- Nutraceuticals & Functional Foods

- Astaxanthin Market

Astaxanthin Market Size, Share, and Growth Forecast, 2025 - 2032

Astaxanthin Market By Source (Natural, Synthetic, Fermentation/Yeast), Application (Aquaculture & Animal Feed, Nutraceuticals, Others), Form, and Regional Analysis for 2025 - 2032

Astaxanthin Market Size and Trends Analysis

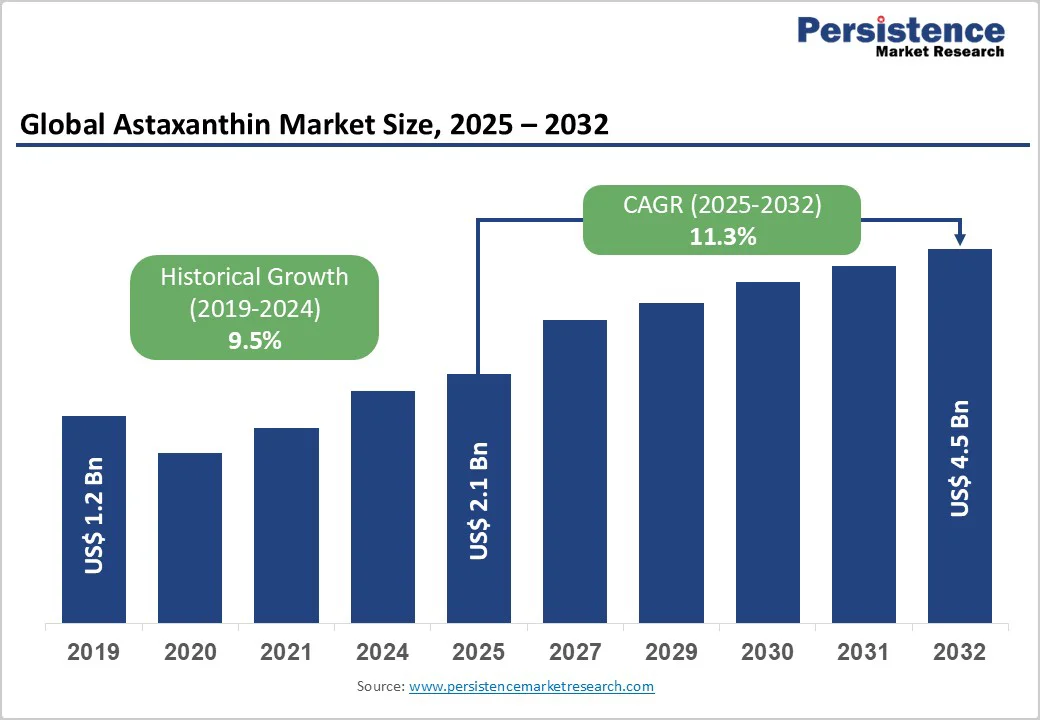

The global astaxanthin market size is likely to be valued at US$2.1 Billion in 2025 and is expected to reach US$4.5 Billion by 2032, growing at a CAGR of approximately 11.3% during the forecast period from 2025 to 2032, driven by rising nutraceutical demand fueled by its well-documented antioxidant properties, increasing use in cosmetics for skin-health benefits, and sustained utilization in aquaculture and animal feed for pigmentation and overall health performance.

Supply-side advances, such as higher-concentration oleoresins, improved beadlet systems, and more efficient microalgae cultivation, are reducing costs and expanding applications. Growing regulatory approvals are further widening market potential, though price volatility and reliance on limited raw-material sources remain near-term challenges.

Key Industry Highlights

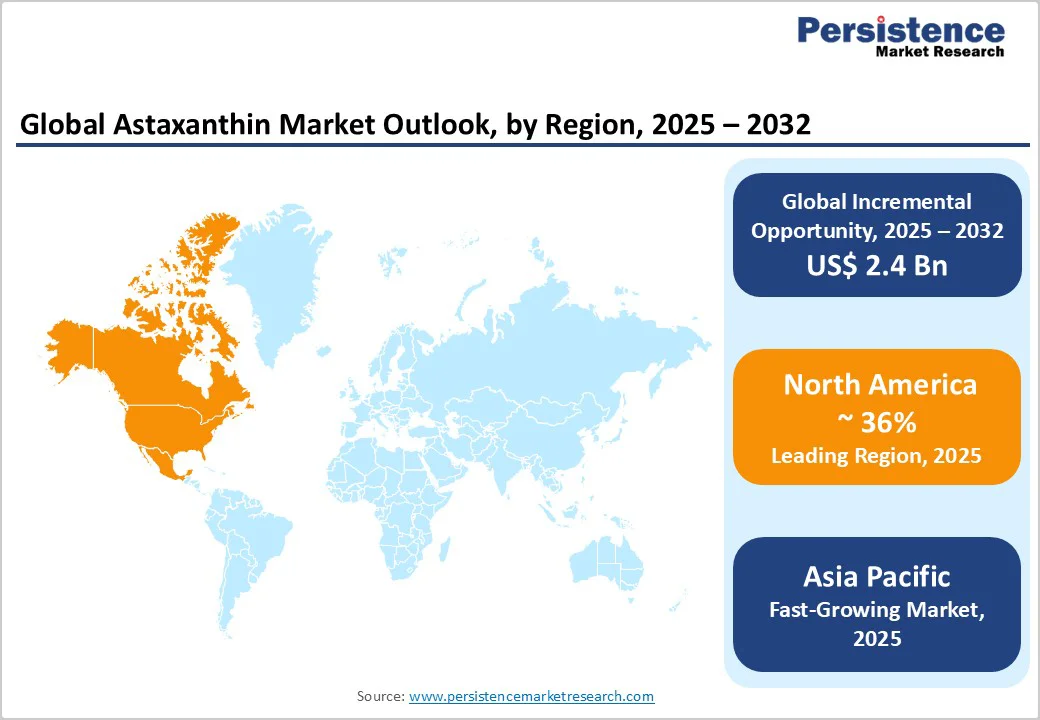

- Leading Region: North America accounts for the largest share of global astaxanthin consumption, contributing around 36% of total market value, driven by strong nutraceutical penetration and well-established retail channels.

- Fastest-growing Region: Asia Pacific is expanding at the quickest pace, supported by rising aquaculture output, increased supplement adoption, and innovative cosmetic formulations across China, Japan, and Southeast Asia.

- Investment Plans: Global producers are accelerating investments in microalgae cultivation, including photobioreactor upgrades, sustainability-focused facilities, and partnerships for encapsulation technologies, with several expansions announced across the U.S., Europe, and Asia between 2024 and 2025.

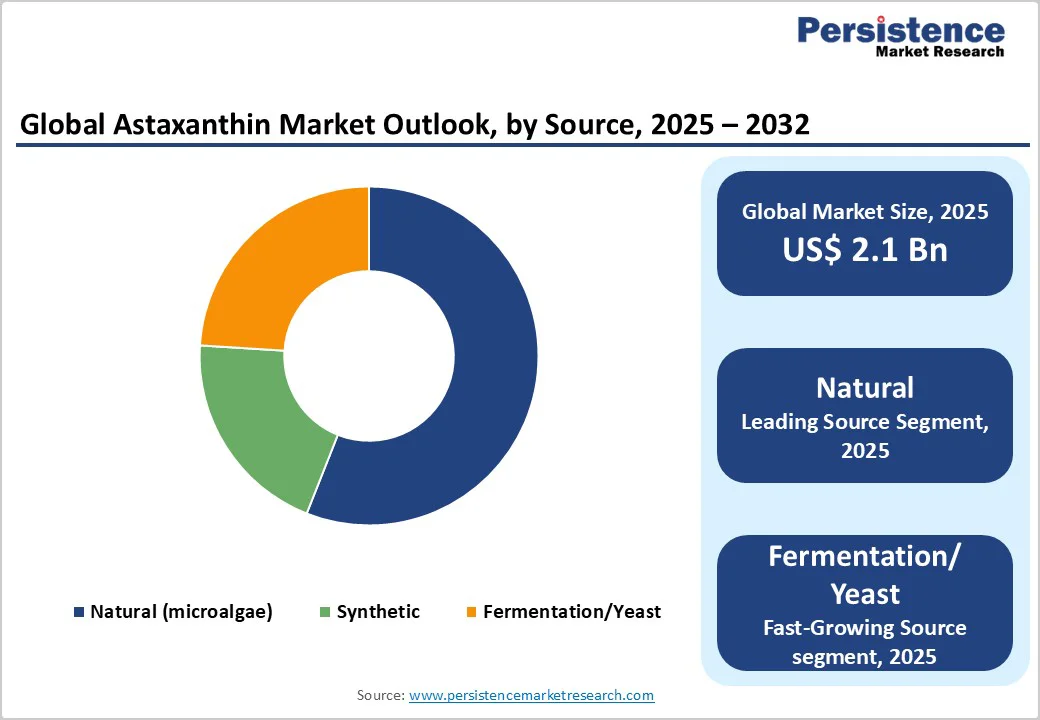

- Dominant Source: Natural astaxanthin maintains dominance holding a market share of 56%, due to clean-label preferences, renewable-energy cultivation, and strong adoption in premium nutraceuticals.

- Leading Application: Aquaculture remains the largest application segment accounting for 44% of market share, supported by its essential role in pigmentation and immune performance in salmon, trout, and shrimp.

| Key Insights | Details |

|---|---|

|

Astaxanthin Market Size (2025E) |

US$2.1 Bn |

|

Market Value Forecast (2032F) |

US$4.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

11.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expanding Nutraceutical and Cosmetic Demand

Growing consumer preference for clinically supported antioxidants is accelerating astaxanthin adoption in dietary supplements and topical skincare. Manufacturers have introduced higher-strength oleoresins, concentrated beadlets, and customized formulations to meet premium retail demand. The clean-label movement, combined with strong consumer acceptance of natural carotenoids, supports higher price realization. This has strengthened the value share of nutraceutical and cosmetic channels, making them central to long-term growth.

Aquaculture and Animal Feed Requirements

Astaxanthin remains an essential ingredient in aquaculture due to its role in pigmentation and animal performance, particularly in salmonid farming. Feed manufacturers rely on a consistent, large-volume supply, making this segment the most stable volumetric consumer of astaxanthin. The predictable demand from aquafeed provides producers with a reliable offtake, enabling investment in production scale, improved cultivation systems, and manufacturing efficiencies.

Production Innovation & Sustainability Focus

Producers are deploying advanced photobioreactors, closed-loop microalgae systems, and renewable-energy-powered operations to improve yield and reduce production costs. New high-concentration oleoresins and beadlet technologies enable smaller dosage formats, better stability, and more efficient supply chains. Sustainability certifications and environmentally responsible production practices help suppliers differentiate products in both feed and human-consumption markets.

Barrier Analysis - Price Volatility & High Production Costs

Natural astaxanthin production, particularly from Haematococcus pluvialis, is resource-intensive and sensitive to energy costs, climatic variations, and cultivation efficiencies. Fluctuations in these input factors can lead to inconsistent yields and higher final prices. Manufacturers of supplements and functional foods face compressed margins during periods of supply tightness, limiting rapid penetration in cost-sensitive categories.

Regulatory Complexity across Regions

Regulatory frameworks governing astaxanthin vary widely across jurisdictions. Differences in permitted uses, daily intake limits, labeling requirements, and color-additive regulations create barriers for product harmonization. This fragmentation slows product-launch cycles and raises compliance costs, especially for applications such as fortified foods or novel dosage forms.

Opportunity Analysis - High-Value Human Nutraceuticals & Personalized Wellness

Even modest shifts of astaxanthin volumes from aquafeed to human-use nutraceuticals can significantly enhance overall market value due to higher selling prices in the supplement and skincare industries. Premium formulations emphasizing bioavailability, antioxidant potency, or stress-modulation benefits present substantial margin opportunities. Brands focusing on targeted benefits and personalized nutrition platforms can unlock new consumer demographics.

Advanced Formulation Technologies & Sustainable Branding

High-concentration oleoresins, microencapsulated beadlets, and multi-layer delivery systems support better stability and enhanced bioavailability. If such formats achieve even mid-range adoption in supplement portfolios by the late 2020s, the incremental market value could be considerable. Sustainable sourcing, traceable production, and co-branded ingredient partnerships offer additional levers for differentiation and price premium.

Category-wise Analysis

Source Insights

Natural astaxanthin sourced from Haematococcus pluvialis microalgae continues to dominate, holding a market share of 56%, due to its strong alignment with clean-label and plant-derived ingredient preferences. Its high antioxidant potency and robust scientific validation have reinforced its role in premium nutraceuticals, skincare, and functional beverage formulations. Companies such as AstaReal, Cyanotech, and Algalif have expanded microalgae cultivation capacities using closed photobioreactor systems and low-carbon, renewable-energy inputs. These controlled-environment facilities improve purity, limit contamination risks, and help producers meet stringent safety requirements for human consumption. The segment benefits from rising demand for non-synthetic antioxidants and sustainability-centered branding.

Fermentation- and yeast-derived astaxanthin, along with enhanced natural variants, are experiencing the fastest growth due to biotechnology improvements that reduce cost volatility and enhance consistency. Innovations in precision fermentation, strain engineering, and high-density bioreactors have enabled companies such as Kerry Group (through biotechnology platforms) and emerging biotech firms to achieve superior yields and improved stability profiles. Fermentation-based production offers reliable scalability independent of climatic variability, making it attractive for high-volume nutraceutical and cosmeceutical markets. At the same time, enhanced natural formats, such as microencapsulated natural astaxanthin and water-dispersible oleoresins, support product developers seeking improved bioavailability. These advancements help manufacturers serve premium supplement brands and dermo-cosmetic lines that require consistent potency and traceable supply chains.

Application Insights

Aquaculture continues to be the largest application segment by volume as astaxanthin is essential for pigmentation, oxidative stress management, and immune function in salmon, trout, shrimp, and other species. Large feed producers such as Skretting, BioMar, and Mowi Feed remain major buyers, relying on both synthetic and natural sources depending on cost structures and country-specific regulations. In regions with strict sustainability or labeling requirements, producers increasingly trial natural variants, although synthetic formats remain dominant due to their pricing advantages and supply reliability. The rising intensification of fish farming and the expansion of salmonid cultivation in Norway, Chile, and Canada support stable long-term demand, while feed formulators emphasize consistent performance and predictable nutrient delivery.

Nutraceuticals and cosmetics represent the fastest-growing value segment, driven by expanding consumer interest in cellular health, antioxidant protection, skin elasticity, and anti-inflammatory support. Brands such as BioAstin, NOW Foods, and various K-beauty players have launched high-purity astaxanthin capsules, softgels, and topical formulations that leverage its well-documented antioxidant activity. Skincare manufacturers are incorporating astaxanthin into serums, emulsions, and sun-protection blends due to its photoprotective potential and compatibility with retinoids and vitamin C. Advances in encapsulation, such as sustained-release beadlets and cold-water dispersible ingredients, enable higher active concentrations and better stability in finished products. These innovations are raising average selling prices and shifting production priorities toward human-use segments with stronger margins.

Product Form Insights

Oleoresin remains the leading form in commercial applications due to its versatility, especially in softgel and liquid supplement manufacturing. Extracts produced through CO2 or solvent extraction are widely accepted in regulatory frameworks across North America, Europe, and Asia, enabling broad global commercialization. Companies such as AstaReal and Algatechnologies supply oleoresin in standardized concentrations that integrate easily into feed formulations and high-volume supplement production lines. The format’s compatibility with lipid-based delivery systems results in favorable bioavailability profiles, making it a preferred choice for human health brands targeting antioxidant, cardiovascular, and skin-health applications.

Beadlets and advanced concentrated forms are gaining momentum due to superior handling, improved stability during storage and transport, and greater dose efficiency per capsule or sachet. Controlled-release beadlet technologies offered by ingredient manufacturers such as DSM-Firmenich and specialized encapsulation suppliers provide enhanced protection against oxidation and heat exposure. These formats are also advantageous for tablet compression, stick-pack products, and functional foods where stable dispersion is essential. High-concentration formats, including microencapsulated powders and ultra-potent beadlets, support premium supplement offerings and emerging cosmetic formulations. As formulation flexibility increases, demand for these formats continues to accelerate among global nutraceutical and beauty-from-within brands.

Regional Insights

North America Astaxanthin Market Trends - Clinical-Backed Nutraceutical Growth & Sustainability-Driven Microalgae Innovation

North America remains the leading market with a share of 36%, with the U.S. serving as the core demand center due to strong nutraceutical penetration, mature retail distribution, and a well-developed product-development ecosystem. High-purity softgels, beadlets, and topical formulations gain steady traction through supplement retailers, online wellness platforms, and premium skincare brands. Aquaculture maintains a stable consumption base, especially in Pacific Northwest salmon farming, while ongoing U.S. clinical research related to eye health, photoprotection, and metabolic wellness reinforces product credibility.

The regulatory landscape under DSHEA supports rapid commercialization of new formulations, though restrictions in certain feed and food-colorant applications continue to shape sourcing and product strategies. The competitive environment features global ingredient suppliers, natural-astaxanthin specialists, and an active nutraceutical industry that incorporates astaxanthin into antioxidant and skin-health blends. Recent developments include AstaReal’s July 2024 expansion of its U.S. formulation support center, the February 2025 launch of an astaxanthin-collagen supplement using advanced beadlet technology, and a late-2024 solar-powered photobioreactor upgrade by an Arizona microalgae producer to reduce energy intensity and improve sustainability.

Europe Astaxanthin Market Trends - Premium Beauty-from-Within Demand & Low-Carbon, Traceable Production Expansion

Europe represents a high-value, premium-focused market driven by strong demand for science-backed nutraceuticals, ingestible beauty solutions, and advanced dermocosmetics. Western Europe leads adoption across supplements and beauty-from-within products, while Northern Europe sustains substantial aquaculture-related demand for salmon, trout, and shellfish. Harmonized EFSA regulations and updated authorizations for carotenoid-rich oleoresins have expanded innovation opportunities in supplement and fortified-food applications.

European buyers emphasize sustainability, lifecycle assessments, and transparent supply chains, positioning low-carbon and traceable astaxanthin sources favorably. The competitive landscape includes natural-astaxanthin suppliers, Icelandic and Nordic microalgae innovators, and global formulation specialists supporting premium product development. Notable recent developments include Algalif’s March 2024 expansion of closed photobioreactor capacity in Iceland, the September 2024 launch of a French anti-pollution serum using certified low-carbon natural astaxanthin, and a June 2025 shift by a Nordic aquafeed producer toward natural astaxanthin to meet retailer-driven sustainability standards.

Asia Pacific Astaxanthin Market Trends - Fast-Growth Aquaculture Demand & Diversified Regulatory-Driven Product Innovation

Asia Pacific is the fastest-growing region for astaxanthin, driven by expanding aquaculture activity, rising disposable incomes, and increasing awareness of antioxidant and skin-health benefits. China is both a major consumer and an emerging producer, supported by growth in synthetic and natural production and strong domestic demand in aquafeed and beauty-from-within categories. Japan remains a leading innovator, with cosmetic and supplement companies adopting combination formulations supported by the Foods with Function Claims (FFC) system. India and Southeast Asia show fast growth in lifestyle-oriented supplements, functional beverages, and wellness products distributed through modern retail and e-commerce.

Regulatory diversity across the region requires tailored commercialization strategies, with China’s evolving NDI framework and Japan’s FFC system enabling more advanced product formats. Investment flows support new microalgae farms in South Korea and China, manufacturing partnerships serving regional supplement brands, and the build-out of export-oriented facilities supplying North American and European markets. Recent developments include a major Chinese biotech firm launching a fermentation-based astaxanthin plant in April 2024, a January 2025 release of an FFC-compliant Japanese astaxanthin UV-protection cream, and an August 2024 Indian, ASEAN partnership securing a long-term natural astaxanthin supply for antioxidant supplements.

Competitive Landscape

The global astaxanthin market is semi-consolidated, with a blend of natural microalgae producers, synthetic-production companies focused on feed applications, and global ingredient houses offering extensive distribution. Natural astaxanthin commands premium prices while synthetic forms supply cost-efficient solutions for high-volume feed customers. Competitive advantage stems from vertical integration, strong regulatory capabilities, and advanced formulation technologies.

Leading suppliers focus on premiumization, sustainability, vertical integration, and formulation innovation. Long-term supply contracts, clinical-evidence programs, and regulatory-first product development are core strategic pillars.

Key Industry Developments

- In January 2025, BASF received regulatory approval in Europe for its fermentation-derived astaxanthin, paving the way for broader commercial use.

- In April 2024, Divi’s Nutraceuticals and Algalif launched AstaBead, a 5% natural astaxanthin beadlet (cold-water dispersible and compressible), for use in gummies, tablets, powders, and food fortification.

Companies Covered in Astaxanthin Market

- DSM-Firmenich

- AstaReal

- Algatechnologies (Solabia Group)

- Algalif

- BASF

- Cyanotech Corporation

- Fuji Chemical Industries

- Divis Laboratories

- BlueOcean NutraSciences

- BGG World (Beijing Gingko Group)

- Parry Nutraceuticals

- Zhengzhou Debao

- Fenchem

- Cardax

- InnoBio

- Piveg

- Supreme Biotechnologies

- Igene Biotechnology

- Heliae Development

- Kemin Industries

Frequently Asked Questions

The astaxanthin market is valued at US$2.1 Billion in 2025.

By 2032, the astaxanthin market is projected to reach US$4.5 Billion.

Key trends include growing demand for science-backed nutraceuticals, premium ingestible beauty products, and rapid expansion of microalgae cultivation, sustainability-focused sourcing, and wider use of microencapsulation to improve stability in supplements and cosmetics.

The nutraceuticals segment represents the leading one, accounting for over 45% of global demand due to strong uptake across antioxidant, eye-health, and skin-health applications.

The astaxanthin market is expected to grow at a CAGR of 11.3% between 2025 and 2032, driven by expanding supplement consumption, rising aquaculture output, and increasing use in dermocosmetic formulations.

Major players with strong global portfolios include DSM-Firmenich, AstaReal, Algatechnologies (Solabia Group), Algalif, and BASF.