- Biotechnology

- Fibrin Glue Market

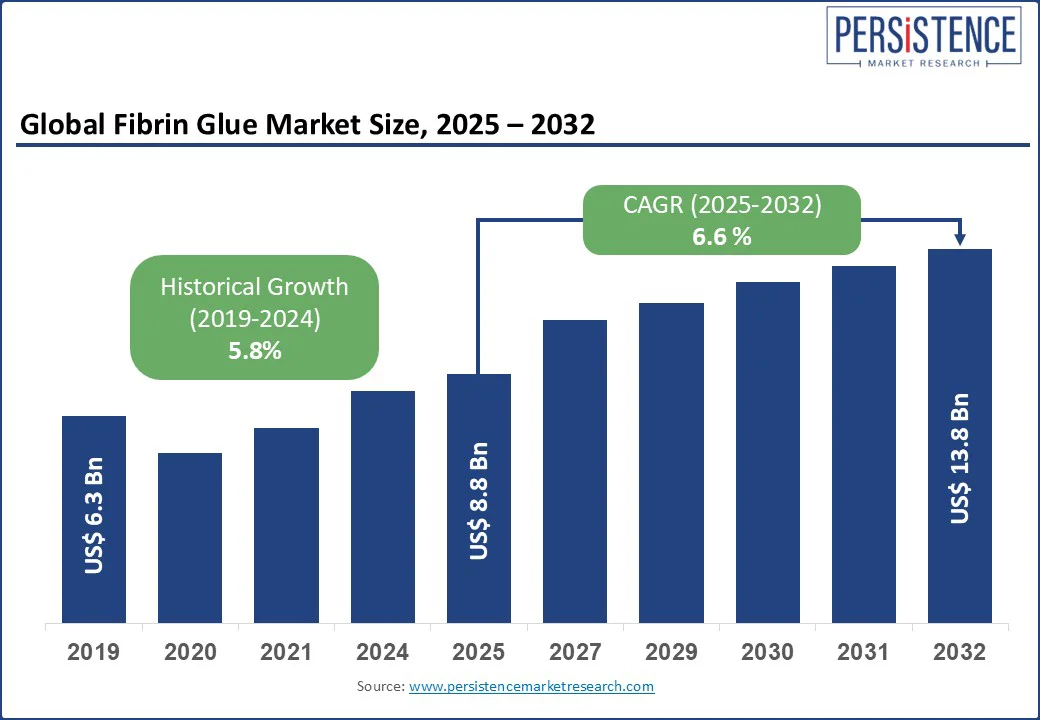

Fibrin Glue Market Size, Share, Trends, Growth, and Forecasts

Fibrin Glue Market By Product Type (Viral Inactivation, Autologous Donation, Recombinant Production, Others), Application (Hemostat, Adhesive, Sealant), End-Use (Cardiac Surgery, Pulmonary Surgery, Burn bleeding, Vascular surgeries, Orthopedic surgeries, Lacerations of liver and spleen, Neurosurgery, Plastic Surgery, General Surgery, Wound management), and Regional Analysis for 2025-2032.

Fibrin Glue Market Size and Forecast Analysis

Market Overview

The global fibrin glue market is likely to be valued at US$8.8 Bn in 2025, and reach US$13.8 Bn by 2032, driven by CAGR of 6.6% from 2025 to 2032. Fibrin glue, a type of biological adhesive composed of fibrinogen and thrombin, is widely used in surgical procedures to support surgical hemostasis, tissue adhesion, and sealing. This tissue glue is vital in cardiac, pulmonary, vascular, orthopedic, and neurosurgeries, as well as wound management and general surgery. Market growth is fueled by the increasing number of surgical procedures, advancements in biocompatible surgical adhesives, and rising demand for minimally invasive surgery. Leading companies focus on innovation, partnerships, and global expansion to meet growing demand.

Market Dynamics

Drivers

- Rising Demand for Minimally Invasive Surgeries Drives Fibrin Glue Market: The growing adoption of minimally invasive surgeries (MIS), such as laparoscopic and robotic-assisted procedures, is a major driver for the fibrin glue market. MIS techniques, known for reduced trauma, faster recovery, and minimal scarring, require precise hemostatic agents to control bleeding and promote tissue adhesion. Fibrin glue, derived from fibrinogen and thrombin, excels in these applications due to its biocompatibility and ability to accelerate wound healing. It is widely used in specialties such as cardiac, vascular, and orthopedic surgeries, where precision is critical.

For instance, a study published in Heliyon compared mesh fixation methods in laparoscopic hernia repair and found that glue fixation resulted in lower early postoperative pain, reduced chronic pain, and a lower incidence of hematoma compared to traditional methods. The study also noted that patients in the glue group returned to work sooner, highlighting the benefits of fibrin glue in enhancing recovery times in MIS.

As healthcare systems globally prioritize efficient, patient-centric procedures, fibrin glue’s versatility and effectiveness make it indispensable. Innovations in delivery systems, such as sprayable formulations, further boost its adoption, driving market growth as MIS continues to reshape surgical practices worldwide.

- Increasing Prevalence of Chronic Diseases Fuels Fibrin Glue Adoption: The rising global burden of chronic diseases—especially cardiovascular disease and cancer—is intensifying demand for surgical interventions, where effective hemostatic agents such as fibrin glue become indispensable. Cardiovascular diseases (CVDs) remain the leading cause of death worldwide, claiming approximately 17.9 million lives annually, accounting for nearly one-third of all global fatalities.

As the population ages and NCDs proliferate, more patients undergo cardiac and vascular surgeries, creating a growing need for rapid and reliable bleeding control. Fibrin sealants are particularly vital in reoperations, bypass grafts, and aortic dissection repairs, where they significantly reduce postoperative bleeding and the incidence of emergency resternotomy.

For instance, A multicenter U.S. trial found fibrin sealants achieved hemostasis within 5 minutes in 92.6% of cardiac reoperations versus just 12.4% with conventional agents, also lowering resternotomy rates from ~10% to 5.6%.

Such compelling clinical evidence, aligned with the growing volume of surgeries driven by chronic disease prevalence, enhances the adoption trajectory of fibrin glue in hospitals and surgical centers worldwide.

Restraint

- High Production Costs and Regulatory Challenges can hamper the market: The high cost of producing fibrin glue, particularly due to stringent purification processes to eliminate viral contamination risks from human or animal-derived sources, poses a significant restraint. Regulatory bodies such as the U.S. FDA require extensive clinical data for approval, increasing development costs and delaying market entry.

Opportunities

- Integration with Regenerative Medicine and Advanced Surgical Applications: One of the most promising opportunities for the fibrin glue market is its expanding role in regenerative medicine and tissue engineering. As healthcare systems evolve toward more personalized and advanced treatments, fibrin glue is being increasingly explored as a biocompatible scaffold for stem cells, growth factors, and tissue regeneration therapies.

Growth in Regenerative Medicine and Wound Healing Applications: The increasing adoption of fibrin glue in regenerative medicine and wound management presents a significant opportunity, particularly for chronic wound care and tissue regeneration. For instance, fibrin glue is used in treating diabetic ulcers, which affect 15% of diabetic patients globally (approximately 70 million people). Companies such as Baxter have developed fibrin-based products tailored for wound healing, such as Tisseel, which supports tissue sealing in burn treatment.

Category-wise Insights

Product Type Insights

- Recombinant Production dominated the fibrin glue market, fueled by advancements in biotechnology and increasing demand for safer, viral-free fibrin glue, particularly in advanced surgical settings. By utilizing genetically engineered proteins, recombinant fibrin glue eliminates the risk of viral transmission associated with plasma-derived products, making it ideal for high-risk applications such as cardiac and neurosurgery.

- Autologous donation is the fastest-growing product type, fueled by its use of patient-derived blood, which minimizes immune reactions and enhances safety. This segment is expected to grow rapidly due to the rising demand for personalized medical solutions, particularly in orthopedic and plastic surgeries. Advancements in autologous processing technologies further support this growth, with the segment projected to gain traction in regions with increasing surgical volumes.

Application Insights

- Hemostat applications lead, accounting for a significant share due to their critical role in controlling bleeding during cardiac surgery and vascular surgeries. Fibrin glue’s rapid clot formation and ability to reduce blood loss make it indispensable, with the global rise in surgical procedures reinforcing its dominance in this application.

- Sealant applications are the fastest-growing, driven by their increasing use in minimally invasive surgeries and wound management, offering effective tissue sealing and reduced complications. This application is critical in surgeries where maintaining a tight seal is essential to prevent complications such as postoperative bleeding, air leaks, or cerebrospinal fluid (CSF) leakage.

End-Use Insights

- Cardiac Surgery holds the largest share, driven by the high volume of procedures such as CABG, which require fibrin glue for hemostasis. Fibrin glue’s ability to manage bleeding and improve patient outcomes drives its dominance, with cardiac surgeries forming a significant portion of global surgical volumes.

Orthopedic Surgery is the fastest-growing end user, propelled by rising joint replacement and trauma surgeries, particularly among the aging population. Fibrin glue is employed in these procedures as a hemostat to control bleeding, an adhesive to secure grafts or implants, and a sealant to prevent fluid leakage or promote tissue healing

Regional Insights

North America Fibrin Glue Market Trends.

North America holds the largest market share at 42%, with the U.S. contributing over 80% of the region’s revenue.

- Advanced Healthcare infrastructure: The U.S. market is driven by advanced healthcare infrastructure, high surgical volumes (over 50 million procedures annually), and strong adoption of innovative fibrin glue products.

- R&D Investments: The presence of key players such as Johnson & Johnson and Baxter, coupled with significant R&D investments (e.g., US$ 12 billion in biotech R&D in 2024), supports market growth.

- Regulatory Support: Stringent FDA regulations ensure high product safety, boosting confidence and adoption across surgical specialties.

Europe Fibrin Glue Market Trends

In the Europe region the Germany, the U.K., and France are leading due to their advanced medical systems and high surgical demand.

- Germany: Germany’s advanced medical technology sector and high surgical volumes drive demand for fibrin glue in cardiac and orthopedic applications.

- France: Increasing healthcare expenditure and a focus on minimally invasive surgeries boost adoption in wound management and neurosurgery.

- UK: Emphasis on regulatory compliance and sustainable medical solutions supports market growth, particularly for recombinant fibrin glues.

Asia Pacific Fibrin Glue Market Trends

Asia Pacific is the fastest-growing region, led by China, India, and Japan.

- China: China’s healthcare infrastructure expansion and 15% annual surgical volume growth drive fibrin glue demand, supported by initiatives such as Healthy China 2030.

- India: Rising government healthcare investments and adoption of advanced surgical techniques fuel market growth.

Japan: A large aging population drives demand for fibrin glue in neurosurgery and wound management.

Competitive Landscape

The global fibrin glue market is highly competitive. Key Strategies include R&D investment for innovative products, such as recombinant and nanotechnology-based fibrin glues, to meet safety and efficacy demands. Companies such as Baxter and BD focus on strategic acquisitions to expand market share, while Shanghai RAAS and Hualan Biological Engineering target the Asia Pacific through localized production. Partnerships with hospitals and ASCs are also common to enhance product adoption.

Key Developments

Recent developments include Johnson & Johnson’s 2024 launch of a next-generation fibrin sealant with enhanced biocompatibility, and Baxter’s US$50 million investment in recombinant fibrin glue production. CSL Behring partnered with a Chinese biotech firm in 2023 to expand its presence in Asia Pacific, while Cryolife introduced a new hemostat for neurosurgery in 2024.

Companies Covered in Fibrin Glue Market

- Johnson & Johnson

- Baxter

- CSL Behring

- Shanghai RAAS

- Corza Health

- Marquee Biosurgical

- Hualan Biological Engineering

- Becton Dickinson and Company (BD)

- Cryolife

- Nordson Corporation

- Others.

Frequently Asked Questions

The Fibrin Glue market is projected to reach US$8.8 billion in 2025.

The rising prevalence of chronic diseases and the growing demand for minimally invasive surgeries are the key market drivers.

The Fibrin Glue market is poised to witness a CAGR of 6.6% from 2025 to 2032.

Advancements in recombinant fibrin glue and biodegradable formulations are the key market opportunities.

Johnson & Johnson, Baxter, CSL Behring, Shanghai RAAS, Corza Health, Marquee Biosurgical, Hualan Biological Engineering, Becton Dickinson and Company (BD), Cryolife, and Nordson Corporation are key market players.