2050 from 55% in 2020, concentrating demand for mass transit capacity in major cities across Asia-Pacific, Europe, and emerging markets. Metro rail systems inherently operate on electrified infrastructure with underframe and machine room mounting configurations, creating consistent demand for compact, lightweight traction transformers optimized for constrained physical envelopes. Asia-Pacific cities including Shanghai, Mumbai, Jakarta, Bangkok, and Manila are executing major metro expansion programs, with India’s metro expansion targeting 25 new metro systems across tier-two cities through 2035, requiring 500+ million-dollar equipment procurement programs. These urban systems typically operate 18-24 hours daily with high duty cycles, necessitating premium reliability and thermal management, driving specification upgrades toward advanced cooling designs and IoT-enabled predictive maintenance systems that command 20-30% price premiums. The machine room mounting segment is anticipated to expand at a 7.5% CAGR through 2032, representing the fastest-growing position variant, as modern metro procurement standards increasingly specify integrated traction-converter packages offering space optimization and system reliability benefits.

Integration of IoT and Predictive Maintenance Technologies

Next-generation traction transformers incorporating Internet of Things technologies and machine learning-enabled predictive maintenance represent a transformative market opportunity addressing operator demands for lifecycle cost reduction and fleet availability optimization. IoT-enabled transformer monitoring systems integrating real-time sensors for temperature, dissolved gas analysis, vibration, and partial discharge enable fault detection accuracy exceeding 93% with remaining useful life prediction correlation of 0.92, substantially exceeding conventional offline testing methodologies.

Implementing predictive maintenance regimes reduces annual maintenance costs by approximately 30% through early fault detection and optimized scheduling, translating to US$ 50-100 million annual savings for major freight and metro operators managing 500+ electric locomotive fleets. Leading manufacturers including Siemens AG, Hitachi Energy, and ABB Ltd have initiated product portfolio expansion toward smart transformer variants, with Siemens Mobility launching oil-free dry-type transformers in 2023 specifically targeting urban rail operators prioritizing fire risk reduction and sustainability credentials. The integration of cloud-based analytics platforms and mobile applications enabling remote fleet health monitoring creates recurring revenue opportunities through software licensing and managed service contracts, potentially tripling lifetime customer value versus traditional component sales models.

Category-wise Analysis

Rolling Stock Insights

The electric locomotives segment dominates the traction transformer market with an estimated market share of 58% in 2025, reflecting the structural shift across global rail networks toward electrified freight and passenger transport. Electric locomotives represent the primary application endpoint for conventional load-bearing traction transformers, with global installed bases exceeding 18,000 units concentrated in Europe, China, India, and North America. The leadership position reflects multiple competitive advantages: electric locomotives deliver 30% superior energy efficiency versus diesel counterparts, achieve lower total cost of ownership over 30-year operational cycles, and enable seamless integration with regenerative braking systems that recover kinetic energy during deceleration.

Manufacturers including Alstom SA and Siemens AG secure disproportionate market share in electric locomotive procurement through established OEM relationships, integrated traction system offerings combining transformers with motors and control electronics, and superior service networks supporting the 1,500+ electric locomotives deployed annually across developing markets.

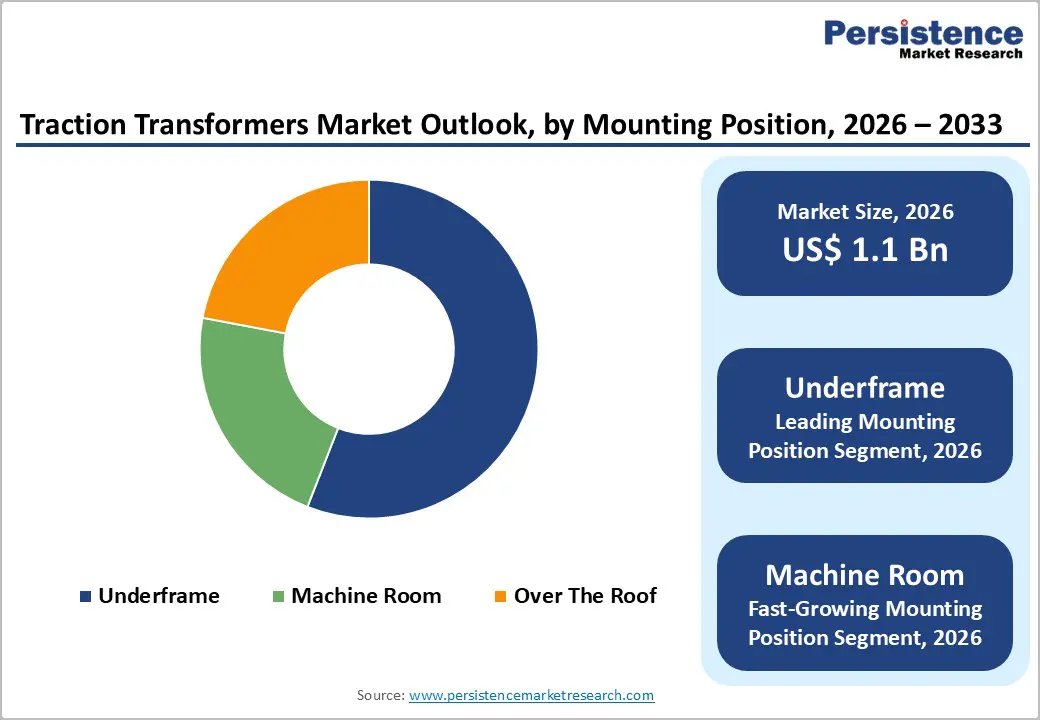

Mounting Position Insights

The underframe mounting configuration commands the dominant market position with approximately 56% market share in 2025, attributable to space optimization advantages enabling increased passenger capacity within constrained train envelopes. Underframe placement positions the transformer beneath the railway vehicle floor, preserving interior volume for passenger accommodation or cargo storage while maintaining thermal dissipation through bottom-mounted cooling elements. The underframe segment demonstrates steady 5.8% CAGR expansion through 2033, supported by metro expansion in developing Asia-Pacific markets and urban rail modernization in developed economies.

Conversely, the machine room mounting segment is anticipated to achieve rapid 7.5% CAGR growth through 2033, representing the fastest-growing position variant, driven by equipment reliability and maintainability advantages in multi-phase rail systems. Machine room configurations facilitate maximum reliability through optimal thermal management, simplified cooling fluid circulation, and accessibility for preventive maintenance without vehicle disassembly, supporting premium pricing 15-20% above underframe equivalents.

Overhead Line Voltage Insights

The AC systems segment maintains clear market leadership with approximately 70% market share in 2025, reflecting the global predominance of alternating current electrification across mainline railway networks and high-speed rail corridors. AC systems deliver superior technical performance for long-distance transmission through reduced power losses over extended overhead line distances, lower infrastructure costs compared to equivalent DC systems on major routes, and seamless integration with grid power supplies eliminating rectification requirements at terminal substations.

The segment encompasses 15 kV 50 Hz, 25 kV 50 Hz, and 16.7 Hz AC systems, collectively representing 95%+ of electrified global rail networks. AC traction transformers command approximately 30-40% price premiums versus DC equivalents due to operational complexity and specialized cooling requirements managing harmonics and power factor characteristics. The segment is anticipated to expand at approximately 6.5% CAGR through 2033, driven by continued mainline electrification investments across developing markets and high-speed rail expansion in India, Southeast Asia, and Eastern Europe.

Regional Insights

North America Traction Transformers Market Trends

The North American traction transformer market is experiencing modest acceleration despite representing a mature, electrification-constrained market, with growth catalyzed by federal infrastructure stimulus and emerging freight electrification initiatives. The Infrastructure Investment and Jobs Act allocated US$ 66 billion for rail improvements, including US$ 39 billion for transit modernization and US$ 12 billion for passenger rail expansion, establishing multi-year procurement pipelines for traction transformer equipment.

However, North America’s market development remains limited by the region’s predominantly diesel-powered rail infrastructure, with electric track representing less than 1% of total US railway network, concentrated on commuter lines in the Northeast Corridor, California, and select metropolitan areas. These initiatives collectively represent US$ 40-50 billion infrastructure investment through 2035, generating approximately 1,500-2,000 unit traction transformer demand. Regional demand concentrates on AC systems for high-speed applications and DC systems for urban transit modernization, with leading manufacturers Siemens, Alstom, and ABB maintaining North American manufacturing and service facilities to support infrastructure projects and aftermarket support requirements.

Europe Traction Transformers Market Trends

Europe represents the world’s most mature and electrification-advanced market, with 55% of railway networks electrified and leadership concentrated among Germany, France, Switzerland, Austria, and Belgium. The region drives global innovation in traction transformer technology through stringent performance standards, aggressive sustainability mandates, and high-density rail networks supporting premium product specifications. The European Union’s Green Deal and 2050 carbon neutrality commitment establish regulatory frameworks accelerating electrification investment, with national targets including Germany’s 75% network electrification by 2030, France’s comprehensive mainline and regional rail modernization, and ongoing expansion of cross-border electrified corridors supporting integrated European rail mobility.

Established high-speed rail networks including TGV, ICE, Eurostar, and Renfe systems operate mature procurement and maintenance ecosystems, supporting recurring transformer replacement demand as legacy equipment approaches end-of-life, typically occurring every 25-30 years. Europe’s market is characterized by sophisticated operator demand for advanced features including IoT integration, lightweight designs, and multi-system compatibility, supporting premium pricing and technology differentiation among suppliers. The region demonstrates rapid adoption of innovative solutions including oil-free dry-type transformers, lightweight composite designs reducing unit weight by 10-15%, and digital twin technologies enabling predictive life extension modeling.

Asia Pacific Traction Transformers Market Trends

Asia-Pacific dominates global traction transformer demand, accounting for approximately 40% of worldwide market share, driven by unprecedented electrification expansion across China, India, Japan, and Southeast Asian emerging markets. China operates the world’s largest high-speed rail network at 40,000+ kilometers, representing approximately 65% of global HSR mileage and requiring continuous investment in transformer replacement and fleet expansion, with manufacturers including CRRC partnering with global suppliers ABB, Siemens, and Mitsubishi Electric for technology transfer and joint manufacturing. India’s electrification momentum represents the region’s most transformative trend, with 94% of railway networks electrified as of early 2024, supported by US$ 5.5 billion investment since 2014, establishing trajectory for 100% electrification by 2025-2026.

The Indian Railways expansion plan targets rolling out 50 Namo Bharat AC trains and 100 new MEMUs during 2025-2026, requiring 2,000+ traction transformer units, with manufacturers Alstom, Siemens, and ABB securing major supply contracts through local manufacturing partnerships. Japan maintains world-leading standards for transformer reliability and efficiency, operating the Shinkansen network and supporting continuous rolling stock modernization requiring advanced transformer solutions from Mitsubishi Electric, Hitachi Energy, and Toshiba Corporation. Southeast Asian metro expansion represents the highest-growth sub-segment, with Manila, Bangkok, Jakarta, and Ho Chi Minh City executing major urban transit systems creating 1,500+ transformer unit demand through 2032, supported by favorable government policies and multilateral development bank financing facilitating infrastructure deployment.

Competitive Landscape

The traction transformer market is moderately consolidated, with a concentrated group of global suppliers holding over three-quarters of total revenue and a long tail of regional manufacturers serving localized or niche applications. The market structure increasingly favors companies with integrated traction system capabilities, allowing OEMs to source transformers alongside converters, motors, and control electronics to minimize integration risks and shorten project timelines. Business strategies center on sustained R&D investment in lightweight materials, improved thermal performance, and digitally enabled monitoring to support predictive maintenance offerings.

Modular and standardized design platforms are becoming key competitive levers, enabling lower engineering costs while supporting customization for multi-voltage or roof-mounted configurations. Regional manufacturers strengthen their position through cost-efficient production, proximity to large rail procurement programs, and government-supported localization policies. Across the competitive landscape, differentiation is shaped by technology innovation, manufacturing scalability, lifecycle service support, and long-term supply agreements with rolling stock OEMs and transit authorities.

Key Market Developments

- January 2025: Alstom secures a €144 million contract to supply Mitrac traction components and electrical equipment for 17 Vande Bharat Sleeper trainsets (408 cars) including five-year maintenance support, to be manufactured in its Indian facilities under the Make in India initiative.

Companies Covered in Traction Transformers Market

- ABB Ltd

- Alstom SA

- JST Transformateurs

- Mitsubishi Electric Corporation

- Siemens AG

- EMCO Limited

- Hind Rectifiers Ltd

- International Electric Co., Ltd.

- Wilson Transformer Company

- Toshiba Corporation

- Neeltran Inc

- Hitachi Energy

- CRRC (China Railways Rolling Stock Corporation)

- Hyundai Electric

- BHEL (Bharat Heavy Electricals Limited)

Frequently Asked Questions

The market is expected to reach US$ 1.7 billion by 2033, driven by global rail electrification programs, sustainability policies, and advances in lightweight and IoT-enabled transformer technologies.

Demand is fueled by large rail modernization budgets, rising adoption of energy-efficient electric locomotives, rapid metro expansion, and global electrification rates moving toward 50% penetration.

Electric locomotives dominate with about 58% share due to superior efficiency, lower lifetime costs, environmental compliance, and strong global fleet deployment.

Asia-Pacific leads with 40% share, supported by extensive high-speed rail networks, near-complete electrification in India, and rapid metro development across major cities.

IoT-enabled predictive maintenance offers the largest opportunity by improving fault detection accuracy, lowering maintenance costs, and creating recurring software and service revenue streams.

Global leadership is held by major industrial manufacturers with strong OEM partnerships and service networks, while emerging regional suppliers compete through cost efficiency and localized production.