- Smart Packaging

- Thin Wall Packaging Market

Thin Wall Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Thin Wall Packaging Market by Packaging Type (Cups, Bowls & Lids, Others), Material (Polypropylene (PP), Biopolymers, Others), Manufacturing Process, End-user Industry, and Regional Analysis for 2026 - 2033

Thin Wall Packaging Market Size and Trends Analysis

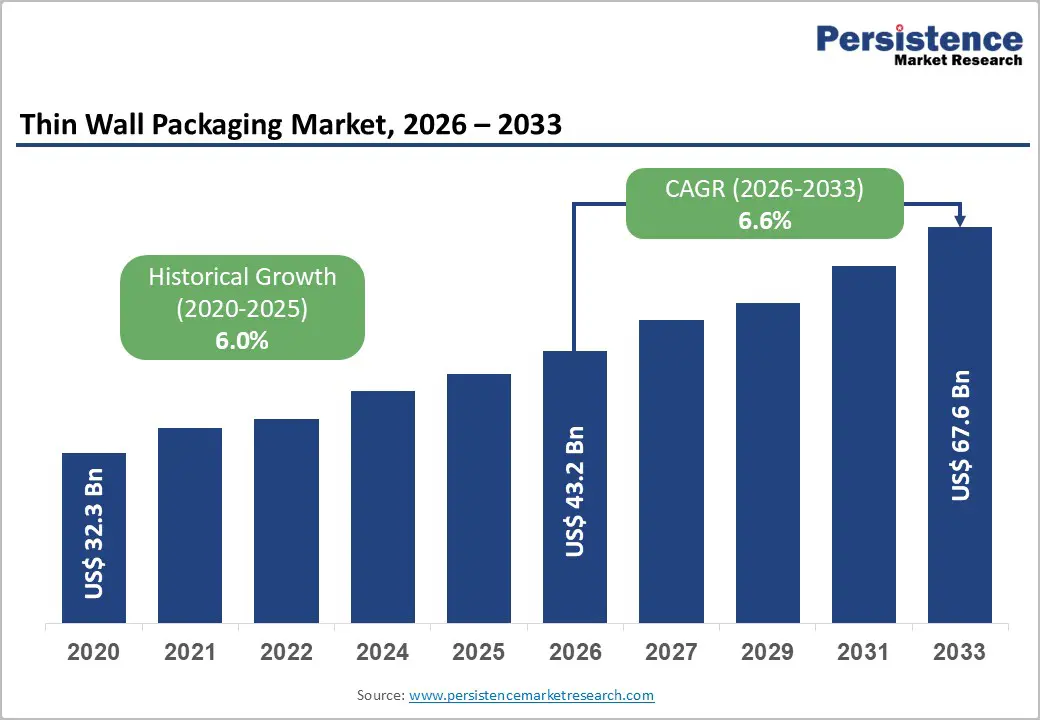

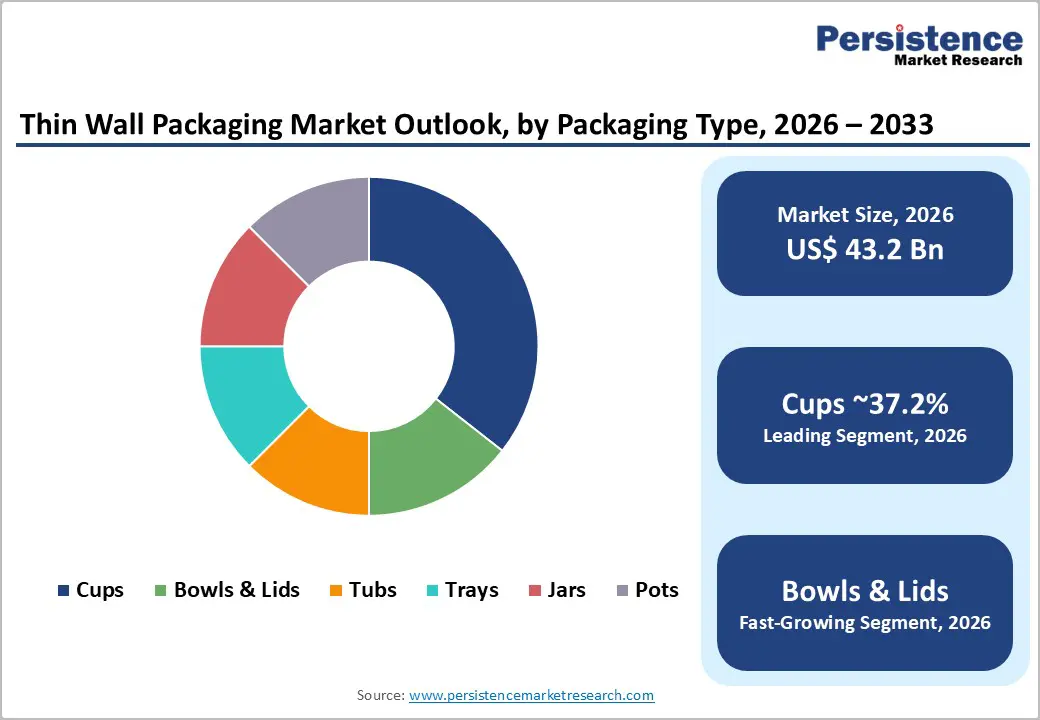

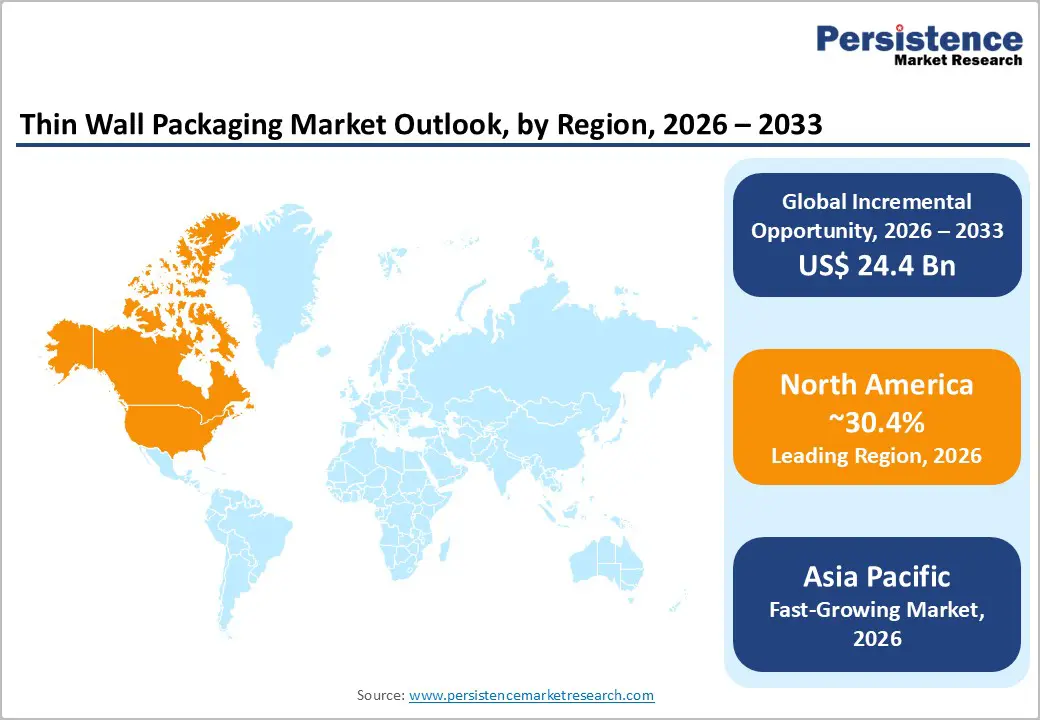

The global thin wall packaging market size is likely to be valued at US$43.2 billion in 2026 and is expected to reach US$67.6 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033, driven by the sustained shift toward lightweight, cost-efficient, and material-optimized packaging solutions across food, personal care, and pharmaceutical end-use industries.

Rising packaged food consumption, regulatory pressure to reduce plastic intensity, and advances in injection molding and extrusion technologies continue to strengthen adoption.

Key Industry Highlights

- Leading Region: North America, to account for 30.4% of global market share, driven by advanced food processing infrastructure, high adoption of automated injection molding, and strong private-label food demand across the U.S. and Canada.

- Fastest-growing Region: Asia Pacific, to register the highest regional growth rate globally, supported by rapid urbanization, expansion of packaged food consumption, and capacity additions across China, India, and ASEAN manufacturing hubs.

- Investment Plans: Capacity expansion and automation upgrades remain the primary investment focus, with leading converters allocating capital toward high-speed injection molding lines, high-cavitation tooling, and energy-efficient machinery, particularly in North America and Asia Pacific, to support cost leadership and volume scalability.

- Dominant Packaging Type: Cups, to hold 37.2% revenue share, supported by extensive usage in dairy, beverages, and ready-to-eat foods, along with compatibility with high-throughput automated filling systems.

- Leading Material: Polypropylene (PP), to represent 44.6% revenue share, due to its superior balance of rigidity, heat resistance, and regulatory acceptance for food contact, and well-established recycling infrastructure.

| Key Insights | Details |

|---|---|

| Thin Wall Packaging Market Size (2026E) | US$43.2 Bn |

| Market Value Forecast (2033F) | US$67.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Lightweight and Material-Efficient Packaging

The thin wall packaging industry benefits directly from global initiatives aimed at material reduction and packaging weight optimization. According to the European Commission and U.S. Environmental Protection Agency (EPA), lightweight packaging can reduce raw material usage by 20-30% per unit, lowering logistics emissions and resin costs. Food and beverage manufacturers increasingly adopt thin wall cups, tubs, and trays to meet sustainability targets without compromising functionality. This structural shift improves supply-chain efficiency, lowers transportation costs, and enhances shelf competitiveness, reinforcing long-term demand across mass-consumption categories.

Growth in Packaged and Convenience Food Consumption

Urbanization, dual-income households, and changing dietary habits have driven sustained growth in packaged foods. Data from FAO and national food safety authorities indicate that packaged food volumes in Asia Pacific and North America are growing at 5-7% annually. Thin wall packaging, particularly injection-molded cups and tubs, supports high-volume, high-speed filling operations essential for dairy, ready meals, and frozen foods. This compatibility with automated production lines positions thin wall packaging as a preferred solution for large FMCG manufacturers.

Advancements in High-Speed Molding Technologies

Technological improvements in injection molding cycle times, multi-cavity molds, and energy-efficient machinery have improved production economics. Industry associations such as SPE and PlasticsEurope report productivity gains of 15-20% per molding line over the last decade. These advancements allow manufacturers to maintain margins despite resin price volatility, making thin wall packaging scalable for both developed and emerging markets.

Barrier Analysis - Regulatory Pressure on Single-Use Plastics

While thin wall packaging reduces material usage, it remains exposed to single-use plastic regulations. The EU Single-Use Plastics Directive and similar policies in Canada and parts of Asia impose restrictions or extended producer responsibility (EPR) costs. Compliance can increase packaging costs by 5-12%, particularly for small and mid-scale converters, creating entry barriers and slowing adoption in highly regulated markets.

Volatility in Polymer Raw Material Prices

Thin-wall packaging predominantly uses polypropylene and PET resins, which are sensitive to fluctuations in oil prices and potential supply disruptions. Data from the World Bank commodity outlook indicate that polymer prices have experienced year-on-year volatility of approximately ±25% in recent cycles. This price instability puts pressure on converters’ margins, particularly those bound by long-term supply agreements, restricting their ability to adjust pricing and invest in capacity expansion.

Opportunity Analysis - Rapid Adoption of Biopolymer-Based Thin Wall Packaging

Biopolymers represent a high-growth opportunity as governments and brand owners pursue recyclable and bio-based materials. Industry data from European Bioplastics indicates biopolymer demand growth of over 8% CAGR, aligning with thin wall packaging requirements for rigidity and lightweight performance.

Expansion in Emerging Asian and ASEAN Markets

Asia Pacific offers substantial upside due to rising middle-class populations and expanding food retail infrastructure. According to World Bank urbanization data, over 250 million consumers are expected to enter urban consumption brackets by 2030. Thin wall packaging adoption in India, Indonesia, and Vietnam remains below North American penetration levels, presenting scalable growth opportunities for global converters.

Smart and Functional Packaging Integration

Integration of barrier coatings, tamper-evidence, and smart labeling into thin wall formats enhances value propositions. Industry pilots supported by packaging technology institutes indicate shelf-life extensions of 10-15% when advanced barrier solutions are used, creating premiumization opportunities for converters.

Category-Wise Analysis

Packaging Type Insights

Cups are estimated to lead, accounting for 37.2% of the revenue share in 2026, reflecting their critical role in high-volume food and beverage applications. They are widely used for dairy products (such as yogurt, sour cream, and desserts), beverages, and ready-to-eat foods, where efficiency, consistent wall thickness, and dimensional precision are essential. Injection-molded cups allow manufacturers to reduce resin usage by 20-30% per unit compared to conventional rigid containers while maintaining structural integrity. Major dairy processors in North America and Europe, including private-label yogurt producers and multinational FMCG companies, rely on thin-wall cups to operate high-speed filling lines exceeding 60,000 units per hour, enhancing throughput and operational efficiency. Compliance with food contact regulations and compatibility with polypropylene (PP) recycling streams further support the continued dominance of cups in both developed and emerging markets.

Bowls and lids are expected to be the fastest-growing packaging type, expanding at a CAGR of 7.9%, driven by the surge in ready meals, takeaway food, and premium convenience packaging. Growth is especially strong in urban centers where food delivery platforms and quick-service restaurants demand lightweight yet durable containers suitable for hot and semi-liquid foods. Thin-wall bowls with integrated lids are increasingly adopted by meal kit providers and cloud kitchens to improve portion control, stackability, and brand presentation. For instance, ready-meal brands in Western Europe and East Asia are transitioning from thermoformed trays to injection-molded thin-wall bowls to achieve superior heat resistance and leak prevention. Innovations in multi-layer structures and enhanced lid-seal designs have further improved thermal performance and visual appeal, positioning bowls and lids as a key growth driver within the packaging segment.

Material Insights

Polypropylene (PP) is anticipated to lead, accounting for a revenue share of 44.6% in 2026, supported by its optimal balance of rigidity, heat resistance, lightweight properties, and recyclability. PP remains the material of choice for injection-molded thin wall cups, tubs, and lids used in food, pharmaceutical, and nutraceutical packaging. Its ability to withstand hot-fill processes and microwave heating makes it particularly suitable for dairy products and ready meals. Regulatory approval for food contact across the U.S. FDA and European Food Safety Authority (EFSA) frameworks further strengthens PP’s position. Large-scale converters supplying multinational food brands favor PP due to its stable supply base, established recycling infrastructure, and compatibility with downgauged designs, allowing manufacturers to meet sustainability targets without major capital reconfiguration.

Biopolymers are likely to be the fastest-growing material segment, reflecting accelerating sustainability commitments from brand owners and tightening environmental regulations. Adoption is most pronounced in Europe and North America, where retailers and consumer goods companies face regulatory scrutiny under extended producer responsibility (EPR) schemes and plastic reduction mandates. Bio-based PP, PLA, and blended biopolymer solutions have seen significant improvements in impact strength, thermal stability, and processability, enabling their use in thin wall injection molding applications previously dominated by fossil-based resins. For example, premium yogurt and organic food brands in Germany and the U.K. have introduced biopolymer thin wall cups to reinforce eco-label positioning. This segment is particularly attractive for premium, private-label, and sustainability-driven brands, although cost premiums and limited recycling infrastructure remain adoption constraints in price-sensitive markets.

Regional Insights

North America Thin Wall Packaging Market Trends - Downgauging-Driven Growth in High-Throughput Food Packaging

North America is anticipated to lead with a market share of 30.4% in 2026, underpinned by a highly developed food processing ecosystem, advanced packaging automation, and strong alignment between sustainability goals and industrial capabilities. The U.S. accounts for the majority of regional demand, driven by high per-capita consumption of packaged dairy products, frozen foods, ready meals, and convenience snacks. According to data from the U.S. Department of Agriculture (USDA), over 70% of food consumed in U.S. households is processed or packaged, reinforcing structural demand for thin wall containers such as cups, tubs, and trays.

A defining feature of the North America market is the regulatory emphasis on recyclability and source reduction, rather than outright bans on plastic packaging. Policies promoted by the U.S. Environmental Protection Agency (EPA) and state-level packaging EPR programs encourage downgauging and material efficiency, conditions that directly favor thin wall packaging formats. As a result, major FMCG brands such as Danone North America, General Mills, and Kraft Heinz continue to redesign packaging toward thinner, injection-molded PP cups and containers rather than shifting away from plastics entirely.

Automation and high-speed molding adoption represent a key growth driver. Leading packaging converters such as Berry Global, Silgan Plastics, and IPL Plastics have expanded thin wall injection molding capacity across the Midwest and Southeast U.S. regions that offer proximity to food manufacturing hubs and cost-efficient logistics.

For example, Berry Global has publicly emphasized investments in high-cavitation molds and energy-efficient presses to support private-label dairy and foodservice customers, enabling higher throughput and consistent quality. These investments support retailers such as Walmart, Kroger, and Costco, whose private-label food brands increasingly rely on thin wall packaging for margin optimization. Overall, North America’s leadership position reflects a mature yet innovation-driven market, where technological upgrades, sustainability-aligned regulation, and private-label growth reinforce steady demand rather than short-term volume spikes.

Europe Thin Wall Packaging Market Trends - EU Regulation-Led Lightweighting and Mono-Material Transition

Europe represents a mature but regulation-led and innovation-intensive market, with Germany, the U.K., France, and Spain acting as primary demand and technology centers. The region’s growth is shaped by harmonized EU regulatory frameworks, particularly the EU Packaging and Packaging Waste Regulation (PPWR), which prioritizes lightweighting, recyclability, and circular material flows. These policies have accelerated the transition from thicker rigid packaging to thin wall formats, especially in food and dairy applications.

Germany functions as the regional manufacturing and technology hub, supported by strong engineering expertise and close collaboration between packaging converters, machinery suppliers, and resin producers. Companies such as Greiner Packaging and Jokey Group play a central role in advancing thin wall container design, particularly for yogurt, spreads, and ready meals.

German retailers and dairy brands increasingly favor thin wall PP and mono-material solutions to comply with recycling mandates under the country’s VerpackG (Packaging Act). The U.K. market is more redesign-driven, influenced by plastic taxes and retailer-led sustainability commitments. Major retailers such as Tesco, Sainsbury’s, and Marks & Spencer have pushed suppliers to reduce plastic weight per unit, directly benefiting thin wall packaging adoption. In response, converters supplying the U.K. market have focused on downgauged cups and tubs with enhanced stiffness, often replacing multi-material structures with recyclable mono-PP formats.

Asia Pacific Thin Wall Packaging Market Trends - Urbanization-Fueled Expansion in Cost-Efficient Food Containers

Asia Pacific is likely to be the fastest-growing regional market for thin wall packaging, driven by rapid urbanization, rising disposable incomes, and the expansion of organized food retail and foodservice sectors. China, India, Japan, and ASEAN economies collectively account for the bulk of growth, supported by large populations transitioning toward packaged and convenience foods. World Bank urbanization data indicates that Asia Pacific continues to add tens of millions of new urban consumers annually, directly expanding the addressable market for thin wall food containers.

China leads the region in production capacity and export-oriented manufacturing, supported by a dense network of injection molding and extrusion facilities. Domestic food brands and multinational FMCG companies operating in China increasingly use thin wall packaging to reduce costs and improve logistics efficiency. Large dairy and ready-meal producers favor injection-molded PP cups and tubs for their compatibility with high-speed filling lines and cold-chain distribution.

India and Southeast Asia represent the strongest consumption growth engines, driven by packaged dairy, instant foods, and takeaway meals. Indian dairy cooperatives and private brands have steadily shifted from heavier rigid containers to thin wall cups to reduce resin usage and transportation costs. In ASEAN markets such as Indonesia, Vietnam, and Thailand, the rapid rise of food delivery platforms and modern retail chains has accelerated demand for bowls, lids, and trays with improved stackability and leak resistance.

Regulatory frameworks across Asia Pacific remain heterogeneous, with most governments balancing sustainability goals against affordability and industrial growth. While plastic restrictions exist in select urban centers, many countries prioritize material reduction over bans, creating favorable conditions for thin wall packaging adoption. Reflecting this demand outlook, multinational packaging companies such as Amcor, Huhtamaki, and Berry Global have expanded local manufacturing footprints or entered joint ventures to serve regional FMCG clients more efficiently.

Competitive Landscape

The global thin wall packaging market is moderately fragmented, with the top five players accounting for approximately 35-40% of global revenue. These companies benefit from global manufacturing footprints, proprietary mold designs, and long-term supply contracts with multinational FMCG and foodservice brands, which create high entry barriers for smaller competitors. Scale advantages allow leading players to absorb resin price volatility, invest in advanced tooling, and maintain consistent quality across large production volumes. Market leaders compete primarily on operational efficiency and technical capability rather than pricing alone.

Investments in high-cavitation injection molds, automation, and energy-efficient machinery enable lower per-unit costs and tighter dimensional tolerances, critical for thin wall applications. Large converters leverage their R&D capabilities to support packaging redesign initiatives for brand owners, including downgauging, mono-material structures, and improved recyclability. This consultative approach strengthens customer retention and reinforces long-term contractual relationships.

Key Industry Developments

- In March 2025, LyondellBasell introduced Pro-fax EP649U, a novel high-flow polypropylene impact copolymer specifically designed to improve thin wall injection molding speed, efficiency, and output quality for food packaging production.

Companies Covered in Thin Wall Packaging Market

- Amcor plc

- Berry Global Group, Inc.

- Greiner Packaging International GmbH

- Silgan Holdings Inc.

- Huhtamaki Oyj

- Paccor GmbH (Coveris Rigid)

- Double H Plastics, Inc.

- ILIP S.r.l.

- Sem Plastik Sanayi ve Ticaret A.S.

- Groupe Guillin

- Omniform Group

- Plastipak Industries Inc.

- Acmepak Plastic Packaging

- EVCO Plastics

- Sunrise Plastics

Frequently Asked Questions

The thin wall packaging market is estimated to be valued at US$ 43.2 billion in 2026.

By 2033, the thin wall packaging market is forecast to reach US$ 67.6 billion.

Key trends shaping the thin wall packaging market include lightweight and down gauged packaging designs, increasing use of automation and high-speed injection molding, rising adoption of recyclable and mono-material formats, and growing interest in biopolymer-based thin wall solutions, particularly in Europe and North America.

Cups are the leading packaging type, accounting for 37.2% market share, primarily due to their widespread use in dairy products, beverages, and ready-to-eat food applications.

The thin wall packaging market is projected to grow at a CAGR of 6.6% between 2026 and 2033.

Major players include Berry Global Group, Amcor plc, Greiner Packaging, Huhtamaki Oyj, and Silgan Holdings.